The story of "domestic substitution", does it still work?

1

Net profit fell by 320%.

United Imaging Medical's (688271) third quarterly report is a bit heart-wrenching.

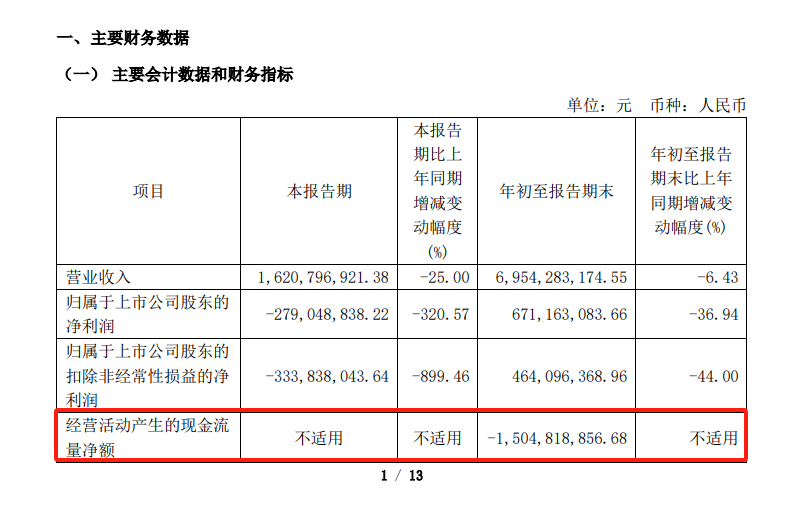

According to the financial report, in the first three quarters of this year, United Imaging Medical achieved operating income of 6.954 billion yuan, a year-on-year decrease of 6.43%; the net profit attributable to the parent company was 671 million yuan, a year-on-year decrease of 36.94%; The net profit after deducting non-attributable to the parent company was 464 million yuan, a year-on-year decrease of 44.00%.

If we focus on the third quarter, the situation is even more severe. In the third quarter of this year, United Imaging Medical's operating income was 1.621 billion yuan, a year-on-year decrease of 25.00%; net profit attributable to the parent company -279 million yuan, a year-on-year decrease of 320.57%; Net profit after deducting non-attributable to the parent company was -334 million yuan, a year-on-year decrease of 899.46%!

A little longer, the trend has already appeared.

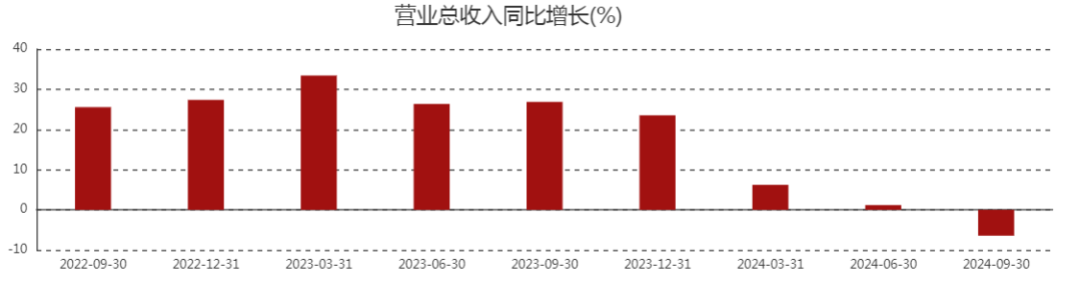

From the perspective of revenue, since the beginning of 2024, United Imaging Medical's revenue growth has slowed down until the third quarter.

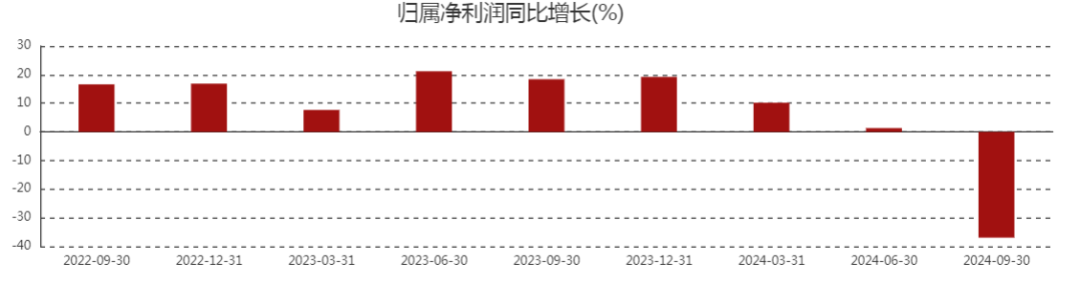

The trend in net profit is similar, with a steeper downward curve than revenue.

From the perspective of the capital market, as of the close of trading on November 12, 2024, United Imaging Medical's share price is 139.40 yuan per share, which is 35% lower than the previous high.

In August 2022, United Imaging Healthcare officially landed on the Science and Technology Innovation Board of the Shanghai Stock Exchange, with an initial public offering price of 109.88 yuan per share and a total of 10.988 billion yuan.

This record made United Imaging Healthcare the largest IPO of the year on the Science and Technology Innovation Board, and the third largest IPO since the opening of the Science and Technology Innovation Board.

On the first day of listing, United Imaging Medical rose by more than 60%, and its market value once exceeded 150 billion. With the halo of "the first domestic high-end medical imaging equipment", United Imaging Medical once had unlimited scenery.

But the aura didn't last long. In September 2023, United Imaging Healthcare's share price once fell to more than 100 yuan, down more than 50% from its previous high.

Taking advantage of this round of market, United Imaging Medical's stock price has risen a little, but it is still far from its original glory.

What's even more curious is that with such a three-quarter report, what has United Imaging Medical experienced?

2

The ability to "make blood" is questioned

The answer can also be found in the financial report.

There is a factor in the industry environment here. It is mainly reflected in two aspects, one is the impact of medical anti-corruption, and the other is the impact of the progress of medical equipment update. These directly lead to the delay of hospital procurement, the delay in the purchase of equipment by hospitals, and where do equipment companies get orders and income?

For example, data from SDIC Securities shows that in the first half of 2024, the bidding scale of the medical equipment industry will be about 55 billion yuan, a year-on-year decrease of about 35%.

Industry factors cannot be ignored, but the more critical reasons have to be found from within United Imaging Healthcare.

Looking through the financial report of United Imaging Medical, there is a data that has attracted the author's attention-

In the first three quarters of this year, United Imaging Healthcare's net cash flow from operating activities decreased by about 1.505 billion yuan.

According to the company, this was due to a decrease in revenue and collections. With curiosity, I looked at the company's payment situation, which I didn't know, and I was shocked when I saw it.

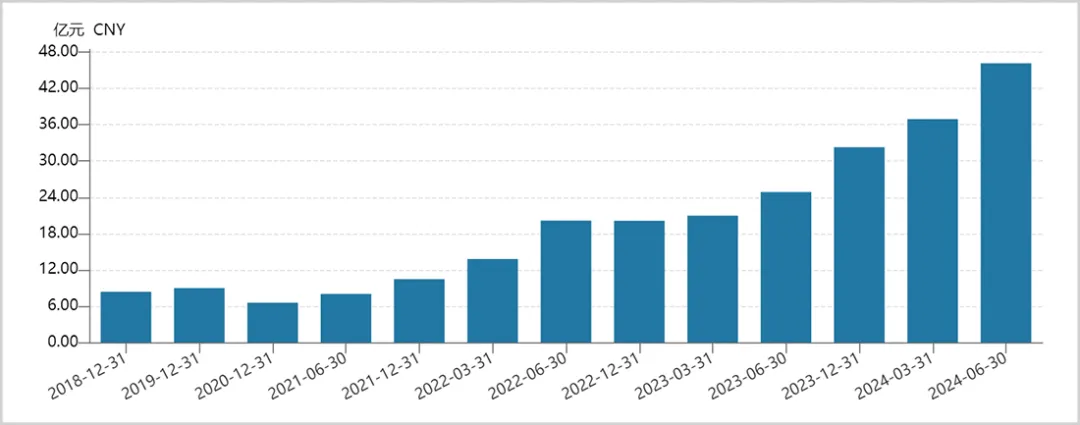

According to the financial report, as of the first half of 2024, United Imaging Medical's accounts receivable reached 4.615 billion yuan, a significant increase of 350% from the end of 2021. The company's latest accounts receivable have accounted for more than 85% of the revenue in the same period.

▲United Imaging Medical's accounts receivable trend, source: Wind

What is this concept? The data shows that looking at the same industry, the scale of accounts receivable accounts for about 65% of the revenue in the same period. In other words, the proportion of United Imaging Medical is indeed high.

With such a large scale of accounts receivable, people have to worry about the company's potential bad debt risk.

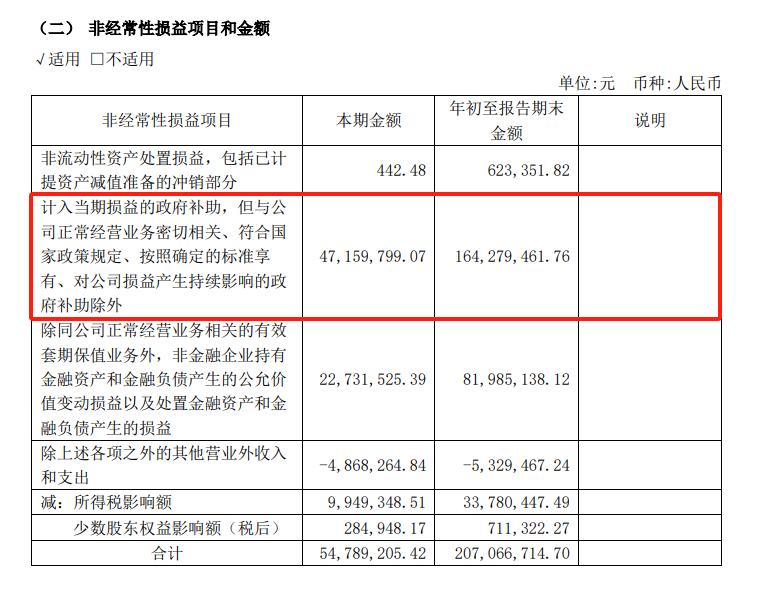

Another statistic worth paying attention to is subsidies.

According to the United Imaging Medical prospectus, from 2019 to 2021, the company received government subsidies of 306 million yuan, 348 million yuan, and 438 million yuan respectively, with a total of 1.092 billion yuan.

In 2020 and 2021, when profits were realized, government subsidies accounted for 30.11% and 25.83% of the total profit, respectively—accounting for 47.62% of the cumulative net profit.

According to the latest financial report, the government subsidy included in United Imaging Medical in the first nine months of 2024 is 164 million yuan.

In other words, in the past few years, a large part of United Imaging Healthcare's revenue has come from government subsidies, which can't help but make people question United Imaging Healthcare's own "hematopoietic" ability.

3

Deeply trapped in the low-end market

Looking deeper, the weakness of this "hematopoietic" ability is related to the product layout.

United Imaging Medical has been sought after by capital before, telling the story of "domestic substitution".

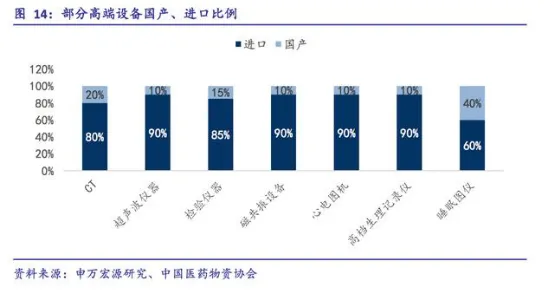

For a long time, due to the lack of core technology, high-end medical equipment has been our shortcoming.

The "2014-2018 China Medical Device Industry Market Prospect and Investment Forecast Analysis Report" shows that in the field of medical devices in China, about 80% of the CT market, 90% of the ultrasonic instrument market, 85% of the inspection instrument market, 90% of the magnetic resonance equipment, 90% of the high-end physiological recorder and 60% of the sleep chart market are monopolized by foreign-funded enterprises.

What United Imaging Healthcare hopes to do is to break this monopoly and replace high-end medical equipment in China.

According to the data, in terms of market share, United Imaging Healthcare's MR market share has increased from 7.6% in 2019 to 21.3% in 2023, ranking third in the country. The CT market share increased from 7.8% in 2019 to 23.5% in 2023, ranking second in the country.

United Imaging Healthcare is indeed moving towards the goal of "domestic substitution". But another fact, a little embarrassing:

It is still struggling in the low-to-mid market.

Industry observer "Archimedes Biotech" has done a combing that in 2021, among United Imaging Medical's MR products, 1.5T (including 1.43T) MR sales accounted for 79%:

The low-end 1.43T MR is favored by many grassroots hospitals because of its high cost performance and has become the main product of sales.

The same situation occurred in the field of CT, in the same period, the sales of United Imaging Medical's economical CT (CT with 60 detector rows and below) accounted for 86%, and the growth of mid-to-high-end CT stagnated.

To use a not necessarily appropriate analogy, this is like making a mobile phone, it can produce cost-effective low-end mobile phones, and the sales are also good, but if you want to wrestle with a high-end machine like Apple and Samsung, it is almost meaningless.

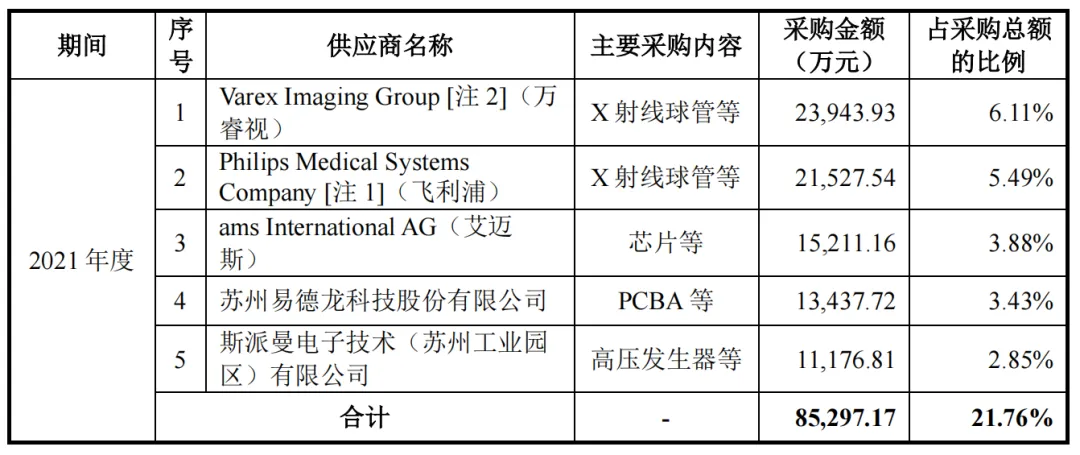

What's even more surprising is that the core components of United Imaging Healthcare's important products still rely on external procurement.

These parts include tubes and high-voltage generators for the production of CT products, X-ray tubes, high-voltage generators and flat panel detectors for the production of XR products. Taking CT tubes as an example, the main suppliers are Varex in the United States and Philips in the Netherlands. And these products are basically the main force of the company's revenue.

What is this concept? It's like if you make a mobile phone, the chip has to rely on the outside, and you can only watch it get stuck in the neck when something happens.

4

Epilogue

United Imaging Healthcare still has a long way to go.

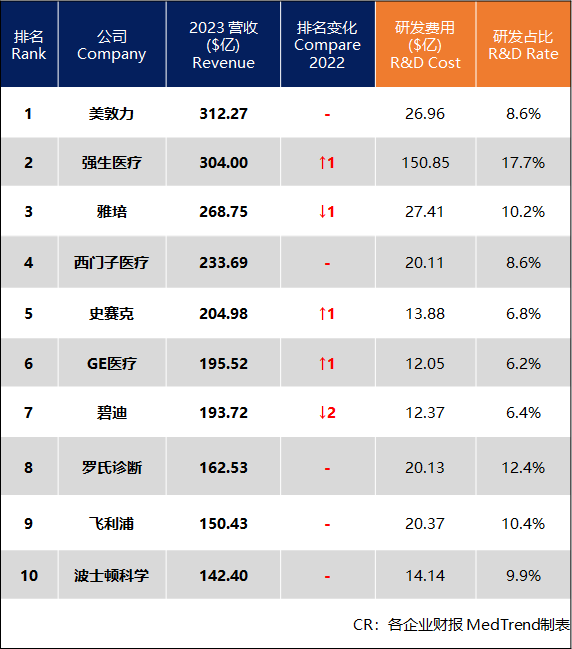

In 2023, United Imaging Medical's revenue will be 11.411 billion yuan. In the same period, the international giants, Siemens Healthineers, GE Healthineers, GE Healthineers, and Philips Healthcare, had revenue of 168.9 billion yuan, and Philips Healthcare.

In the end, United Imaging Medical's revenue is almost 1/10 of others.

If you want to become a real industry giant, you have to go global. The three global healthcare giants all account for more than 50% of their revenue from non-local regions.

On the other hand, United Imaging Medical's revenue share in the international market has increased greatly compared with previous years, but it is still only about 20%.

And, according to industry insiders, United Imaging Medical is facing a serious problem overseas:

(Many of its products) are directly from Siemens pulled a team to do it, so its set of patents may be used in other people's patents, and they will be allowed to be sued overseas.

In addition to patent issues, there are also product positioning issues, according to the analysis of industry insiders:

The unit price of the product is too high, but the update frequency of hospital equipment is not so high, for example, an MRI, unless it is a tertiary hospital, otherwise the general tertiary hospital, in fact, it is good to buy it once in 5 years.

Objectively speaking, United Imaging Medical still has tenacity and momentum. I took a look at the fact that from 2019 to 2021, United Imaging Healthcare's R&D investment totaled nearly 2.6 billion yuan, accounting for 16.25% of its revenue in the same period. Whether from the perspective of peers or the entire technology field, this proportion is not low.

But in the fierce business scene, this is not enough, or the same sentence:

Sailing against the current, if you don't advance, you will retreat.

Ticker Name

Percentage Change

Inclusion Date