From: Prospective Industry Research Institute

Major listed companies in the industry: Aimee (300896), Haohai Biotech (688366), Huaxi Bio (688363), Huadong Medicine (000963), Longzi (002612), Huahan Plastic (430335), etc.

The core data of this article: China's light medical beauty industry chain combing; China's non-surgical medical beauty, surgical medical beauty project market size and growth rate comparison; China's light medical beauty industry online transaction order volume ratio; light medical beauty industry value chain distribution, etc.

Industry Overview

1. Definition

light medical beauty refers to non-surgical medical beauty items, mainly including injection items, photoelectric items and other fine-tuning items. injection items include thin face needle, hyaluronic acid filling, water light needle, etc., and photoelectric items include photon skin rejuvenation, hot maggie, ultrasonic knife, etc. Compared with traditional medical beauty, light medical beauty has the characteristics of no operation, smaller wound, short recovery period and remarkable effect, which has been widely welcomed by young consumers in recent years.

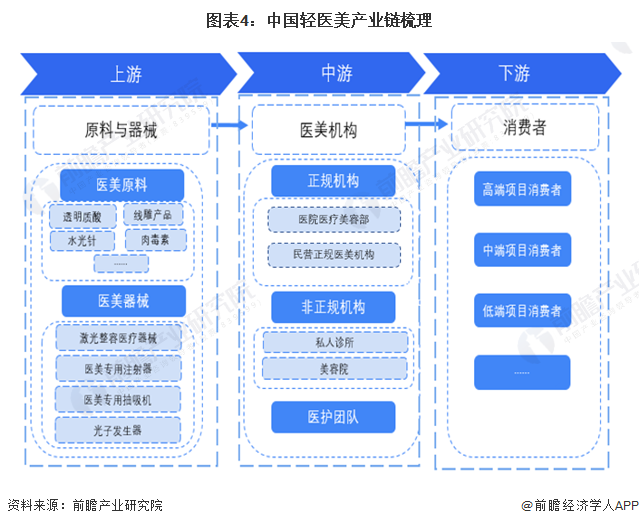

2, industrial chain analysis: midstream medical and beauty institutions still need to speed up the pace of integration

from the perspective of industrial chain, according to the types of light medical beauty projects, corresponding to different raw materials, the upstream raw materials of photoelectric projects include laser cosmetic medical devices, photon generators, etc., and the upstream raw materials of injection projects include hyaluronic acid, water needle, botulinum toxin, wire carving products, special syringes for medical beauty, special suction machines for medical beauty, etc. In the middle reaches of the industrial chain, there are various medical and aesthetic institutions with injection and optoelectronic projects, including public hospitals and private medical and aesthetic institutions. At the same time, there are a large number of informal institutions in the market, including private clinics and beauty salons. These places are areas with a high incidence of medical accidents, and they are also a major source of consumers' distrust of the entire industry. The downstream of the industrial chain is consumers, which are mainly divided into high-end project consumers, mid-range project consumers and low-end project consumers according to their consumer preferences for medical and beauty projects.

from the perspective of industry chain participants, China's light medical and beauty upstream raw material manufacturers mainly include Huaxi Biology, Aimee, Haohai Biotech, East China Medicine, Focus Biology, etc. Light medical and beauty related medical devices are mainly foreign leading manufacturers of medical and beauty devices. The middle reaches of the light medical and beauty institutions mainly include China and Korea, Lido, Ruili, Pengai and other emerging light medical and beauty platforms include new oxygen, more beautiful and other Internet platforms; downstream is mainly the vast number of light medical beauty consumers.

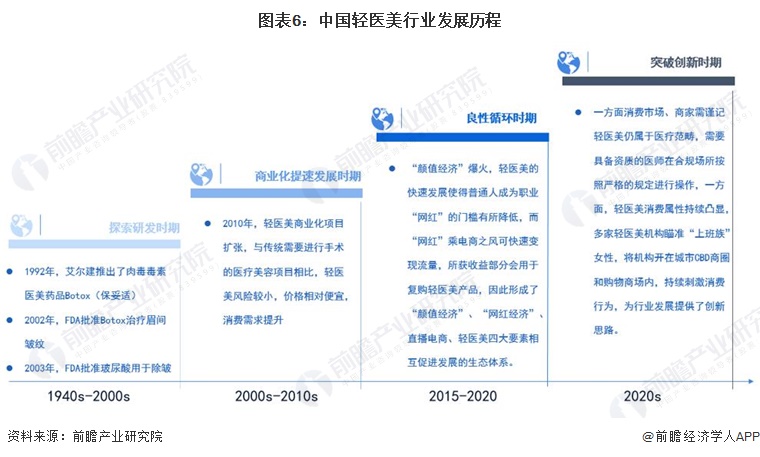

Industry development history: mistakenly hit the golden road

Light medical beauty is a new concept that has only emerged in recent years, but the application of injection and photoelectric medical beauty projects mentioned under the concept of light medical beauty can be traced back to the Second World War. During the Second World War, due to the strong toxicity of botulinum, it can induce human poisoning and was once used as a biochemical weapon. After the war, scholars at the University of Cambridge in the United Kingdom discovered the mechanism of action of botulinum toxin, that is, after botulinum toxin enters the muscle, it will block the impulse from the nerve, causing the muscle to not contract, but in a "paralyzed" state. In 1992, the international medical and American pharmaceutical giant Aljian introduced Botox (Botox), a botulinum toxin medical and American drug, and from then on, thin face needles became popular. In 2002, FDA (U.S. Food and Drug Administration) approved Botox to treat eyebrow wrinkles. In 2003, FDA approved hyaluronic acid for wrinkle removal. This sulfur-free acidic mucopolysaccharide can quickly replenish water and restore vitality to connective tissue, epithelial tissue and nerve tissue of human body, and then gradually become the golden track of light medicine and beauty.

after 2010, the internet, social media and other technologies have developed rapidly, and internet medical beauty platforms have been established one after another. compared with consumers' perception of traditional medical beauty as "expensive", "South Korea", "bold" and "easily disfigured" during the millennium, light medical beauty projects such as hyaluronic acid, botulinum toxin, collagen, poly-L-lactic acid, as well as photon rejuvenation, picosecond, laser hair removal, hair transplant, etc., etc. are less risky, at the same time, the price is relatively cheap and the effect is immediate, so the consumer's willingness to spend is greatly increased in the short term.

around 2015, driven by the "Yan value economy" and superimposed on the increasingly mature community content platform, more and more people have discovered the development opportunities of self-media and professional "net red", which is different from the situation that the first generation of net red has high threshold, difficult to realize traffic, and most of them still need talents to be added to not be eliminated by the ever-changing internet. in 2015 and after, the "light medical beauty" within reach has broadened the channels for consumers to become beautiful. At the same time, it has also greatly lowered the threshold for self-media and professional "online celebrities". The take-off of e-commerce has promoted the realization of traffic. In order to maintain the best state, most of the "online celebrities" who have obtained the benefits will re-purchase light medical beauty projects. As a result, the commercial closed loop of light medical beauty is formed, it also attracts waves of consumers who want to be more beautiful. Since 2020, light medical beauty has grown rapidly. In first-tier cities, light medical beauty institutions have gradually become the mainstream trend to enter shopping malls and CBD. Representative cases include Enid Light Medical Beauty in Hangzhou Wulin CBD, Light Reed Light Medical Beauty in Shenzhen Futian CBD, Ning Yue Light Medical Beauty in Beijing Guanghua Road SOHO, and "Medical Beauty Street" in Guangzhou Zhujiang New Town CBD. With the rapid growth of demand and market, light medical beauty or will become the mainstay of the second half of the medical beauty industry.

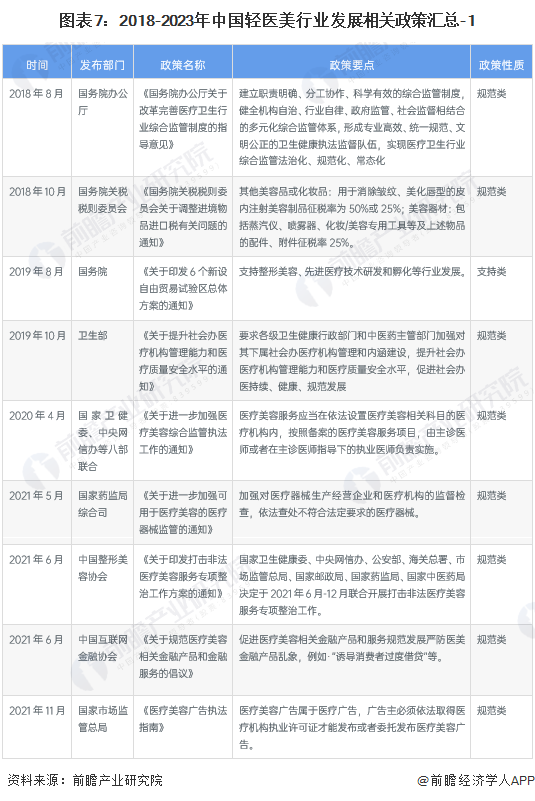

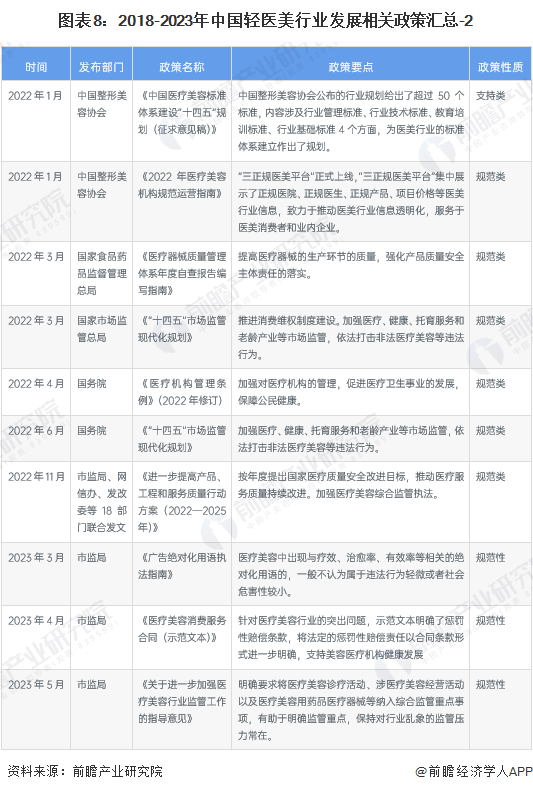

Industry policy background: Tighter supervision and large number of normative policy documents

In recent years, many departments in my country have issued policy documents to regulate the development of the light medical and beauty industry, which fully protects the rights and interests of consumers. At the same time, they have also severely cracked down on counterfeit products and non-compliant businesses. To a certain extent, it promoted the healthy development of the industry.

Industry development status

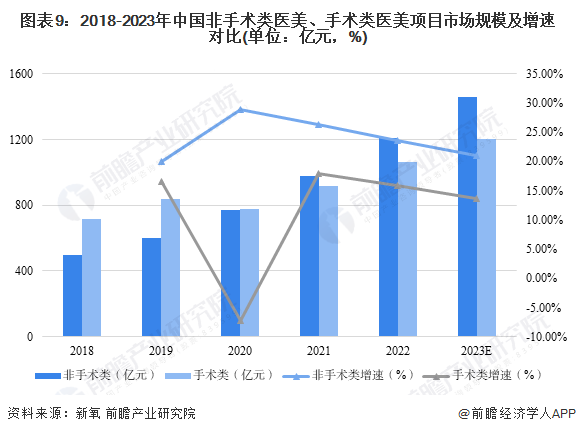

1, light medical beauty industry market growth faster than surgical medical beauty

Before 2021, the market size of surgical medical beauty projects is larger than that of non-surgical medical beauty projects, and in recent years, China's light medical beauty industry has developed rapidly, and the market size growth rate is far faster than that of surgical projects. Therefore, from 2021 onwards, the market size of non-surgical medical beauty projects (light medical beauty) will begin to exceed that of surgical medical beauty projects. According to forward-looking preliminary statistics, in 2023, the market size of China's light medical beauty industry will reach 146.4 billion billion yuan, a growth rate of 21.04.

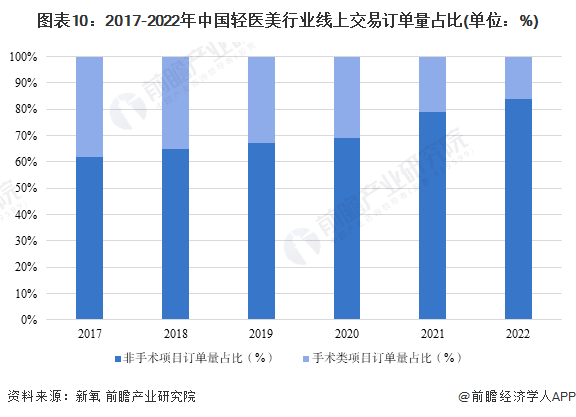

2, light medical online order volume accounted for more than 80%

judging from the online order volume, light medical beauty basically dominates 80% of the online platform. in 2017, the online order volume of light medical beauty in China accounted for 62%, while in 2022, this data has increased to 84%. On the one hand, my country's light medical beauty online resource integration has developed well, and has formed a momentum of integrated development. On the other hand, it reflects the heavy dependence on platforms and traffic. If businesses cannot obtain traffic through the platform, it will be difficult to compete. Survive in an increasingly fierce industry.

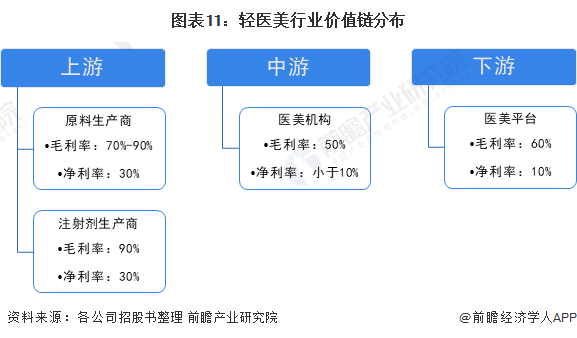

3. The net interest rate of midstream medical institutions is low, and the pressure on upstream and downstream is greater

From the perspective of value chain distribution, the net interest rate of medical and beauty institutions in the middle reaches of the industrial chain of my country's light medical and beauty industry is low, usually less than 10%. The main reason is that, unlike other medical projects, the light medical and beauty project itself does not belong to "rigid demand". Although consumer demand is relatively strong, because the industry has certain consumption attributes, consumers usually adopt the consumption strategy of "shop around".The card will have a greater advantage in obtaining customers. As a result, these institutions are more dependent on online platforms and multi-party advertising channels, with higher advertising costs and crowding out net interest margin space. The upper reaches of the industry are biomedical companies, which have patented technology moats, with gross margins as high as 70% to 90% and net margins of more than 30%. The downstream of the industry is the consumer or platform side, and the platform side gross margin is usually around 10%.

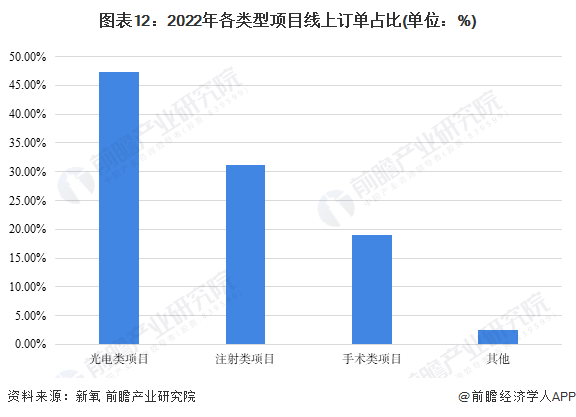

4. Photoelectric projects have become the most popular projects for consumers

in 2022, 47.34 percent of the consumer orders for online medical and beauty projects in China will be photoelectric projects, such as hot maggie and photon rejuvenation, followed by injection projects, including hyaluronic acid injection and botulinum toxin injection, accounting for 31.22 percent. Surgical items ranked third, accounting for only 19.04 percent. Generally speaking, photoelectric projects are the favorite projects of consumers. The main reason is that photoelectric projects do not involve surgery or even filling. The risk coefficient is low and the price is relatively low. It can be used as a good start for consumers to test water and medical beauty.

Industry competition landscape

1, regional competition: Guangdong light medical beauty industry developed

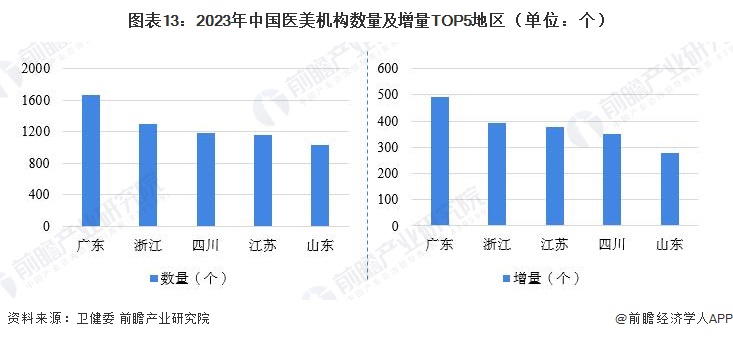

The development and growth of light medical beauty requires a solid foundation for the development of the medical beauty industry. Usually, the more developed areas of the medical beauty industry have formed a relatively good development division, and consumers also have a certain basis for consumption habits. According to the relevant data released by the National Health and Care Commission in June 2023, the number of compliance Junior College medical and beauty institutions in China is 15513 (excluding comprehensive and public institutions, according to the big data analysis of Shenzhen medical and beauty institutions in 2023, the proportion of private comprehensive and public institutions is about 10%). Among them, Guangdong Province has the largest number of medical and aesthetic institutions, reaching 1664. In the first half of 2023, Guangdong Province also has the largest increase of medical and aesthetic institutions, reaching 493. This is followed by Zhejiang Province, which has 1291 medical and beauty institutions, with an increase of 393 in the first half of 2023.

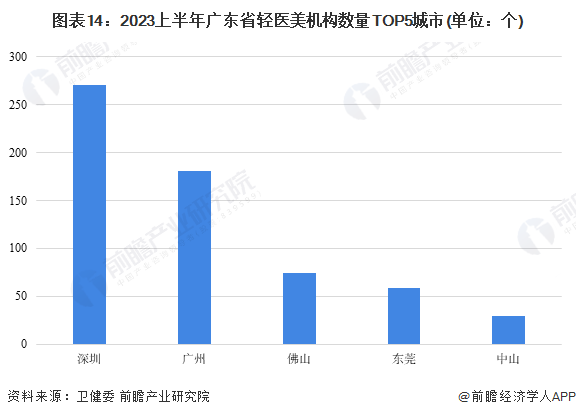

judging from the development atmosphere of light medical beauty industry in Guangdong province, the development of light medical beauty in Shenzhen is relatively cutting-edge. according to the data of the health and health Commission, as of the first half of 2023, there were 270 light medical beauty institutions in Shenzhen, followed by Guangzhou, with a total of 181, and the third was Foshan, with a total of 74. As the region with the largest number of medical and aesthetic institutions Junior College Guangdong Province, Shenzhen is far ahead of the opening of big data, which is also the starting point of the reform of medical and aesthetic big data analysis.

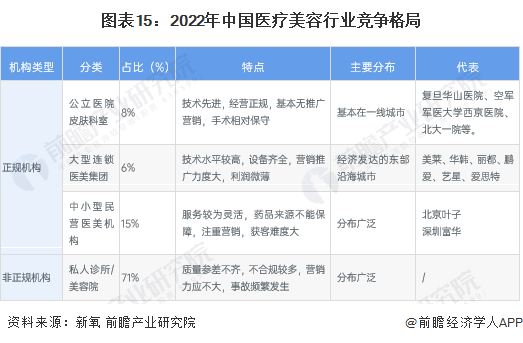

2. Enterprise competition: informal institutions account for a large proportion

From the perspective of hospitals and institutions, my country's institutions involved in light medical beauty mainly include dermatology departments in public hospitals, large chain medical beauty groups, small and medium-sized private institutions, and private clinics and beauty salons. Overall, China's medical and beauty institutions show a messy distribution, uneven quality, uneven development of good and bad phenomenon. Public hospitals, large chain medical beauty groups and even small and medium-sized private medical beauty institutions account for a relatively low market share. More than 70% of the market is occupied by informal institutions. These places are also places where medical beauty accidents occur frequently. In the future, as consumer awareness increases and competition in the industry intensifies, non-compliant institutions may accelerate their clearance.

Industry development prospect and trend forecast

1, photoelectric projects continue to lead the consumption boom

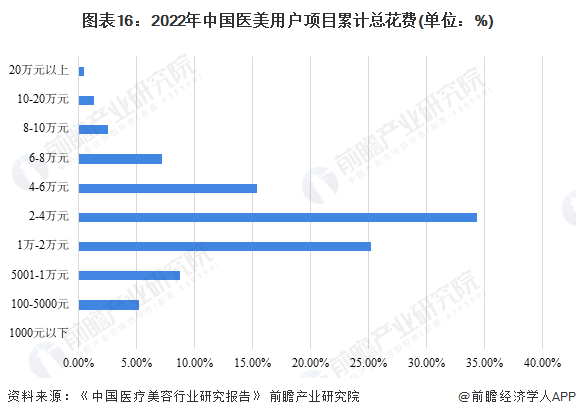

According to the research results in the Research Report on China's Medical Beauty Industry, in the past year, the largest number of consumers spent 1-60000 yuan on medical beauty projects, of which more than 30% spent 2-40000 yuan. Refer to the previous price and theoretical frequency of medical beauty projects (Chart 1-Chart 3), projects with high repeatability, short cycle and short interval will play an increasingly important role. Representative projects include photon rejuvenation and picosecond laser. Injection projects are less feasible for long-term operation due to certain skin lesions or unclean metabolism, while hair projects and dental beauty projects cannot form a stock market due to their long validity period and can only continuously develop an incremental market, thus lacking customer stickiness. Generally speaking, photoelectric projects are an important growth point for the light medical and beauty industry in the future.

2. China's light medical beauty market is expected to exceed 400 billion yuan in 2030

according to the new oxygen data Yan research institute, the market size of China's light medical beauty industry will reach 415.7 billion yuan in 2030, about twice the market size of surgical medical beauty. It is estimated that in 2023, the size of China's light medical beauty market can reach 146.1 billion billion yuan, with a compound growth rate of about 16.11 from 2023 to 2030.

For more research and analysis of this industry, please refer to the "China Medical Beauty Industry Market Demand Forecast and Investment Strategic Planning Analysis Report" by the Prospective Industry Research Institute.

at the same time, the prospective industrial research institute also provides solutions such as industrial big data, industrial research report, industrial planning, park planning, industrial investment promotion, industrial map, intelligent investment promotion system, industry status certificate, IPO consultation/feasibility study of investment raising, IPO working paper consultation, etc. Citing the contents of this article in any public disclosure such as the prospectus and the company's annual report requires formal authorization from the Prospective Industry Research Institute.

more in-depth industry analysis can be found in [prospective economist APP], and you can also communicate and interact with 500 + economists/senior industry researchers.

Ticker Name

Percentage Change

Inclusion Date