From the perspective of valuation level, the valuation of some Chinese medicine targets is still too high. When their performance growth fails to meet market expectations, it has intensified the concerns of the secondary market

Punctuation Finance Researcher Dong Lin

The annual performance forecast has increased, but Zhangzhou Pien Tze Huang Pharmaceutical Co., Ltd. (hereinafter referred to as Pien Tze Huang, 600436.SH) has taken a "heavy punch" in the secondary market ".

The 2023 performance forecast released by Pien Tze Huang shows that the company expects to achieve operating income of 10.035 billion yuan in 2023, a year-on-year increase of 15.42; it is expected to achieve net profit attributable to shareholders of listed companies (hereinafter referred to as net profit attributable to the parent) of 2.784 billion yuan, a year-on-year increase of 12.59%; it is expected to achieve non-net profit of 2.845 billion yuan, a year-on-year increase of 14.89%.

However, the secondary market does not recognize the "report card" in which Pien Tze Huang's revenue exceeded the 10 billion yuan mark for the first time, and both revenue and profit achieved double-digit growth. After the opening of the market on January 31, the share price of Pien Tze Huang "diving" flash collapse, near the midday close, the stock is touched the limit price of 197.55 yuan/share (before the right, the same below), a new low since August 2020.

In order to reassure investors and save the stock price, Pien Tze Huang issued an emergency forecast for the first quarter of 2024 at the noon break. The announcement shows that during the beginning of 2024, the company's product sales momentum is improving, the market shows a strong sales trend, and successfully achieved a "good start". According to the company's preliminary accounting, it is expected that in the first quarter of 2024, the company can achieve a year-on-year growth of not less than 25%.

The good news did not play a significant role. As of the close of trading on January 31, Pien Tze Huang's share price was reported at 199.4 yuan per share, a decrease of 9.16 percent, and its one-day market value shrank by more than 12 billion yuan. After two trading days, the company's share price is still a downward trend. On February 2, the share price of Pien Tze Huang hit a new low, falling as low as 180.69 yuan/share, which is nearly 63% lower than the highest price of 487.9 yuan/share hit by the company on July 21, 2021.

In fact, with the recent announcement of performance forecasts by many listed Chinese medicine companies, the expected changes in the annual report have caused the stock price of the Chinese medicine sector to fluctuate greatly. Punctuation financial researchers checked Wind data and noticed that as of January 31, of the 155 listed pharmaceutical companies whose A shares had disclosed their full-year performance forecasts, 64 had full-year pre-losses, accounting for more than 40%.

Trend of share price movements since July 2021 ($/share)

Data source: Wind

Results below expectations, 4Q net profit down 9.76

The reason why the secondary market reacted so much may be because the "report card" of Pien Tze Huang is not as glamorous on the surface.

From a single quarter point of view, the company's fourth quarter net profit attributable to the parent showed negative growth. According to the performance forecast, in 2023, Pien Tze Huang is expected to achieve operating income of 10.035 billion yuan, an increase of 15.42 percent over the same period last year; it is expected to achieve a net profit of 2.784 billion yuan, an increase of 12.59 percent over the same period last year. Comparing the company's performance data for the first three quarters, it can be calculated that in the fourth quarter of 2023, Pien Tze Huang expects operating income to be 2.435 billion yuan, up 17.18 percent year-on-year and down 4.7 percent month-on-month; it is expected to return net profit to 0.379 billion yuan, down 9.76 percent year-on-year and down 56.13 percent month-on-month.

Pien Tze Huang stated in the announcement that the increase in revenue during the period was due to the strengthening of market planning and the expansion of sales channels, and the increase in sales revenue of the company and its holding subsidiaries; the increase in profit was due to the company's core products Pien Tze Huang series products, Pien Tze Huang brand Angong The increase in sales of Niuhuang pills led to an increase in operating profit. But the company did not mention the reason for the year-on-year decline in net profit in the fourth quarter.

It is worth mentioning that the decline in net profit attributable to the parent in the fourth quarter of Pien Tze Huang occurred when the company raised prices sharply.

In May 2023, Pien Tze Huang made the largest price increase decision in history. The company raised the domestic retail price of its leading product, Pien Tze Huang ingot, from 590 yuan per grain to 760 yuan per grain, a price increase of 28.8 per cent. At the same time, the company will increase the supply price of the product by about 170 yuan/grain, and the overseas market supply price will be increased by about $35/grain.

Punctuation financial researchers noted that previously, the market generally predicted that Pien Tze Huang's annual net profit should be more than 3 billion yuan, and the growth rate should be more than 20%. Among them, Cinda Securities forecasts that the net profit of the mother of the film in 2023 will be 3.058 billion yuan, up 23.7 percent year-on-year. Huaan Securities predicts that the company's revenue in 2023 will be 10.39 billion yuan, a year-on-year increase of 19.5; the net profit attributable to the parent company will be 3.07 billion yuan, a year-on-year increase of 24.2. Obviously, after the sharp price increase, such profit growth is lower than market expectations.

And in the past month of 2024, Pien Tze Huang has handed over its first-quarter earnings forecast, which inevitably makes the market wonder, where does the company's profit growth forecast come from? In fact, from the earnings data of the past five years, the first quarter of each year is not the peak sales season for Pien Tze Huang, the last time the company achieved a net profit growth of more than 25% in the first quarter, or in 2018.

Chinese medicine sector volatility

on January 31, except for the drop limit of pien zehuang, the whole Chinese medicine sector fell across the board, with the wande Chinese medicine index falling 4.87 per cent on that day. Among them, Dali Pharmaceutical (603963.SH) and Longjin Pharmaceutical (002750.SZ) fell by the limit, Tonghua Jinma (000766.SZ) fell by 7.75, Tongrentang (600085.SH) fell by 6.96, Zhongsheng Pharmaceutical (002317.SZ) fell by 6.87, and Yiling Pharmaceutical (002603.SZ) fell by 6.46.

Punctuation financial researchers noted that with the recent announcement of performance forecasts by a number of listed Chinese medicine companies, the expected changes in the annual report have caused large fluctuations in the stock price of the Chinese medicine sector.

On January 30, Tongrentang issued a performance forecast. The company expects to achieve a net profit of 1.568 billion yuan to 1.668 billion yuan in 2023, an increase of 10% to 17% year-on-year; it is expected to achieve a non-net profit of 15.39 to 1.639 billion yuan, an increase of 10% to 17.2%. As in the case of the film, in the return of the mother net profit to achieve double-digit growth, Tongrentang's share price on the day also ended with a "down stop.

Dong 'e Jiao (000423.SZ) and Guangyuyuan (Rights Protection)(600771.SH), whose performance growth exceeded expectations, saw a significant rise in the company's share price after the disclosure of the performance forecast. On Friday, January 26, Dong 'e Ejiao issued a performance forecast. The company expects to achieve a year-on-year increase of 41% to 49% in net profit for the whole year. At the close of the market on Monday, the share price of Dong 'e Ejiao rose 5.64 percent. Guangyuyuan announced on January 29 that the company expected its annual net profit to turn losses into profits. At the close of January 30, the stock rose 9.98 percent.

Some analysts in the industry believe that from the perspective of valuation levels, the valuations of some Chinese medicine targets are still too high, and their performance growth has failed to meet market expectations, which has intensified the concerns of the secondary market. Secondly, for the Chinese medicine sector, policy support has always been an important factor in its performance growth. At present, the successive implementation of the policy of centralized collection of proprietary Chinese medicines, coupled with the continuous rise in the cost of medicinal materials, will have an impact on the operating performance of relevant listed companies to a certain extent.

64 pharmaceutical companies full-year performance pre-loss

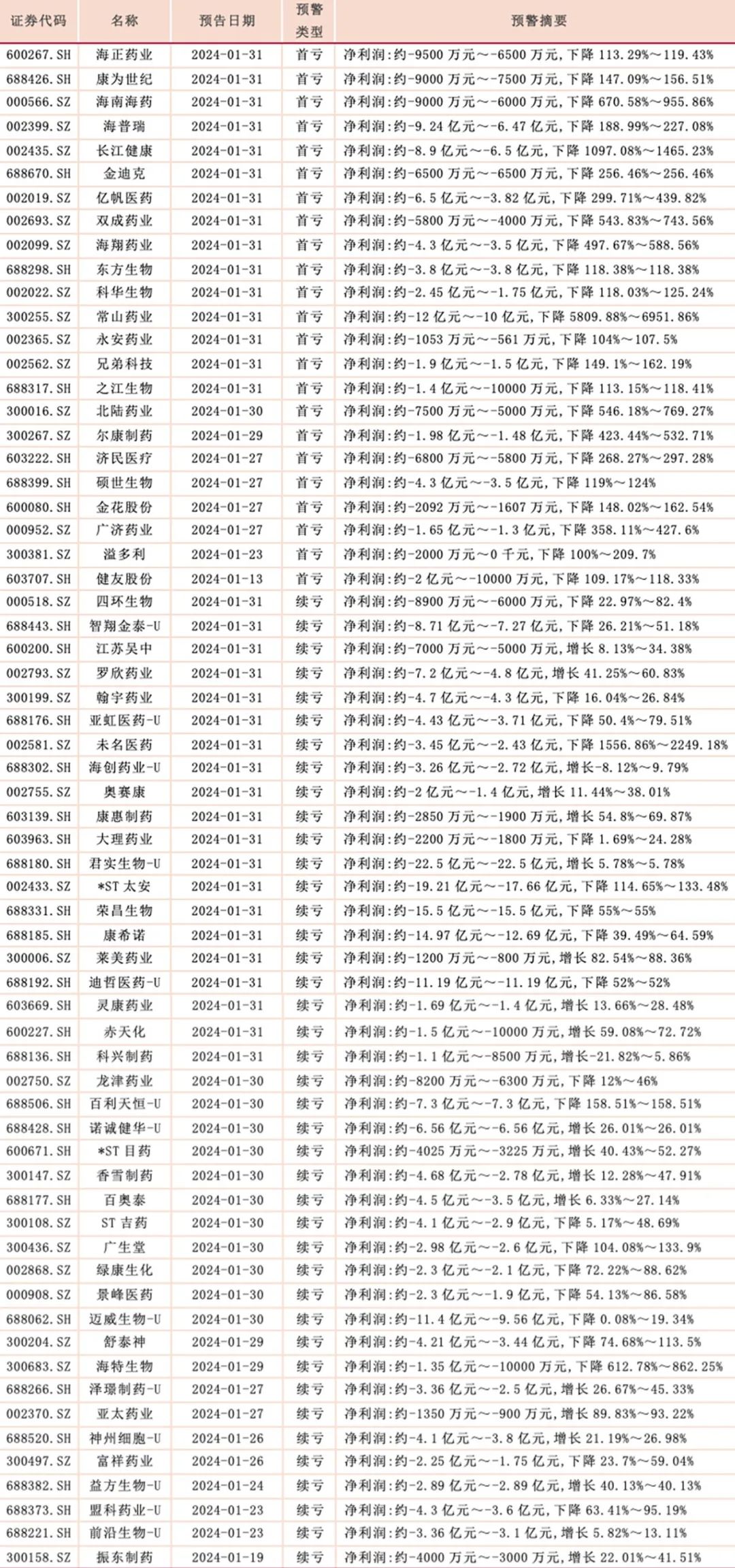

punctuation financial researchers looked up Wind data and found that as of January 31, 155 enterprises in the-share pharmaceutical sector had issued 2023 performance forecasts, of which 88 enterprises were expected to make profits for the whole year and 64 enterprises were expected to make losses for the whole year, accounting for more than 40%. Of the 64 pre-loss enterprises, 23 suffered the first loss and 41 continued to lose.

Among them, China Resources Sanjiu (000999.SZ) is the pharmaceutical company with the highest profit expected for the whole year. The company expects to achieve a net profit of 2.818 billion yuan to 3.065 billion yuan in 2023, an increase of 15.08 to 25.16 percent over the same period last year, compared with a profit of 2.449 billion yuan in the same period last year; it is expected to achieve a net profit of 2.678 billion yuan to 2.888 billion yuan, an increase of 20.69 to 30.15 percent over the same period last year, compared with a profit of 2.219 billion yuan in the same period last year.

the most serious loss is junshi biology-U(688180.SH). the company expects to realize a net profit loss of 2.25 billion yuan in 2023, a decrease of 0.138 billion yuan and a decrease of 5.78 percent compared with the same period last year. It is estimated that the net profit loss of non-returning parent will be 2.279 billion yuan, 0.171 billion yuan less than the same period last year, and 6.99 less than the same period last year.

from the point of view of the first loss of enterprises, Changshan Pharmaceutical (Rights)(300255.SZ), Changjiang Health (002435.SZ), Haipurui (002399.SZ) three enterprises with the largest loss range, is expected to return to the parent net profit loss of more than 0.6 billion yuan in 2023. Judging from the enterprises that continued to lose money, Junshi Biology-U, * ST Taian (Rights Protection)(002433.SZ), Rongchang Biology (688331.SH), Kangxinuo (688185.SH), Dizhe Medicine (688192.SH) and Maiwei Biology (688062.SH) have the largest losses. The above six pharmaceutical enterprises expect the net profit losses of 2023 to be above 1 billion yuan.

Relevant agencies stated that since 2023, the adverse effects of pharmaceutical policies and medical reform processes on the industry have tended to weaken, and achieving high-quality development has always been the focus of the industry. Industry research and development investment continues to increase, transformation and upgrading, quality and efficiency, to achieve a virtuous circle of research and development innovation trend is obvious.

Although the main economic indicators of industries and enterprises declined in the first three quarters of 2023, it is expected that the high base effect will be gradually digested throughout the year. With the support of a good external environment and rigid demand, industries and enterprises are expected to gradually return to growth in 2024. The pharmaceutical industry has always maintained greater development resilience and potential, and the credit fundamentals of the pharmaceutical manufacturing industry remain stable.

64 pharmaceutical companies release 2023 performance pre-loss announcement

Data source: Wind

Ticker Name

Percentage Change

Inclusion Date