Source: Market Cap

Solved the problem of "stuck neck" of key strategic materials.

Author Fusu

Edited by Xiaobai

Superalloys, as an advanced metal material, have always been irreplaceable key materials in modern aerospace engines, gas turbines and steam turbine hot end components.

It can be said that without superalloys, there would be no modern aerospace industry.

(Application of superalloys in aero engines).

Due to the strategic nature of superalloys, some Western countries have imposed blockades on some superalloy products and grades in China, such as the United States, which has made it clear that military superalloy materials are completely banned from being exported to China.

In this context, the "stuck neck" problem of superalloy is undoubtedly related to the batch replacement production of China's military fighters, the "two-machine special", nuclear power engineering and other national defense and security fields.

In recent years, a domestic superalloy manufacturer has filled the domestic technology gap by developing a high return ratio regenerated superalloy preparation process route, and broke the technological monopoly of developed countries led by United States.

This company is the company listed on the GEM of the Shenzhen Stock Exchange on October 16 (301522. SZ, "the Company").

"AVIC" background, with state-owned shareholders participating in the shares

Founded in 2007, the full name of Shangda Co., Ltd. is "AVIC Shangda Superalloy Materials Co., Ltd.", and has won the titles of National High-tech Enterprise, National Specialized and New "Key Little Giant" Enterprise, and Hebei Science and Technology Leading Enterprise.

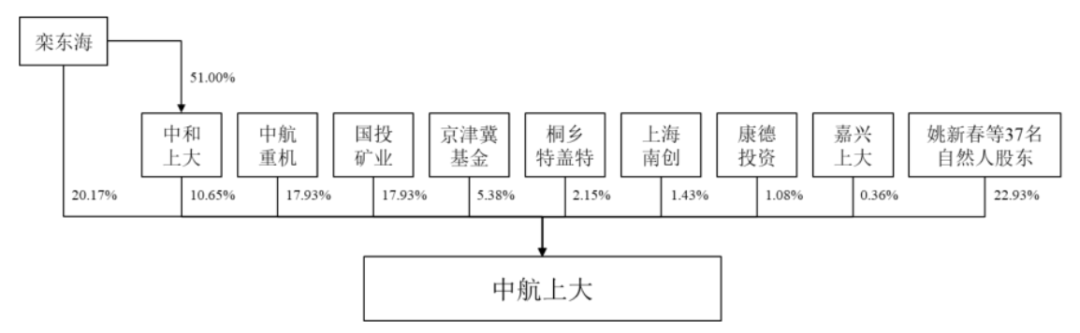

The company is a mixed-ownership enterprise with the participation of central enterprises. As of the IPO, Luan Donghai was the controlling shareholder and actual controller of the company, holding a total of 30.82% of the shares.

Other major state-owned assets, including AVIC Heavy Machinery (600765. SH), SDIC Mining and Beijing-Tianjin-Hebei Fund, holding 17.93%, 17.93% and 5.38% of the shares respectively.

(Source: Company Prospectus).

The company has a deep relationship with the "AVIC Department".

By the way, in this IPO, the company continues to gain the favor of state-owned assets.

According to the disclosure, the company issued 92.97 million shares at a price of 6.88 yuan per share, and all of them were new shares, and the original shareholders did not sell shares publicly.

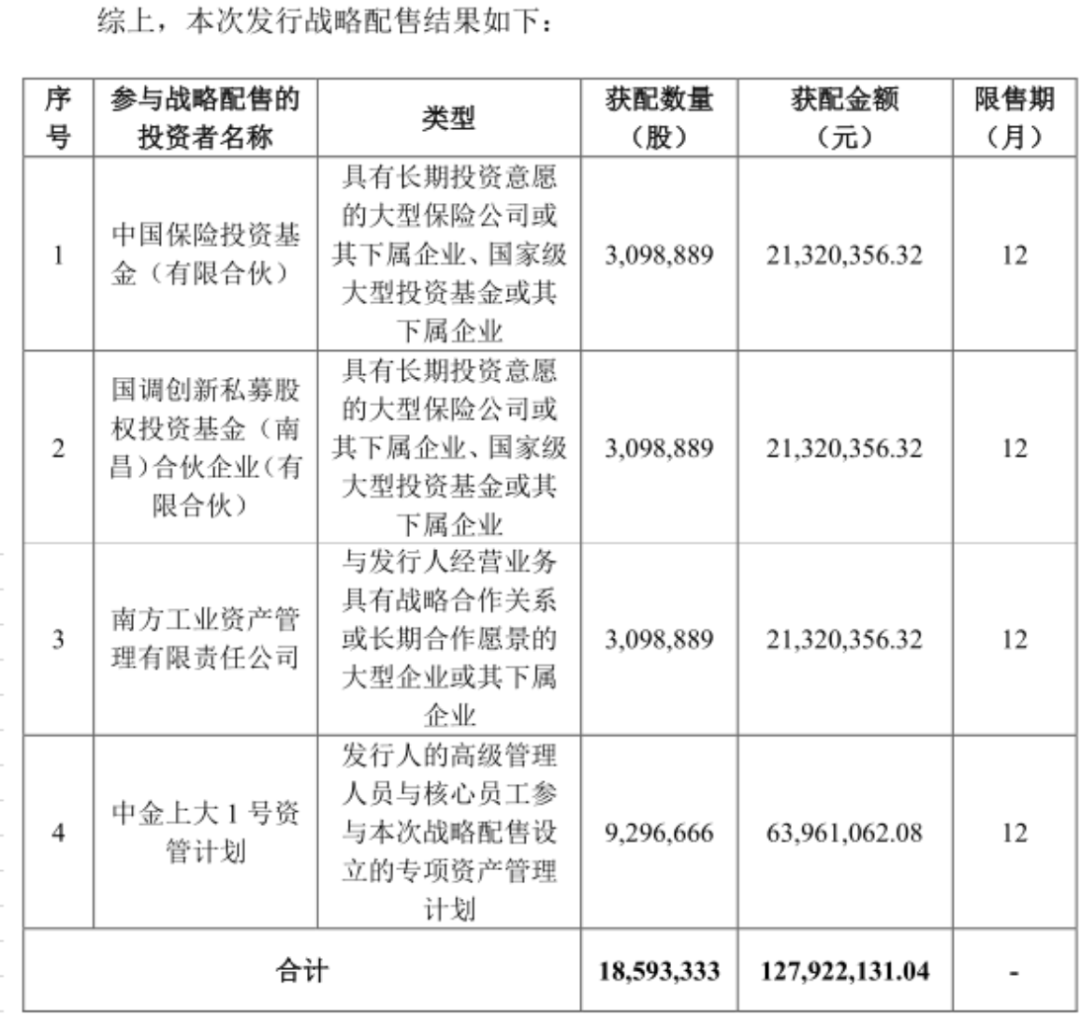

Among them, the number of shares issued in the strategic placement is 18.59 million shares, accounting for about 20% of the issued shares.

Among the shareholders participating in the placement, in addition to the company's employee shareholding platform "CICC Shangda No. 1", they also include China Insurance Investment Fund, Guotuo Innovation and Southern Industry, all of which are state-level large-scale investment funds or large state-owned enterprises.

(Source: Company Prospectus).

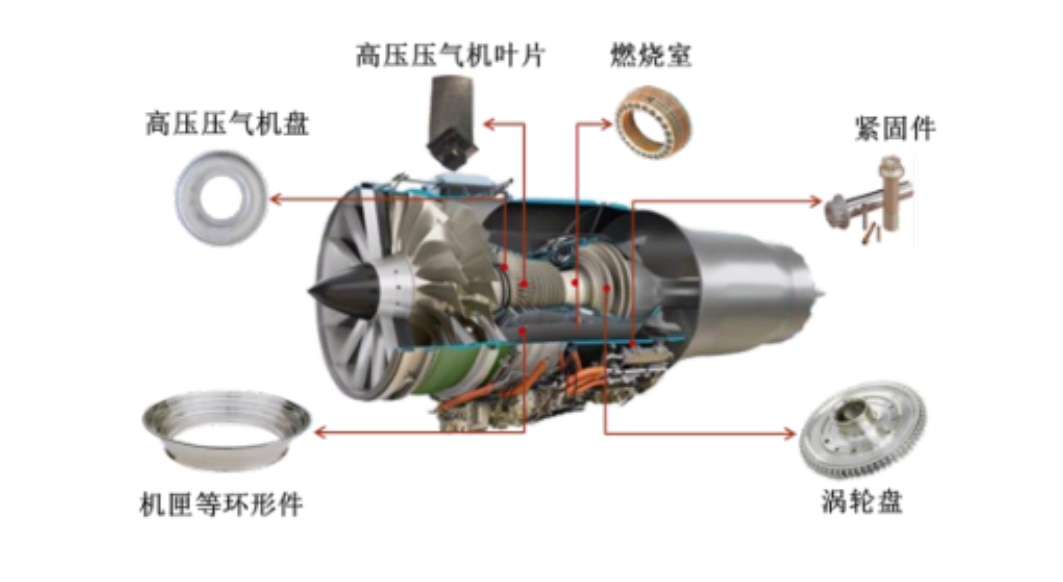

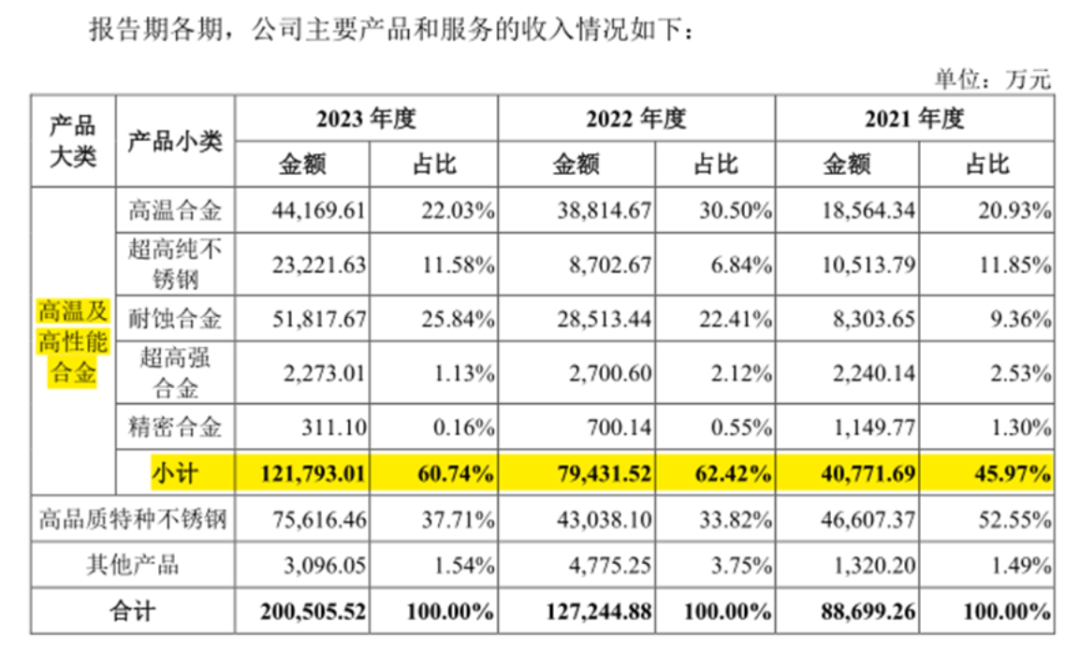

The company's main business is R&D, production and sales of special alloys represented by superalloys, and at the same time for the military and civilian markets, including high-temperature alloys, ultra-high-strength alloys, ultra-high-purity stainless steel, high-quality special stainless steel, etc.

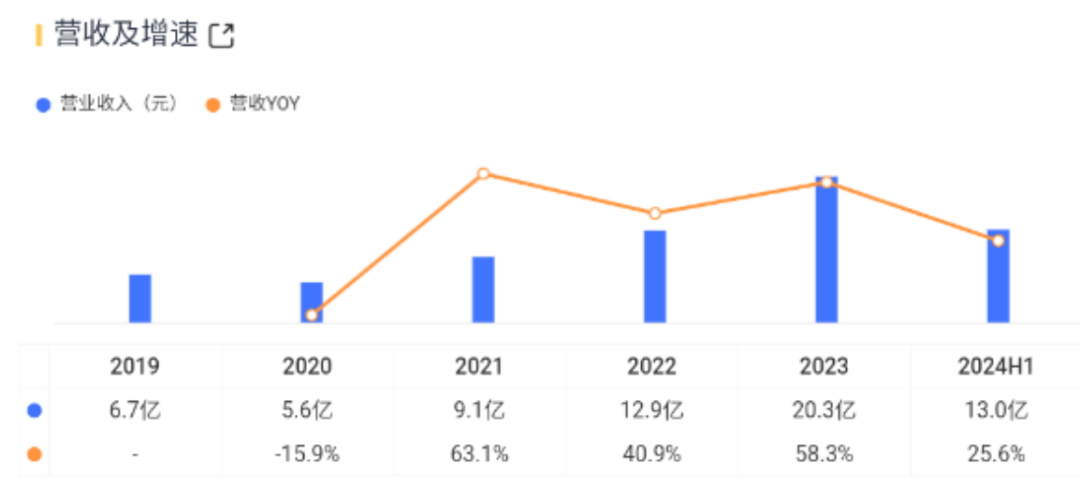

From 2021 to 2023, the company's revenue increased from 910 million yuan to 2.03 billion yuan, an increase of 58% year-on-year in 2023.

(Source: Market Cap App).

During the period, the position of high-temperature and high-performance alloys as the company's core business was stable, and the business revenue increased from 410 million yuan to 1.22 billion yuan, accounting for 46% to 61%.

(Source: Company Prospectus).

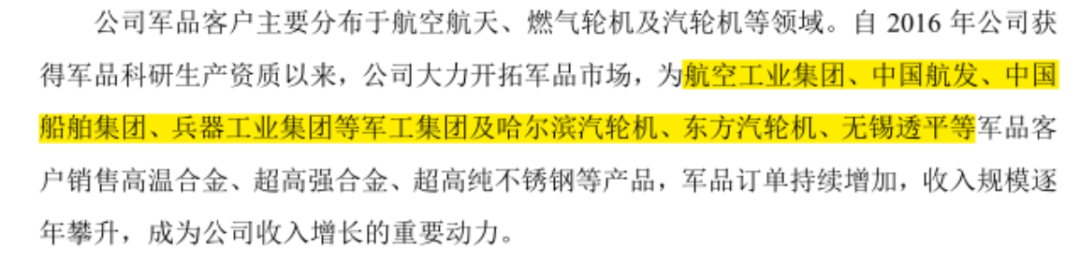

In 2016, the company obtained the qualification of military scientific research and production, and since then has sold superalloys and other products to military customers in the fields of aerospace and steam turbines.

According to the disclosure, the company's military customers include Aviation Industry Corporation of China, AECC, China Shipbuilding (600150. SH), Ordnance Industry Group and other military industrial groups, as well as Harbin Steam Turbine, Dongfang Steam Turbine, Wuxi Touping and other military enterprises.

(Source: Company Prospectus).

In recent years, military sales have become a new driver of the company's revenue. According to the disclosure, in 2022 and 2023, the company's military sales revenue will increase by 87% and 11% year-on-year, respectively.

In 2023, the company's military sales revenue will be 510 million yuan, accounting for 26% of the revenue in the same period.

(Source: Company Prospectus).

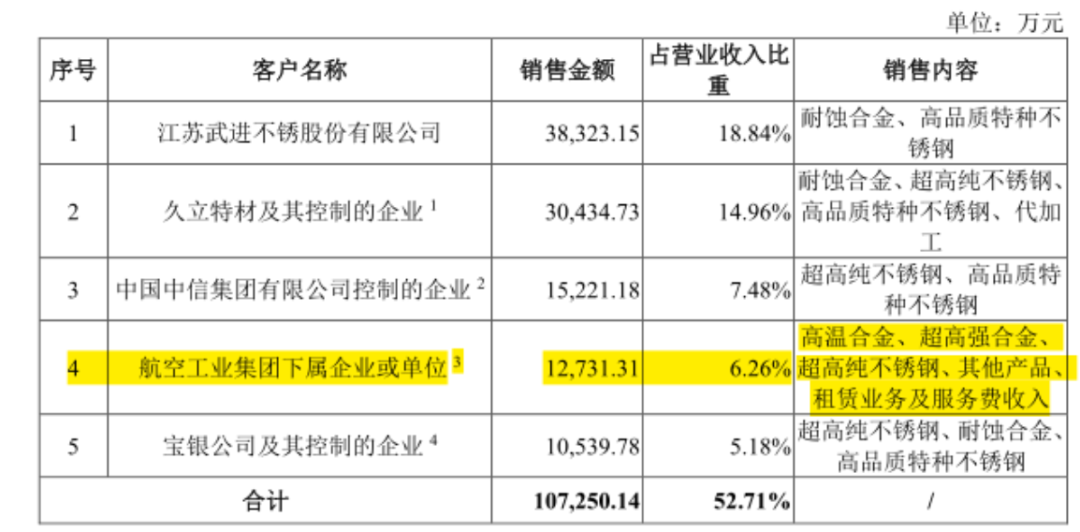

Since the development of China's aerospace industry is mainly dominated by large state-owned assets represented by Aviation Industry Corporation of China, the company's customer concentration as an upstream supporting enterprise is also high.

However, judging from the sales of the top five customers, the company does not have an over-dependence on the AVIC system.

According to the disclosure, from 2021 to 2023, the total sales of the company's top five customers will account for 51%-53%. During this period, the sales proportion of AVIC enterprises will not exceed 8%, and 6.3% in 2023.

(Source: Company Prospectus).

The above shows that the company has a strong ability to continue to develop new customers and obtain new orders in aerospace, nuclear power, gas turbines, steam turbines, petrochemicals and other fields.

It is the only one in China to master the application technology of high-temperature alloy return material recycling

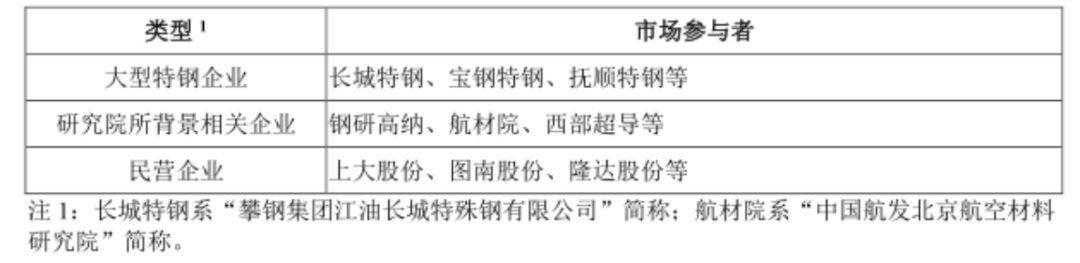

At present, the number of enterprises engaged in the research and development and preparation of superalloys in China is small, only more than a dozen.

Among them, Great Wall Special Steel, Baosteel Co., Ltd. (600019. SH), Fushun Special Steel (600399. SH) and other large state-owned special steel enterprises, as well as the steel research institute Gaona (300034. SZ), Aviation Materials Co., Ltd. (688563. SH), Western Superconductor (688122. SH) and other enterprises with scientific research institute background.

(Source: Company Prospectus).

The

focus of investors' attention undoubtedly revolves around a question: under the current situation of the concentration of the head of the domestic superalloy industry, is the company competitive as a relatively young and small "civilian army" enterprise?

In Fengyunjun's view, domestic superalloys are a market where downstream demand continues to grow and existing production capacity is difficult to meet.

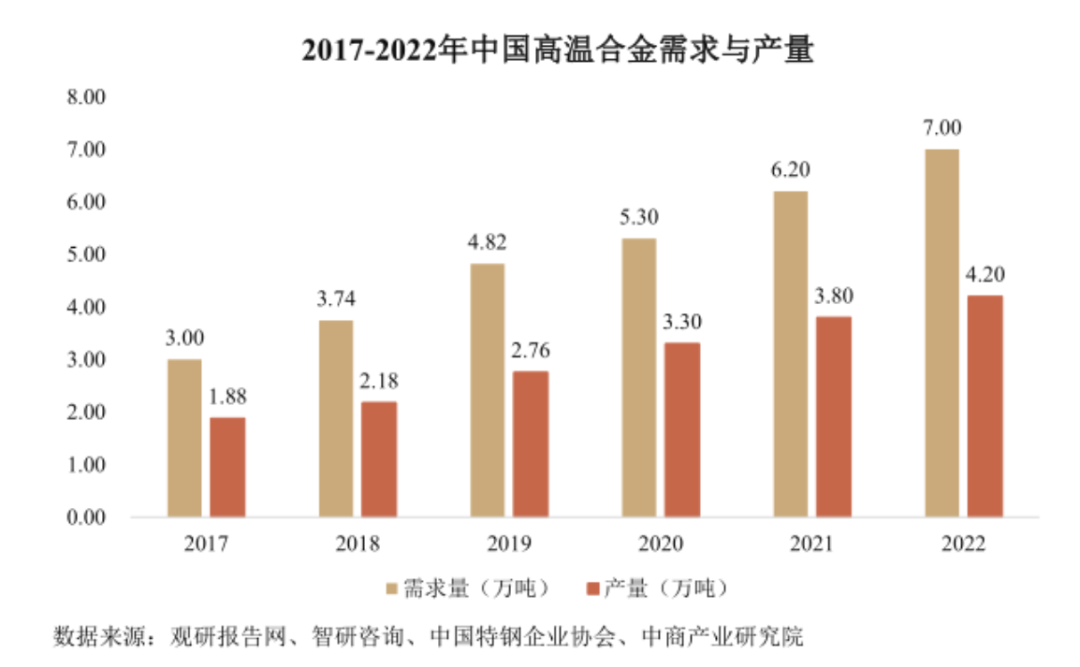

As a key material for China's high-end equipment manufacturing, in recent years, the market demand has been greater than the supply, and the gap between supply and demand has been expanding year by year.

According to third-party industry data, from 2017 to 2022, China's demand for superalloys increased from 30,000 tons to 70,000 tons, with a CAGR of 18%; Production increased from 19,000 tonnes to 42,000 tonnes, with a CAGR of 17%.

(Source: Company Prospectus).

The above-mentioned demand gap is mainly solved by imports. According to the disclosure, China's dependence on superalloy imports has been high, close to 50%.

The key to achieving "domestic substitution" lies in solving the problem of "high price and low quality" of domestic superalloys through technology research and development.

The

reason for the above differences is that foreign countries have developed mature superalloy recycling technology, while China once lacked technology and standards in this regard.

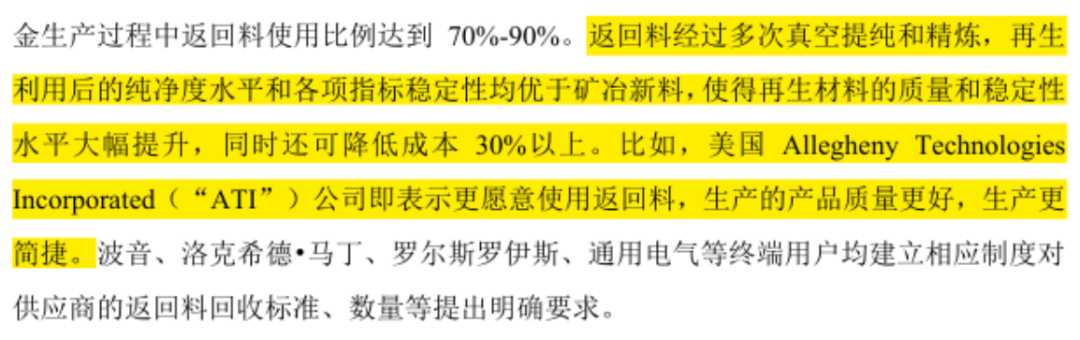

The recycling technology of superalloy refers to the use of the returned material generated in the previous processing link in the manufacturing process of superalloy to obtain new superalloy materials through vacuum purification, remelting, forging and casting and other processing links.

It should be pointed out that the recycled superalloy prepared from the returned material can not only reduce the production cost, but also its quality and stability are even better than that of the new material due to repeated vacuum purification and refining.

For example, Allegheny Technologies (ATI.N), the largest special steel producer in the United States, said it prefers to use returned material because it produces better quality and easier production.

As early as the 70s of the 20th century, United States carried out the recycling of superalloy recyclables, and has formed a recycling technology system with mature technology and perfect system.

However, China's superalloy industry started late, and for a long time, developed countries have adopted a technical blockade on China in terms of superalloy products involving the aerospace field, especially since 2018, and the blockade trend has been intensifying.

In recent years, the company has been committed to establishing a recycling system for superalloy returns to fill the technical gap in this area in China.

According to the disclosure, the company has undertaken 56 major projects, participated in more than 40 military product verification reviews, and achieved early intervention in the pre-research stage of high-end equipment in the fields of aerospace, weapons, gas turbines, nuclear engineering and other fields.

During this period, the company has obtained 46 invention patents and 20 utility model patents, and currently has more than 110 professional and technical personnel in the production and preparation of superalloys and other special alloys.

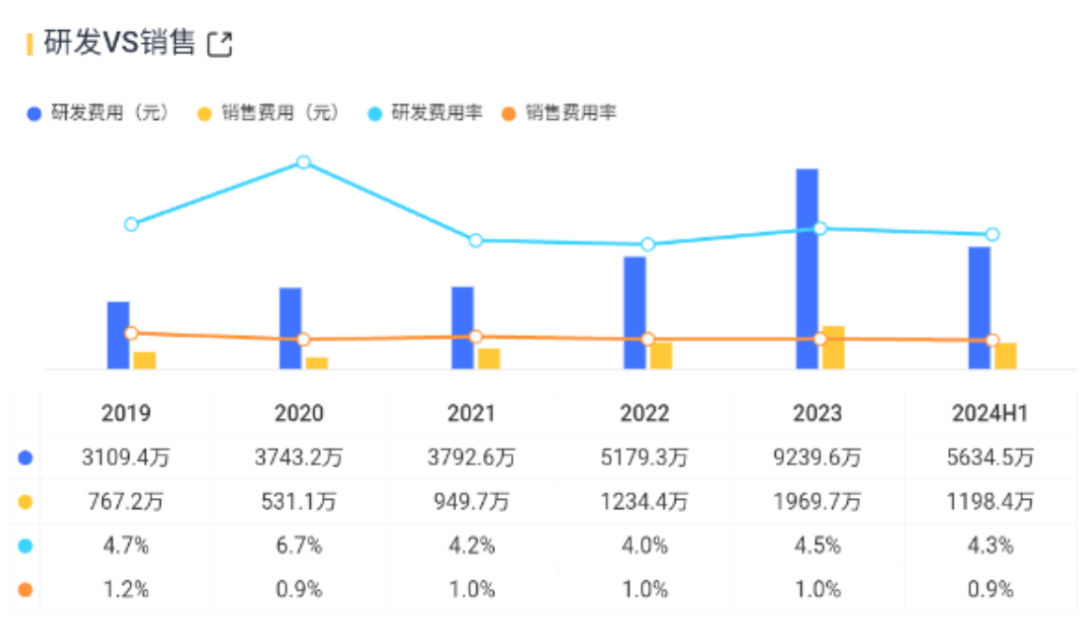

The company's R&D drive is distinctive. From 2019 to 2023, the company's R&D expenses increased year by year, and the annual R&D expense rate remained above 4%, and in 2023, it was 4.5%, an increase of 0.5 percentage points year-on-year.

In contrast, the company's selling expense ratio is low, maintaining around 1%.

(Source: Market Cap App).

Years of R&D investment have finally brought the company the accumulation of core technologies.

This means that the company has since broken the technological monopoly of developed countries led by United States.

At present, the company's R&D achievements have blossomed in many places, and have made outstanding contributions to the independent controllability and recycling of key strategic materials in China.

At this stage, the company is benefiting from the cost advantages brought by the recycling application technology of superalloy returns.

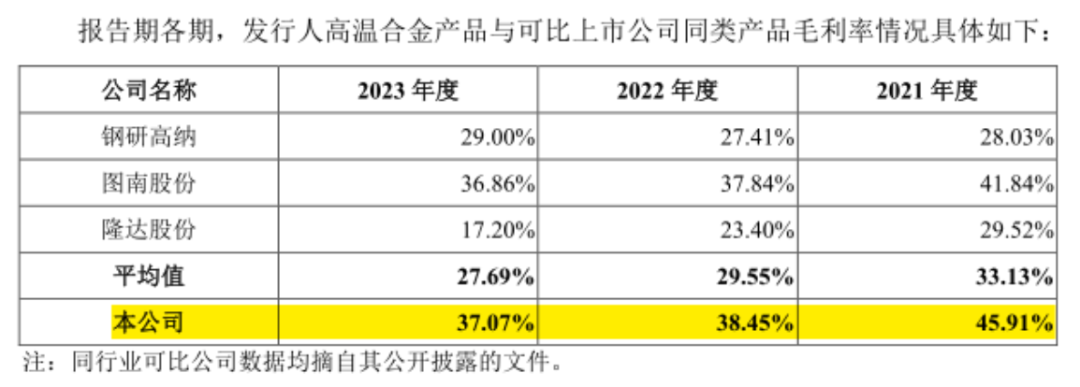

From 2021 to 2023, the gross profit margin of the company's superalloy products has been higher than that of comparable companies in the same industry, with 37.1% in 2023, more than 9 percentage points higher than the average of 27.7% in the same industry.

(Source: Company Prospectus).

There is an urgent need to release production capacity through fundraising

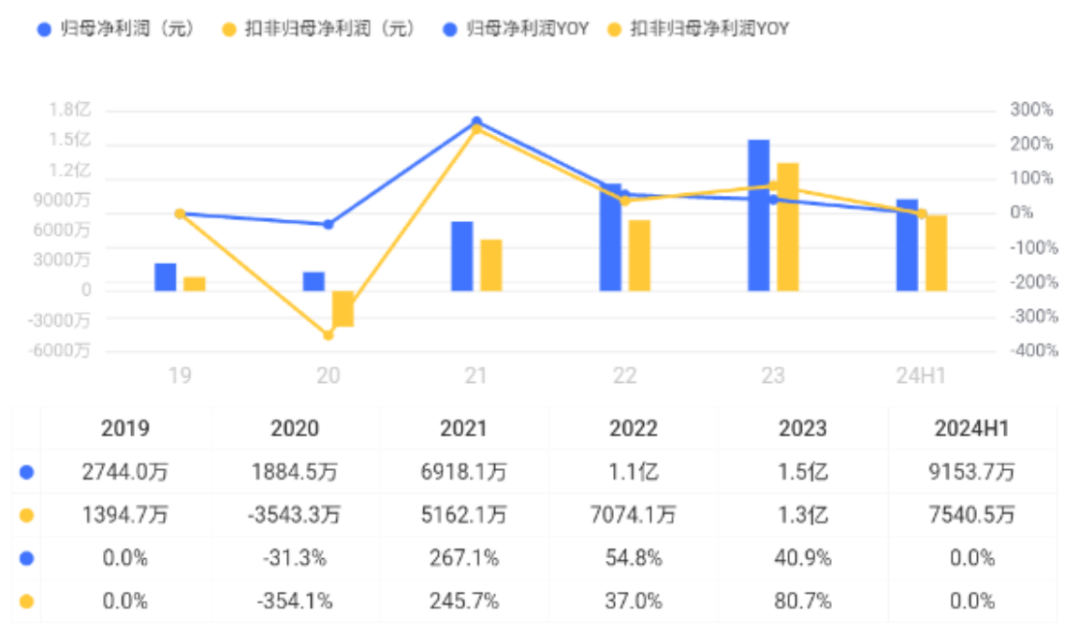

In recent years, with the expansion of the company's production scale and the scale effect, the company has begun to enter the stage of stable profitability.

Since 2021, the company's net profit attributable to the parent company and non-net profit deducted have continued to increase year-on-year. In 2023, the company's net profit attributable to the parent company will be 150 million yuan, an increase of 41% year-on-year; deducted non-net profit of 130 million yuan, an increase of 81% year-on-year.

(Source: Market Cap App).

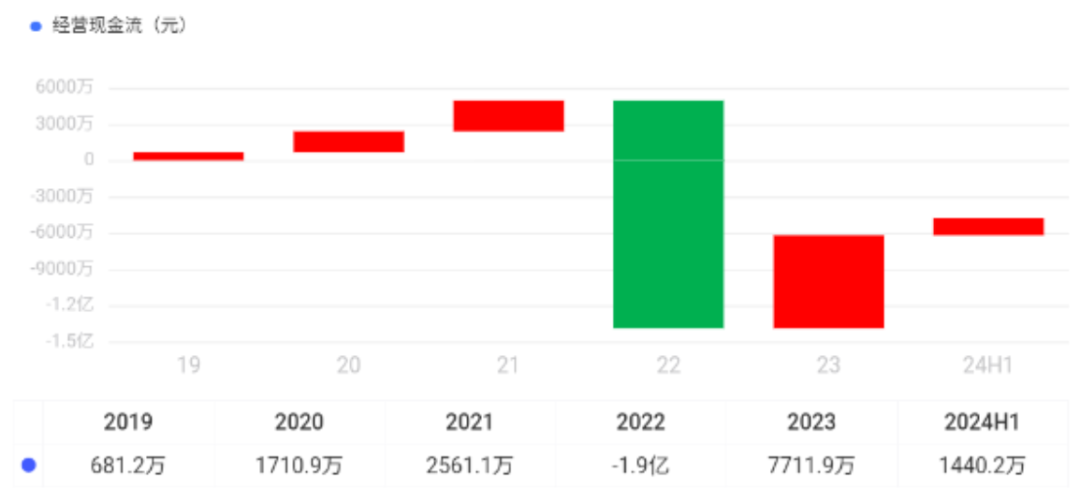

Cash flow can directly reflect the quality of a company's earnings. Judging from the disclosure, in most periods, the company has been able to achieve a net inflow of cash flow from operating activities.

(Source: Market Cap App).

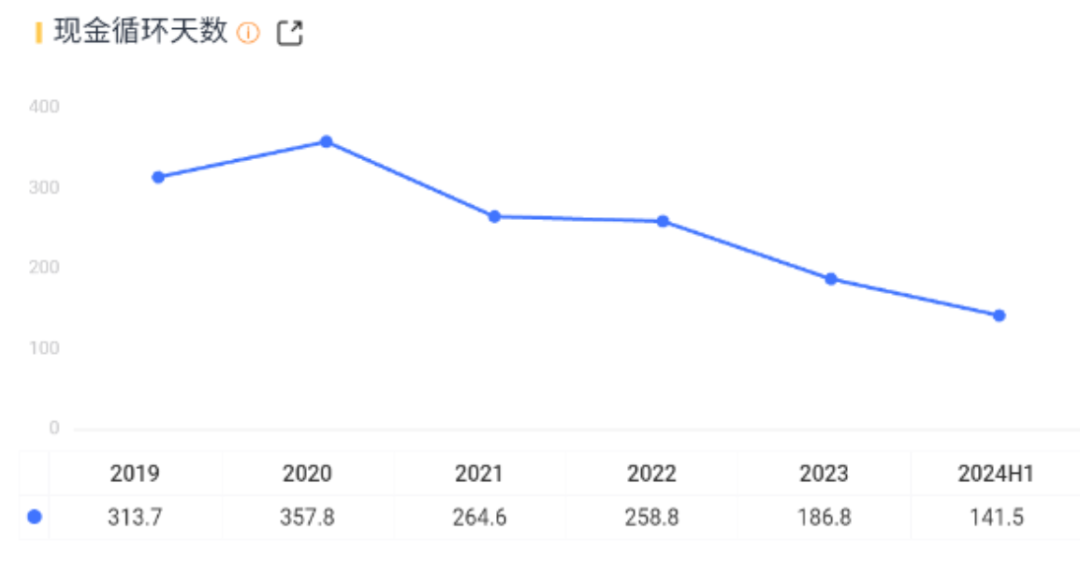

The company's cash cycle days have improved significantly, from 314 days in 2019 to 187 days in 2023, a reduction of 127 days, indicating that the company's capital use efficiency has improved significantly.

(Source: Market Cap App).

In Fengyunjun's view, the outstanding problem that the company is currently facing is that the existing production capacity is still difficult to meet the needs of the market, which restricts growth.

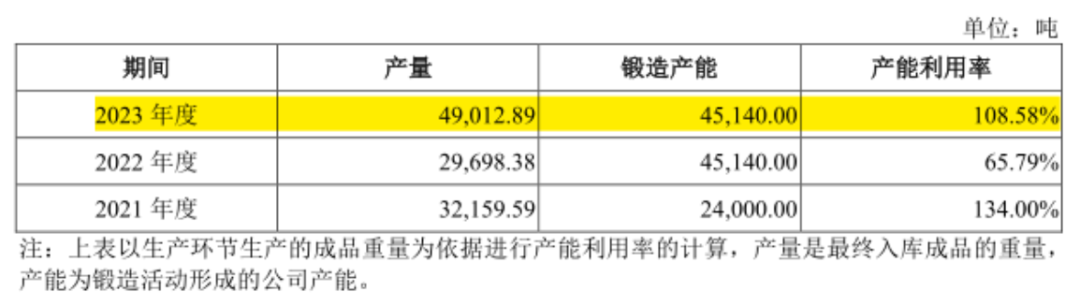

In 2022, the company completed the expansion of production capacity, and the production capacity was 45,000 tons by the end of the year, nearly doubling from the end of 2021.

However, due to the strong downstream demand, in 2023, the company's new capacity will be quickly digested, and the capacity utilization rate will also rebound to the saturation level, reaching 109%.

(Source: Company Prospectus).

It is worth noting that the superalloy industry has formed a high barrier to entry due to the complex production process and the long verification cycle of downstream customers. Therefore, the growth of industry capacity is dominated by the expansion of existing manufacturers.

In the vernacular, what the company needs to do now is nothing more than to expand production capacity at full speed and show its strength to meet the huge stock and incremental market.

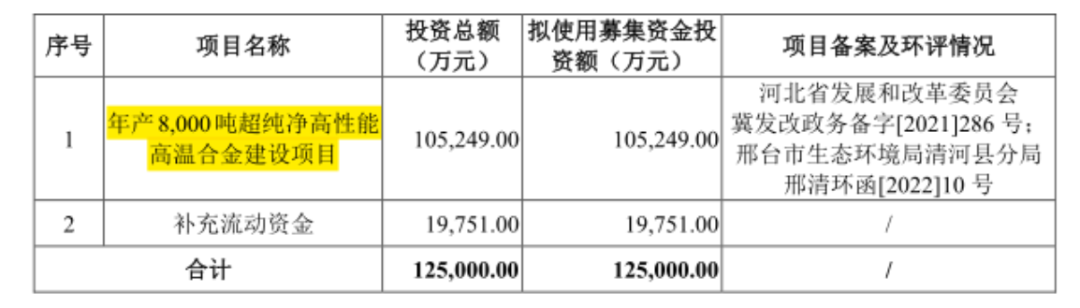

According to the disclosure, the company's IPO raised 125 million yuan, of which more than 105 million yuan, accounting for about 84% of the funds, is planned to be invested in the "annual output of 8,000 tons of ultra-pure high-performance superalloy construction project".

(Source: Company Prospectus).

It is foreseeable that the fund-raising project will greatly make up for the lack of the company's existing production capacity. With the implementation of new production capacity, the company's growth potential is expected to be unleashed.

Shangda Co., Ltd. is the representative of the "new quality productivity" of China's superalloy industry, and the company is the first and only enterprise in China to master the application technology of superalloy regeneration and realize industrialization.

As a key strategic material in the field of high-end equipment manufacturing such as aerospace and nuclear power, the company has made outstanding contributions to the country's national defense security and resource security.

The company itself has also benefited from the improvement of R&D and manufacturing levels, realized the optimization of product structure, and the cost advantage of leading peers.

Disclaimer: This report (article) is an independent third-party research based on the public company nature of listed companies and the core information publicly disclosed by listed companies in accordance with their statutory obligations (including but not limited to temporary announcements, periodic reports and official interactive platforms, etc.); Market Value strives to be objective and fair in the content and opinions contained in the report (article), but does not guarantee its accuracy, completeness, timeliness, etc.; The information or opinions expressed in this report (article) do not constitute any investment advice, and Market Capitalization does not assume any liability for any actions taken as a result of the use of this report.

The above content is the original of the Market Value Fengyun APP

Special statement: The above content only represents the author's own views or positions, and does not represent the views or positions of Sina Finance Headlines. If you need to contact Sina Finance Toutiao due to the content of the work, copyright or other issues, please do so within 30 days after the above content is published.

Ticker Name

Percentage Change

Inclusion Date