Transfer from: Prospective Industry Research Institute

major listed companies in the industry: mainly Chujiang new materials (002171.SZ); Antai Technology (000969.SZ); There are research powder materials (688456.SH); Silver Jubilee Technology (300221.SZ); Platinum (688333.SH); Yinbang shares (300337.SZ); Yue 'an New Material (688786.SH) etc.

The core data of this article: market size, competition pattern, production and sales scale

Industry Overview

1. Definition

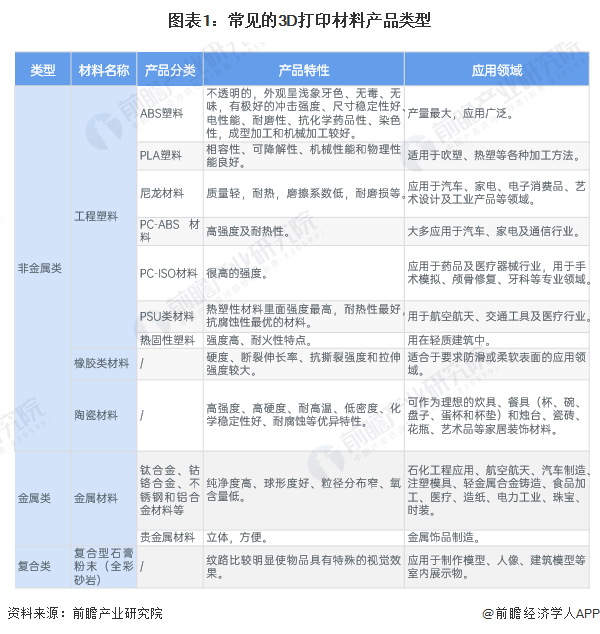

There are many products that can be used as 3D printing materials, mainly including non-metallic, metallic, and composite materials.

2. Industry chain analysis: rich product types in the middle reaches

The upper reaches of my country's 3D printing material industry are mainly basic material mining, smelting, and processing enterprises, including non-ferrous metal smelting, rubber processing, plastic processing, etc.; the middle reaches are 3D printing material processing and manufacturing enterprises, which are divided into metal materials, non-metal materials and Three major sectors of composite materials; downstream applications include medical and health, aerospace, building materials, and automobiles.

from the ecological map of the industrial chain, the upstream related enterprises include Baosteel group (non-ferrous metals), Hainan rubber (rubber processing) and baoshuo profile (plastic processing); The mid-stream related enterprises include yue 'an new materials (metal materials), huashu high-tech (non-metal materials) and yinbang shares (composite materials). Downstream enterprises are mainly used in BMW (automobile), Meirui Medical (medical health) and other fields.

Industry development history

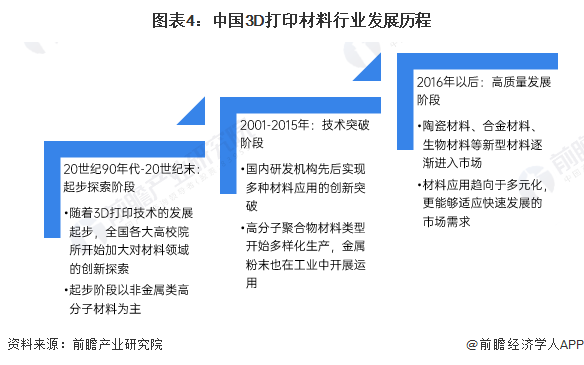

3D printing material is an important material basis for the development of 3D printing technology. Material technology is the core of 3D printing technology, which directly affects the development process of 3D printing. The development of 3D printing materials With the development of 3D printing technology, we continue to achieve innovative breakthroughs, and gradually develop breakthroughs in the direction of diversification, high performance, and intelligence from the beginning of polymer materials. After the rapid development of the early 21st century, China's 3D printing materials industry is entering a stage of high-quality development.

Industry policy background

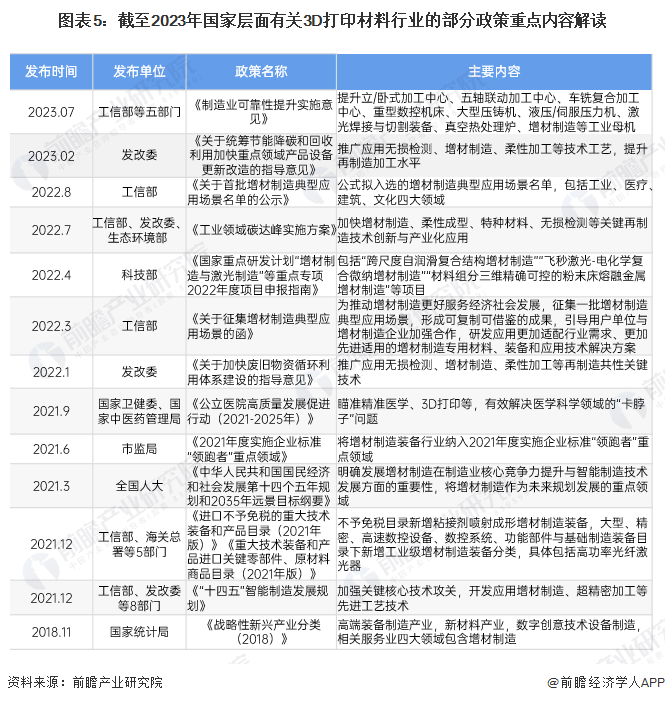

China attaches great importance to the development of 3D printing industry. In November 2018, the National Bureau of Statistics issued the Classification of Strategic Emerging Industries (2018), incorporating 3D printing equipment manufacturing into strategic emerging industries. In June 2021, the additive manufacturing equipment industry will be included in the key areas of the "leader" in the implementation of enterprise standards in 2021. In addition, China has also formulated relevant policies to promote the application of 3D printing technology in medical, construction, remanufacturing and other fields.

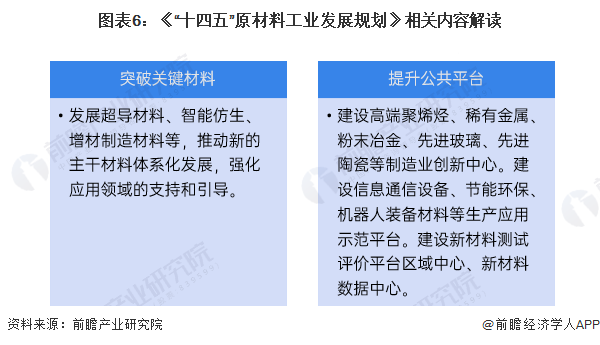

The "14th Five-Year Plan for the Development of the Raw Material Industry" clearly states that by 2025, key material support capabilities will be improved, public service capabilities will be significantly improved, and more than 10 new material platforms will be built.

Industry development status

1. The technical level of some domestic enterprises can be comparable to that of international leaders

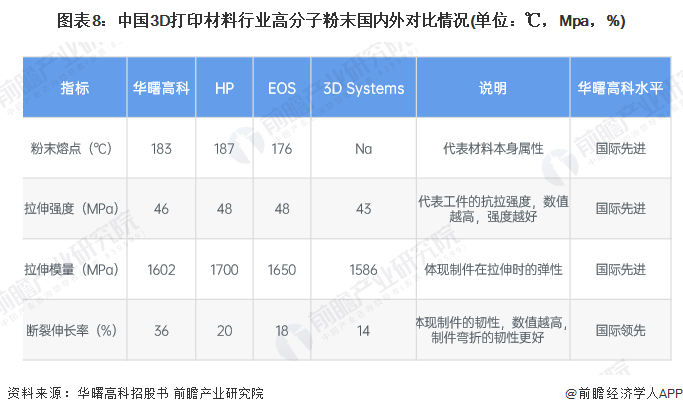

According to the prospectus of Platinum, the relevant technical indicators of its titanium alloy powder are basically equivalent to those of TLS in Germany. Reflect the domestic 3D printing material metal material has reached the export standard, in the domestic and international are competitive.

According to the prospectus (application draft) of Huashu Hi-Tech, compared with similar products of comparable listed companies in the same industry, the key performance indicators such as thermal deformation temperature, tensile strength, tensile modulus, bending strength and bending modulus are similar, which are in the international advanced level, and the elongation at break is better than similar products, reaching the international leading level.

On the whole, my country's 3D printing materials are developing rapidly, and domestic and foreign products have reached a consistent level in specific fields such as titanium alloy powder and polymer powder, and even domestic companies have a leading edge.

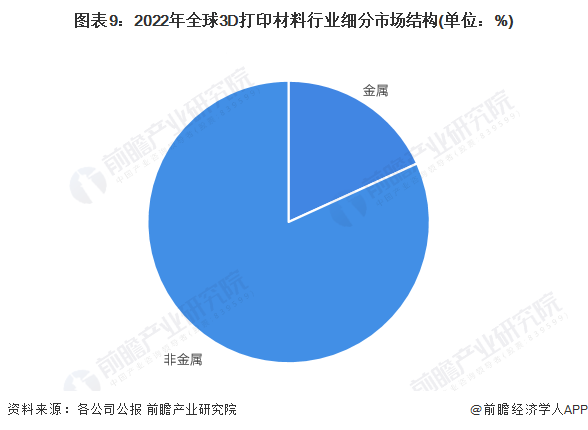

2, non-metallic materials occupy the main market share

the domestic market segment structure of 3D printing materials is roughly similar to the global structure. according to Wohler's Associates data, non-metallic 3D printing materials will account for more than 80% in 2022, of which polymer materials are the most widely used, accounting for 59% of the market of 3D printing materials.

3. the market size of 3D printing materials exceeds 8 billion yuan

The 3D printing material industry is an important foundation of the 3D printing industry. According to CCID data, the scale of China's 3D printing industry will reach 26.15 billion billion yuan in 2021. Preliminary statistics exceed 34 billion yuan in 2023, and the total proportion of 3D printing materials in the total scale of 3D printing industry is between 20% and 30%. Preliminary estimates show that the market scale of China's 3D printing materials industry will exceed 8 billion yuan in 2023.

Industry competition landscape

1, regional competition pattern

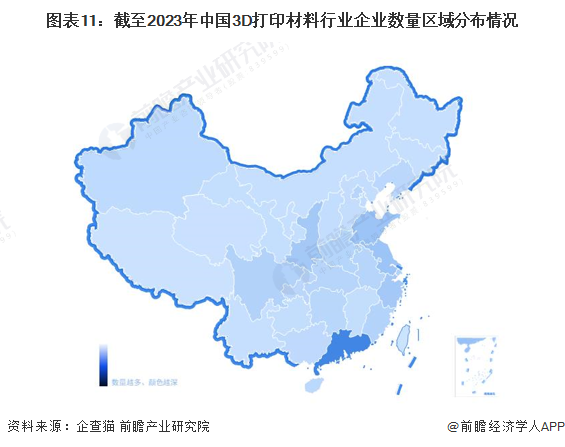

According to the data of the enterprise search cat, the registered enterprises of 3D printing materials in China are mainly distributed in Guangdong Province. Followed by Shandong, Jiangsu and other coastal cities; Shaanxi Province, the number of 3D printing materials enterprises is also more.

Note: The darker the color, the more the number of enterprises.

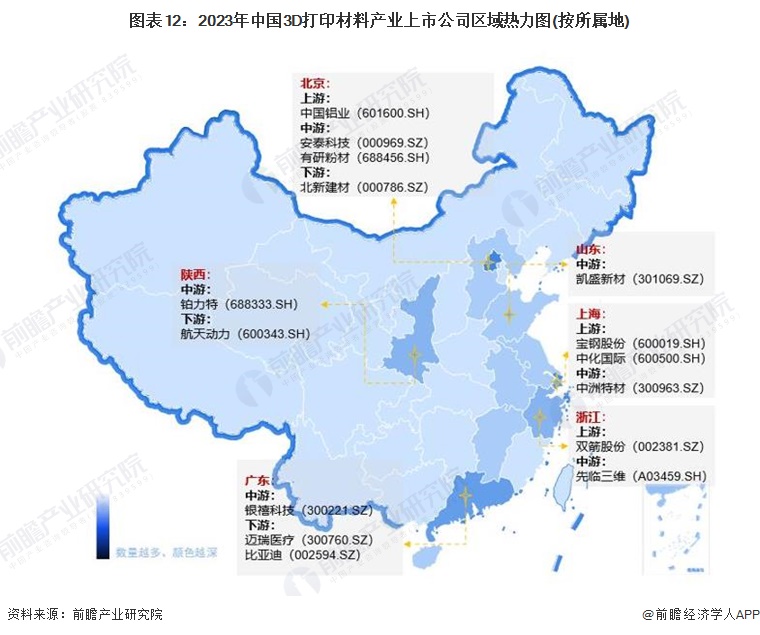

judging from the regional distribution of listed companies in the 3D printing material industry, Beijing has the largest number of listed companies in the 3D printing material industry, including Antai technology (000969.SZ), research powder (688456.SH) and other midstream enterprises. There are also a large number of listed companies in the 3D printing materials industry in Shanghai and Guangdong, with the former having midstream companies such as Zhongzhou Special Materials (300963.SZ) and the latter having midstream listed companies such as Jubilee Technology (300221.SZ).

Note: Darker color means more quantity.

2, enterprise competition pattern

at present, major domestic listed enterprises of 3D printing materials have different statistical standards for their businesses. most large enterprises have not yet disclosed the statistical standards for 3D printing materials business. therefore, listed enterprises related to 3D printing materials business are integrated and statistics are made according to the 2022 revenue of disclosed standard materials business or 3D printing materials business (if any). chujiang new materials, shengquan group and other enterprises are in the leading position in the industry in terms of revenue scale.

Note: Due to the different caliber of financial disclosure, the data of large-scale metal, plastic and other material manufacturers such as Chujiang New Material are relatively large.

Industry development prospects and trend forecast

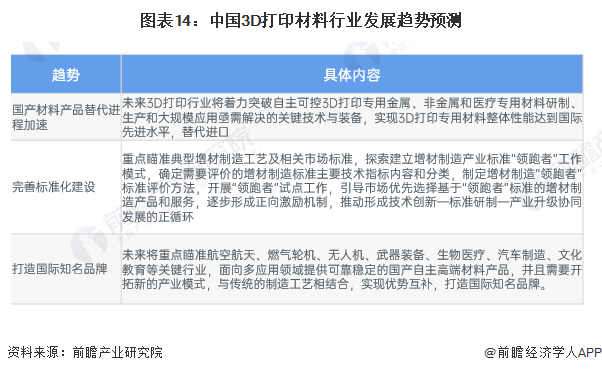

1, the industry to accelerate the development of domestic substitution process to accelerate

With the acceleration of China's localization and the gradual improvement of the standardization system, the future trends of China's 3D printing material industry are as follows:

2. 3D printing material market is about to exceed 10 billion

it is expected that the growth momentum of the 3D printing industry will change from 3D printing equipment to dual-drive equipment and materials in the next few years. the demand for 3D printing materials will grow rapidly. the scale of China's 3D printing materials industry will exceed 10 billion yuan in 2025 and reach 18.7 billion yuan in 2029.

For more research and analysis of this industry, please refer to the "China 3D Printing Material Industry Market Outlook and Investment Strategic Planning Analysis Report" by the Foresight Industry Research Institute.

at the same time, the prospective industrial research institute also provides solutions such as industrial big data, industrial research report, industrial planning, park planning, industrial investment promotion, industrial map, intelligent investment promotion system, industry status certificate, IPO consultation/feasibility study of investment raising, IPO working paper consultation, etc. Citing the contents of this article in any public disclosure such as the prospectus and the company's annual report requires formal authorization from the Prospective Industry Research Institute.

More in-depth industry analysis can be found in [Prospective Economist APP], and you can also interact with 500 economists/senior industry researchers. More enterprise data, enterprise information and enterprise development are all in [enterprise search cat APP], the most cost-effective and most functional enterprise query platform.

massive information and accurate interpretation are all available on Sina financial APP

Ticker Name

Percentage Change

Inclusion Date