log on Sina financial APP to search [letter cover] to see more evaluation grades

Transfer from: Prospective Industry Research Institute

Major listed companies in the industry: China Railway (601766.SH), China Railway (601390.SH), Connie Electromechanical (603111.SH), Jinxi Axle (600495.SH), China Tong (688009.SH), Xinzhu Stock (002480.SZ), etc.

The core data of this article: the market competition echelon of the rail transportation equipment industry;

China rail transportation equipment industry market competition echelon

Based on the revenue from the rail transit equipment business, China's rail transit equipment industry can be divided into three competitive echelons. The first echelon of enterprises is CRRC, with annual business income exceeding 100 billion yuan. The business income of the second echelon enterprises is between 100 and 100 billion yuan, including China Railway and China Tong. The business income of the third echelon enterprises does not exceed 10 billion yuan, including Connie Electromechanical, Jinxi Axle, Xinzhu Stock, Jinchuang Group, Brilliant Technology, etc.

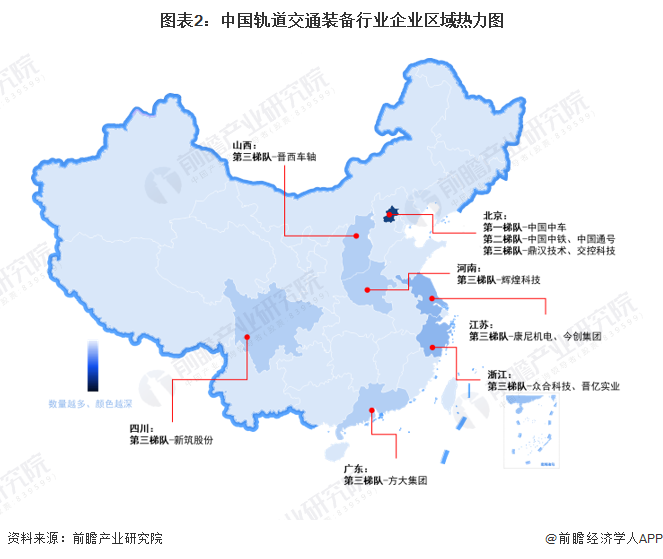

From the perspective of regional distribution, the first and second echelon of rail transit equipment industry enterprises are concentrated in Beijing, and the third echelon enterprises are distributed in Shanxi, Henan, Jiangsu, Zhejiang, Guangdong, Sichuan and other regions.

China Rail Transit Equipment Industry Market Ranking

in 2023, the national EMU issued a total of 7 tender announcements, a total of 268 groups. Judging from the winning bid, CRRC Qingdao Sifang won the largest number of bids, reaching 62 groups. The second is the consortium of CRRC Zhuji and CRRC Nanjing, with a total of 52 winning bids. From the holding situation of the winning enterprises, all the enterprises of the winning EMU are controlled by China.

In 2023, the total bid amount for urban rail transit vehicles nationwide will reach 45.87 billion yuan. Among them, CRRC Changchun won the highest bid, reaching 15.414 billion yuan; CRRC Qingdao Sifang and CRRC Nanjing ranked second and third respectively, with the bid winning amounts of 10.26 billion yuan and 9.335 billion yuan respectively. Judging from the holding situation of the winning companies, 6 of the 7 winning companies are controlled by CRRC. Combined with the winning bid of railway vehicles, it can be found that CRRC has a high market share and monopoly competitive strength in the rail transit vehicle market.

Market Share of China Rail Transit Equipment Industry

in 2023, in terms of railway vehicles, the market share of Qingdao Sifang ranked first, accounting for 23.13 percent; the market share of the consortium of Zhongche Zhuji and Zhongche Nanjing ranked second, accounting for 19.40 percent; and Zhongche Changchun ranked third, accounting for 18.66 percent.

In 2023, in terms of urban rail transit vehicles, CRRC Changchun ranked first in market share, accounting for 33.60 per cent; secondly, CRRC Qingdao Sifang and CRRC Nanjing ranked second and third respectively, with market shares of 22.37 per cent and 20.35 per cent respectively.

Summary of the competitive status of China's rail transit equipment industry

from the perspective of the five-force competition model, there is a surplus supply of raw materials in the upstream of the industry and the specificity of parts is strong, resulting in the average bargaining power of upstream suppliers. The buyers who have demand for rail transit equipment in the downstream of the industry are single and mainly central state-owned enterprises, resulting in strong bargaining power of the downstream demanders. Within the industry, there are fewer participants in the vehicle field and the leading enterprises have obvious advantages, with average fierce competition, however, there are many participants in the manufacture of important equipment and systems and the variety of products supplied is rich, and the competition is fierce; the overall capital, technology and resources of the industry are relatively high, but the enterprises that lay out vehicle manufacturing may pose a certain threat to the enterprises that lay out important equipment and systems. Rail transit equipment itself is the main carrier of national public transportation and bulk transportation, and there is no threat of substitutes for the time being. The main threat comes from the upgrading of internal product technology.

According to the above analysis, the competition in all aspects is quantified, 1 represents the largest and 0 represents the smallest. At present, the five forces of competition in China's rail transit equipment industry are summarized as follows:

For more research and analysis of this industry, please refer to the "China Rail Transit Equipment Industry Development Trend and Market Segment Investment Prospect Analysis Report" by the Prospective Industry Research Institute.

at the same time, the prospective industrial research institute also provides solutions such as industrial big data, industrial research reports, industrial planning, park planning, industrial investment promotion, industrial mapping, intelligent investment promotion system, industry status certificate, IPO consultation/feasibility study of fund-raising and investment, and application of specialized and special new small giants. Citing the contents of this article in any public disclosure such as the prospectus and the company's annual report requires formal authorization from the Prospective Industry Research Institute.

more in-depth industry analysis can be found in [prospective economist APP], and you can also communicate and interact with 500 + economists/senior industry researchers. More enterprise data, enterprise information and enterprise development are all in [enterprise search cat APP], the most cost-effective and versatile enterprise query platform.

Ticker Name

Percentage Change

Inclusion Date