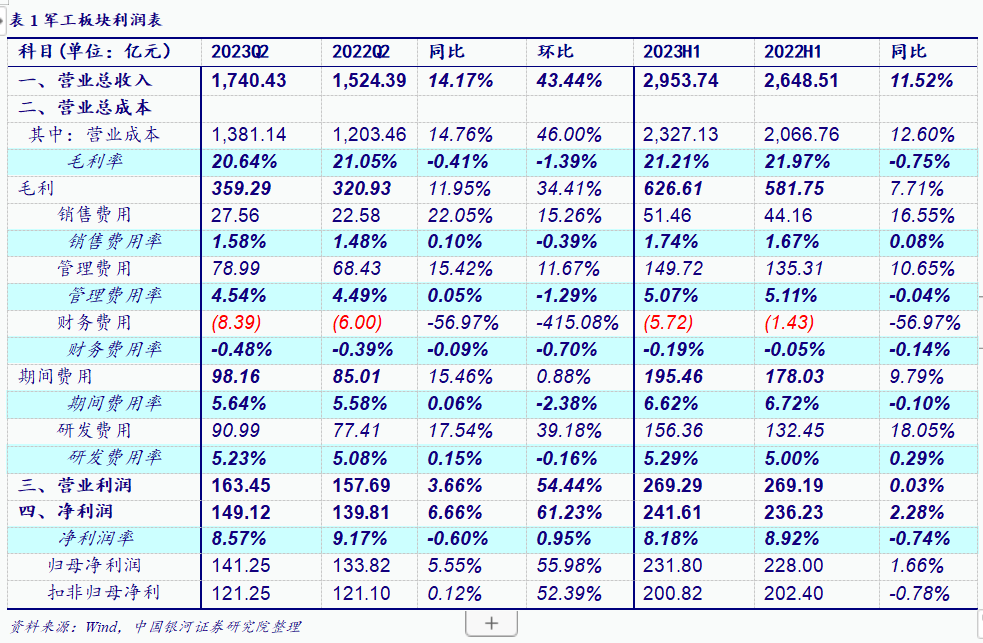

◆ The military sector increased revenue but not profit, lower than expected at the beginning of the year. 2023H1 military industry revenue of 295.374 billion yuan (YoY plus 11.52%), home-to-home net profit of 23.18 billion yuan (YoY plus 1.66%). 2023Q2 revenue of 174.043 billion yuan (YoY plus 14.17%), net profit of 14.125 billion yuan (YoY plus 5.55%), the growth rate was less than expected. The reason is that, first of all, due to macro factors such as medium-term adjustment, the newly signed orders have been affected to a certain extent. At the same time, the delivery and acceptance process of some products has been extended, and the revenue confirmation time has been delayed. Secondly, due to factors such as localization requirements, price reduction pressure and changes in VAT subsidy policies, the cost side has gone up. Thirdly, driven by the modernization of weapons and equipment, research and development costs have increased rapidly (YoY +18.05), and cost rate up 0.29pct; finally, accounts receivable and inventory hit a record high, resulting in high impairment losses, affecting the current profit of the sector.

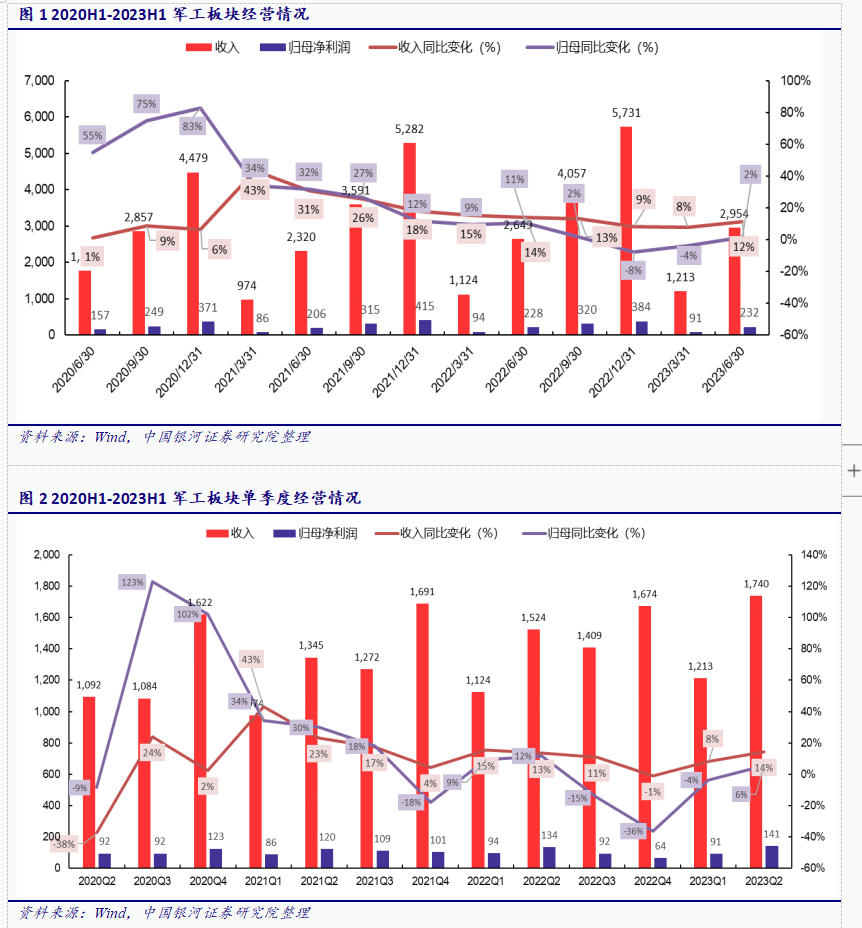

◆ In the full-year dimension, quarterly performance growth may be low before and high after. 2023Q1 performance growth rate of about -3.86, reversing the quarterly performance growth rate continued to decline, 2023Q2 performance growth rate of about 5.55, the month-on-month trend is accelerating. With the medium-term adjustment landing, Q4 orders will gradually become clear, the pre-delivery of goods (inventory transfer out) revenue recognition is expected to accelerate, Q4 sector performance year-on-year growth rate or step up. The full-year quarterly growth rate is expected to be low and high, with full-year revenue and non-return net profit increasing by 14% and 6%, respectively, in 2023.

◆ The main engine factory and the machine plus sub-plate performed brightly. 2023H1 military sub-sector revenue have achieved double-digit positive growth, midstream information technology, machine-plus sector performance, revenue growth of 20.4 and 20.9, respectively. On the profit side, the machine plus sector and the final assembly plant sector led the performance, with net profit growth of 34.5 and 29.2, respectively. In terms of the segmented track, the radar/communications/electronic warfare sub-sector performed better, with revenue and home-to-home net profit up 8.5 per cent and 35.9 per cent, respectively.

The time has come for the layout on the left, waiting for the east wind to sail again. [Profit Full + Waiting for Dongfeng] In the short term, first of all, valuation suppression factors such as uncertain industry orders, price cuts for key models, and weak Q3 performance expectations are basically priced in; Secondly, the mid-term adjustment Q3 of the five-year equipment procurement plan will fall to the ground, the order Q4 may be visible, and the improvement expectation of sector performance will be raised. The time has come for the left layout. [Volume and Price] "Volume" and "price" are two important factors affecting the performance of the military sector in the second half of the year. It is expected that the sector will rebound due to "volume" and the transparency of "price" will lag behind one earnings season. Although the rebound height is limited, it will not affect the rebound time point. At present, it should be moderately positive. [layout period] since the beginning of the year, the military sector has been fully adjusted, the left layout time has come, waiting for the east wind to set sail again, the "five-dimensional" configuration is recommended:

-Left layout target, Western Superconductivity, Triangle Defense, Ziguang Guoguangwei;

-New quality and new domain, including unmanned aerial vehicles, aerospace electronics, far-fire suppliers, northern navigation, radar/communications/electronic countermeasures core suppliers, Zhenlei Technology, Mengsheng Electronics, and military information security suppliers, Bangyan Technology;

-central enterprises reform beneficiaries, recommended AVIC Electronics, Tianao Electronics, Guorui Technology, Aviation Control and Aviation Materials shares, etc., pay attention to the aerospace department;

-Targets benefiting from localization, including Lunda, Zhenhua Scenery, etc.;

-Military trade beneficiaries, including Space South Lake, Space Rainbow, etc.

The risk of less than expected equipment procurement and industry capacity expansion.

Q4 will meet marginal improvement 1. to the volatility of the military industry

We regard the 157 listed companies of the state-owned enterprises of the military industry group as a whole, representing the military industry sector. Regardless of the related transaction factor, the profit statement and balance sheet of the military sector are obtained by simply adding up each account, and comparative analysis is carried out.

a brief analysis of (I) income statement: Q2 performance increased slightly year-on-year, gross margin under pressure

2023Q2 Military industry revenue achieved rapid growth, but gross margin and R & D expense ratio suppressed performance growth

2023H1 Military industry revenue was 295.374 billion yuan, up 11.52 percent year-on-year, and net profit attributable to the parent company was 23.18 billion yuan, up 1.66 percent year-on-year. In a single quarter, 2023Q2 military industry achieved revenue of 174.043 billion yuan, up 14.17 percent year-on-year, up 43.44 percent month-on-month, and net profit of 14.125 billion yuan, up 5.55 percent year-on-year and 55.98 percent month-on-month. The overall performance is that the growth rate is less than expected, and the increase in revenue does not increase profits. We think there are mainly the following reasons:

· Due to the medium-term adjustment and other macro factors, the overall performance of the industry for orders, bidding time delayed, new signing orders were affected to a certain extent. At the same time, some product deliveries and customer acceptance processes were extended, resulting in an increase in the revenue recognition cycle.

-Due to localization requirements, downstream price reduction pressure and changes in VAT subsidy policy, the industry's cost-side upward gross margin fell from 21.97 percent to 21.21 percent, down 0.75pct year-on-year.

-Driven by the modernization of weapons and equipment, the industry is paying more attention to the promotion of sustainable development by research and development, with faster growth in research and development costs (YoY +18.05%) and an upward 0.29 in cost rates.

-Accounts receivable and inventories increased by 48.12 and 8.86 respectively from the beginning of the period, a record high, resulting in high impairment losses, affecting the current profit of the military sector.

We believe that in addition to the above macro and industry factors, it is also affected by the high base in 2022.

month-on-month, the industry is growing rapidly, we believe that mainly due to seasonal fluctuations in revenue recognition in the military industry, the middle of the year, the end of the year is usually the order concentration confirmation period, so 2023Q2 revenue growth is larger (QoQ +43.44%), in line with the industry law. We believe that industry quarterly differences may narrow and inter-quarter comparability is expected to improve in the coming quarters as the group's balanced production plans advance. In addition, the growth rate of net profit is higher than the growth rate of revenue, which we believe is related to the industry's implementation of strict cost control in Q2 to improve quality and efficiency. 23Q2 Industry Period Cost Rate (excluding research and development) 5.64%, down 2.38pct month-on-month.

From the perspective of profitability, the gross profit margin of the sector has declined, and the ability to control expenses has improved

profit side, due to equipment demand volume overlay localization requirements to enhance, military enterprises "price for volume" into the general trend, components and other links of localization rate to enhance the squeeze in the lower and middle reaches of the gross margin, the industry gross margin has declined. Looking ahead, the scale effect brought about by mass production will gradually appear, while the upstream domestic parts volume, price decline is also conducive to the improvement of the gross margin in the middle and lower reaches. With the medium-term adjustment into the end, equipment demand can be released again, the next two years the industry's overall gross margin is expected to gradually bottom out, and reach a new steady-state level.

2023H1 period cost rate (excluding research and development costs) was 6.62 percent, down 0.10pct year-on-year, and cost control capacity continued to improve, with financial expenses down 56.97 percent year-on-year and financial expense rate down 0.14pct. 2023Q2 period cost rate (excluding research and development costs) 5.64 percent, up 0.06pct YoY, of which research and development costs increased significantly, research and development costs increased by 0.15pct YoY. The proportion of income from various expenses continued to decrease, indicating that the scale effect of the sector still exists and the ability to control expenses has been improved.

2023H1 industry research and development costs increased by 18.05 YoY, research and development costs rate of 5.29 percent, an increase of 0.29pct YoY, of which 2023Q2 research and development costs increased by 17.54 percent YoY, research and development costs rate of 5.23 percent, an increase of 0.15pct YoY. The growth of research and development expenses exceeded the growth rate of revenue in the same period, indicating that military enterprises attach importance to scientific and technological innovation, and the accumulation of research and development strength is expected to contribute to the continuous driving force for the future. In addition, in the context of the upward trend of the industry, the level of profitability of the sector has reached a record high, and the proportion of R & D expenditure of most enterprises has increased.

from the perspective of growth ability, the first half of the performance improved quarter by quarter, Q4 performance growth is expected to step up

2023Q1 performance growth rate of about -3.86, reversing the quarterly performance growth rate continued to decline, 2023Q2 performance growth rate of about 5.55, the ring showed an accelerating trend. We believe that with the medium-term adjustment landing, Q4 orders will gradually become clear, the pre-delivery of goods (inventory transfer out) revenue recognition is expected to accelerate, Q4 sector performance year-on-year growth rate or step up.

looking at the full-year dimension of 23 years, the quarterly performance growth rate may be low before and high after

The international situation is becoming increasingly tense, and military expansion is still imminent. The mid-term adjustment of the five-year plan is coming to an end, with the late orders gradually clear, the business climate of the military sector will be significantly improved, the full-year quarterly performance growth rate will be low after the high, the overall performance growth or exceed expectations. We expect full-year 2023 revenue and non-return net profit to grow by 14% and 6%, respectively.

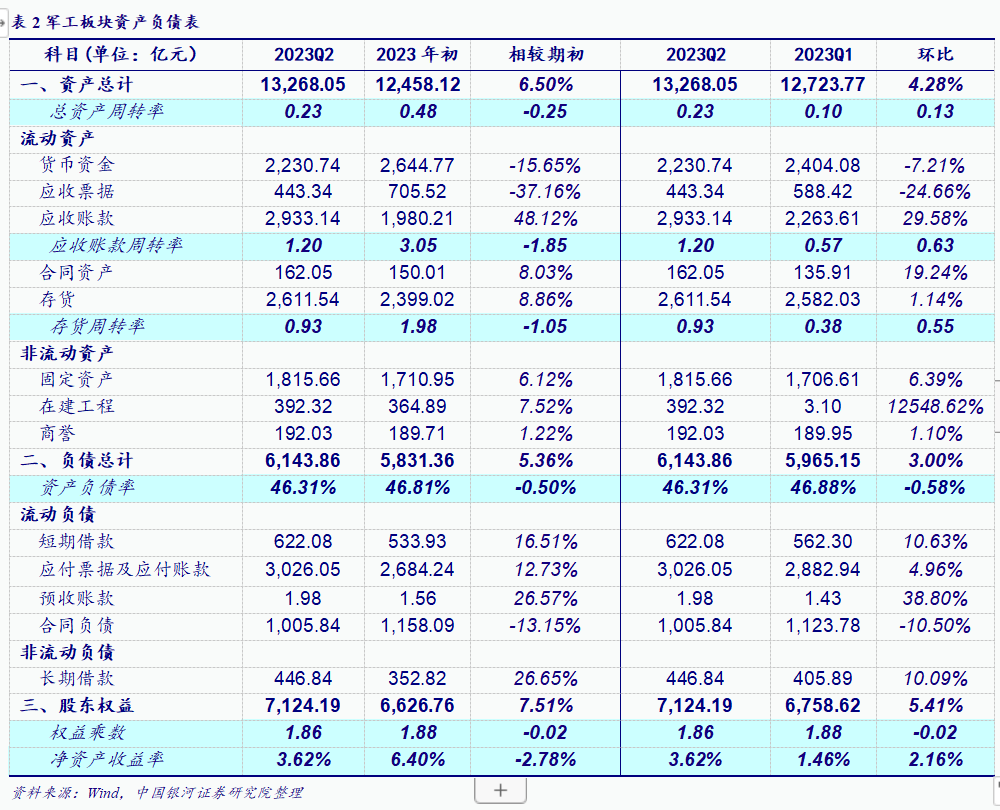

(II) balance sheet analysis: inventories and fixed assets continue to grow, demand-driven industry boom still exists

analysis of the accounts in the balance sheet, 2023Q2 military sector total assets of 1326.805 billion yuan, total liabilities of 614.386 billion yuan, asset-liability ratio of 46.31, compared with the beginning of 2023 decreased by 0.50pct.

Under Assets:

2023Q2 accounts receivable balance was 293.314 billion yuan, up 48.12 from the beginning of the period and 29.58 from 2023Q1. High accounts receivable and higher credit impairment losses, which we believe are related to delays in product delivery and revenue recognition during the medium-term adjustment period. However, given that the downstream of the industry is mostly creditworthy military customers, the risk of bad debt receivables is small.

2023Q2 inventory balance increased 8.86 percent from the beginning of the period and 1.14 percent from 2023Q1. We believe that, first of all, military enterprises production and operation planning is strong, inventory and orders in hand have a certain correlation, the rapid growth of inventory for demand traction, enterprises take the initiative to increase the stocking efforts to cope with the performance of order growth. Secondly, due to the order uncertainty brought about by the mid-term adjustment of the five-year plan, the overall product delivery of 23H1 military industry was lower than expected, and some passive inventory also became one of the reasons for inventory growth. In addition, 2023Q2 fixed asset 181.566 billion, construction in progress 39.232 billion, increased by 6.12 and 7.52, respectively, compared with the beginning of the period, showing a sustained growth trend, reflecting the sector enterprises in response to downstream demand growth, capacity expansion on the road.

Under Liabilities:

2023Q2 contract liabilities of 100.584 billion yuan, a decrease of 10.50 compared with 2023Q1, a decrease of 13.15 compared with the beginning of the period, or due to the combined effect of quarterly product delivery and new signing orders, superimposed on the negative impact of medium-term adjustment on the landing of new orders. In addition, 23Q2 observed rapid growth in long-term borrowing (+26.65 per cent from early 23), or long-term financial arrangements for companies to increase capital expenditures and cope with the impact of high accounts receivable on cash flow.

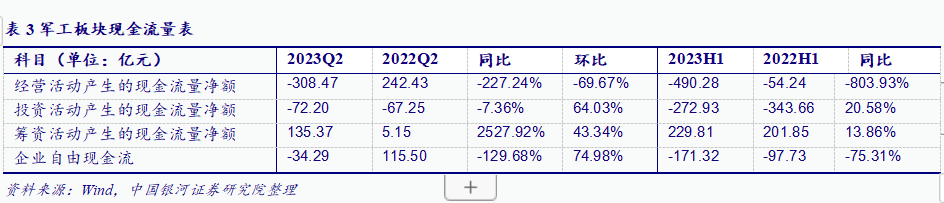

Brief Analysis of (III) Cash Flow Statement: Deterioration of Operating Cash Flow and Increased Pressure on Payback

Analysis of the main accounts in the statement of cash flows, 2023Q2 operating cash flow was negative, down 227.24 percent year-on-year, 2023Q2 decreased 69.67 percent month-on-month from 2023Q1, and cash flow showed a deteriorating trend. We believe that the main reason for the tight cash flow from operating activities is the rapid growth of the industry's overall accounts receivable and the deterioration of the repayment under the condition that the 23H1 delivery acceptance is not as expected. At the same time, in order to cope with potential demand, the company's pace of production and stocking has not decreased, and the two factors together affect operating cash flow performance.

2. sub-sectors are greatly affected by the industrial environment and their performance is differentiated

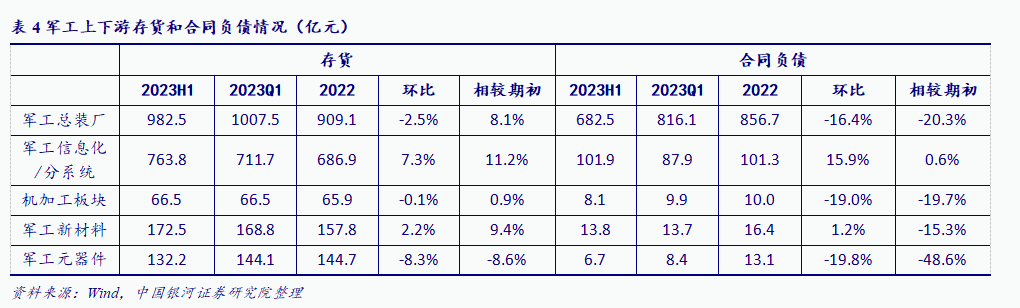

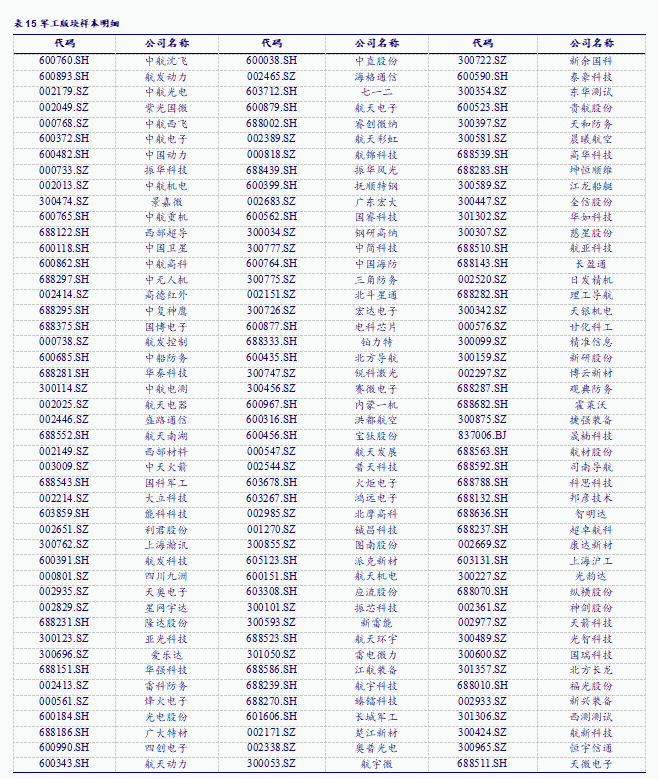

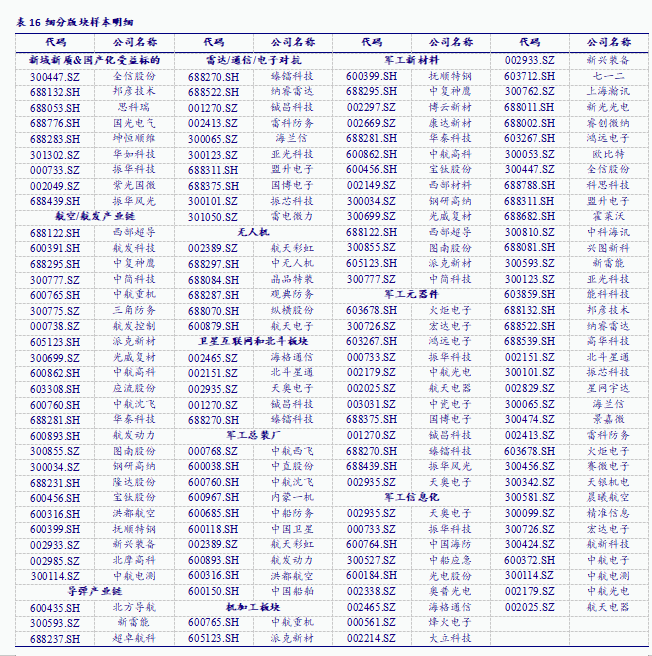

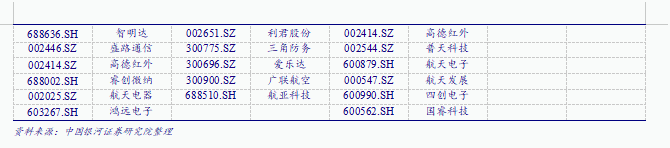

Tips: 1. Study sample selection. Our general industrial plate according to two classification methods, first of all, according to the industrial chain upstream and downstream classification: divided into downstream military assembly plant, midstream military information and machining plate, upstream military new materials and military components a total of 5 sub-plates (see appendix): aviation aviation industry chain, missile industry chain, drone industry chain, radar-electronic countermeasure plate, satellite Internet-Beidou plate, new domain new quality-domestic benefit target, state-owned enterprise reform expected target.

2, we select operating income, net profit and inventory, accounts receivable four financial indicators reflecting the operating conditions of the enterprise;

3, regardless of related transactions, through the overall method of sub-plate analysis.

(I) Prospective Analysis: Inventory and Contract Liabilities

The increase in inventories includes both active and passive increases in inventories, and the military industry will be in an upward cycle during the 14th Five-Year Plan period. With the gradual release of market demand, the increase in inventory in the military industry is likely to belong to the active stocking behavior of the main body of the industry, and is expected to translate into an increase in future revenue. In contrast, during the outbreak and during the mid-term adjustment of the 14th Five-Year Plan, passive inventory increases are more common. The increase in accounts receivable directly reflects the demand intensity of downstream customers in the industry, and the certainty of revenue growth is strong.

1. Analysis of upstream and downstream of industrial chain

from the upstream and downstream analysis, in addition to components, 2023H1 military industry whole industry chain inventory compared to the beginning of the period to achieve a certain growth, of which the upstream new materials and midstream information sector growth faster, respectively, compared with the beginning of the growth of 9.4 and 11.2, the industry active replenishment will be strong. Month-on-month, the industrial chain links 23Q2 compared to 23Q1 have increased or decreased, of which military components, assembly plant month-on-month decline, down 8.3 percent and 2.5 percent, respectively, while military information technology and new materials inventory have risen.

contract liabilities, in addition to the information sector, the industry-wide 2023H1 compared to the beginning of the period have declined, of which the new materials and machining sectors changed less, down 15.3 and 19.7 percent, respectively. Upstream component end, downstream assembly plant decreased significantly by 48.6 and 20.3, respectively.

We believe that the decline in industry-wide contract liabilities is related to the consumption of stock orders and the shortage of new orders, in which components are the first to be consumed due to the short order cycle and delivery cycle, while the final assembly plant is directly connected to the end customer, and the decline in contract liabilities may directly indicate that 23H1 new demand is weak. On a month-on-month basis, the level of military information and new materials has improved compared with 23Q1.

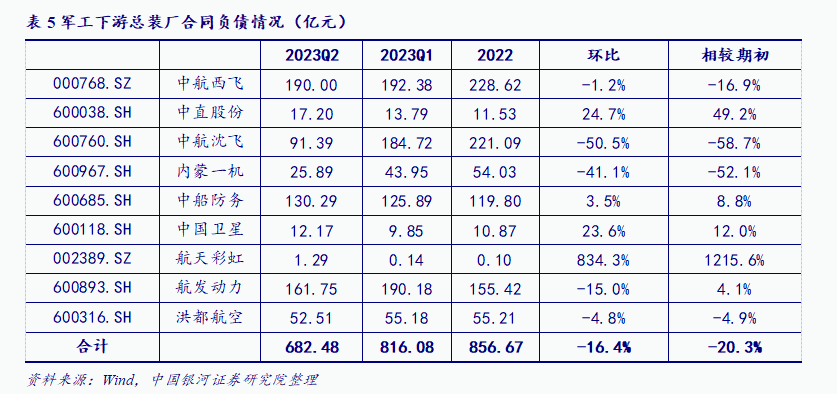

In the host plant, the level of liabilities of the aerospace rainbow contract was bright, up 1215.6 percent from the beginning of the period, mainly due to the receipt of payment for drones, and the high business climate in the field of military drones was highlighted.

2. Subdivision analysis

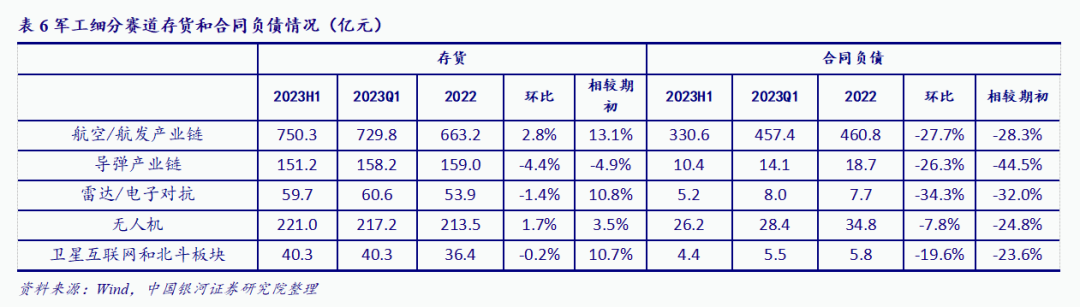

judging from the subdivision of the track, 2023H1 has seen a certain increase in all sectors except the slight decrease in the inventory of the missile industry chain compared with the same period last year. we believe that there are two factors that jointly affect: 1) the confidence of the sector enterprises in the future order situation and the appropriate reserve of raw materials; 2) Due to changes in the macro and industrial environment, some orders have not yet been delivered and inventories have increased.

Contract liabilities 2023H1 multi-sector continued to weaken.

(II) Lag Analysis: Revenue and Profit Side

1. Analysis of upstream and downstream of industrial chain

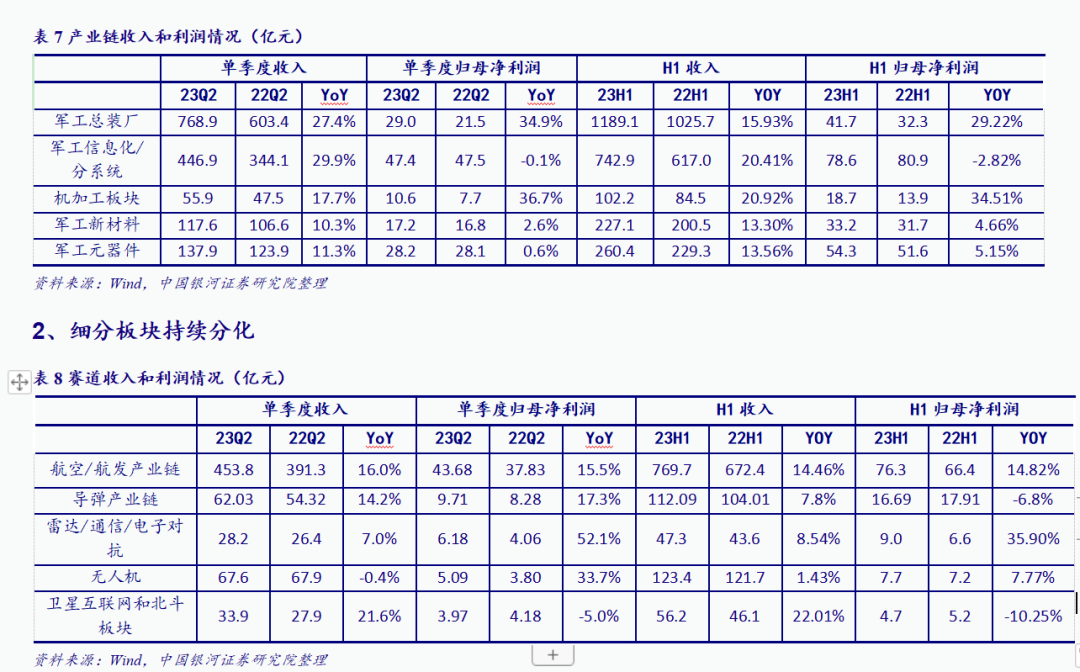

From the revenue side, 2023H1 industry chain revenue achieved double-digit positive growth, midstream information technology, machine plus sector performance, revenue growth of 20.41 and 20.92, respectively. From the profit side, the machine plus sector and the final assembly plant sector performed first, with net profit growth of 34.51 and 29.22, respectively.

midstream military information technology and upstream components, new materials in the field of profit growth than the income growth rate narrowed, we believe that the main reason is that the relevant enterprises by the upstream and downstream double suppression: 1) raw material prices; 2) military products VAT cancellation led to the biggest impact on midstream and upstream enterprises; 3) product price downward pressure.

General assembly plant and machine plus plate revenue more profit, the scale effect is obvious.

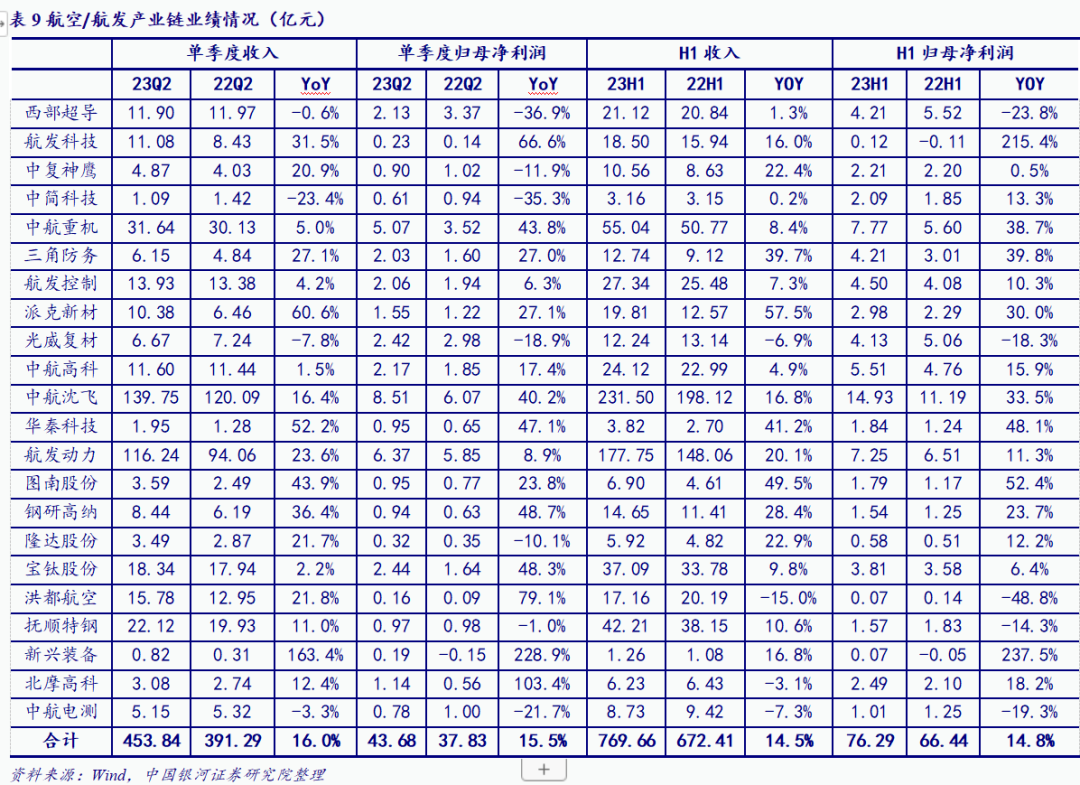

(1) Aviation/Aviation Industry Chain

the overall performance of the sector is more robust, 23H1 revenue growth of 14.5 percent, the return of net profit increased by 14.8 percent year-on-year, of which Q2 single-quarter revenue increased by 16.0 percent year-on-year, the return of net profit increased by 15.5 percent. Among them: the main engine factory, AVIC Shenfei 23H1 revenue of 23.15 billion yuan, net profit of 1.493 billion yuan, an increase of 16.8 and 33.5 respectively, the business situation is good. Hongdu Airlines saw a decline in 23H1 revenue and profit growth due to a decrease in the number of products delivered.

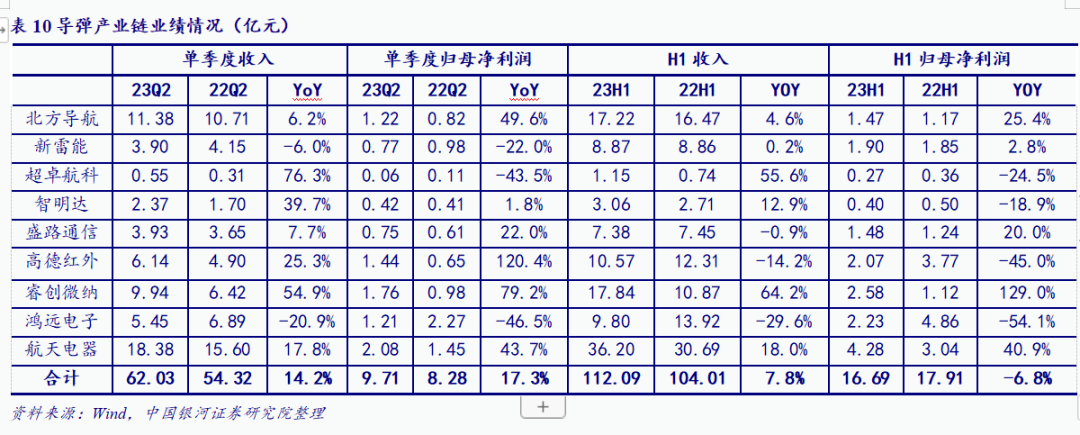

(2) Missile Industry Chain

23H1 overall revenue 11.21 billion, up 7.8 percent year-on-year, with net profit attributable to the parent company 1.669 billion, down 6.8 percent year-on-year, with Q2 revenue 6.2 billion, up 14.2 percent year-on-year, and net profit attributable to the parent company 0.97 billion, up 17.3 percent year-on-year.

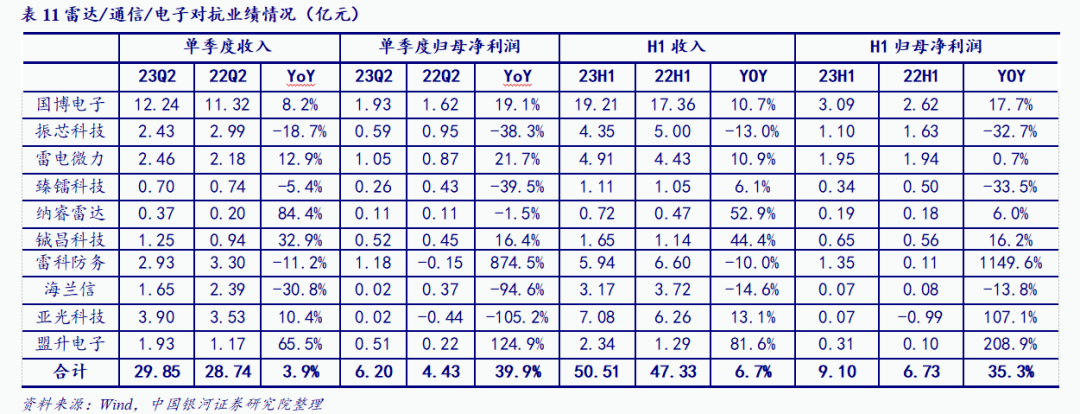

(3) Radar Communication Board

23H1 contributed a large growth rate due to the low base of Yaguang Technology 2022H1. Excluding Yiguang Technology, the sector 23H1 total revenue of 4.343 billion yuan (YoY plus 5.8%), the parent net profit 9.03(YoY plus 17.1%).

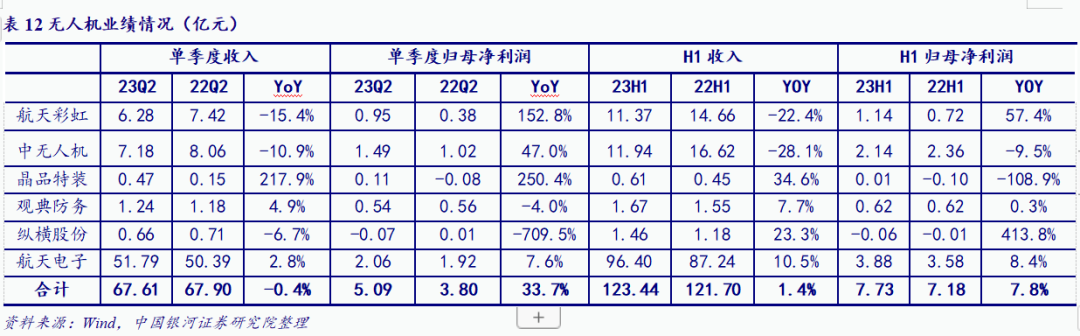

(4) Unmanned Equipment Board

23H1 overall revenue 12.344 billion, up 1.4 percent year-on-year, with net profit attributable to the parent company 0.773 billion, up 7.8 percent year-on-year, of which Q2 revenue 6.76 billion, down 0.4 percent year-on-year, and net profit attributable to the parent company 0.509 billion, up 33.7 percent year-on-year. Among them, aerospace electronics, aerospace rainbow and medium-sized drones to the sector revenue and profit contribution is greater.

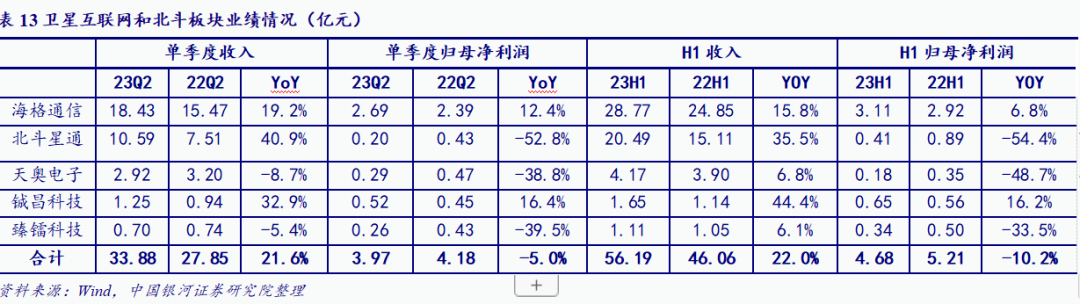

(5) Satellite Internet and Beidou Plate

23H1 overall revenue 5.619 billion, up 22.0 YoY, net profit attributable to the mother 0.468 billion, up -10.2 YoY, of which Q2 revenue 3.388 billion, up 21.6 YoY, net profit attributable to the mother 0.397 billion, down 5.0 YoY.

The overall valuation of the 3. military sector has more room for improvement

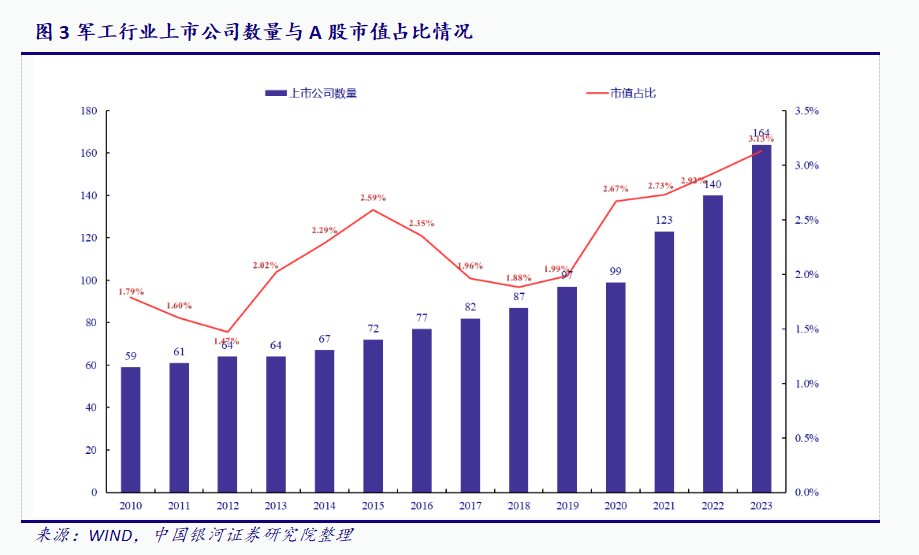

there are currently 164 military-related listed companies in (I), accounting for 3.13 of the total market value of a shares

In terms of the number of listed companies, as of September 8, 2023, there were 5274 listed companies in China's A- shares, of which 164 were listed in the military industry, accounting for 3.11. In terms of market capitalization, as of September 8, 2023, the total market capitalization of A- shares was 87.01 trillion, and the total market capitalization of listed companies in the military industry was 2.72 trillion, accounting for 3.13 percent. As of September 8, 2023, the top five listed companies by market capitalization were AVIC Shenfei, China Shipbuilding, Hangfa Power, AVIC Optoelectronics, and China Heavy Industry (Rights Protection).

We select the CSI Military Industry Index and the CSI 800 to approximate the characterization of the military industry and the entire A- share market, respectively, and through the regression analysis of the yield data for both from the beginning of 2012 to the present, we obtain a beta of about 1.0378 for the military industry, indicating that the military industry is slightly more volatile relative to the market.

(II) military sector valuation is lower than the valuation center, the upside is still large

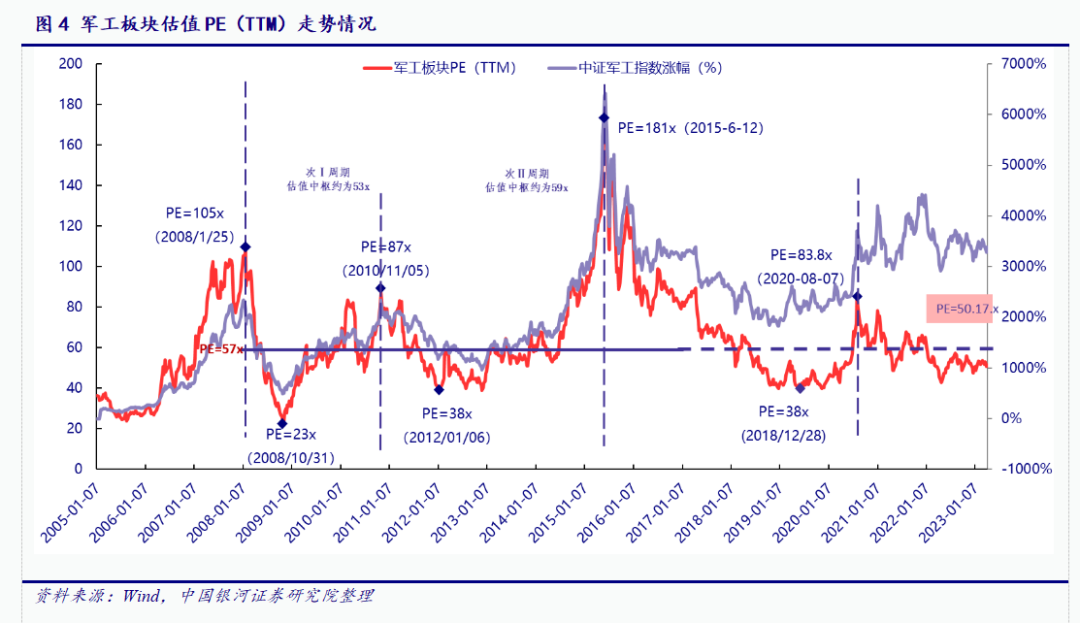

1, vertically, the current valuation level of the military sector is lower than the valuation pivot

judging from the historical trend of the valuation level of the military industry sector (excluding listed companies in the ship assembly category and regularly adding new military industry shares), we regard January 2008 to June 2015 as a typical bull-bear cycle with a large time span, including two sub-cycles. according to calculation, the valuation center of the large-cycle sector (taking the median) is about 57x, and the two sub-cycles are 53x and 59x respectively.

In the second cycle stage, the military business of listed companies in the sector accounts for a relatively small proportion, and the attitude of the competent authorities towards the injection of military assets is not clear, but at this stage, the industry valuation level takes into account not only the endogenous growth rate, but also the asset securitization factor;

in the second cycle stage, with the start of the injection of core military assets of listed military companies represented by aviation power, the attitude of the competent authorities to support the securitization of military products gradually became clear. asset injection began to be included as an important factor in the consideration of the industry valuation level and was interpreted and amplified until it reached its peak in mid -2015. At the same time, the high growth of the extended M & A model has also been sought after by the market, and goodwill risk has begun to accumulate at an accelerated pace. Since June 2015, the market has gradually returned to rationality, and the marginal impact of asset injections and extended M & A expectations on sector valuation levels has weakened.

Looking ahead, we believe that the industry valuation pivot should better balance the two phases of the sub-cycle I and the sub-cycle II, so we choose the valuation pivot of the large cycle from January 2008 to June 2015 as the reference standard.

As of September 8, 2023, the overall valuation (TTM) of the military sector was about 50.17x, below the valuation center of 57x.

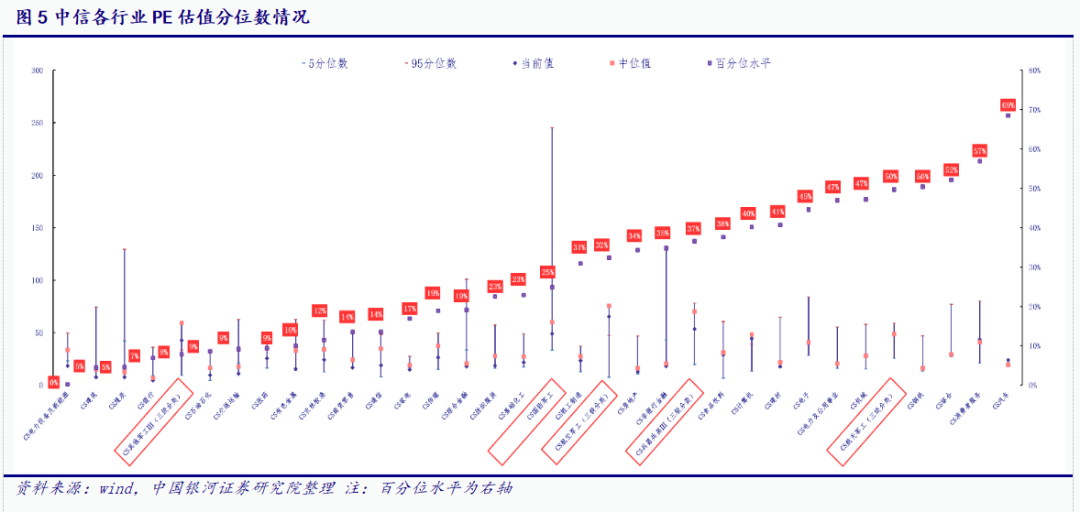

2. Looking horizontally, the sector valuation is about 24.9 per cent, with more room for improvement

from a horizontal comparison, referring to citic's first-class industry classification, as of September 8, 2023, the top three valuations were national defense industry (49.1 times), computers (44.3 times) and consumer services (43.7 times), while the bottom three valuations were banks (4.7 times), coal (7.7 times) and construction (7.8 times).

Comparing the historical average levels of various industries, the valuation of consumer services, automobiles and other industries is significantly higher than the historical average, while the non-ferrous metals, coal and other industries are significantly lower than the historical average. Compared with other technology sectors, the valuation level of the military industry is relatively high, but the valuation number is only 24.9, the space is larger.

In the three-tier industry classification of CITIC Defense and Military Industry, the valuation of aviation and military equipment is the highest, at 65.48 times and 53.61 times respectively, followed by the valuation of aerospace and other military industries, at 48.7 and 42.7 times respectively. However, compared with the current percentile level, aerospace industry, weapons and aviation industry are 49.7 per cent, 36.6 per cent and 32.4 per cent, respectively, all below 50 per cent, with more room for improvement.

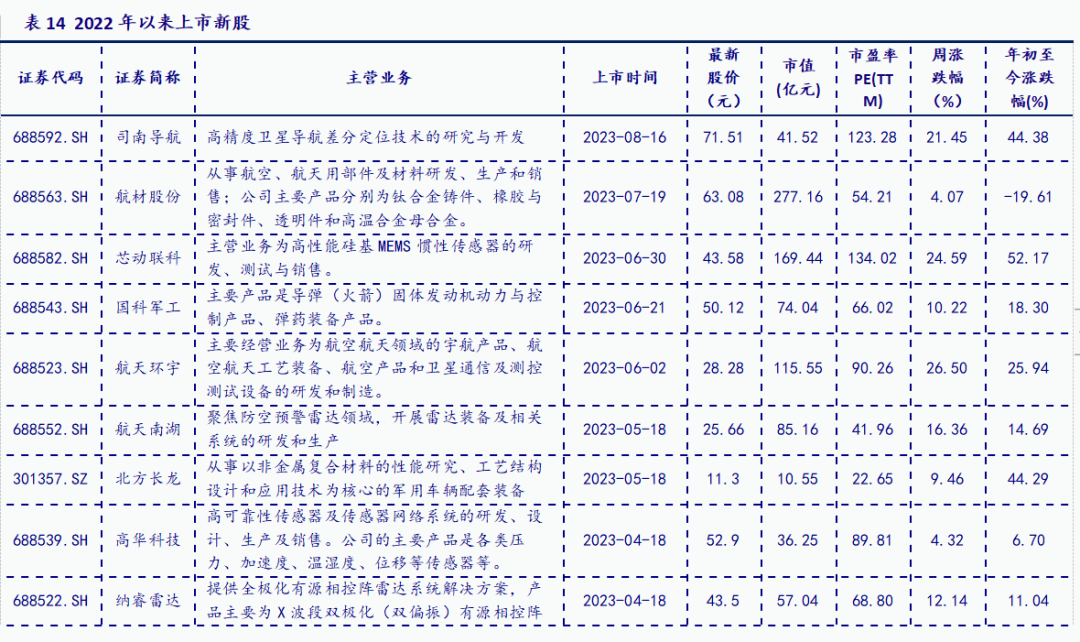

(III) Military New Stock Tracking

4. investment advice: "left" layout time has come, wait for the east wind to set sail again

[all profits + waiting for east wind] in the short term, first of all, valuation suppression factors such as uncertain industry orders, price cuts for key models, and weak Q3 performance expectations are basically priced in; Secondly, the mid-term adjustment Q3 of the five-year equipment procurement plan will fall to the ground, the order Q4 may be visible, and the expected improvement of sector performance will be raised. The time has come for the left layout.

[volume and price] "volume" and "price" are two important factors affecting the performance of the military sector in the second half of the year. it is expected that the sector will rebound due to "volume" and the transparency of "price" will lag behind a financial reporting period. although the rebound height is limited, it will not affect the rebound time point. currently, it should be moderately positive.

[asset restructuring of central enterprises on the way] the SASAC central enterprises high-quality development promotion meeting was held intensively, requiring a number of flagship leading listed companies with strong core competitiveness and great market influence within three years. The listed companies of military central enterprises are generally "small but not strong" or "big but not excellent", and the restructuring tide is approaching.

[squat jump] in the medium and long term, the war between Russia and Ukraine caused great changes in the geopolitical pattern, the rapid deterioration of the security situation around China, the upgrading of equipment and the demand for new quality and new domain equipment is still urgent, "low cost + consumable" is the development trend of equipment, long-term prosperity is inevitable.

[layout period] the military sector has been fully adjusted since the beginning of the year. the time has come for the layout on the left side. wait for the east wind to set sail again. it is suggested to configure the "five dimensions":

1) left layout target, western superconducting (688122.SH), triangular defense (300775.SZ), purple light country micro (002049.SZ);

2) new quality and new domain, including unmanned aerial vehicles (688297.SH), space rainbow (002389.SZ), space electronics (600879.SH), crystal special equipment (688084.SH), far fire suppliers north navigation (600435.SH), science and technology navigation (688282.SH), radar/communication/electronic countermeasure core suppliers radium electronic technology (68862.SZ), shengyi security supplier (SH6.886);

3) the central enterprise reform beneficiary target, recommended China Aviation Electronics (600372.SH), Tianao Electronics (002935.SZ), Guorui Technology (600562.SH) and Aviation Control (000738.SH), etc., pay attention to the aerospace department;

4) domestic beneficiary targets, including Lunda shares (688231.SH), Zhenhua scenery (688439.SH), etc.;

5) Military trade beneficiaries, including Aerospace South Lake (688552.SH), Aerospace Rainbow (002389.SZ).

5. risk warning

The risk of military reform not meeting expectations, the risk of equipment procurement not meeting expectations, the risk of enterprises expanding production less than expected, and the risk of upstream raw material price fluctuations.

6. Appendix

This article is excerpted from: the research paper "[industry in-depth review]" left "layout time has come, waiting for the east wind to set sail again" released by China Galaxy Securities on September 12, 2023

Analyst: Li Liang, Hu Haomiao

Rating system:

Recommended: Expected to exceed the average return of the benchmark index by 20% or more.

Cautious recommendation: Expected to outperform the average return of the benchmark index.

Neutral: Expected to be comparable to the average return of the benchmark index.

Avoidance: Expected to be below the benchmark index.

Recommended: Expected to exceed the average return of the benchmark index by 20% or more.

Cautious recommendation: Expected to outperform the average return of the benchmark index.

Neutral: Expected to be comparable to the average return of the benchmark index.

Avoidance: Expected to be below the benchmark index.

Ticker Name

Percentage Change

Inclusion Date