interface news reporter Tao zhixian

Interface News Editor Chen Fei Ya

With the disclosure of the 2023 annual report and the 2024 quarterly report, investors seem to be dissatisfied with the "performance" of the photovoltaic industry. Leading company Longji Green Energy (601012.SH) has lost money for two consecutive quarters, and its share price is close to a new low for the year. The share price of star company Tongwei (600438.SH) even hit a new annual low, and its market value has fallen below 100 billion yuan.

The photovoltaic industry has once again become the most concerned topic in the market.

The end of the era

The era of rapid growth in photovoltaics is over . Global PV installations will exceed 400GW in 2023, a significant increase of more than 70% over 2022. Among them, China's photovoltaic new installed capacity of 216, an increase of 148.1 over 2022, the new installed capacity and growth rate are a record high. According to the International Energy Agency (IEA) forecast, the installed capacity of photovoltaic systems will increase by only 8% in 2024, significantly lower than the 70% increase in 2023. Longji Green Energy also believes that global PV demand will increase in 2024, but the growth rate will slow down.

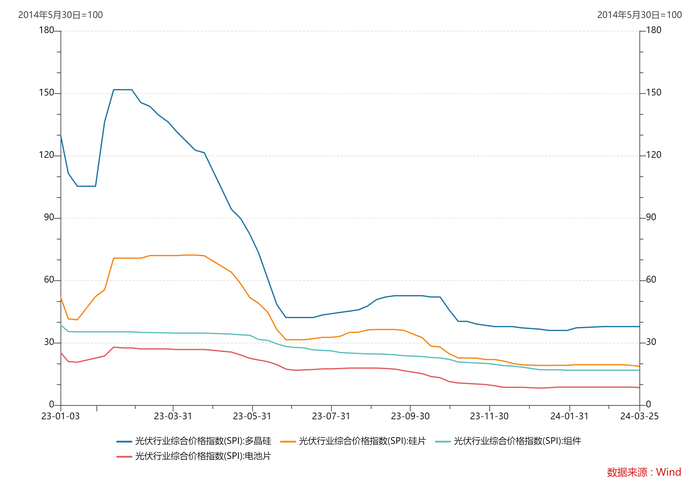

Demand has skyrocketed, while PV prices have plummeted. From 2023 to the first quarter of this year, the prices of all links in the photovoltaic industry chain fell sharply. The composite price index for silicon, silicon wafers, batteries and components fell by 71%, 64%, 67% and 56%, respectively, from 130.03, 52.1, 25.36 and 38.55 in early 2023 to 37.77, 18.63, 8.45 and 16.78, respectively, and hit a new low in recent years.

photo source: WIND, interface news research department

The most hurt by the sharp drop in prices is the leader of each sub-industry chain. As silicon and battery chips fell the most, silicon, battery double dragon head Tongwei shares performance is naturally the most "injured".

Tongwei's revenue in 2023 was 139.1 billion yuan, down 2.33 percent from the same period last year; net profit attributable to its parent was 13.6 billion yuan, down 47.25 percent from the same period last year; revenue in the first quarter of this year was 19.6 billion yuan, down 41.13 percent from the same period last year; and net profit loss attributable to its parent was 0.787 billion yuan, down 168 percent from the same period last year. It is worth mentioning that the company's revenue in the fourth quarter of 2023 was 27.7 billion yuan, down 31.37 percent from the same period last year, and net profit loss was 2.728 billion yuan, down 109 percent from the same period last year.

Aixu shares (600732.SH), the second largest market share of battery chips, also performed poorly. In 2023, the company's revenue was 27.2 billion yuan, down 23% year-on-year; the net profit attributable to the parent was 0.757 billion yuan, down 68% year-on-year; the revenue in the first quarter of this year was 2.5 billion yuan, down 68% year-on-year; the net profit loss attributable to the parent was 0.09 billion yuan, down 113 year-on-year.%. The company's revenue in the fourth quarter of 2023 was 4.55 billion yuan, down 51% year-on-year; net profit loss was 1.13 billion yuan, down 220 percent year-on-year.

After silicon and battery chips, silicon chip prices ranked third with a 64% decline, and its industry leader is having a hard time. TCL Central (002129.SZ) revenue in 2023 was 59.1 billion yuan, down 11.74 percent from a year earlier; net profit attributable to its parent was 3.4 billion yuan, down 50 percent from a year earlier; revenue in the first quarter of this year was 9.9 billion yuan, down 43.62 percent from a year earlier; and net profit loss attributable to its parent was 0.88 billion yuan, down 139 percent from a year earlier. The company's revenue in the fourth quarter of 2023 was 10.5 billion yuan, down 39% year-on-year; net profit loss was 2.772 billion yuan, down 252 percent year-on-year.

Persistent Involved

"Involved" is the core reason for this round of price plunge. it stands to reason that under the soaring demand, the whole industry should present a bull market in prices. however, the fact is that the rising price is getting worse and worse. the root cause is the rapid expansion of the industry and the imbalance of supply and demand structure. In recent years, with the strong support of capital, photovoltaic new expansion investment projects have been fast, upstream and downstream production capacity has been greatly expanded, and a large number of cross-border people have poured in, resulting in a sharp increase in production capacity in various links in the short term, and the imbalance between supply and demand is prominent. In this context, the price of photovoltaic products fell sharply in 2023, especially since the fourth quarter of 2023, the bidding price of modules has repeatedly hit new lows, and the price of modules has fallen below 1 yuan per watt. Disorderly low-price competition has greatly damaged the profitability of various enterprises.

For the long bear market, Longji Green Energy said that the entire industry is currently in a state of loss, due to many links and even a state of loss of cash.

When the bear market will end seems a long way off. Longji Green Energy expects industry-wide losses to be difficult to resolve in the short term, but not to get worse. With regard to the duration of the downturn and the timing of the inflection point, it is difficult to predict at present, and if no special events occur, painstaking preparations may still be needed.

Under the internal volume, the performance of components naturally declined across the board. Jingao Technology (002459.SZ), one of the "four leaders" of the components, had revenue of 81.6 billion yuan in 2023, up 12% year-on-year; net profit attributable to the parent was 7 billion yuan, up 27% year-on-year; revenue in the first quarter of this year was 16 billion yuan, down 22% year-on-year; net profit loss attributable to the parent was 0.48 billion yuan, down 119 percent year-on-year. The company's revenue in the fourth quarter of 2023 was 21.6 billion yuan, down 8.83 percent year-on-year; net profit was 0.275 billion yuan, down 119 percent year-on-year.

Alternate tap

The dramatic changes in the industry have brought about not only losses, but also the alternation of internal patterns.

photovoltaic "total rudder owner" Longji green energy fell behind. Longji's 2023 revenue was 129.5 billion yuan, up only 0.39 percent year-on-year; its net profit was 10.75 billion yuan, down 27.41 percent year-on-year; its revenue in the first quarter of this year was 17.7 billion yuan, down 37.59 percent year-on-year; and its net profit loss was 2.35 billion yuan, down 165 percent year-on-year. It is worth mentioning that the company's revenue in the fourth quarter of 2023 was 35.4 billion yuan, down 16% year-on-year; net profit loss was 0.942 billion yuan, down 125 percent year-on-year. From 2020 to 2022, the best component manufacturer for three consecutive years, fell to third in 2023.

Trina Solar (688599.SH) revenue in 2023 was 113.4 billion yuan, up 33% year-on-year; net profit attributable to parent was 5.53 billion yuan, up 50% year-on-year; revenue in the first quarter of this year was 18.3 billion yuan, down 14.37 percent year-on-year; net profit attributable to parent was 0.516 billion yuan, down 71% year-on-year. The company's revenue in the fourth quarter of 2023 was 32.3 billion yuan, up 20.18 percent year-on-year, while net profit was 0.454 billion yuan, down 64.48 percent year-on-year. Although Trina Solar has also declined, it is at least profitable in the fourth quarter of 2023 and the first quarter of this year. On the other hand, Longji Green Energy has lost money for two consecutive quarters.

in this round of photovoltaic cycle, the best performance is the former king jingke energy (688223.SH), the "former king" who has been firmly in the component industry leader until 2020 has been killed back. The company's revenue in 2023 was 118.7 billion yuan, up 43.55 percent from the same period last year; its net profit was 7.44 billion yuan, down 153 percent from the same period last year; its revenue in the first quarter of this year was 23.1 billion yuan, down 0.3 percent from the same period last year; and its net profit was 1.176 billion yuan, down 29 percent from the same period last year. The company's single-quarter revenue in the fourth quarter of 2023 was 33.6 billion yuan, up 12.31 percent from a year earlier, while net profit was 1.086 billion yuan, down 14 percent from a year earlier.

In terms of shipments, Jingke Energy sold 83.56GW of photovoltaic products in 2023, including 78.52GW of shipped components. According to data Consulting by InfoLink, the company ranked first in the industry in component shipments.

Jingke Energy can return to the throne by new technology. From 2020 to 2022, Longji Green Energy by virtue of 166, 182 silicon wafer size technology iteration of the opportunity to overtake Jingke Energy, and in 2023, Jingke Energy "heavy warehouse" N-type Topcon battery components, by virtue of capacity advantages low-cost snatch the market, back to the industry first.

For the photovoltaic industry, time is the best "antidote". with the cancellation of the fixed increase plan of 16 billion yuan by tongwei shares in September 2023, the expansion cycle of the industry has ended, the internal volume will not intensify, and the whole industry is close to the bottom. From the emotional side, Longji Green Energy, Tongwei shares and Jingke Energy's price-to-book ratio is only 2 times, 1.66 times and 2.19 times, whether from a 3-year, 5-year or 10-year perspective, the company's valuation is lower than 95% of the time, "left" investment value is obvious.

Ticker Name

Percentage Change

Inclusion Date