Chapter 1 Industry Overview

The home theater and audio industry refers to a comprehensive industry with home entertainment audio-visual system as the core, covering a series of economic activities such as equipment research and development, production, sales, installation, commissioning, maintenance, and providing related consulting and services. The industry is committed to creating a high-quality, immersive movie-watching experience for consumers at home, integrating technology, art and quality of life improvement, with the characteristics of innovation, experience and service. It mainly includes: R&D and production of home theater equipment, such as audio, projectors, screens, intelligent control systems, etc.; Installation and commissioning services for home theater systems to ensure optimal equipment performance; Maintenance and upgrade of home theater equipment to extend the service life of the equipment and improve the viewing effect; Consulting and design of home theater solutions, providing personalized customized services according to customer needs; and market activities such as equipment sales, leasing, and after-sales service formed around home theaters. In real life, people usually refer to the industry engaged in the sales, installation and service of home theater equipment as the home theater and audio industry.

Figure Home theater and audio industry chain

Source: Asset Information Network Qianji Investment Bank

According to the latest release of the industry observer, the total number of home theater-related enterprises in China has reached about 300,000. The number of newly registered enterprises in 2021 was 45,000, an increase of 12% over the previous year, showing the continued vitality within the industry. In the same period, the number of enterprises cancelled or revoked was 12,000, a year-on-year increase of 8%, and the number of net growth enterprises was 33,000. In terms of geographical distribution, Guangdong Province ranks first in the country with 52,000 enterprises, followed by Zhejiang, Jiangsu, Beijing and Shanghai with 31,000, 28,000, 21,000 and 19,000 respectively.

In terms of registered capital, in the home theater industry, the number of enterprises with registered capital of less than 500,000 yuan is the largest, accounting for 32%, reflecting the characteristics of start-ups and small and medium-sized enterprises in the industry. Enterprises with registered capital of 500,000-2 million yuan and 2 million-5 million yuan account for 25% and 18% respectively, while enterprises with registered capital of 5 million yuan and above account for 25%, showing that there are also a certain number of large-scale enterprises in the industry.

According to recent market research, with the improvement of residents' living standards and the diversification of home entertainment needs, home theater systems have gradually become the standard configuration of many families. Although there is no official comprehensive statistics on the number of employees, according to incomplete statistics, more than one million people are directly or indirectly engaged in the design, installation, maintenance and product sales of home theaters, and this number continues to grow with the popularization of the concept of smart home.

In 2021, the scale of China's home theater market will reach about 30 billion yuan, a year-on-year increase of 7%. Among them, the high-end customized home theater system has a particularly significant growth rate of 10% due to its personalized service and excellent experience. In contrast, the low-end market is affected by cost control and price wars, and the growth is relatively flat, about 5%. In terms of product types, smart projection, surround sound, and high-definition large-screen TVs have become the main hot spots for consumers to buy.

From the perspective of market trends, the construction and installation volume of the home theater industry will reach 800,000 units in 2021, a year-on-year increase of 6%, reflecting consumers' demand for improving the quality of home entertainment environments. About 60% of the new projects started (i.e. new home theater installations) are concentrated in mid-to-high-end residential areas in cities, while the rural and small town markets, although they started late, have huge growth potential, with a year-on-year increase of 12%. 720,000 home theater systems were completed and put into use, an increase of 8% year-on-year, indicating that the market demand is strong and the project implementation efficiency is high. It is worth noting that the home theater industry has made significant progress in technological innovation in 2021, including the wide application of advanced audio technologies such as 4K/8K ultra-high-definition display technology, Dolby Atmos, and the integration of smart home control systems, which have greatly improved the user experience. At the same time, the industry is also facing challenges such as rising raw material costs and intensified market competition, prompting enterprises to continuously seek differentiated competitive strategies, such as providing customized services and strengthening the construction of after-sales service systems.

Looking back on the past few years, the home theater industry has maintained a steady growth trend with the upgrading of China's residents' consumption and the improvement of the living environment. In the future, with the further popularization of 5G and Internet of Things technologies, as well as the continuous improvement of consumers' pursuit of high-quality life, the home theater industry is expected to usher in broader development prospects.

The traditional home theater and audio industry focuses on the sale of home audio-visual equipment, including TVs, audio systems, projectors and other products, to meet consumers' demand for a high-quality home entertainment experience. In recent years, with the growing demand of consumers for intelligent and personalized entertainment, as well as the improvement of the family living environment, industry enterprises have begun to actively explore the road of transformation and increase the proportion of business integrated with the smart home ecosystem. This includes the integration of home theater equipment with smart home control systems to realize multi-scene linkage such as lighting, curtains, and temperature control, providing consumers with a more convenient and comfortable experience of watching movies and listening to music.

At the same time, in the process of industry transformation and upgrading, some enterprises have also begun to get involved in high-end customized services, providing one-stop solutions from design, installation to post-maintenance according to the specific living space and personalized preferences of customers, so as to enhance market competitiveness with differentiated services. In addition, with the continuous improvement of people's requirements for sound quality, professional-grade audio equipment and home theater renovation services are gradually favored by audiophiles and high-end users, becoming a new growth point in the industry.

Driven by consumption upgrading and technology iteration, the home theater and audio industry is developing in the direction of more intelligent, personalized and professional, which not only meets consumers' pursuit of high-quality lifestyle, but also injects new vitality into the sustainable development of the industry.

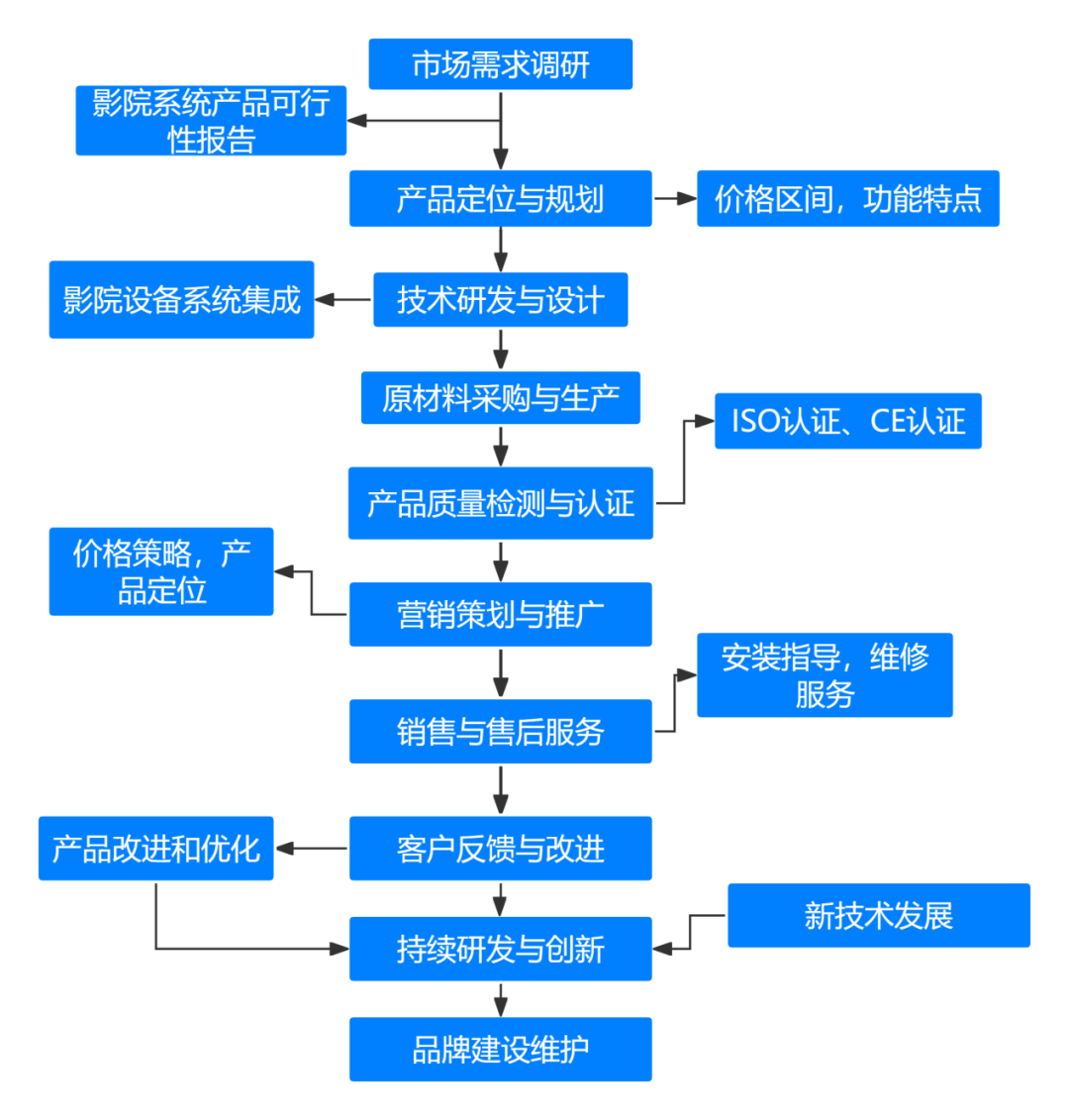

Figure: General construction of home theater and audio projects

Source: Asset Information Network Qianji Investment Bank

The home theater and audio industry is a highly technical consumer field, from system planning and design to installation and commissioning, and then to the final sound tuning and enjoyment, all aspects of the technical understanding, professional knowledge and practical experience of enthusiasts have high requirements. From selecting the right display equipment and audio components to rationally arranging the acoustic environment of the room, each step requires a deep understanding of audio and video technology, as well as an accurate grasp of the characteristics of different brands and models. In addition, for users who are looking for the ultimate movie-watching experience, mastering basic audio tuning skills, understanding the advantages and disadvantages of different audio formats, and how to improve the overall sound through software optimization are all indispensable skills to enhance the home theater experience. Therefore, in this industry, whether it is a professional or an ordinary enthusiast, continuous learning and practice accumulation is the key to enjoying a high-quality home theater and audio experience.

Chapter II: Industrial Chains, Business Models, and Policy Regulation

2.1 Industrial chain

The home theater and audio industry can be subdivided into the following key segments, which together make up this rich and diverse market for the combination of consumer and technology:

Home theater equipment manufacturing and system integration: Focus on creating a one-stop home entertainment solution for users, including selecting suitable display equipment (such as projectors, large-screen TVs), audio systems (such as surround sound cabinets, subwoofers), playback equipment (such as Blu-ray players, streaming media boxes) and necessary central control systems and cable layouts to ensure the coordination and efficient operation of the overall system.

Sales and customization of high-end audio equipment: Focus on providing high-end, professional audio equipment and customized services, such as high-end Hi-Fi audio, professional monitor headphones, high-end audio cables, etc., to meet the needs of audiophiles for the ultimate pursuit of sound quality, and may also involve the upgrading and modification of audio equipment.

Smart home audio solutions: Focusing on the combination of audio technology and smart home systems, providing smart speakers, multi-room music systems, voice control audio solutions, etc., aiming to improve the home audio experience through intelligent means and realize the convenient management and personalized settings of the home entertainment system.

Audio & Home Theater Consulting Services: Provide professional consultation, design advice and technical support for home theater enthusiasts or users who are ready to build a system, including room acoustic optimization, equipment selection guidance, system debugging and optimization, etc., to help users make the best decisions according to their own needs and budget.

Audio Education & Training: This field focuses on cultivating new talents in the home theater and audio industry, through online or offline courses, workshops, master classes and other forms, to teach audio fundamentals, sound system design principles, advanced tuning skills, etc., to provide the industry with professional skills of practitioners or improve the professional level of enthusiasts.

Source: Asset Information Network Qianji Investment Bank

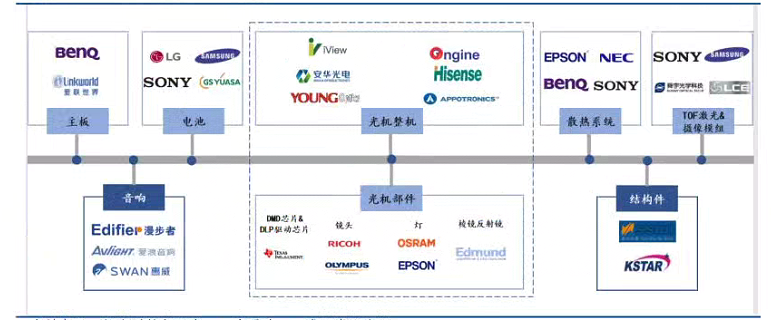

Home theater and audio industry chain composition:

Source: Asset Information Network Qianji Investment Bank

The home theater and audio industry is a comprehensive industry integrating audio equipment, video equipment, smart home, entertainment content and professional installation services. Consumption in the home theater and audio industry not only directly promotes the production and sales of related products, but also indirectly promotes the development of content creation, home design, e-commerce and other fields. The industry has a forward leading effect and a backward supporting effect on the upstream and downstream industries, and the two work together to form a comprehensive driving effect on various related industries.

According to industry research reports, the consumption of home theater and audio industry has a significant multiplier effect on related industries. On the one hand, with consumers' pursuit of high-quality home entertainment experience, the demand for hardware products such as high-end audio equipment, large-screen TVs, and projectors continues to increase, which directly drives the manufacturing and sales of these products, thereby promoting the development of upstream raw material suppliers, electronic component manufacturers and other related industries. On the other hand, the boom in the home theater and audio industry has also promoted the prosperity of the content creation industry, including the production and distribution of entertainment content such as movies, music, and games, bringing more business opportunities to downstream content providers and streaming service platforms.

In addition, the home theater and audio industry is also closely related to smart home, e-commerce, and other fields. With the continuous development of smart home technology, home theater and sound systems have increasingly become an important part of smart homes, driving the rapid growth of the smart home market. At the same time, the rise of e-commerce platforms has also provided a more convenient and efficient channel for the sale of home theater and audio products, further promoting the development of the industry.

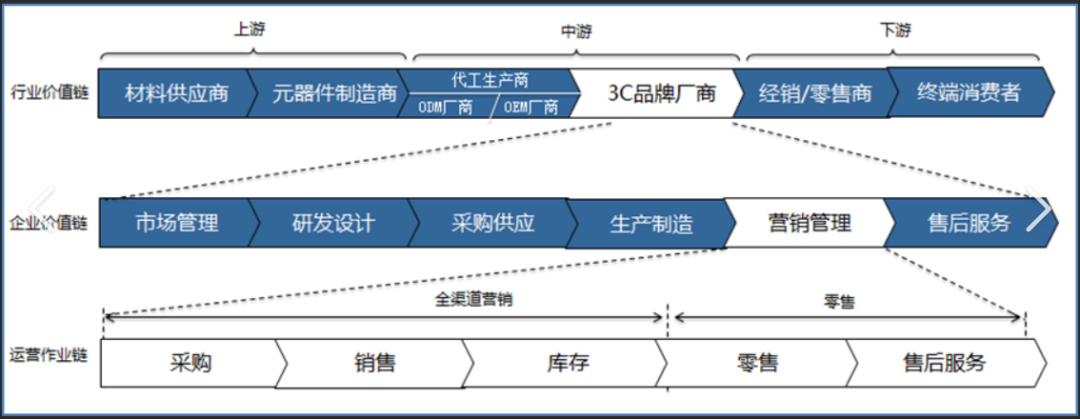

Figure Upstream and downstream industrial chains

Source: Asset Information Network Qianji Investment Bank

Home theater and audio industry: the foundation of entertainment life, the value chain is extensive. As an important part of modern entertainment life, the home theater and audio industry not only provides consumers with high-quality audio-visual enjoyment, but also drives the development of multiple upstream and downstream industries. Here's an overview of the industry's value chain and supply chain structure:

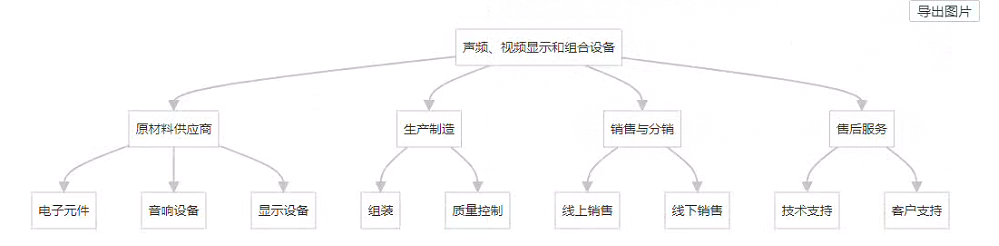

The home theater and audio industry is the core pillar of entertainment life, and it drives a wide range of upstream and downstream industrial chains, covering multiple links from R&D and design, raw material supply, manufacturing, marketing, after-sales service, etc., as well as a number of sub-industries closely related to it. Together, these links constitute the complete value chain and supply chain system of the home theater and audio industry.

Upstream industry chain

1. R&D and design: The design and development of home theater and audio products involves multiple disciplines such as acoustics, electronics, materials, etc., which require a professional R&D team and advanced technical support.

2. Raw material supply: including the supply of key components and raw materials such as speakers, chips, circuit boards, plastics, metals, etc., the quality of these materials directly determines the performance and quality of the product.

Midstream industry chain

3. Manufacturing: Processing and assembling raw materials and parts into final products requires advanced production equipment and technological processes, as well as a strict quality control system.

4. Logistics and distribution: Transporting products from the place of production to the place of sale, including domestic and foreign markets, requires an efficient logistics network and distribution services.

Downstream industry chain

1. Marketing: including brand positioning, advertising, promotional activities, sales channel expansion, etc., aiming to improve the visibility and reputation of products and attract consumers to buy.

2. After-sales service: including product installation, commissioning, repair, maintenance, etc., aiming to improve user experience and satisfaction, and enhance brand loyalty.

The development of the home theater and audio industry not only directly promotes the growth and employment of related enterprises, but also drives the development of electronics, materials, logistics, retail and other industries through the influence of the upstream and downstream industrial chains. At the same time, the development of the industry also reflects the trend of consumers' pursuit of high-quality life and the diversification of entertainment methods.

At present, the market size of the home theater and audio industry is huge, and with the increasing trend of consumers' pursuit of high-quality life and the diversification of entertainment methods, the industry has great potential for future development. It is expected that the industry will continue to maintain a steady growth trend in the coming period to provide consumers with richer and high-quality audio-visual enjoyment.

2.2 Business Model

Figure Value Delivery Chain in the Home Theater and Audio Industry

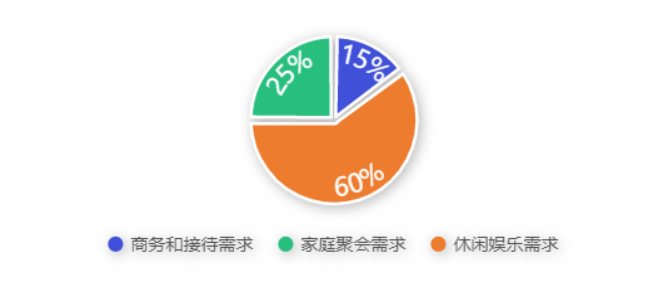

Figure Home theater and audio demand sources

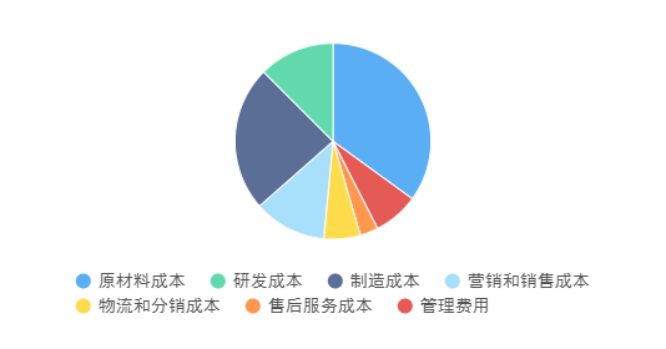

Figure Home theater and audio industry cost composition

Source: Asset Information Network Qianji Investment Bank

The cost of raw materials occupies an important position in audio production and has a great impact on the cost. High-end audio and cinema systems tend to use higher-quality materials, such as high-grade wood, precision metal components, and high-performance electronic components, which cost significantly more than those used in lower-end products. The cost of raw materials as a percentage of the total cost varies depending on the product grade and brand.

China's home theater and audio industry is experiencing a gradual change from a growth period to a mature period, and there is still good development potential

Source: Asset Information Network Qianji Investment Bank

The business models of the home theater and audio industry are diverse, and at this stage they mainly include the following:

1. Brand operation model: Under this model, the company is mainly engaged in consumer demand analysis, brand operation and marketing, sales channel construction, etc., and does not carry out product manufacturing activities. Enterprises solve the problem of supply by purchasing finished products with their own trademarks from processing plants. It is necessary to make independent judgments on market trends, have strong research and development capabilities and rich design experience.

2. Original manufacturer (OEM) model: that is, OEM production, the enterprise purchases raw materials and manufactures products according to the product solutions and technical requirements provided by customers. Do not participate in product design, research and development, sales and service. In the context of increasingly intelligent audio equipment and accelerating the speed of equipment update and iteration, the profit margins of OEM enterprises may be compressed, and the comprehensive competitiveness may gradually weaken.

3. Original Brand Manufacturer (OBM) model: Enterprises carry out independent production according to the functional and performance requirements put forward by customers, and their business usually covers all aspects of the industrial chain such as product design, production, marketing, retail, and distribution.

Compared with the OEM model, enterprises that adopt the OBM model can obtain the added value of all links in the industrial chain, but need to invest a lot of marketing expenses to build sales channels and marketing networks. In addition, with the rapid development of technologies such as the Internet of Things, 5G, and artificial intelligence, the home theater and audio industry is also constantly exploring new business models and innovation points. For example, through intelligent technology, remote control and intelligent recommendation of audio equipment can be realized, and richer content resources can be provided through streaming media services.

In the future, with the continuous progress of technology and the continuous change of consumer demand, the home theater and audio industry will usher in a broader development prospect.

According to the development trend and historical experience of the home theater and audio industry, the industry has also shown a trend of transition from a fast-growing incremental market to a stable stock market. For home theater and audio companies that are determined to develop in the long term, it is an inevitable choice to further develop and maintain their existing customer base, strengthen after-sales service and product upgrades, and build continuous brand loyalty.

The evolution of the home entertainment market in developed countries has taught us that with the increasing diversification and personalization of consumer needs, the home theater and audio industry no longer only relies on the launch of new products and the rapid expansion of market share, but pays more attention to product quality, user experience and follow-up service improvement. This means that companies need to shift from simply selling products to providing a full range of home entertainment solutions, including customized installation services, intelligent upgrade support, and long-term after-sales service guarantees.

In the process, the holding business model – that is, not just focusing on a single transaction, but realizing long-term revenue by building stable customer relationships, providing continuous product updates and service upgrades – has become a critical path to sustainability in the home theater and audio industry. Enterprises need to invest in brand building, improve product technology and aesthetic design, and use modern information technology means such as big data and cloud computing to optimize user experience and enhance user stickiness, so as to stand out in the highly competitive market.

2.3 Trading Markets and Instruments

The home theater and audio industry market is divided into individual consumer market, professional audio market, enterprise application market, and investor market. Tradable financial investment vehicles include home theater and audio enterprise stocks, home theater and audio industry ETF funds, related bonds, private equity and venture capital, derivatives and structured products, etc., although the home theater and audio industry itself may not directly generate derivatives (such as MBS, CDS, CDO, etc.), but investors can invest indirectly through derivatives linked to indices or stocks related to the relevant industry. These derivatives can provide additional leverage or the opportunity to hedge risk.

2.4 Product and Technology Development

The home theater and audio industry has shown vigorous vitality in technological innovation and business model innovation. At present, although the number of listed companies in the A-share market focusing on the field of home theater and audio is limited, there are many companies with patent licenses, which are leading the development of the industry through technological innovation. In the industry, the emergence of energy-saving audio technology, new audio processing algorithms, intelligent home entertainment systems, audio Internet of Things (Audio IoT), new audio materials, 3D audio printing and other technologies has a profound impact on the future direction of the home theater and audio industry.

High-speed communication technology, big data analytics, and Internet of Things technologies are driving the innovation of smart home theaters and smart audio systems. The Internet of Things (IoT) technology enables audio devices in the home to be intelligently interconnected, enabling remote control, personalized audio scene settings, and seamless connection with other smart home devices, bringing users an unprecedented immersive entertainment experience. At the same time, the application of new materials not only improves the sound quality performance of audio products, but also brings lighter design, stronger durability and lower manufacturing costs. 3D printing technology is also beginning to make its mark in home theater and audio, allowing designers and manufacturers to create audio enclosures and internals with unprecedented precision and complexity, opening up new avenues for personalization and the development of high-performance audio products. In addition, prefabricated audio technology simplifies the installation process, making it easier for users to set up and optimize the sound system in their homes.

The home theater and audio industry has also undergone significant changes in terms of business models and operating models. The product supply is no longer limited to traditional audio equipment, but has expanded to include smart home theater systems, wireless audio solutions, audio subscription services and other categories. At the same time, "one-stop home entertainment solutions" have become a new trend in the industry, requiring enterprises to not only provide high-quality products, but also integrate content resources, and provide installation and maintenance services to meet consumers' needs for convenient, efficient and personalized home entertainment experiences. In addition, emerging business models such as shared audio services and subscription-based audio experiences have also brought new growth points to the industry, further broadening the boundaries of the home theater and audio industry.

Data source: Qianji Investment Bank Asset Information Network official website

2.5 Policy and Regulation

The

main regulatory units of the home theater and audio industry are the Ministry of Industry and Information Technology of the People's Republic of China and the State Administration for Market Regulation, and are also subject to the multi-dimensional supervision of the National Development and Reform Commission, the State Administration of Radio and Television, the Ministry of Culture and Tourism, the State Administration of Taxation, the General Administration of Customs, the Ministry of Ecology and Environment and other departments. The state implements a macro guidance strategy that combines policy guidance and market supervision for the home theater and audio industry. At the local level, the local Department of Industry and Information Technology, the Administration for Market Regulation, the Bureau of Culture, Radio, Television and Tourism, and the Bureau of Ecology and Environment are jointly responsible for the management.

In terms of self-regulatory organizations, including the China Electronic Audio Industry Association and the Technical Committee for Standardization of Audio and Audio-Visual Equipment, they play an important role in promoting the formulation of industry standards, technical exchanges and market self-discipline.

The main regulatory laws and regulations of the industry cover the "People's Republic of China Product Quality Law", "People's Republic of China Consumer Rights Protection Law", "People's Republic of China Standardization Law", "People's Republic of China Environmental Protection Law", "People's Republic of China Certification and Accreditation Regulations", "Administrative Measures for Electronic Product Maintenance Services", "Administrative Measures for Imported Audio Products" and "Regulations on the Safe Use of Household Appliances", etc., which provide legal guarantee for the healthy development of the industry.

In view of the uneven product quality and false propaganda in the home theater and audio market, the relevant government departments have continuously strengthened supervision, implemented product quality certification systems, cracked down on unfair competition, and encouraged technological innovation and green development. At the same time, with consumers' pursuit of high-quality life, the government and industry associations are also guiding enterprises to pay attention to user experience and promote the development of intelligent and personalized products to meet market demand.

Chapter 3 Financial, Risk and Competition Analysis

3.1 Financial Analysis and Valuation Methods

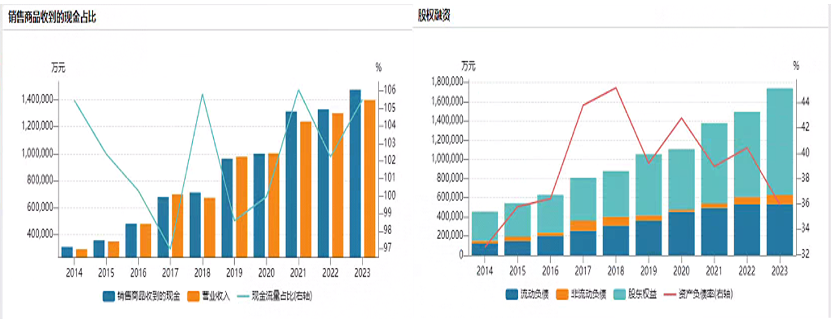

Chart: Comprehensive financial analysis of the industry

Figure: Industry history comparison

Source: Qianji Investment Bank Asset Information Network

The valuation methods of the home theater and audio industry can choose from the price-earnings ratio valuation method, PEG valuation method, price-to-book ratio valuation method, price-to-present ratio, P/S price-to-sales ratio valuation method, EV enterprise value method, EV/Sales price-to-sales ratio valuation method, RNAV revaluation net asset valuation method, EV/EBITDA valuation method, DDM valuation method, DCF discounted cash flow valuation method, dividend discount model, equity free cash flow discount model, unleveraged free cash flow discount model, net asset value method, Discounted Economic Value Added Model, Adjusted Present Value Method, NAV Net Asset Value Valuation Method, Book Value Method, Liquidation Value Method, Cost Replacement Method, Real Options, LTV/CAC (Customer Lifetime Value/Customer Acquisition Cost), P/GMV, P/C (customer), Metcalfe Valuation Model, PEV, etc.

3.2 Drivers

The

home theater industry looks at the content ecology in the long term, technological innovation and hardware upgrades in the medium term, and consumption power and market policies in the short term. Content is the core of demand, technological innovation and hardware upgrading determine the quality of supply, and consumption capacity and market policies are the levers for short-term fluctuations. Regions with rich content, rapid updates and high quality often stimulate the rapid growth of the home theater market if it coincides with the improvement of consumption power and favorable market policies, and may encounter development bottlenecks otherwise. Keeping up with the trend of content innovation and consumption upgrading, the market will tend to segment and differentiate competition from a global perspective with the diversification and quality of home entertainment demand. At present, with the advancement of technology and the improvement of living standards, home theater equipment has been more popular in most developed cities, but there is still great potential in intelligent and personalized services in the future. It is expected that in the future, most traditional home theater products or services will face the risk of homogeneous competition and surplus, while only about 20%-30% of high-quality, intelligent, and customized brands or platforms can continue to attract users and achieve steady growth. In short, content is king, technological innovation is the wing, and consumption power and policy orientation are the wind, and this analytical framework has guiding significance for the insights of the home theater industry. Based on this framework, we can predict market trends in advance, such as accurately assessing the long-term impact of a technological innovation or policy on the home theater market, and similarly, in-depth analysis and prediction of the home theater market will become a classic case of industry insight.

The factor drivers for the home theater and audio industry mainly include the following:

1. Technological innovation is a key force to promote the sustainable development of the home theater and audio industry. Technological innovations in high-quality sound, low power consumption, ease of use, intelligent control and Internet applications have continuously improved the performance and user experience of products. For example, the popularity of 4K and 8K ultra-high-definition technology, HDR (high dynamic range), Dolby Atmos and other technologies has greatly improved the viewing experience of home theaters. At the same time, with the continuous development of smart home technology, the home theater system is gradually realizing intelligent control to provide consumers with more convenient and personalized services. In terms of hardware upgrades, from traditional speakers to smart speakers, to portable projectors and other devices, it continues to meet the diverse needs of users.

2. Content is one of the core needs of the home theater and audio industry. With the vigorous development of the online audiovisual industry, consumers' demand for high-quality and diversified content is growing. The prosperity of the audio-visual entertainment industry, such as online video, audio, smart TV (OTT), interactive network television (IPTV), etc., has provided rich content resources for the home theater and audio industry. At the same time, consumers' demand for personalized content is also increasing, which requires the industry to provide more customized services to meet the viewing needs of different consumers.

3. Consumption power is an important factor affecting the development of the home theater and audio industry. With the improvement of residents' living standards, consumers' demand for home entertainment products is also escalating, from the initial pursuit of affordable prices to the current focus on quality, experience and service. In addition, market policies also have an important impact on the development of the industry. The government's support for the cultural industry and scientific and technological innovation has been increasing, providing a good policy environment for the development of the home theater and audio industry. For example, the support policies for the cultural and creative industries and the encouragement policies for scientific and technological innovation will help promote the rapid development of the industry.

4. Brand competition is one of the important characteristics of the home theater and audio industry. Well-known brands at home and abroad, such as XGIMI, nuts, dangbei, Sony, Samsung, etc., have launched fierce competition in the home theater market. These brands have won wide recognition from consumers with their high-quality products, advanced technology and perfect after-sales service. At the same time, in order to enhance brand influence, these brands also carry out brand publicity and promotion by sponsoring sports events, holding concerts, etc. In terms of channel construction, online and offline integration has become a new trend of channel competition in the home theater and audio industry. Online channels such as e-commerce platforms and social media have become important channels for consumers to purchase products. Offline channels focus on experience and service, and provide consumers with a more intuitive and convenient shopping experience by setting up specialty stores and experience stores.

3.3 Risk Analysis and Management

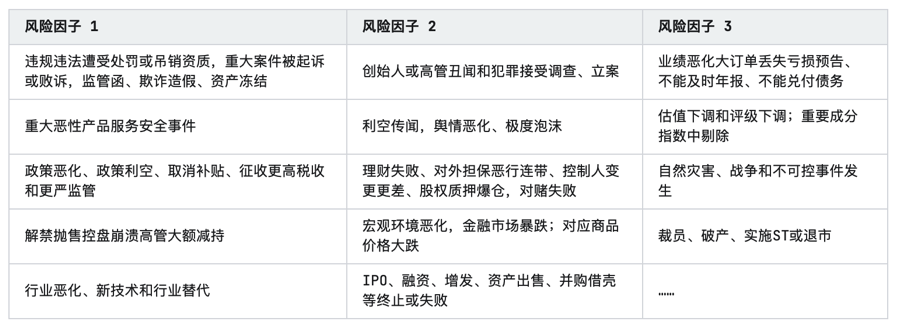

Table Common industry risk factors

Source: Asset Information Network Qianji Investment Bank

Common risks for upstream raw material suppliers

(1) Market supply and demand risks

The fluctuation of market supply and demand in the home theater industry has a direct impact on upstream raw material supply enterprises. With the change of consumer demand, the iteration of technology and the adjustment of the industry competition pattern, the market demand for raw materials may be unstable. In addition, factors such as the global economic situation, changes in trade policies, and fluctuations in raw material prices may also affect the stability and cost of raw material supply. In order to better adapt to market changes, enterprises need to pay close attention to market dynamics, strengthen supply chain management, and establish a diversified supplier system to ensure the stable supply of raw materials and cost control.

(2) Raw material quality risk

Home theater products have high requirements for the quality of raw materials, such as audio materials, screen materials, electronic components, etc., and their quality directly affects the performance and user experience of the final product. Raw material suppliers need to ensure that the materials they supply meet industry standards and customer needs to avoid customer loss and reputational damage due to quality problems. To this end, enterprises should establish a sound raw material inspection system, strictly control the quality level, and establish long-term and stable cooperative relations with suppliers to jointly improve the quality of raw materials.

(3) Technological innovation risks

The technology of the home theater industry is rapidly updated, and new materials and new processes are constantly emerging, which puts forward higher technological innovation requirements for upstream raw material supply enterprises. If companies fail to keep up with technology development trends and launch new materials that meet market demand, they may lose market share and competitive advantage. Therefore, enterprises need to increase R&D investment, strengthen technological innovation and intellectual property protection, and improve the technical content and added value of products.

(4) Supply chain risks

The stability and efficiency of the supply chain is critical for upstream raw material suppliers. Factors such as supply chain disruptions, supplier bankruptcies, and transportation delays can lead to insufficient supply of raw materials or rising costs, affecting the normal production and operation of enterprises. In order to reduce supply chain risks, enterprises need to establish a sound supply chain management system, strengthen strategic cooperation with suppliers, optimize procurement processes, and improve supply chain resilience and risk resistance.

(5) Compliance risks

Upstream raw material suppliers need to comply with relevant laws, regulations and policy requirements in the production process, such as environmental protection regulations, safety production regulations, etc. If a company violates laws and regulations, it may face serious consequences such as fines, suspension of production and rectification, and even affect its reputation and market share. Therefore, enterprises need to strengthen compliance management, establish and improve compliance systems, and ensure that production activities are legal and compliant.

(6) Environmental protection risks

With the improvement of environmental awareness and increasingly stringent environmental protection regulations, upstream raw material suppliers need to assume greater environmental responsibility. If the enterprise produces pollution or does not meet the emission standards in the production process, it may face penalties and public pressure from the environmental protection department. To this end, enterprises need to strengthen environmental protection investment, adopt environmental protection technology and equipment, reduce pollution emissions in the production process, and achieve green production.

(7) Financial risks

Upstream raw material supply enterprises may face financial risks in the course of operation, such as shortage of funds, bad debts of accounts receivable, exchange rate risks, etc. These risks may affect the normal operation and profitability of the business. Therefore, enterprises need to strengthen financial management, optimize the capital structure, improve the efficiency of capital use, and establish a risk early warning mechanism to detect and respond to potential financial risks in a timely manner.

Equipment manufacturer risk

1. Market risk

According to industry reports, the home theater market has shown rapid growth in recent years, and consumers' demand for high-quality home entertainment experiences is increasing. However, with the rapid expansion of the market, midstream equipment manufacturers in the home theater industry are facing fierce market competition. Many domestic and foreign brands have poured into the market, which not only exacerbates the phenomenon of product homogenization, but also leads to the continuous escalation of price wars. In addition, the diversification of consumer needs also requires manufacturers to continuously innovate to meet the individual needs of different consumers. If manufacturers are unable to adapt to market changes in a timely manner, they risk losing market share and weakening profitability.

2. Operational risks

(1) The risk of fluctuation in the cost of raw materials

Home theater equipment manufacturers need a large number of raw materials in the production process, such as electronic components, display screens, audio components, etc. The prices of these raw materials are affected by various factors such as the global economic situation, trade policies, supply and demand, and the prices fluctuate greatly. If raw material costs continue to rise, and manufacturers are unable to offset the increase by raising selling prices or optimizing production processes, it will have a direct impact on their profitability and market competitiveness.

(2) Technology update and iteration risks

The home theater industry is rapidly evolving with new products and features. Manufacturers who fail to keep up with technology updates and launch new products that meet market demand will lose their competitive advantage. At the same time, technology updates and iterations also mean rapid depreciation of old products, and if manufacturers have serious inventory backlogs, they will face asset impairment and capital occupation pressure.

(3) Supply chain risks

The supply chain of home theater equipment manufacturers involves multiple links, including raw material procurement, production and processing, logistics and distribution, etc. If there is a problem in one part of the supply chain, such as supplier bankruptcy, logistics delays, etc., it will directly affect the manufacturer's production schedule and delivery time. In addition, quality issues in the supply chain can also lead to product recalls and increased after-sales costs.

(4) Customer concentration risk

Home theater equipment manufacturers' customers typically include large retailers, e-commerce platforms, and system integrators. If a manufacturer relies too much on a single customer or sales channel, there is a risk of high customer concentration. Once there is a problem with that customer or sales channel, such as the breakdown of the partnership, the adjustment of the sales policy, etc., it will have a significant impact on the manufacturer's sales and profitability.

(5) Product quality and safety risks

As an electronic product, the quality and safety of home theater equipment are of paramount importance. If the manufacturer fails to strictly control the quality during the production process, or if the product has design defects, it will lead to product quality and safety risks. This not only affects the consumer experience, but can also lead to legal disputes and brand reputation damage.

(6) Risks of intellectual property protection

Home theater equipment manufacturers need to invest a lot of manpower, material and financial resources when developing new products and technologies. If the manufacturer is not aware of the protection of intellectual property rights, or fails to apply for patents and registered trademarks in a timely manner, it will face the risk of intellectual property infringement. This not only leads to economic losses, but can also affect the manufacturer's ability to innovate and market competitiveness.

(7) Environmental protection and compliance risks

As global environmental awareness increases, home theater equipment manufacturers need to comply with increasingly stringent environmental regulations and emission standards during their production processes. If manufacturers fail to meet environmental protection requirements, they will face serious consequences such as fines and suspension of production for rectification. In addition, manufacturers also need to comply with the laws and regulations of the relevant countries and regions, such as product safety standards, consumer protection laws, etc. If manufacturers fail to operate in compliance, they will face legal risks and loss of brand reputation.

3. Manage risk

(1) Expansionary risks

In the process of continuously expanding the production scale and enriching the product line, the number of home theater equipment, market share and operating income produced by midstream equipment manufacturers in the home theater industry have shown a significant growth trend. With the expansion of the company's scale, higher requirements have been put forward for production management, supply chain management, technology research and development, marketing and internal control. However, if the company's management system, production process, quality control and internal supervision mechanism cannot be optimized and upgraded in a timely manner with the expansion of business scale, it may lead to problems such as decreased production efficiency, product quality fluctuations, and poor cost control, which will have an adverse impact on the company's operating performance.

(2) Multi-production base management risk

In order to respond to market demand and reduce costs, home theater equipment manufacturers often have multiple production sites in different regions. With the implementation of the company's strategic plan, it is possible to continue to expand the layout of the production base in the future. However, the management of multiple production sites faces challenges such as geographical dispersion, cultural differences, and poor information transmission, which can lead to reduced management efficiency, higher operating costs, and increased quality control difficulties. In order to effectively deal with these risks, the company needs to establish a unified management system, standardized production processes and efficient communication and coordination mechanisms. If the company's management system and system cannot adapt to the needs of multiple production sites, it may adversely affect the company's production efficiency and profitability.

(3) The risk of loss of key technical talents

The home theater equipment manufacturing industry is a technology-intensive industry, and key technical talents are crucial to the company's R&D innovation, product upgrading and market competitiveness. With the expansion of the company's scale and the intensification of market competition, the demand for key technical talents will also increase. However, if a company fails to provide competitive compensation and benefits, a good working environment, and career development opportunities, it may lead to the loss of key technical talent. This will directly affect the company's R&D capabilities and innovation capabilities, which in turn will adversely affect the company's product competitiveness and market position.

(4) Compliance risks

In the home theater equipment manufacturing industry, companies need to comply with a series of laws, regulations and industry standards, including product quality standards, environmental protection requirements, intellectual property protection, etc. If the company does not strictly comply with relevant laws, regulations or industry standards in the production process, it may face the risk of being punished by the competent authorities, product recall, and damage to brand reputation. In particular, with regard to the protection of employees' rights and interests, if the company fails to pay social insurance or housing provident fund for all employees, there is a risk of being required to make supplementary contributions, which will not only increase the company's operating costs, but also may have a negative impact on the company's brand image and employee morale. Therefore, the company needs to establish a sound compliance management system to ensure the legal and compliant operation of each business.

Common risks for sales companies

1. Policy and standard risks

As an important part of the consumer electronics market, the home theater industry is susceptible to the impact of national policy adjustments, changes in industry standards and consumer protection regulations. In particular, policy changes regarding product quality, after-sales service, data security, and environmental protection requirements may have a direct impact on the operating costs, product compliance, and market competitiveness of sales companies.

2. Market risk

The downstream sales enterprises in the home theater industry are directly oriented to end consumers, and the fluctuation of market demand has a significant impact on their performance. With the diversification of consumer entertainment methods, the market demand for home theater products has shown cyclical changes, and is affected by multiple factors such as the macroeconomic environment, consumer purchasing power, the speed of technological upgrading, and the impact of new forms of entertainment. During the market adjustment period, problems such as declining sales, intensifying price wars and inventory backlogs are particularly prominent, posing challenges to the profitability of sales companies.

In response to market risks, sales enterprises can adopt the following strategies to deal with them: (1) strengthen market research, accurately locate target customer groups, and launch product portfolios that meet market demand; (2) Expand sales channels, integrate online and offline, and use new media tools such as e-commerce platforms and social media to improve brand exposure and sales conversion rate; (3) Implement differentiated competition strategies, strengthen after-sales service systems, and enhance customer loyalty.

3. Operational risks

1. Supply chain stability risk: Home theater products involve many component suppliers, and the supply chain is complex and susceptible to global supply chain fluctuations. Issues such as rising raw material costs, supply chain disruptions or delayed deliveries will directly affect the cost control and delivery ability of sales enterprises.

2. The risk of intensified market competition: With the relatively low entry threshold of the industry, there are many brands in the market and the price war is fierce. Sales companies need to constantly innovate marketing strategies and enhance brand influence to stand out from the competition.

3. Inventory management risk: Home theater products are updated quickly, and inventory management has become a major challenge. Excessive inventory can tie up funds, while stockouts can impact sales opportunities. Sales companies need to establish an efficient inventory management system to quickly respond to market demand.

4. Risk of changes in consumer preferences: Consumers' preferences for home theater products are becoming increasingly diversified, pursuing personalized and intelligent experiences. Sales companies need to keep up with the trend of technology and quickly adjust the product structure to meet the needs of consumers.

4. Manage risk

1. Brain drain risk: Sales companies in the home theater industry rely on high-quality sales, customer service and technical support teams. Brain drain not only affects day-to-day operations, but can also take away customer resources and damage the competitiveness of enterprises. Enterprises should strengthen talent training and incentive mechanisms to build a stable talent team.

2. Service quality risk: After-sales service is the key to improving customer satisfaction and loyalty. Sales enterprises need to establish a sound after-sales service system to ensure rapid response to consumer needs, handle complaints and return issues, and maintain brand image.

3. Digital transformation risks: With the acceleration of digital transformation, sales enterprises need to invest a lot of resources in building e-commerce platforms and data analysis systems to improve operational efficiency and market competitiveness. However, in the process of digital transformation, there may be problems such as improper technology selection, data security risks, and uncertainty of return on investment.

3.4 Competitive Analysis

Figure SWTO analysis of industry development

Source: Asset Information Network Qianji Investment Bank

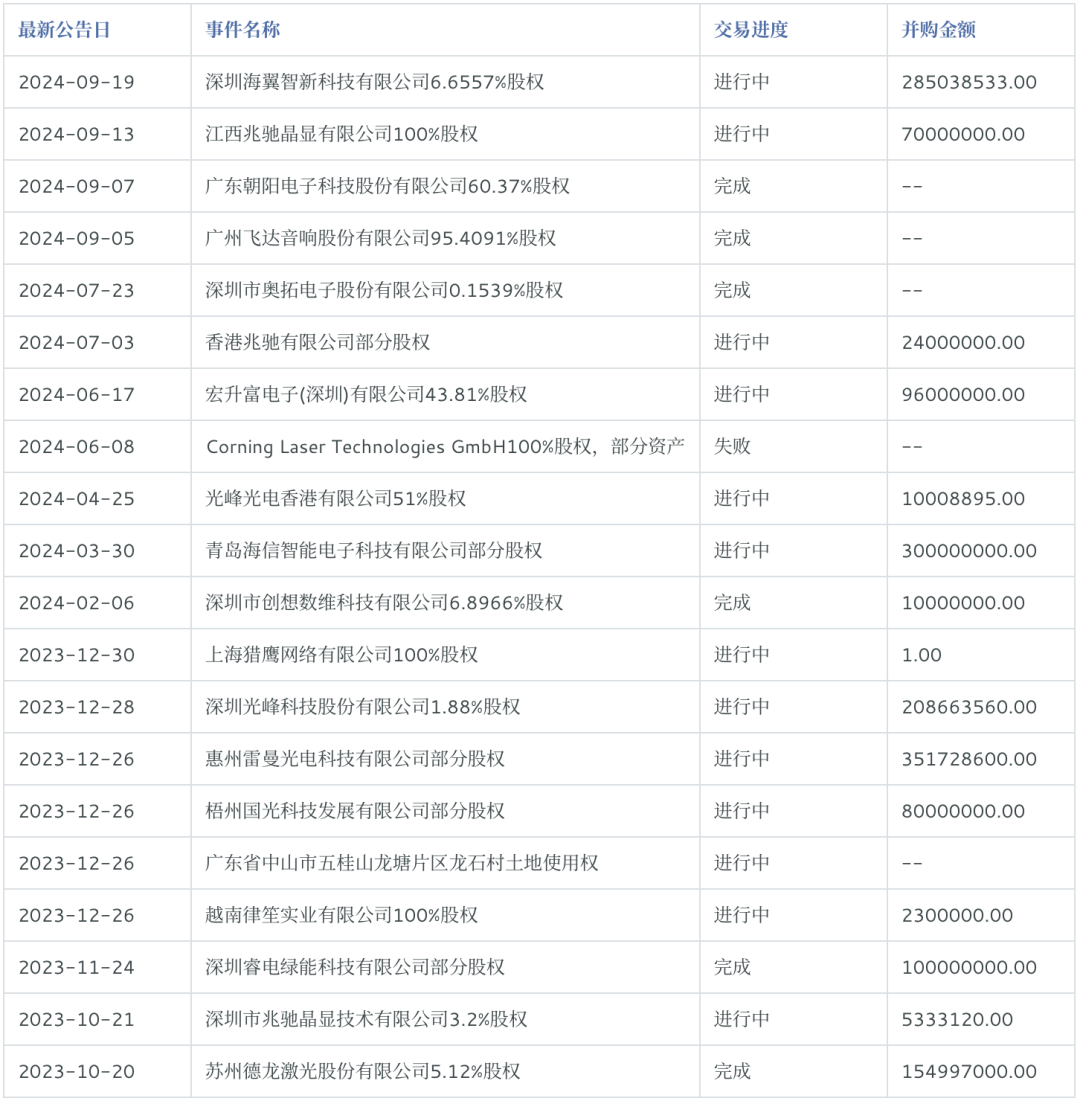

As of October 11, 2024, there have been more than 100 million mergers and acquisitions in the industry, with more than 100 cases.

Table Mergers and acquisitions in the home theater and audio industry

Source: Asset Information Network Qianji Investment Bank

3.5 Important Participating Enterprises in China

China's major listed companies include Guoguang Electric Co., Ltd. (002045. SZ), Guangzhou Huiwei Electroacoustic Technology Co., Ltd. (002888.SZ), Xiamen Yealink Network Technology Co., Ltd. (300628.SZ), Shenzhen Guangfeng Technology Co., Ltd. (688007.SH), China Optics Group Co., Ltd. (002189.SZ), Xi'an Nova Nebula Technology Co., Ltd. (301589.SZ), Colorlight Cloud Technology Co., Ltd. (301391.SZ), Guangdong Sanxiong Aurora Lighting Co., Ltd. (300625.SZ), Shenzhen Besdaq Technology Co., Ltd. (300822.SZ). Chengdu Information Technology Co., Ltd., Chinese Academy of Sciences (300678. SZ), Shenzhen Iklet Technology Co., Ltd. (300889.SZ), Jiangsu Litong Electronics Co., Ltd. (603629.SH), Beijing Golden Years Media Technology Co., Ltd. (834021.BJ), Tonghui Jiashi (Beijing) Information Technology Co., Ltd. (430090.BJ), Anker Innovation Technology Co., Ltd. (300866.SZ), XGIMI Technology Co., Ltd. (688696.SH), Lingyun Optical Technology Co., Ltd. (688400.SH), Lingda Group Co., Ltd. (300125.SZ). Hangzhou Hikvision Digital Technology Co., Ltd. (002415. SZ), Guangdong Optima Technology Co., Ltd. (688686.SH), Shenzhen Sino Sound Zhilian Co., Ltd. (002651.SZ), Shenzhen Zhaochi Multimedia Co., Ltd. (002429.SZ), Shenzhen Genvict Technology Co., Ltd. (002869.SZ), Shenzhen Edifier Technology Co., Ltd. (002351.SZ), Guangdong Guoguang Electric Co., Ltd. (002045.SZ), Shenzhen Aite Aviation Technology Co., Ltd. (300206.SZ), Shenzhen Rapoo Technology Co., Ltd. (002577.SZ). Shenzhen Fenda Technology Co., Ltd. (002681. SZ), Shenzhen Alto Electronics Co., Ltd. (002587.SZ), Shenzhen Yingqu Technology Co., Ltd. (002925.SZ), Shenzhen Meige Intelligent Technology Co., Ltd. (002881.SZ), Shenzhen Kelu Electronic Technology Co., Ltd. (002121.SZ), Shenzhen Hehong Industrial Co., Ltd. (002521.SZ), Shenzhen Konka Group Co., Ltd. (000016.SZ), Shenzhen Zhaochi Co., Ltd. (002429.SZ), etc.

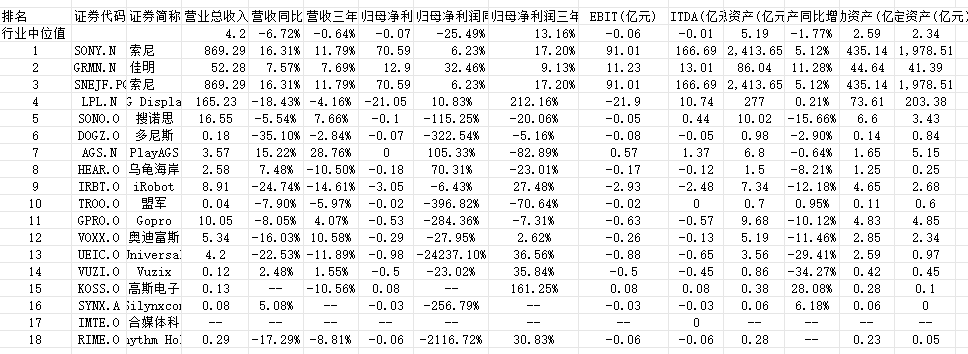

The China Home Theater Industry Association and the Beijing Smart Home Research Institute jointly selected and released the "2023 Top 100 List of Comprehensive Strength in the Home Theater Industry". The list shows that the average total assets of the companies on the list of the top 100 comprehensive strength of the home theater industry in 2023 is 2.547 billion yuan, an increase of 8.65% over the previous year; The average net assets were 1.276 billion yuan, an increase of 11.23% over the previous year. On the whole, the total assets of the TOP100 companies continued to expand, but the growth rate slowed down slightly, showing that the industry is seeking new growth points in the steady development.

From the perspective of revenue capacity, the average operating income of enterprises in the home theater industry will reach 895 million yuan in 2023, a year-on-year increase of 6.78%. This is mainly due to the increased consumer demand for high-quality home entertainment experiences, as well as the continuous introduction of innovative products and services by enterprises. The average operating cost was 723 million yuan, an increase of 7.94% over the previous year, showing the continuous investment in improving product quality and service level. However, the average net profit was only 124 million yuan, a year-on-year decrease of 1.32%, which may be related to factors such as intensified competition in the industry and rising raw material costs. The average balance of cash and cash equivalents reached 456 million yuan, down 0.98% year-on-year, indicating that enterprises still need to be cautious in maintaining liquidity.

From the perspective of regional distribution, East China accounts for the highest proportion of the TOP100 in the home theater industry, reaching 42%, showing the region's strong strength in the home theater market and strong consumer demand. South China is a close second, accounting for 25%, with a developed economy and consumers' pursuit of a high quality of life driving the rapid growth of the home theater market. The central region accounted for 18%, an increase year-on-year, reflecting the rise of the central region's economy and the increase in consumer demand for home entertainment. North China accounted for 10%, the western region accounted for 4%, and the northeast accounted for 1%, although there was a year-on-year decline, there is still a large market potential to be tapped.

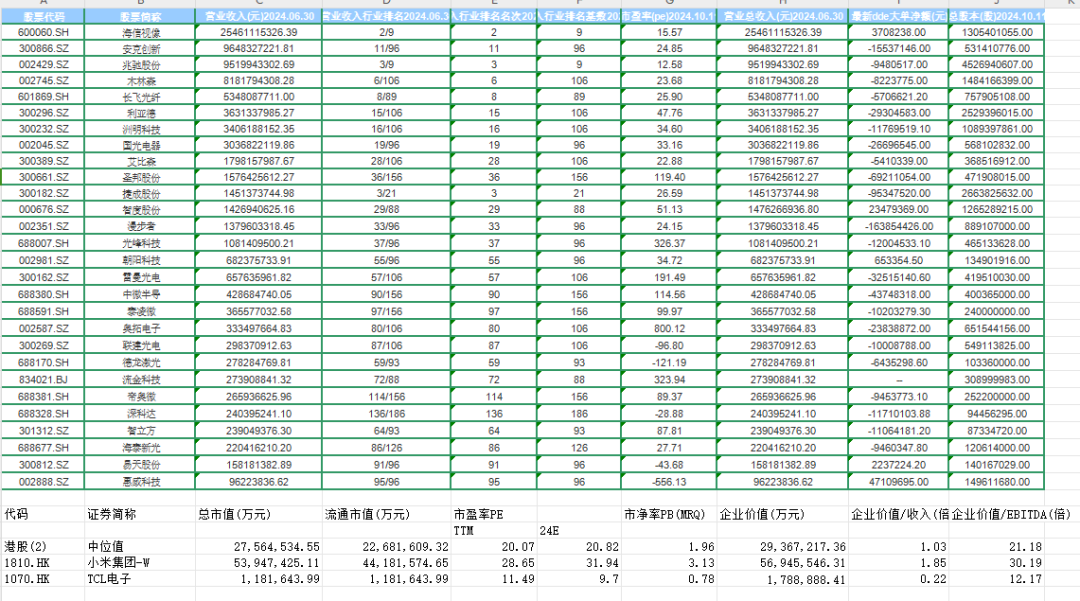

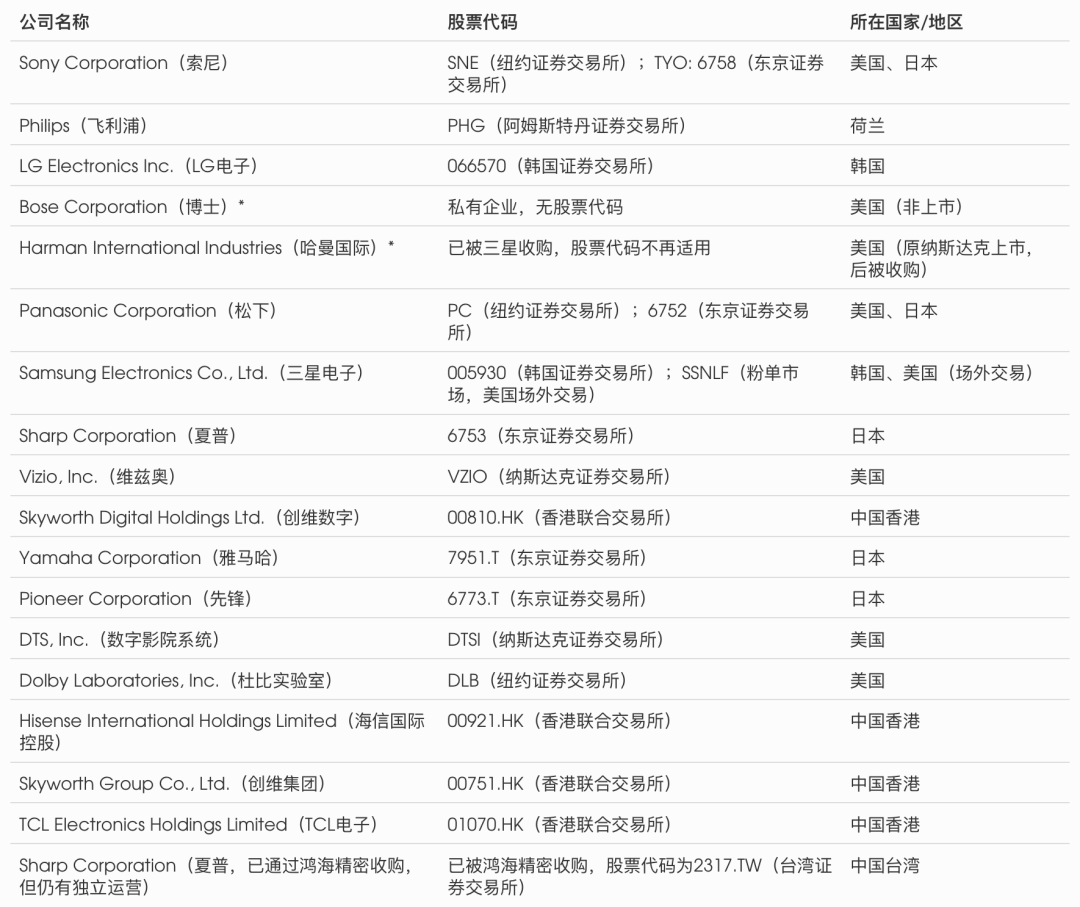

Table Listed home theater industry companies in Chinese mainland and Hong Kong

Source: Asset Information Network Qianji Investment Bank

1. Hisense Video Technology Co., Ltd. is a company mainly engaged in the research and development, production and sales of display products and display chips, as well as Internet operation services. The main products are smart display terminal business, laser display, commercial display, cloud service, and chip business. At the "China Digital TV Annual Ceremony" hosted by the China Electronic Video Industry Association,The company100L5Laser TV also won"High-end Intelligent Product Award",In the China Electronics Chamber of Commerce、China Electronics Standardization Institute"2019China Digital TV Industry Development Conference",Hisense won"2019Consumer favorite TV brand",Laser TV100L7Won the "2019Top Ten TV"Honor。

2. Shenzhen Edifier Technology Co., Ltd. is a company engaged in the research and development, production and sales of home audio, professional audio, car audio, headphones and microphones, and its main products include various multimedia audio, professional audio and car audio. The company actively expands overseas markets and goes to the world with the image of China's own brand. Today, the trademarks "Edifier" and "EDIFIER" have registered international trademarks in more than 80 countries and regions such as Germany, United Kingdom, France, Italy, United States, Canada, Japan, Australia, Russia and Mexico. A number of products of the company's "EDIFIER" brand have won the "Red Dot Design Awards", "iF Design Award" (iF Design Award), "CES Product Design and Innovation Award" (CES Design and Engineering Award), and the "EDIFIER" brand has become synonymous with high-quality multimedia audio and headphones. The sales volume in the domestic market has been far ahead for many years, and it has a high reputation and good reputation in the industry.

3. The main business of Shenzhen MTC Co., Ltd. includes smart display, smart home networking and the whole LED industry chain, and the company's main products cover LCD TVs, set-top boxes and other multimedia audio-visual terminals and smart display products, content operation platforms and software solutions, network communication equipment, LED chips, LED packaging, lighting and display products and other fields. In the field of applied lighting, the company has promoted the development of finished LED lighting equipment through the independent brand "Zhaochi Lighting" and the ODM business department. In terms of products, the company has launched more than 1,000 products, covering more than 10 categories in commercial lighting, engineering, home furnishing, circulation and other channels, and the product lineup has begun to take shape.

3.6 Global Significant Competitors

The world's major well-known brands are Sony, Samsung, Yamaha, Harman Kardon, JVC, Bowers & Wilkins, Dynaudio, Philips, Pioneer, Dr. Bose, Sennheiser, Shanshui, Tianlang TANNOY, ELAC, KEF, Marantz, etc.

Figure of the world's most important listed companies

Source: Asset Information Network Qianji Investment Bank

Table The world's major non-Chinese listed companies in the home film and audio industry

Source: Asset Information Network Qianji Investment Bank

1. Sony Group was incorporated in Japan on May 7, 1946. It is engaged in the development, design, manufacture, and sale of a wide range of electronic devices, instrumentation and consumer electronic devices, professional and industrial markets, and gaming consoles and software. Sony's main production plants are located in Asia, including Japan. Sony also uses third parties to outsource the production of certain products. Sony's products are sold primarily through sales subsidiaries and non-affiliated distributors, as well as through direct sales through the Internet. Sony is engaged in the development, production and acquisition, manufacturing, marketing, distribution and broadcasting of image-based software, including motion pictures, home entertainment and television products. Sony has been engaged in the development, production and acquisition, production and sale of music records. In addition, Sony is engaged in various financial services businesses, including the sale of life and non-life insurance through its Japan insurance subsidiaries and banking business, as well as its network of affiliated banking subsidiaries. In addition to the above, Sony is also engaged in the network service business and advertising agency business in Japan.

2. LG Electronics is a global leader and technology innovator in consumer electronics, mobile communications and home appliances, employing more than 84,000 people and 112 locations in 81 locations worldwide.

LG has been committed to enhancing the global awareness of the LG brand and maximizing profitable growth. LG Electronics is particularly focused on achieving sustainable profitable growth in mobile communication products and home entertainment products to consolidate its leading position in the IT industry, while LG will also increase its market share in home appliances, air conditioning and business solutions.

3. BOSE is the largest speaker manufacturer in the United States, headquartered in Massachusetts, United States, with hundreds of engineers engaged in research and development alone, and is a wholly-owned independent company. The products also have excellent performance in the field of car audio and aerospace technology. In addition to civilian products, Bose also has a wide range of development in the field of professional audio. Bose professional audio systems are successfully used in large stadiums, multi-purpose conference halls, churches, high-end hotels and brand flagship stores. On February 17, 2024, it was reported that the audio brand Bose launched its first open-back audio device, Bose Ultra open-back headphones

Chapter 4 Future Prospects

In the next decade, the development of the home theater industry will focus on key areas such as technological innovation, user experience, content ecology, smart home integration, and personalized customization. Many home theater brands and related companies, such as industry leaders Sony, Samsung, LG, Bose, Yamaha, etc., are actively exploring diversified development paths, aiming to broaden market boundaries and enhance competitiveness. This diversification strategy is also reflected in two aspects: one is the cross-border innovation that is completely independent of traditional home theater equipment, such as immersive home entertainment systems combined with VR/AR technology; The other is to deepen the integration with existing home theater systems, such as launching more intelligent home theater solutions, as well as customized products for specific scenarios (such as home fitness, remote work + entertainment), both of which have brought new vitality to the industry.

The supply structure of home theater products is constantly being optimized, shifting from single equipment sales to comprehensive solution provision, including the integrated packaging of hardware, software, content and services. The growing demand for high-quality audio-visual experiences has prompted the industry to explore a new development model of "device + content + service". At the same time, with the popularization of smart home technology, home theater systems are gradually integrated into the whole house intelligent ecology to achieve a more convenient and intelligent control experience.

In recent years, the home theater market has experienced a period of adjustment after rapid growth, and consumers have become more rational in their choice of products, paying more attention to cost-effectiveness and long-term value. Since 2020, due to the impact of the global epidemic, the demand for home entertainment has surged, but it has also exposed problems such as unstable supply chains and rising raw material prices, which have posed challenges to the capital chain of some enterprises. In the future, investment may be more prudent, and market growth may slow down, but high-quality, innovative products and services are still expected to be favored by the market.

Industry concentration is expected to be further enhanced, and technological innovation and brand influence will become the key to differentiating enterprises. As consumers' acceptance of smart homes increases, companies that can quickly adapt to market demand and provide intelligent, personalized solutions will occupy more market share. At the same time, changes in the financial environment, such as the adjustment of credit policies, may also affect the purchasing power of consumers, which in turn will affect the sales of home theater products.

Qianji Investment Bank believes that the challenges faced by the home theater industry include accelerated technology iteration, fierce market competition, and rapid changes in user preferences. Therefore, companies in the industry need to adopt a "core-focused, innovation-driven, and adaptable" strategy, focus on technology research and development, improve user experience, and strengthen cooperation with partners to jointly build a healthy and sustainable home theater ecosystem. In the short term, strengthening cash flow management, optimizing cost structure, and ensuring on-time product delivery and service quality will be the key to the steady progress of the enterprise.

Author: Qianji Investment Bank

Cover: AI-generated

Ticker Name

Percentage Change

Inclusion Date