Log in to the Sina Finance APP and search for [Xinphi] to see more evaluation grades

point of view

Last week (11/11-11/15) semiconductors lagged behind most major indices. Last week, the ChiNext index fell 3.36%, the Shanghai Composite Index fell 3.52%, the Shenzhen Composite Index fell 3.70%, the SME Index fell 3.25%, Wind All A fell 3.94%, and the Shenwan Semiconductor Industry Index fell 4.34%. All sub-sectors of semiconductors fell, with the IC design sector falling the most, and other sectors falling the least. Among the semiconductor sub-sectors, the packaging and testing sector fell 3.6% last week, the semiconductor materials sector fell 3.5% last week, the discrete device sector fell 4.8% last week, the IC design sector fell 5.6% last week, the semiconductor equipment sector fell 3.7% last week, the semiconductor manufacturing sector fell 4.7% last week, and the other sectors fell 0.6% last week.

The

industry cycle is currently at the relative bottom of the long cycle, in the short term, the second half of the year into the traditional peak season, benefiting from the release of new flagship mobile phones, double eleven and other consumer festivals and other factors are expected to continue to grow in the industry terminal sales month-on-month, we believe that we should improve the sensitivity to demand-side innovation, priority by consumers to accept the AI terminal, is expected to become a new popular application, in the long run, the semiconductor blue chips that the Tianfeng Electronics team has covered are currently at a low level of valuation, Companies that continue to optimize and iterate in operation are expected to achieve better market share and profitability at the high point of the next cycle. In terms of innovation, it is expected that artificial intelligence/satellite communication/MR will be a major industrial trend, and the stocks in the industrial chain are expected to continue to reflect thematic opportunities with the progress of technological innovation.

Again, the investment opportunities for domestic substitution of semiconductors are emphasized. We have recently repeatedly emphasized the investment opportunities of domestic substitution of semiconductors in reports such as "Domestic Substitution Continues to Accelerate, Optimistic about Investment Opportunities in the Equipment and Materials Sector 20241023 and "Xiongguan Mandao is Really Like Iron, Domestic Substitution Should Be Self-Improvement, and Talk About Investment Opportunities in the Equipment and Materials Sector" 20241029. We highlight the urgent demand for domestic substitution of semiconductors, the large market space, and the potential catalysts brought by external (international political instability) and internal (large manufacturers to expand production, policy boosts, etc.) to the sector. We judge that the domestic substitution of domestic semiconductor equipment, materials, and EDA/IP is expected to continue to accelerate, and the investment opportunities in the sector are worth paying attention to.

SMIC Huahong released its 3Q24 financial report, with improved capacity utilization and stable guidance in the fourth quarter, indicating that the industry may enter the peak season.

SMIC's 3Q24 revenue hit a record high of $2.17 billion, QoQ +14%, in line with previous guidance (up 13% to 15% sequentially), and revenue growth benefited from ASP improvement due to the increase in the proportion of 12 inches. Gross margin improved to 20.5% quarter-on-quarter, slightly exceeding the previous guidance (18%-20%), and capacity utilization continued to improve to 90.4% in 3Q24. The company guides 2024Q4 revenue to increase by 0% to 2% quarter-on-quarter, and the gross profit margin is in the range of 18% to 20%, and the continuous quarter-on-quarter growth of revenue indicates that the industry may enter the peak season.

Hua Hong Semiconductor's 3Q24 revenue was US$526 million, QoQ was 10%, slightly exceeding the previous guidance range (US$500 million to US$520 million), gross margin increased to 12.2% quarter-on-quarter, slightly exceeding the previous guidance range (10% to 12%), and the capacity utilization rate reached 105.3% in 3Q24, of which 8-inch reached 113%, reflecting a strong supply and demand trend, and 12-inch reached 98.5% and continued to increase. The company has guided 2024Q4 revenue of $530-540 million, an increase of 1% to 3% sequentially, and the gross margin is expected to be 11%-13%, looking forward to the marginal positive impact of the new 12-inch production capacity release on the company's revenue.

Global semiconductor sales continued to grow month-on-month in September, increasing year-on-year for 11 consecutive months. According to SIA, global semiconductor sales reached US$55.32 billion in September, a year-on-year increase of 23.2%, achieving 11 consecutive months of year-on-year growth, of which the United States increased by 46.3% year-on-year, which is the fastest growing region, and China increased by 22.9% year-on-year in September, indicating that demand continues to improve.

It is recommended to pay attention to:

1) EDA/IP & Design Services: Brite / VeriSilicon / Empyrean / Primarius / Guangli Micro

2) Semiconductor design: Goodix Technology/Smartway/Yangjie Technology/Rockchip/Hengxuan Technology/Puran Shares/Longsys (Tianfeng Computer Joint Coverage)/Dongxin Shares/Fudan Microelectronics/Juquan Technology/Jingchen Shares/Lihe Microelectronics/Allwinner Technology/Espressif Technology/Cambrian/Loongson Zhongke/Haiguang Information (Tianfeng Computer Coverage)/Beijing Junzheng/Montage Technology/Juchen Shares/Diao Micro/NOVOSENSE Micro/Shengbang Shares/Zhongying Electronics/Star Semiconductor/Macro Micro Technology (Rights Protection) / Dongwei Semiconductor/Minde Electronics/Siruipu/Xinjieneng / GigaDevice / Weir Shares / Aiwei Electronics / Zhuosheng Micro / Jingfeng Mingyuan / Xidi Micro / Anlu Technology / Zhongke Lanxun

3) Semiconductor materials and equipment parts: Jacques Technology / Dinglong Co., Ltd. (Tianfeng Chemical Joint Coverage) / Heyuan Gas (Tianfeng Chemical Joint Coverage) / Zhengfan Technology (Tianfeng Machinery Joint Coverage) / North Huachuang / Fuchuang Precision / Jingzhida / Shanghai Silicon Industry / Shanghai Xinyang (Rights Protection) / China Micro Corporation / Anji Technology / Shengmei Shanghai / Zhongjuxin / Qingyi Optoelectronics / Research New Materials / Huate Gas / Nanda Optoelectronics / Kaimei Special Gas / Jinhaitong (Tianfeng Machinery Joint Coverage) / Hongrida / Jingce Electronics (Tianfeng Machinery Joint Coverage) / Tianyue Advanced / Guoli Shares / Xinlai Materials (Rights Protection) / Changchuan Technology (Tianfeng Machinery Coverage) / Linkage Technology / Maolai Optics / Aisen Shares / Jiangfeng Electronics

4) IDM OEM packaging and testing: Weice Technology/SMIC/Hua Hong Semiconductor/Changdian Technology/Tongfu Microelectronics/Times Electric/Silan Microelectronics/Yangjie Technology/Wingtech Technology (Rights Protection)/San'an Optoelectronics

5) Satellite industry chain: Hager Communication/Dianke Chip/Fudan Microelectronics/BDStar/Liyang Chip

Risk warning: unpredictable risks brought by geopolitics, demand recovery is less than expected, technology iteration is less than expected, and industrial policy changes are risky

1. Last week's view: domestic substitution continues to accelerate, optimistic about investment opportunities in the equipment and materials sector

Again, the investment opportunities for domestic substitution of semiconductors are emphasized. We have recently repeatedly emphasized the investment opportunities of domestic substitution of semiconductors in reports such as "Domestic Substitution Continues to Accelerate, Optimistic about Investment Opportunities in the Equipment and Materials Sector 20241023 and "Xiongguan Mandao is Really Like Iron, Domestic Substitution Should Be Self-Improvement, and Talk About Investment Opportunities in the Equipment and Materials Sector" 20241029. We highlight the urgent demand for domestic substitution of semiconductors, the large market space, and the potential catalysts brought by external (international political instability) and internal (large manufacturers to expand production, policy boosts, etc.) to the sector. We judge that the domestic substitution of domestic semiconductor equipment, materials, and EDA/IP is expected to continue to accelerate, and the investment opportunities in the sector are worth paying attention to.

SMIC Huahong released its 3Q24 financial report, with improved capacity utilization and stable guidance in the fourth quarter, indicating that the industry may enter the peak season.

SMIC's 3Q24 revenue hit a record high of $2.17 billion, QoQ +14%, in line with previous guidance (up 13% to 15% sequentially), and revenue growth benefited from ASP improvement due to the increase in the proportion of 12 inches. Gross margin improved to 20.5% quarter-on-quarter, slightly exceeding the previous guidance (18%-20%), and capacity utilization continued to improve to 90.4% in 3Q24. The company guides 2024Q4 revenue to increase by 0% to 2% quarter-on-quarter, and the gross profit margin is in the range of 18% to 20%, and the continuous quarter-on-quarter growth of revenue indicates that the industry may enter the peak season.

Hua Hong Semiconductor's 3Q24 revenue was US$526 million, QoQ was 10%, slightly exceeding the previous guidance range (US$500 million to US$520 million), gross margin increased to 12.2% quarter-on-quarter, slightly exceeding the previous guidance range (10% to 12%), and the capacity utilization rate reached 105.3% in 3Q24, of which 8-inch reached 113%, reflecting a strong supply and demand trend, and 12-inch reached 98.5% and continued to increase. The company has guided 2024Q4 revenue of $530-540 million, an increase of 1% to 3% sequentially, and the gross margin is expected to be 11%-13%, looking forward to the marginal positive impact of the new 12-inch production capacity release on the company's revenue.

Global semiconductor sales continued to grow month-on-month in September, increasing year-on-year for 11 consecutive months. According to SIA, global semiconductor sales reached US$55.32 billion in September, a year-on-year increase of 23.2%, achieving 11 consecutive months of year-on-year growth, of which the United States increased by 46.3% year-on-year, which is the fastest growing region, and China increased by 22.9% year-on-year in September, indicating that demand continues to improve.

2. Macro data of the semiconductor industry: semiconductor sales have resumed medium-to-high-speed growth in 24 years, and storage has become the key

Judging from the analysis of the prosperity in October 2024 and the development expectations of a number of leading distributors in the semiconductor industry, the growth expectations of each company in the second half of the year remain optimistic, and the Asia-Pacific region, especially the Chinese market, is still the key to growth.

Many mainstream institutions in the industry are more optimistic about the semiconductor market in 2024. Among them, WSTS said that due to the popularity of generative AI, the demand for related semiconductor products has increased sharply, and the storage demand is expected to show a significant recovery, so the global semiconductor sales will increase by 13.1% in 2024, reaching a record high again; IDC's view is more optimistic than WSTS, which believes that global semiconductor sales will reach $632.8 billion in 2024, a year-on-year increase of 20.20%; In addition, Gartner also believes that global semiconductor sales will usher in growth in 2024, with an increase of 16.80%, and the amount will reach $632.8 billion.

From the perspective of global semiconductor sales, the bottoming out of the semiconductor industry in 2023 has been basically completed, and the steady growth of manufacturers from Q3 for several months may lay the foundation for the semiconductor industry to bottom out. Some mainstream institutions/associations around the world have revised their 2024 global semiconductor sales forecasts upward, and the chip industry will see double-digit percentage growth of between 10% and 18.5% in 2024. IDC and Gartner are the most optimistic, forecasting growth of 20.2% and 18.5%, respectively.

In terms of sub-categories, the top three fastest growing WSTS forecasts in 2024 are storage, logic, and processors, with growth of 44.8%, 9.6%, and 7.0%, respectively. Among other categories, optoelectronics had the lowest growth rate, about 1.7%; Analog chips were affected by inventory depletion and sluggish demand, with a growth rate of about 3.7%. Overall, memory products may become the key to the recovery of the global semiconductor market in 2024, and sales are expected to return to 2022 levels.

Macro data of the semiconductor industry: According to the latest data from SIA, the global semiconductor market sales in September 2024 will be US$55.32 billion, a year-on-year increase of 23.2%, a new high; Monthly sales increased by 4.1% month-on-month, rebounding for the sixth consecutive month. Among them, the quarterly sales of global semiconductors in 2024Q3 increased by 23.24% year-on-year, the highest quarterly growth rate since 2016. In terms of regional markets, the Americas market had the strongest growth, with a year-on-year increase of 46.3%; Chinese mainland increased by 22.9% year-on-year, and China and the United States continued to lead the recovery of the global semiconductor market. It is worth noting that monthly sales in Europe fell by 8.2% year-on-year, and the impact of weak automotive and industrial demand continued. Please be sure to read the disclosure and disclaimer following the text

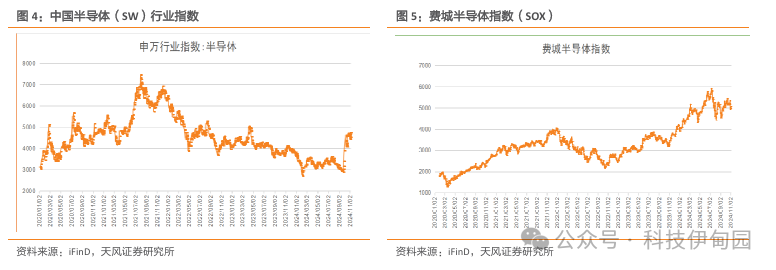

Semiconductor index trend: In October 2024, the China Semiconductor (SW) Industry Index fell by 2.41%, and the Philadelphia Semiconductor Index (SOX) fell by 1.56%.

In October 2024, in addition to branded consumer electronics, all electronic sub-sectors of the Shenwan Index rose to varying degrees. The top three gainers were optical components (36.99%), brand discrete devices (31.59%), and other electronics III (22.69%).

From January to October 2024, in addition to branded consumer electronics, all electronic sub-sectors of the Shenwan Index have risen to varying degrees. The top three gainers were printed circuit boards (37.22%), optical components (35.10%), and semiconductor equipment (34.41%).

3. Chip delivery and inventory in October: The delivery time of major chip categories has stabilized in the short term

Overall chip delivery trend: In October, the delivery time of major chips tended to be stable, and most of the spot delivery times were at a low level, but the delivery time of some categories was extended due to demand.

Delivery time of key chip suppliers: In October, the delivery time of chips was stable, and the price fluctuated slightly. Among them, the delivery time of analog chips is stable, and the price inversion continues; RF and wireless product prices rebounded; The delivery time and price fluctuations of discrete devices such as Infineon and ST fluctuate significantly; The delivery time of mainstream MCUs is stable, and the price is low; The prices of storage and mid-to-high-end passive components have rebounded, and the delivery time of some mid-to-high-end MLCCs has been extended.

Orders and inventories of leading enterprises: In October, consumer orders continued to recover, and inventories were normal; sluggish automotive and industrial orders and high inventories; Declining communication orders; Strong demand for energy storage and AI orders, high PV inventories.

4. The prosperity of all links in the industrial chain in October:

4.1. Design: The benefits of inventory depletion are emerging, and the recovery of demand is expected to drive the fundamentals to continue to improve

4.1.1. Storage: There is a shortage of low-price resources in the channel, but the storage market is still in a period of shock grinding, and PC terminals are worried that Q4 is facing a "peak season".

According to the weekly (as of 2024.11.12) review of the storage market on the official account of the flash memory market, since the second half of the year, the general performance pressure of storage brand manufacturers has gradually become prominent, except for the Q3 net profit of many domestic storage manufacturers has fallen significantly month-on-month, and the storage manufacturers in Taiwan have not been "better" recently, judging from the performance in October, the monthly revenue of many manufacturers is inferior to the level of the same period last year, and the revenue has declined year-on-year for two consecutive months, and the market is pessimistic. Pan Jiancheng, CEO of Phison Electronics, predicts that NAND OEMs are likely to reduce production in December this year, pushing the second half of 2025 back to a tight supply situation. However, at present, some of the original factories have not yet made a clear "card", and both supply and demand sides are patiently waiting for market changes.

In terms of upstream resources, recently, the prices of some Flash Wafer and DDR particles have been slightly reduced. Among them, the price of 1Tb QLC/1Tb TLC NAND Flash Wafer has been reduced to $5.00/$5.90 respectively, and the other prices remain unchanged, DDR4 16Gb 3200/16Gb eTT/8Gb eTT has been reduced to $2.58/2.25/1.13 respectively, and DDR4 8Gb 3200/4Gb eTT price remains unchanged.

In terms of the channel market, there has been no obvious change in the channel market demand recently, most channel customers are mainly "on-demand delivery", and most of them are small orders, and individual channel manufacturers frequently bargain for accelerated realization, but the impact on the overall market is limited, and the price of channel SSD and memory modules is temporarily unchanged this week; In addition, as some of the low-cost resources thrown out by the supply side of the channel spot market have been almost fully absorbed by channel manufacturers, there has been a shortage of resources in the near future, and the price has gradually stopped falling and turned upward. In terms of the industry market, the price of supply-side resources has gradually stabilized, and some industry storage manufacturers have a small amount of pick-up; On the demand side, the overall situation is relatively stable, and the price of SSD/memory modules in the industry is basically unchanged this week. In addition, PC terminal customers in Taiwan have recently announced their latest results, and the revenue in October fell by 2-3% month-on-month.

In the embedded market, with the continuous increase of some supply-side resources, the number of storage master control manufacturers with complete turn-key solutions has also increased, and the price of large-capacity embedded products continued to fall this week with the support of the resource cost advantage. At the mobile terminal level, due to the current high inventory of Tier1 customers, they are generally still on the sidelines, and the willingness to negotiate prices is not strong.

NVIDIA H200 Release: NVIDIA Announces New H200 GPU and Updated GH200 Product Line. Compared with the H100, the H200 is equipped with HBM3e for the first time, and the comprehensive performance of running large models is improved by 60%-90%. The new generation of GH200 still uses CPU+GPU architecture, which will also provide power for the next generation of AI supercomputers. HBM3E is the most advanced High Bandwidth Memory (HBM) product on the market, HBM stands for High Bandwidth Memory, which is a high-performance DRAM based on 3D stacking process, which reduces the latency and power consumption caused by memory and storage solutions by increasing bandwidth and expanding memory capacity, allowing larger models and more parameters to stay closer to the core computing. HBM's high bandwidth is equivalent to widening the channel, so that data can flow quickly. Therefore, in the face of hundreds of billions or trillions of parameters in large AI models, the GPU responsible for computing in the server must almost always be equipped with HBM. Jensen Huang, founder of NVIDIA, has also said that the biggest weakness of computing performance expansion is memory bandwidth, and HBM's application breaks the bottleneck of memory bandwidth and power consumption. When processing Meta's large language model Llama2 (70 billion parameters), the inference speed of H200 is 2 times faster than that of H100, and the application processing of high-performance computing is improved by more than 20%, and HBM3e is used to complete the upgrade of 1.4 times the memory bandwidth and 1.8 times the memory capacity.

HBM's process development: The latest HBM3E, the fifth-generation HBM, is currently on the market and is being installed in NVIDIA's products. As AI-related demand increases, mass production of the sixth-generation high-bandwidth memory HBM4 will begin as early as 2026. According to Korean media reports, SK hynix has started recruiting logic semiconductor designers such as CPUs and GPUs. SK hynix wanted the HBM4 stack to be placed directly on the GPU, thus integrating memory and logic semiconductors on the same chip. This will not only change the way logic and storage devices are typically interconnected, but also how they are manufactured. If SK hynix succeeds, it could change the way some semiconductor foundries operate to a great extent.

HBM iteration process: The market share of HBM2, HBM2e, and 3e will change significantly in 2024. In the first half of 2023, the mainstream is still HBM2e, but because of the advent of H100, HBM3 will become the mainstream of the market in the second half of the year, and it will soon be HBM3e in 2024, because it stacks a higher number of layers, so the average unit price must be more than 20%-30% higher than now, so its contribution to the output value will be more obvious.

Overall forecast of the storage market in 2024: According to CFM flash memory market data, the storage market size is expected to increase by at least 42% in 2024 compared with last year. In terms of total production capacity, NAND Flash will increase by 20% compared to last year and will exceed 800 billion gigabytes equivalent, and DRAM is expected to grow by 15% to reach 237 billion gigabit equivalent. In the cyclically fluctuating storage market, looking back on the cycle changes from 2019 to 2023, we have experienced oversupply, epidemic, shortage, inventory, and overfall, and finally ended with the original factory taking the initiative to reduce production, and as of the fourth quarter of last year, the original factory's profit has improved considerably, and individual companies have even begun to recover profitability. After another sharp rally in the first quarter of this year, the CFM flash memory market expects the profit margins of most companies to be fully and effectively reversed, and prices are expected to maintain a steady upward trend in the next three quarters of this year.

2024 storage downstream demand forecast: In NAND and DRAM applications, mobile phones, PCs, and servers are still the main production capacity outlets, consuming more than 80% of NAND and DRAM production capacity. The three major application markets have already broken out of the decline, and the CFM flash memory market is expected to show modest growth this year. Among them, mobile phones are expected to achieve 4% growth this year; PC will grow by 8%; Servers will see a 4% increase. With the reduction of storage prices in the first two years, the capacity of a single machine has increased significantly, and storage products have ushered in a price sweet spot. Among them, UFS has further increased its market share in mobile phones, and high-end models have basically entered the era of 512GB and TB, and the average capacity of mobile phones is expected to exceed 200GB this year, and the memory is also rapidly evolving towards the higher performance LPDDR5, and the CFM flash memory market is expected to have an average DRAM capacity of more than 7GB this year. AI mobile phones will become the next hot spot for mobile phones, which will strongly promote the upgrade of mobile phone storage again.

Server market: 2024 is the year when DDR5 officially passes 50%, and the second-generation CPUs of DDR5 platforms will be released this year, which will push the 5600 rate into the mainstream in the second half of this year; At the same time, the demand for high-capacity module 128GB/256GB products will increase more in 2023 due to the emergence of AI large models, but the supply is limited due to TSV production capacity. However, in 2024, all OEMs will launch 32Gb single-die, so that 128GB does not need to be TSV, which will clear the main obstacle for 128GB modules to enter the mainstream server market. In addition, CXL has entered the practical stage, officially starting a new era of patent pooling, and HBM3e has entered mass production, so server memory is expected to usher in a big upgrade this year. In terms of Sever SSDs, in order to meet the application needs of higher capacity and better performance, the penetration rate of server PCIe 5.0 SSDs in 2024 will double compared with 2023, and in terms of capacity, we can see more applications of PCIe SSDs of 8TB/16TB and above in the server market.

PC market: Although the decline in demand for complete machines in 2023 has led to a decline in demand for consumer SSDs, the application of high-capacity SSDs has increased significantly, and 1TB PCIe 4.0 has basically become the mainstream configuration in the PC market. In terms of PC DRAM, the CFM flash memory market is expected to see rapid development of LPDDR, especially LPDDR5/X, due to the development of thinner and lighter products, longer battery life, and the application of new forms of LPCAMM products in PCs. With the introduction of new processor platforms, DDR5 will also increase its use on PCs in 2024. At the same time, after Windows 10 is out of service, the update of Windows will also give a certain boost to PC sales in 2024. AI PC is expected to be fully promoted in 2024, and unlike traditional PCs, the most important thing for AI PCs is to embed AI chips to form a heterogeneous solution of "CPU+GPU+NPU". It can support localized AI models, so faster data transfer speeds, larger storage capacity, and bandwidth are required.

Mobile Market: In the mobile space, smartphone demand is showing signs of recovery, with the CFM flash memory market expecting a modest increase in smartphone shipments in 2024. Micron expects smartphone OEMs to begin mass production of AI-enabled smartphones in 2024, adding an additional 4-8GB of DRAM capacity per unit.

Automotive and industrial markets: With the development of electrification, smart cars have entered the era of large modularization and central integration. ADAS has entered the stage of qualitative change, with the gradual implementation of L3 and above autonomous vehicles, the requirements for storage performance and capacity of automobiles will also increase sharply, and the storage capacity of a single vehicle will soon enter the TB era, and in addition, in terms of performance and reliability, cars will put forward more and more requirements for storage. The CFM flash memory market is expected to exceed $15 billion by 2030.

The full-year outlook is optimistic, with an eye on the DDR3 market. In terms of the current orders and future expectations of the original manufacturers, the current storage market demand is showing a gradual recovery trend, AI and automobiles maintain rapid growth, consumer demand has improved significantly, and the development expectation for the whole year of 2024 remains optimistic. From the perspective of the development of manufacturers, with the significant improvement of the supply and demand relationship in the industry, the increase in capital expenditure of the original storage factory is mainly used for the expansion of advanced products. Among them, SK hynix will slightly increase capital expenditure in 2024 mainly for the expansion of high-value products, plan to double TSV production capacity, expand the supply of 256GB DDR5 and 16-24GB LPDDR5T, and expand the product matrix of mobile modules such as LPCAMM2 and AI server modules such as MCR DIMM. Samsung continues to increase the supply of HBM, 1βnm DDR5, QLC SSDs, and more.

It is worth noting that Samsung and SK hynix are increasing their investment in high-end products such as HBM and DDR5 recently, and plan to gradually withdraw from DDR3 and other markets. As a major supplier of DDR3, capacity adjustment has a great impact on terminal supply and price.

At present, the price of DDR3 and other products is still at the absolute bottom of history, and the core bugs believe that with the reduction of DDR3 supply, the price increase is expected to be paid attention to in the second half of the year.

In the long run, as leading manufacturers such as Samsung, SK hynix and Micron accelerate the expansion of high-end application categories such as HBM, domestic manufacturers have greater potential to replace them in low-end markets such as DDR3. From the perspective of mass production progress, GigaDevice and Beijing Ingenic have achieved large-scale shipments, and the performance of DDR3 products is comparable to that of overseas manufacturers, but there is still a gap in the number of parts.

CES2024-SK hynix highlights the key role of storage in the AI era: SK hynix held a press conference titled "Storage, the Power of AI" during the CES2024 in Las Vegas, where SK hynix President and CEO Guo Luzheng elaborated on SK hynix's vision for the AI era. At the press conference, President Guo said that with the popularity of generative AI, the importance of storage will further increase. He also said that SK hynix is providing products from the world's best technologies to the ICT industry, leading the way in "storage-centric AI everywhere." At the press conference, President Guo mentioned that the ICT industry has undergone great development in the era of PC, mobile, and now cloud-based artificial intelligence. Throughout the process, various types and large amounts of data are being generated and disseminated. Now, we have entered a new era of AGI built on all the data. As a result, the new era will move towards a market where AGI is constantly generating data and learning and evolving repeatedly. In the age of AGI, storage will play a key role in processing data. From a computing system perspective, the role of storage is even more critical. Previously, the system was basically an iteration of the data stream from the CPU to memory and then back to the CPU in a sequential fashion, but this structure is not suitable for processing the massive amounts of data generated by AI (enforcement). Now, AI systems are connecting a large number of AI chips and memories in parallel to accelerate large-scale data processing. This means that the performance of AI systems depends on stronger and faster storage. The direction of storage in the era of artificial intelligence should be to process data as quickly as possible, in the most efficient way, and with greater capacity. This is in line with storage development over the past century, which has increased density, speed, and bandwidth.

Q4 2024 Price Forecast: 1) NAND: Due to the sluggish peak season in the second half of 2024, the contract price of wafer products will take the lead in falling in the third quarter, and the decline is expected to expand to more than 10% in the fourth quarter. In terms of module products, except for Enterprise SSDs, which are expected to rise slightly by 0% to 5% in the fourth quarter due to the support of order momentum; PC SSD and UFS are more conservative in their procurement strategies due to buyers' sales of terminal products falling short of expectations. TrendForce estimates that the overall contract price of NAND Flash products will decline by 3% to 8% quarter-on-quarter in the fourth quarter. 2) DRAM: Before the third quarter of 2024, the terminal demand for consumer products is still weak, with AI servers supporting the main demand for memory, and HBM squeezing out the existing DRAM product capacity, and suppliers maintain a certain insistence on contract price increases. TrendForce expects the average price increase of memory to shrink significantly in the fourth quarter, with the growth rate of conventional DRAM (Conventional DRAM) ranging from 0% to 5%, but due to the gradual increase in the proportion of HBM, the overall average price of DRAM is estimated to increase by 8% to 13%, which is significantly more consistent with the increase in the previous quarter.

4.2. Foundry: AI-related advanced processes are growing rapidly, and customer demand for mature process capacity is sluggish

In October, AI-related advanced processes grew rapidly, and customer demand for mature process production capacity was sluggish.

4.3. Closed test: Market orders have rebounded significantly, but price competition in some low-end categories has intensified

In October, market orders rebounded significantly, but price competition in some low-end categories intensified.

The demand for AI has increased in an all-round way, driving the demand for advanced packaging, and TSMC has launched a large CoWoS expansion plan. Since the first quarter of this year, the growing demand for AI servers, coupled with Nvidia's strong earnings report, has caused TSMC's CoWoS package to become a hot topic. It is reported that companies such as Nvidia, Broadcom, Google, Amazon, NEC, AMD, Xilinx, Habana, and others have widely adopted CoWoS technology. Liu Deyin, chairman of TSMC, said at this year's shareholders' meeting that due to the recent increase in demand for AI, many orders have come to TSMC, and they all need advanced packaging, which is much greater than the current production capacity, forcing the company to increase advanced packaging production capacity sharply.

Chiplet/advanced packaging technology is expected to drive the value of the packaging and testing industry, and the future market space for advanced packaging is broad. According to Yole analysis, Advanced Packaging (AP) revenue is expected to grow from $44.3 billion in 2022 to $78.6 billion in 2028, growing at a compound annual growth rate of 10%. In the field of packaging, 2.5D and 3D chiplet medium-to-high-speed interconnect packaging connections and TSVs will increase the value of packaging, and we predict that the value of packaging will be more than double compared with traditional packaging, bringing higher industrial flexibility.

The capacity utilization rate of some packaging and testing plants has returned to a high level, and the price of metal has risen or driven the price of packaging and testing. In the first quarter, driven by Huawei's mobile phone supply chain for domestic chips, as well as the growth of demand for AI, the capacity utilization rate of some packaging and testing factories (such as Huatian/Yongsi, etc.) returned to a high level, and the off-season was not light, exceeding market expectations. Recently, the price of metal has risen, the cost of packaging and testing is expected to increase, and the industrial chain has entered the traditional peak season in the second half of the year, we expect that the price of packaging and testing will have the momentum to increase, and it is recommended to pay attention to the investment opportunities of companies related to the industrial chain.

4.4. Equipment materials and parts: In October, the number of winning bids for equipment is 10 and the number of bids is 34

In October, equipment orders were stable, material demand fluctuated, foundry production capacity rebounded, original factory demand was differentiated, and terminals continued to rise.

4.4.1. Winning bids for equipment and parts: A total of 10 units of winning equipment can be counted in October, a year-on-year increase of -69.7%.

In October 2024, a total of 10 units of winning bids will be counted, a year-on-year increase of -69.7%. 1 auxiliary equipment, 2 testing equipment, 1 etching equipment, 2 other equipment, 4 heat treatment equipment.

In October 2024, NAURA can count 5 winning equipment, +66.7% year-on-year and +0% month-on-month, including 1 etching equipment, 2 other equipment, and 2 heat treatment equipment.

In October 2024, a total of 9 domestic semiconductor parts can be counted as winning bids, a year-on-year increase of -76%. There are mainly 8 items in the electrical category, which won the bid for NAURA and the Institute of Microelectronics of the Chinese Academy of Sciences, and 1 item in the mechatronics category, which won the bid for Hanbell Precision Machinery.

From 2011 to 2024.10, a total of 822 foreign semiconductor parts can be counted as winning bids. There are 50 electrical categories, 339 optical categories, 5 mechatronics categories, 41 mechanical categories, and 388 gas-liquid/vacuum system categories. In terms of branches, Zeiss can count the largest number of winning bids for parts, with 236 items, 16 items of Advanced Energy, 29 items of Brooks, 2 items of Cymer, 39 items of EBARA, 28 items of Elliott Ebara Singapore, 4 items of Ferrotec, 57 items of Inflicon, 76 items of MKS, 1 item of MKS and Inficon, 1 item of MKS, 1 item of VAT and 131 items of Newport. 164 Pfeiffer items, Pfeiffer and VAT 2 items, and VAT 36 items.

4.4.2. Equipment bidding: In October 2024, a total of 34 units of equipment can be counted for bidding, a year-on-year increase of -46.87%.

In October 2024, a total of 34 units of bidding equipment can be counted, a year-on-year increase of -46.87%. Among them, there is 1 thin film deposition equipment, 4 testing equipment, 2 etching equipment, 25 other equipment and 2 testing equipment.

In September 2024, HHGrace has no statistical bidding equipment.

From 2020 to 2024.9, the company can count a total of 3,592 bidding equipment, including 246 thin film deposition equipment, 395 auxiliary equipment, 56 lithography equipment, 69 post-processing equipment, 305 testing equipment, 2 sputtering equipment, 34 resist processing equipment, 152 etching equipment, 33 ion implantation equipment, 45 polishing equipment, 1523 other equipment, 140 cleaning equipment, 388 heat treatment equipment, and 204 vacuum equipment.

4.5. Distributors: The Euro-US device distribution market continues to be sluggish, the revenue and profit of the main distributors in the Asia-Pacific market continue to recover, and AI, automotive and consumer-related orders grow rapidly

In October, the Euro-US device distribution market continued to be sluggish, the revenue and profit of major distributors in the Asia-Pacific market continued to recover, and AI, automotive and consumer-related orders grew rapidly.

5. Terminal applications: optimistic about the recovery of consumer electronics and pay attention to the development trend of the metaverse

5.1. Consumer electronics: Global demand for consumer products such as smartphones and PCs maintained a weak recovery, AI+-related applications grew rapidly, and XR demand growth continued to be sluggish

Industry institutions are generally optimistic about the market in 2024. Among them, in the field of mobile phones, according to IDC's forecast, global smartphone shipments will decrease by 1.1% year-on-year to 1.19 billion units in 2023, and global smartphone shipments will increase by 4.2% year-on-year to 1.24 billion units in 2024, and in the field of folding phones, according to Counterpoint, global folding screen smartphone shipments are expected to increase by 52% year-on-year to 22.7 million units in 2023, and are expected to enter a period of rapid popularity of folding screen phones in 2024. 55 million units in 2025; In the PC field, according to IDC data, global PC shipments in 23Q3 were 68.2 million units, an increase of 11% quarter-on-quarter, and shipments have increased quarter-on-quarter for two consecutive quarters. According to its forecast, PC sales will grow by 4% in 2024 after a sharp decline of 14% in 2023; In the notebook field, according to TrendForce, global notebook shipments have achieved quarter-on-quarter growth for two consecutive quarters in the third quarter of 2023. According to its forecast, the overall shipment scale of the global notebook market will reach 172 million units in 2024, with an annual growth rate of 3.2%.

In October, mobile phone manufacturers' stocking and orders continued to grow during the peak consumer demand season. It is worth noting that due to the fierce competition in overseas markets, Transsion's revenue and profit have declined significantly.

5.2. New energy vehicles: The sales volume of the automobile market is differentiated, with leading manufacturers such as BYD and Tesla growing strongly, while the sales of traditional car companies continue to decline

In October, the sales volume of the automobile market was differentiated, with leading manufacturers such as BYD and Tesla growing strongly, while the sales of traditional car companies continued to decline.

5.3. Industrial control: data center-related industrial control orders have grown well, and orders for lithium batteries and photovoltaics have declined significantly

In October, data center-related industrial control orders grew well, and orders for lithium batteries and photovoltaics fell significantly.

5.4. Photovoltaics: The price and operating pressure of the photovoltaic industry are relatively high, and the production schedule of leading manufacturers tends to be conservative

In October, the price and operating pressure of the photovoltaic industry were greater, and the production schedule of leading manufacturers tended to be conservative.

5.5. Energy storage: Energy storage orders continue to grow, but there are certain fluctuations in the industry, especially in the highly competitive Chinese market

In October, energy storage orders continued to grow, but there were certain fluctuations in the industry, especially in the fierce competition in the Chinese market.

5.6. Servers: The investment expenditure of cloud computing vendors in data centers has grown rapidly, and the orders and revenues of server-related vendors have grown rapidly

In October, the investment expenditure of cloud computing vendors in data centers grew rapidly, and the orders and revenues of server-related vendors grew rapidly.

5.7. Communications: Mobile operators' investment in traditional communication services has slowed down, and the growth of orders from downstream equipment manufacturers has been sluggish

In October, mobile operators' investment in traditional communication services slowed down, and the order growth of downstream equipment manufacturers was sluggish.

6. Last week's (11/11-11/15) semiconductor market review

Last week (11/11-11/15) semiconductors lagged behind most major indices. Last week, the ChiNext index fell 3.36%, the Shanghai Composite Index fell 3.52%, the Shenzhen Composite Index fell 3.70%, the SME Index fell 3.25%, Wind All A fell 3.94%, and the Shenwan Semiconductor Industry Index fell 4.34%.

All sub-sectors of semiconductors fell, with the IC design sector falling the most, and other sectors falling the least. Among the semiconductor sub-sectors, the packaging and testing sector fell 3.6% last week, the semiconductor materials sector fell 3.5% last week, the discrete device sector fell 4.8% last week, the IC design sector fell 5.6% last week, the semiconductor equipment sector fell 3.7% last week, the semiconductor manufacturing sector fell 4.7% last week, and the other sectors fell 0.6% last week.

The top 10 stocks in the semiconductor sector last week were: Research New Materials, Crystal Integration, Weijie Chuangxin, Brite Chips, Yongsi Electronics, VeriSilicon, Huahai Chengke, Broadcom Integration, Hengxuan Technology, and Runxin Technology.

The top 10 stocks in the semiconductor sector last week were: Fuller, Fuchuang Precision, Maxic, National Technology, Kangxi Communication, Jingfeng Mingyuan, Zhenlei Technology, Kema Technology, Guangli Micro, and Yuanjie Technology (rights protection).

7. Last week's (11/11-11/15) key company announcements

Ole New Material 688530. SH

Guangdong Ole High-tech Materials Co., Ltd. plans to build the Mingyue Lake High-tech Materials Industrial Park Project (Phase I) in Shaoguan City, with a total investment of about 322 million yuan, covering an area of about 208.5 acres, and will build a R&D center, headquarters building, etc., focusing on the development of high-performance sputtering targets and new materials business, and signed an investment agreement with the Management Committee of Shaoguan High-tech Industrial Development Zone.

Shengmei Shanghai 688082.SH

On November 12, 2024, Shengmei Semiconductor Equipment (Shanghai) Co., Ltd. issued the prospectus for the issuance of A-shares to specific targets in 2024, planning to issue A-shares to no more than 35 qualified specific targets, and the total amount of funds raised will not exceed 450,000 yuan, which will be used for R&D and process test platform construction, iterative R&D of high-end semiconductor equipment and replenishment of working capital. The issue price will not be less than 80% of the average trading price of the shares in the 20 trading days prior to the pricing reference date, and the number of shares issued will not exceed 10% of the company's total share capital, i.e. no more than 43,615,356 shares. The issuance will not change the controlling shareholder and actual controller of the company, nor will it affect the listing conditions of the company's equity distribution.

Yan Dongwei 688172. SH

Beijing Yandong Microelectronics Co., Ltd. plans to increase its capital by 4 billion yuan to its wholly-owned subsidiary, Yandong Technology, and Yandong Technology will increase its capital by 4.99 billion yuan to Nortel Integration, and Yandong Technology will hold 24.95% of the equity of Nortel Integration after the completion of the transaction. The counterparties involved in this transaction include related parties such as Beijing Electronic Control, which constitutes a connected transaction. The capital increase funds will be used for Nortel Integration's investment in the construction of a 12-inch integrated circuit production line project, with a total investment of 33 billion yuan, and mass production is expected to be achieved by the end of 2026. The transaction has been deliberated and approved by the board of directors and the board of supervisors of the company, and is subject to the approval of the Beijing State-owned Assets Supervision and Administration Commission, and submitted to the general meeting of shareholders of the company for deliberation.

8. Last week's (11/11-11/15) semiconductor key news

Suteng Juchuang LiDAR SoC chip M-Core has obtained the world's first automotive-grade certification. RoboSense's fully self-developed SoC chip M-Core won the AEC-Q100 automotive-grade reliability certification in October, becoming the world's first LiDAR SoC chip to obtain this certification. The M-Core chip will be used in the ultra-thin medium and long-range LiDAR MX product, which is expected to achieve mass production and delivery early next year. Developed by the Automotive Electronics Council, AEC-Q100 qualification is the most authoritative standard in the global automotive industry, covering the full range of requirements from design to production to ensure chip stability and long-term reliability in the automotive environment.

Pickering Corporation announces the release of the 43-920-002, a new generation of high-performance PXIe embedded controllers. In November 2024, Pickering, Inc., a leading global provider of electronic test and verification solutions, announced the launch of the 43-920-002, a next-generation single-slot PXIe embedded controller, the most compact and powerful 3U single-slot controller on the PXI Express platform. As an upgrade to the 43-920-001, the next-generation controller delivers a two-fold increase in performance, integrating 11th Gen Intel Xeon processors, 64GB of DDR4 memory, and 2TB m.2 Type B SSDs, supporting up to 28GB/s system throughput, and full support for PCIe Gen4 and 10GBASE-T interconnect technologies. Compliant with the PXI-5 PXIe Hardware Specification 2.0, the controller is a perfect fit for Pickering's 21-slot, fully hybrid PXIe chassis and will make its debut at Electronica 2024, the world's leading trade fair for electronics manufacturing.

Infineon Technologies introduces AURIX™ TC4Dx microcontrollers for software-defined vehicles. Summary: Infineon Technologies AG, a global leader in power systems and IoT semiconductors, today announced the AURIX TC4Dx microcontroller (MCU), the first member of the AURIX™™ TC4x family based on 28nm technology. The MCU combines power and performance improvements with the latest trends in virtualization, AI, functional safety, cybersecurity, and more to support new E/E architectures and the next generation of software-defined vehicles. The AURIX™ TC4Dx MCUs are critical for controlling and monitoring systems in the automotive such as vehicle motion control, ADAS, and chassis, improving processing performance and efficiency, accelerating time-to-market, and reducing total system cost.

9. Risk Warning

Unpredictable risks brought about by geopolitics: With the intensification of geopolitical conflicts, the United States and other countries/regions have successively tightened export control policies for the semiconductor industry, the international export control situation has become stricter, and economic globalization has been greatly challenged, bringing uncertain risks to the stability of the global semiconductor market and chip supply chain. In the future, if the United States or other countries/regions escalate trade frictions with China, restrict imports, exports and investment, raise tariffs or set up other trade barriers, companies related to the semiconductor industry may also face the risk of tight supply of relevant controlled equipment, raw materials, spare parts, software and service support, and limited financing, which will adversely affect the R&D, production, operation and business of companies in the industry.

Demand recovery is less than expected: Affected by global macroeconomic fluctuations, industry prosperity and other factors, the integrated circuit industry has a certain cyclicality, which is closely related to the overall development of the macroeconomy. If the macroeconomic fluctuations are large or the trough is long-term, the market demand of the integrated circuit industry will also be affected. In addition, the fluctuation and sluggishness of downstream market demand will also lead to a decline in the demand for integrated circuit products, or due to the overheating of investment and duplicate construction in the semiconductor industry, the supply of production capacity will exceed the market demand when the boom is low.

Technology iteration is less than expected: The integrated circuit industry is a technology-intensive industry, and integrated circuits involve the comprehensive application of dozens of scientific and technological and engineering disciplines, and have the characteristics of fast process technology iteration, large capital investment, and long research and development cycle. Over the years, companies in the integrated circuit industry have adhered to the path of independent research and development and further consolidated their core intellectual property rights. If the company's investment in future technology research and development in the industry is insufficient and cannot support the need for technological upgrading, it may lead to the company's technology being caught up or replaced, which will have an adverse impact on the company's sustainable competitiveness.

Risk of industrial policy change: As the foundation and core of the information industry, the integrated circuit industry is a strategic industry for national economic and social development. The state has successively issued a series of policies, including the Notice of the State Council on Printing and Distributing Several Policies to Further Encourage the Development of the Software Industry and the Integrated Circuit Industry (Guo Fa [2011] No. 4) and the Notice of the State Council on Printing and Distributing Several Policies for Promoting the High-quality Development of the Integrated Circuit Industry and the Software Industry in the New Era (Guo Fa [2020] No. 8), which provide more support for integrated circuit enterprises in terms of finance and taxation, investment and financing, research and development, import and export, talents, intellectual property rights, market application, and international cooperation. In the future, if there are major adverse changes in the relevant national industrial policies, it will have a certain adverse impact on the development of the industry.

Analyst statement

The

undersigned analyst hereby declares that we have the securities investment consulting qualification or equivalent professional competence granted by the Securities Association of China, and all views expressed in this report accurately reflect our personal views on the underlying securities and the issuer. No part of the remuneration we receive has been, is not associated with, and will not be directly or indirectly related to, the specific investment advice or views in this report.

General Statement

Unless otherwise specified, the copyright of all materials in this report belongs to Tianfeng Securities Co., Ltd. (which has been licensed by the China Securities Regulatory Commission ("Golden Kylin Analysts)) for securities investment consulting business" and its subsidiaries (hereinafter collectively referred to as "Tianfeng Securities"). Without the prior written authorization of TF Securities, this report and the materials and contents contained therein shall not be modified, sent or reproduced in any way. All trademarks, service marks and marks used in this report are trademarks, service marks and marks of TF Securities.

This report is confidential and for the use of our clients only, and TF Securities does not consider the recipient to be a client of TF Securities by virtue of its receipt of this report. The information in this report is derived from publicly available information that we believe to be reliable, but TF Securities does not guarantee the accuracy and completeness of such information. The information, opinions, etc. in this report are for the client's information only and do not constitute an offer or solicitation of an offer or offer to buy or sell the said securities. Such information and opinions do not take into account the specific investment objectives, financial situation and specific needs of the person obtaining this report, and do not constitute a personal recommendation to any person at any time. Clients should make an independent assessment of the information and opinions contained in this report and should seek expert advice on legal, commercial, financial, tax and other aspects as necessary, taking into account their respective investment objectives, financial situation and particular needs. TF Securities and/or its affiliates do not assume any legal responsibility for all consequences arising from the reliance on or use of this report.

The opinions, assessments and forecasts contained in this report are those of opinion and judgment as of the date of this report. Such opinions, assessments and forecasts are subject to change at any time without notice. Past performance should not be used as a predictor or guarantee of future performance. At different times, TF Securities may issue research reports that are inconsistent with the opinions, assessments and forecasts contained in this report. TF Securities' salespeople, traders and other professionals may express market commentary and/or trading views that are inconsistent with the opinions and recommendations of this report, either orally or in writing, based on different assumptions and standards and using different analytical methods. TF Securities is under no obligation to update such opinions and recommendations to all recipients of the report. TF Securities' asset management department, proprietary division and other investment business units may independently make investment decisions that are inconsistent with the opinions or recommendations in this report.

Special Statement

To the extent permitted by law, TF Securities may hold and trade in securities issued by the companies mentioned in this report, and may also provide or seek to provide various financial services such as investment banking, financial advisory, and financial products to these companies. Therefore, investors should take into account that TF Securities and/or its related personnel may have potential conflicts of interest that may affect the objectivity of the views in this report, and investors should not regard this report as the sole reference for investment or other decisions.

Note: The report in this article is excerpted from the research report publicly released by Tianfeng Securities Research Institute, and the specific report content and related risk warnings are detailed in the full report.

Securities research report "Re-emphasizing the investment opportunities of domestic substitution of semiconductors".

Release date: November 18, 2024

Report issued by Tianfeng Securities Co., Ltd

Analyst of this report:

Luo Yiyang (Jin Qilin Analyst) SAC Practicing Certificate No.: S1110521050001

Cheng Ruying (Jin Qilin Analyst) SAC Practicing Certificate No.: S1110521110002

Li Hongyi SAC Practicing Certificate No.: S1110524040006

Pan Jian is the chief analyst of the electronics industry of Tianfeng Securities. Master of Microelectronics and Solid-State Electronics of Fudan University, Bachelor's degree in Microelectronics of Fudan University, second major in international economics and trade, once worked as an analyst at Essence Securities, has a comprehensive and profound insight into the electronics industry, excavates many high-growth enterprises, and in-depth cooperation with the industry to help enterprises develop, and is good at recommending investment opportunities in the large cycle of scientific and technological innovation. In 2019 and 2020, the Best Analyst of New Fortune won the fourth and second place respectively, and in 2021, New Fortune was shortlisted, and in 2015-2016, he was the first team member of New Fortune, and in 2017, he was a member of the second team of New Fortune. From 2015 to 2016, he was the first team member of the crystal ball, and in 2017 and 2019, he won the second and fifth places respectively. In 2015-2016, he was a member of the first team of the Golden Bull Award, and in 2017, 2020 and 2021, he won the second, fourth and second places respectively. In 2018, he won the first place in Wind Gold Analyst and in 2020-2021, he won the second place in Wind Gold Analyst. From 2019 to 2021, Golden Kylin Best Analyst won the third, fourth, and sixth places respectively. In 2020, he ranked third in the best analysts of Shanghai Securities News, fifth in the 21st Century Gold Medal Analyst in 2021, and third in the best analysts in the electronics industry in 2021 by Choice. Wen Yuzhang Analyst. With a professional background in computer and industrial engineering, more than 12 years of experience in the research and development of Apple products (iPod & iPhone) and the introduction of new products, he has a deep knowledge and understanding of the development trend of the electronics, computer and Internet industry chains. Yiyang Luo is an analyst. He holds a bachelor's degree in physics from Nanjing University and a master's degree in integrated circuit design from the Hong Kong University of Science and Technology. 3 years of research experience in the electronics industry, covering semiconductor manufacturing, semiconductor equipment materials and some semiconductor design. Cheng Ruying is an analyst. Master of Computer Science from Peking University, covering semiconductor IC design, MCU/SOC/IGBT/analog chip industry & company coverage report. Xu Junfeng (Jin Qilin Analyst) Analyst. Master of Business Administration from the University of Birmingham, covering security, LED, automotive connectors and smart cockpits. Yu Wenjing (Jin Qilin Analyst) Analyst. Master of Science in Finance, Chinese University of Hong Kong, covering consumer electronics and PCB industry chain. Hongyi Li is an analyst. Bachelor's degree and master's degree in accounting and finance from Emory University, covering semiconductor packaging and testing and some materials and equipment, has written a number of industry in-depth reports including automotive chips, third-generation semiconductors, virtual displays, etc. Yu Wu is an assistant researcher. Bachelor of Financial Computing from the University of Liverpool and Master of Business from the University of Queensland, covering some passive components, panels and semiconductor materials. Feng Haofan is an assistant researcher. Bachelor of Information Systems and Master of Finance from the University of New South Wales, covering some automotive electronics fields. Stellar Bao is an assistant researcher. Bachelor's degree in Materials Physics and Master of Materials Physics and Chemistry from Nanjing University, covering the field of consumer electronics.

Jingyi Gao is an assistant researcher. Master of Accounting, Central University of Finance and Economics, covering the field of semiconductors.

(Redirected from: Tech Eden).

Ticker Name

Percentage Change

Inclusion Date