recently, the semiconductor equipment industry said that TSMC's overall capacity utilization rate will also slowly pick up by the end of the year, and it is estimated that it should return to 80% in the first half of 2024.

Among them, TSMC's AI chip customers have expressed their acceptance of the company's decision to raise prices again in 2024. These customers include AMD's high-tech companies such as Selinsi, Amazon, Cisco, Google, Microsoft and Tesla. TSMC said that despite the global economic downturn, companies are eager to build their own artificial intelligence tools, so there is a huge demand for related chips.

It is important to know that TSMC's capacity utilization fluctuations coincide with the boom cycle of the entire semiconductor industry.

it is not difficult to see that this cycle is driven by the explosion of AI chip demand, which represents the direction of advanced productivity.

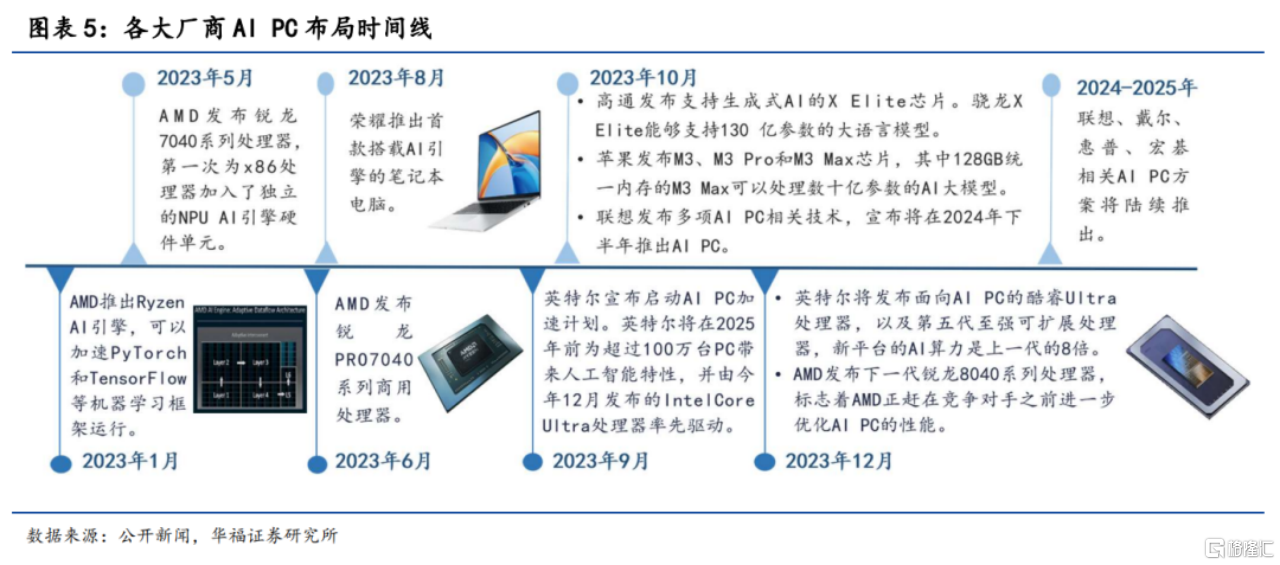

Just a few days ago, global CPU leader Intel made the biggest chip architecture change in 40 years. The idea and characteristics of chip design "tilting" to AI have been revealed.

on December 14, Intel released its first AI processor Meteor Lake, integrating NPU for the first time, bringing end-side AI computing power and enabling AI large models to run efficiently on the end side. At the same time, Intel said it would accelerate the establishment of its end-side AI ecosystem to attract PC manufacturers to join and pave the way for the development of AI PC.

this sends a clear signal that with Intel joining the war, the chip war has finally spread from the cloud to the end side, and the spotlight in the chip industry has begun to fall on the end side AI.

in the past, GPU chips used to have unlimited scenery in the cloud because of their great computing power and versatility, but now the end side, which contains "entrance" opportunities, is no longer very suitable for GPU chips, at least some clues can be seen from the cost performance.

the end side has a huge decentralized and fragmented scene, and has a rich application type. every hardware manufacturer will become the party with the entrance of the end side, and from then on, it will become the entrance of all innovative applications.

however, due to the more complex and multiple computing requirements on the end side, chips such as NPU, which are designed for special purposes and customized for specific user needs, can have the characteristics of small volume and low power consumption under large-scale mass production, thus avoiding the disadvantages of general AI chips.

therefore, it can be predicted that once the end-side AI explodes, unprecedented growth opportunities will be born in AI chips in the future, and the key increment will be on ASIC chips. It is also the reason why Intel, the "giant ship", dares to make the biggest change in 40 years. Intel needs to adapt to the new era and find a new direction for long-term development.

the essence of this new era is "AI reconstruction terminal". just as Baidu's "AI reconstruction application" has entered the AI original era, the terminal under AI reconstruction will also open a new round of innovation cycle. Big bank research also said that with the maturity of AI Agent, the scale of AI applications is imperative, is expected to promote a new round of consumer electronics innovation cycle. The meaning expressed by the two views cannot be said to be exactly the same, only exactly the same.

Where there is a need for computing power, there are chips, so the status of ASIC chips is expected to climb to a higher level in the future.

it can already be seen that AI PC, AI Pin, AI mobile phone, AI audio, MR, humanoid robot and other AI reconstructed terminals have initially shown charm and imagination to the market.

in the future, AI will gradually generalize to all kinds of intelligent terminals, which will bring about deep changes in interactive forms. unimaginable AI terminals may continue to "emerge". As these AI hardware accelerates commercialization and ushers in volume, it will stimulate demand for ASIC chips.

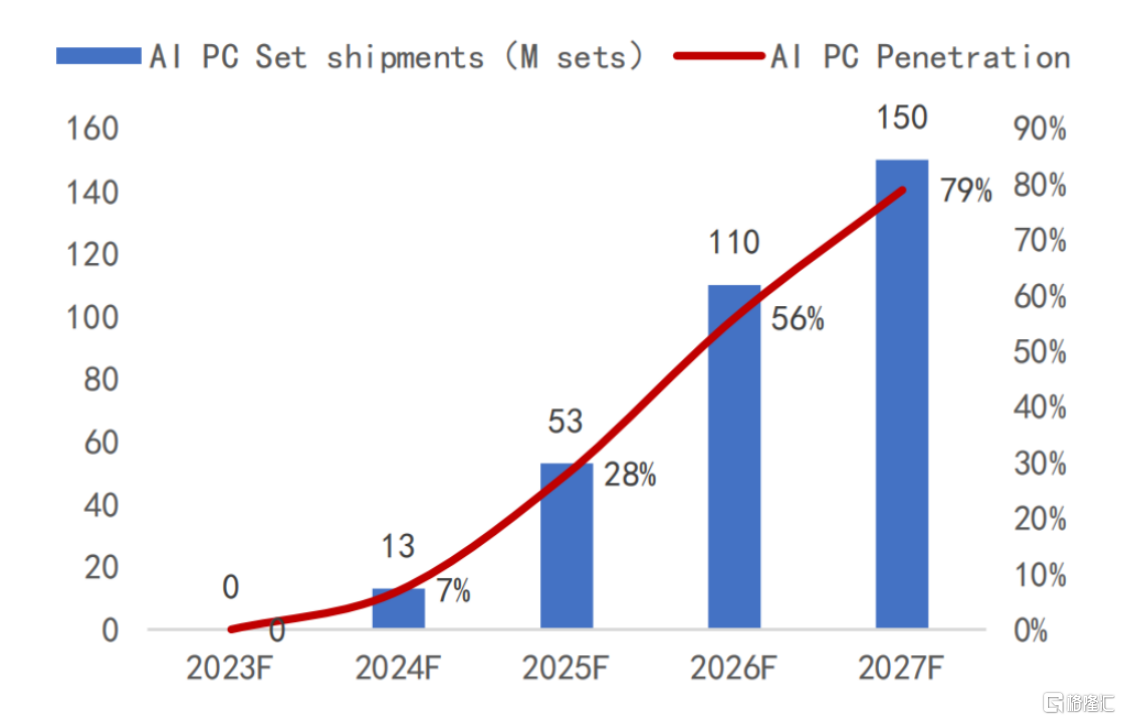

Take the AI PC. Intel officially predicts that Intel will ship more than 0.1 billion AI PCs by 2025. According to third-party forecasts, global AI PC shipments are expected to reach about 13 million units in 2024 and 0.15 billion units in 2027.

behind AI PC alone, there is a very considerable end-side AI chip market. AI mobile phones with larger shipments in the future, together with other AI ecological products, will make the demand space for end-side AI chips difficult to estimate.

In addition to the consumer side, the industrial side may also be able to expand everyone's broader imagination of ASIC chips for a simple reason-this consumption scenario has long been ignored by the market.

in the past, intelligent manufacturing in industrial 4.0 benefited from the application of technologies such as industrial internet of things, cloud computing and automation. now AI large model and end-side intelligence are expected to generate a new development path for China's manufacturing industry. AI technology and terminals are gradually integrated into production lines and equipment. factories are further unmanned and intelligent, and real unmanned factories and super factories are born.

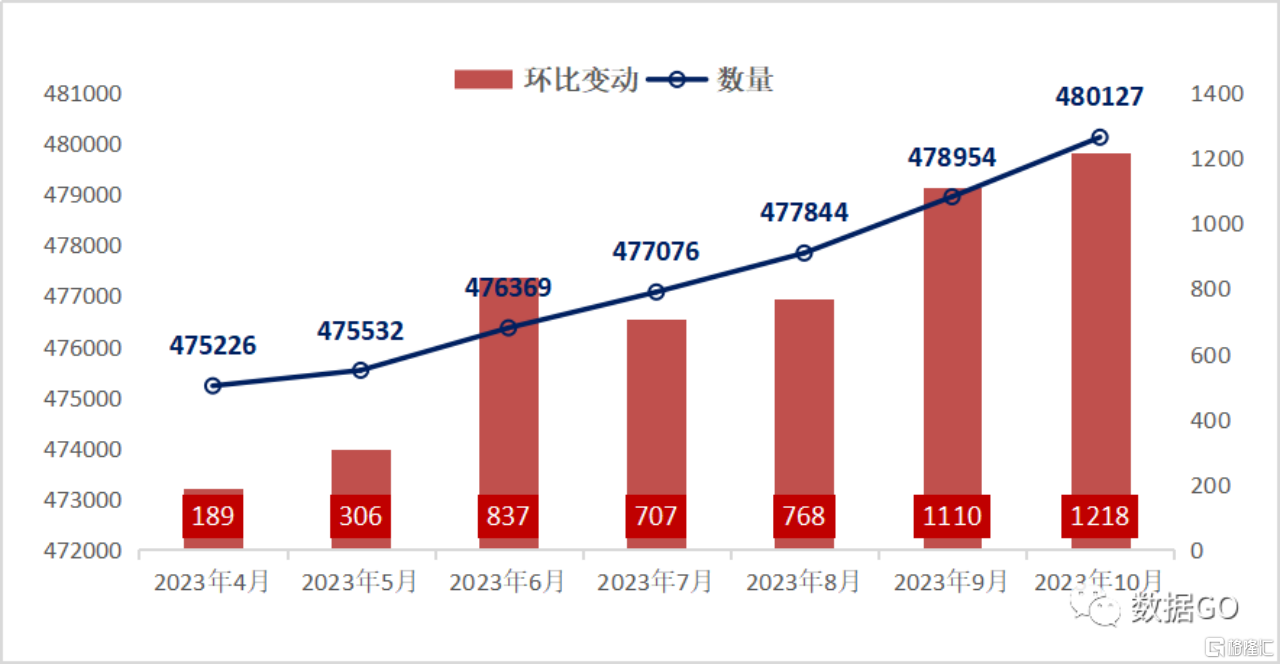

the number of manufacturing in china? if we simply assume that the ratio of an industrial enterprise to the number of its factories is 1:1, then according to the calculation, by the end of October this year, the total number of industrial enterprises above designated size in 31 provinces and cities across the country is 480127, which is the first time in history to break through 480000. From January to October, the operating income of industrial enterprises above designated size nationwide was 107.78 trillion yuan; from January to October, the total profit of industrial enterprises above designated size nationwide was 6.1 trillion yuan.

from the overall perspective, if we assume that industrial enterprises above the national scale use 1% of capital expenditure to invest in AI hardware every year (at least 10% of which is invested in the core parts to meet the demand for AI chips), we will generate an AI chip market over 100 billion scale applied to industrial scenarios.

But Rome was not built in a day. In the process of popularizing AI large models, there are two bottlenecks that must be solved. The first is computing power. Large-scale computing power must be realized at a lower cost. The second is the end side. Each factory has non-standard equipment and different computing requirements. The objective implementation environment of different factories is different. However, in the future, AI capability will eventually be localized and deployed.

this is exactly the "stage" where ASIC chips can fully display their capabilities, and it is the end-side AI opportunity that ASIC chips can seize for industrial equipment terminals. Let's boldly imagine that all factories in China will be reconstructed with AI, and how much market value ASIC chips will explode!

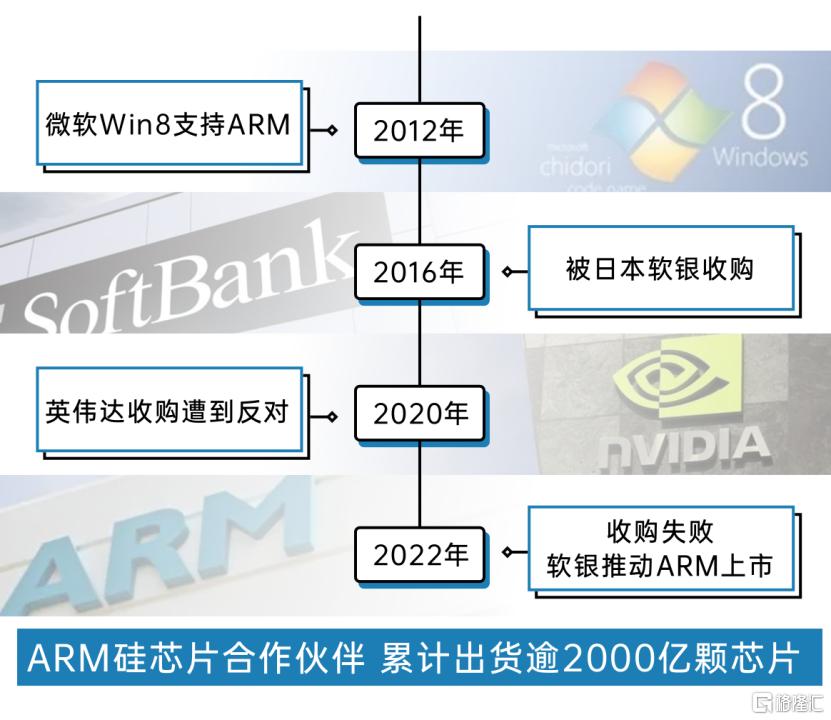

Looking back at historical development, in the PC era, the pursuit of computing speed and performance, so Intel X86 instructions and architecture almost dominate the PC chip market. In the era of mobile interconnection, more attention has been paid to the balance between computing power and power consumption. ARM, which uses low power consumption and high performance, has risen rapidly and has become the world's largest chip design leader. Its latest market has just exceeded $70 billion.

In 2008, Google released a Android operating system based on the ARM instruction set. With its open source characteristics and Google software ecology, it quickly occupied the mobile phone operating system market. In the same year, total ARM chip shipments exceeded 10 billion. The gears of fate began to turn! By the end of 2021, ARM's silicon chip partners had shipped more than 200 billion chips.

Throughout the more than 30 years of development of ARM, the reason why it has been able to turn from an unknown person into a market overlord is that it is good at seizing the opportunities of the times and making use of cooperative resources to expand the market rapidly. Its light assets, open cooperation and win-win attitude, successfully established a win-win relationship with all partners; the low power consumption characteristics of ARM processor, but also in line with the actual needs of the mobile device market outbreak period, the above all ultimately created the ARM company now brilliant.

In the coming era of artificial intelligence, will there be a new hegemon in the field of AI chips?

With the opening of a new round of innovation cycle of "AI reconstruction terminal", under the joint promotion of technological progress and demand explosion, ASIC chip field undoubtedly has the most opportunity to give birth to a new era of giants. coupled with the huge decentralization and fragmentation of end-side AI, the opportunity to become that giant will belong to more manufacturers in the industry chain.

end-side AI outbreak, the domestic related industry chain will benefit, including consumer electronics, Internet of Things end-side chips. Among them, the relevant listed companies or the most direct benefit:

jingchen shares (688099.SH): the leading SOC design enterprise in China, whose main business is the research and development, design and sales of multimedia intelligent terminal SoC chips and wireless connection chips. Related product chips have CPU and NPU computing power and are configured with strong AI performance. In 2023, Q3 achieved revenue of 1.507 billion billion yuan, up 16.60 percent year-on-year, the highest level in history. In 2023, Q4 achieved a net profit of 0.129 billion billion yuan, up 35.23 percent year-on-year.

Beijing Junzheng (300223.SZ): integrated circuit design enterprise, whose main business is the research and development and sales of ASIC chip products and overall solutions such as microprocessor chips and intelligent video chips. In 2023, Q3 achieved revenue of $1.199 billion, down 15.28 percent year-on-year and up 4.03 percent month-on-month, while net profit attributable to the company achieved $0.146 billion, down 33.74 percent year-on-year and up 36.07 percent month-on-month. The bottom of the consumer market recovered and profitability improved month-on-month this year.

cong chain group (ICG.US): a supplier of high-performance computing ASIC chips and supporting integrated software and hardware solutions will soon be able to develop in the future.The potential AI chip field, with the arrival of end-side and edge-side AI opportunities, further opens up the imagination space. The company will 0.474 billion yuan in 2022, with a compound annual growth rate of more than 90% in revenue in the past four years.

Ticker Name

Percentage Change

Inclusion Date