The market value of military central state-owned enterprises accounts for 73.7%, which is the ballast stone of the industry. With the gradual participation of private enterprises in military production, the demand for equipment has increased, more and more private enterprises have been successfully listed, and the market value of military central enterprises has decreased year by year. The proportion gradually decreased from 96% in 2007 to a low of 65.9% in 2022. In recent years, the assessment of the State-owned Assets Supervision and Administration Commission and the reform of state-owned enterprises have had a significant impact on the central state-owned enterprises of the military industry, and the reshaping of the valuation system, coupled with their relatively stable performance expectations and the gradual securitization of high-quality assets, the proportion of the market value of the central state-owned enterprises in the military industry has rebounded. As of November 6, 2024, the market value of central state-owned enterprises accounted for 73.7% of the total market value of the military sector, which is the ballast stone of the industry.

The reform of the military industry and central state-owned enterprises has yielded fruitful results, and the reform will be further deepened in the future. China's national defense industry has undergone three large-scale reforms and reorganizations, forming a military industry system dominated by the ten major military industrial groups. Subsequently, the corporate restructuring of each military industrial group was completed around 2018 and truly became an independent market entity. The new round of state-owned enterprise reform will have both institutional and institutional reform and functional reform, and pay more attention to serving the national strategic orientation. Most of the leading enterprises in the military industry are state-owned enterprises, which are expected to give full play to the leading role of the industry, effectively improve the resilience and security of industrial and supply chains, and grasp the strategic initiative in the deteriorating global geopolitical background.

The expectation of capital operation still exists, and the valuation of the military listing platform can be expected to be reshaped. Compared with China's defense industry base based on specialization, the United States has built a defense industry base based on capabilities. The number of U.S. equipment prime contractors has also been merged from 62 in 1990 to six highly centralized cross-service and cross-platform system integrators, which has strongly supported the new U.S. military transformation. We believe that during the "15th Five-Year Plan" period, the internal reorganization and cross-group integration of China's military industrial group is one of the effective ways to realize the efficiency construction of the core capability system of the military industry and improve the stability of the industrial chain and supply chain, which is still the trend of the times. In the context of the current China Securities Regulatory Commission's strong support for mergers and acquisitions, the valuation of the military listed platform can be expected to be reshaped, and the listed companies of the aerospace and electrical technology departments are expected to benefit significantly.

Market value management solutions have emerged, and innovative mechanisms have been continuously improved. Strengthening the management of the market value of state-owned listed companies in the military industry is an important part of improving the management of China's state-owned assets. In the future, state-owned listed companies in the military industry can strengthen market value management by increasing holdings in the market and encouraging repurchases. With the deepening of market value management, the core competitiveness of state-owned listed companies in the military industry will continue to increase. At the same time, the continuous deepening of market value management will force the optimization and adjustment of market structure, stimulate the innovation potential of state-owned enterprises, and promote sustainable development.

From the perspective of practical actions, as of November 16, 2024, a total of 53 listed companies in the military sector have issued the plan of "Improving Quality and Efficiency and Valuing Returns", of which 32 are central state-owned enterprises; A total of 7 listed military companies have issued an action plan for "double improvement of quality returns", of which 4 are state-owned enterprises.

From the perspective of dividends, the central state-owned enterprises of the military industry will pay dividends of 12.655 billion yuan in 2023, accounting for 80.5% of the total dividends of the sector; 60 of the 76 central state-owned enterprises pay dividends. At present, the proportion of military central state-owned enterprises with a dividend rate of less than 30% is still relatively large, and the dividend rate may be gradually increased in the future.

Investment suggestion: China is exploring a valuation system with Chinese characteristics, and there is still a lot of room for improvement in military central enterprises. First of all, the reform of state-owned enterprises has entered the deep-water area, the requirements for improving the quality and efficiency of central enterprises are even greater, and the operating quality of military central enterprises has been steadily improved; Secondly, the overall asset securitization rate of military central enterprises is low, and the value revaluation is achieved through high-quality asset injection/spin-off, accelerating the integration of the industrial chain and listing; Thirdly, the market value assessment and management measures of central enterprises have been fully implemented, and the assessment and management measures of "one enterprise and one policy" will provide assistance for the revaluation of the value of central enterprises.

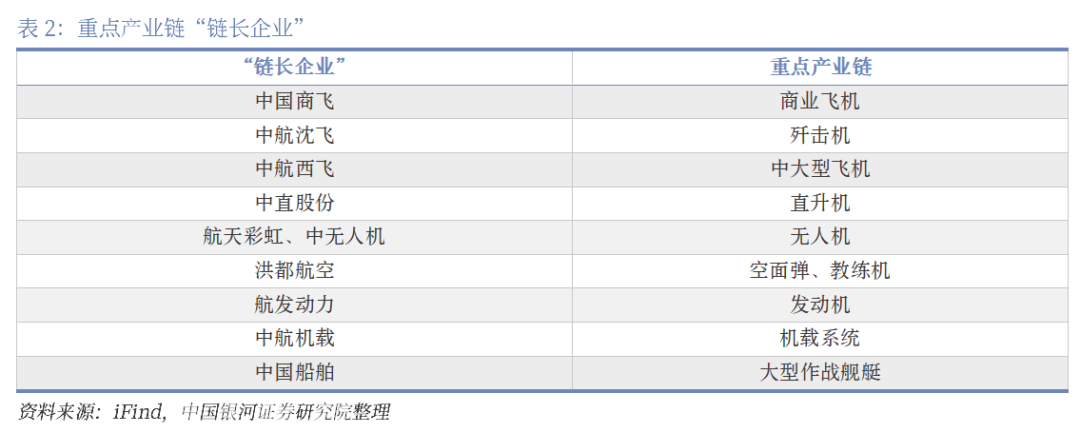

It is recommended to pay attention to: (1) the target of improving the quality and efficiency of the reform of state-owned enterprises: AVIC Xifei, AVIC Optoelectronics, Aerospace Electric and Northern Navigation; (2) "Large groups/institutes, small platforms" listed companies: Guorui Technology, Guobo Electronics, Aviation Materials Co., Ltd., Aviation Development Control, China Haiphong, Aerospace Nanhu and Aerospace Chenguang.

Risk warning: the risk that the reform/restructuring of central state-owned enterprises is not progressing as expected; the risk of fluctuations in military pricing and raw material procurement prices; the risk that downstream orders fall short of expectations; The risk of increased competition in the industry.

1. The

market value of military central state-owned enterprises accounted for 73.7%.

It is the ballast stone of the industry

As the ballast stone and economic pillar of national development, central state-owned enterprises assume the responsibility of promoting economic growth and play a key role in the layout of strategic industries, infrastructure and the construction and development of high-tech fields. The state-owned enterprises of the military industry occupy an important position in the national defense science and technology industry, involving many key fields such as the nuclear industry, aerospace, aviation, ships, and weapons. As the core participants of the military industry, the central and state-owned enterprises of the military industry will continue to promote key tasks such as focusing on their main responsibilities and main businesses, improving their scientific research capabilities, and accelerating the optimization of industrial layout and structural adjustment.

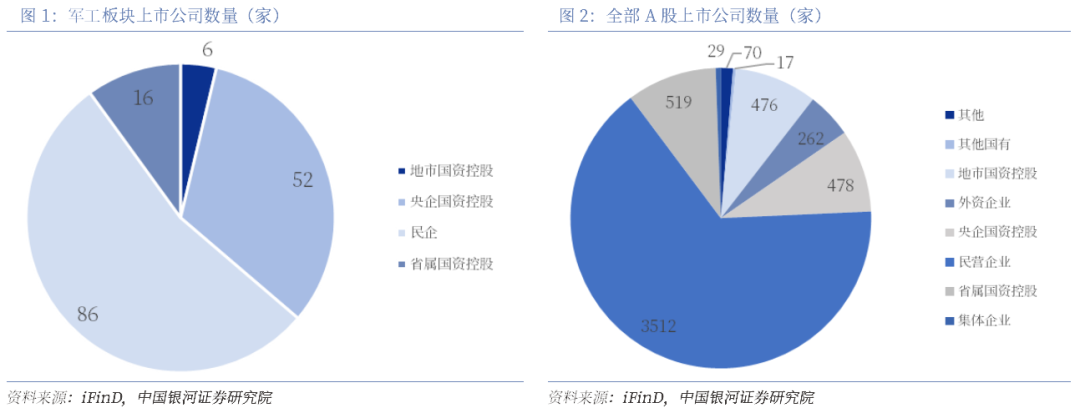

As of November 5, 2024, there were 5,356 A-share listed companies, of which 1,473 were Chinese state-owned enterprises (478 central state-owned enterprises and 995 local state-owned enterprises), accounting for 24.47%. Due to the particularity of the military sector and the restrictions on access qualifications, the proportion of state-owned enterprises is higher. Among the 160 listed companies in the military sector, there are 74 central state-owned enterprises (including 52 central state-owned enterprises and 22 local state-owned enterprises), accounting for 46.25%.

In terms of market capitalization, on November 5, 2024, the total market value of the military sector was 2,653.695 billion yuan, accounting for 2.72% of the total market value of the A-share market; The total market value of its state-owned enterprises is 1,954.699 billion, accounting for 73.57%, accounting for 2.00% of all A-shares. The market value of listed companies in the military sector and the central state-owned enterprises account for far more than their number, and they are the main force in the sector. The top five listed companies in terms of market capitalization are China Shipbuilding, AVIC Shenfei, Hangfa Power, China Heavy Industry (Rights Protection), and AVIC Optoelectronics, of which AVIC Shenfei and AVIC Optoelectronics are subsidiaries of Aviation Industry Corporation of China, Hangfa Power belongs to AECC Group, and CSSC and China Heavy Industry are subsidiaries of China Shipbuilding Group, with deep state-owned backgrounds.

With the gradual improvement of the openness of the military market, the continuous promotion of the military-civilian integration policy, and the further improvement of the activity of the capital market, private enterprises have gradually participated in military production, superimposed on the demand for equipment, more and more private enterprises have been successfully listed, and the proportion of the market value of military central enterprises has decreased year by year. The proportion gradually decreased from 96% in 2007 to a low of 65.9% in 2022. In recent years, the assessment of the State-owned Assets Supervision and Administration Commission and the reform of state-owned enterprises have had a significant impact on the central state-owned enterprises of the military industry, and the reshaping of the valuation system, coupled with their relatively stable performance expectations and the gradual securitization of high-quality assets, the proportion of the market value of the central state-owned enterprises in the military industry has rebounded. As of November 6, 2024, the market value of central state-owned enterprises accounted for 73.7% of the total market value of the military sector, which is the ballast stone of the industry.

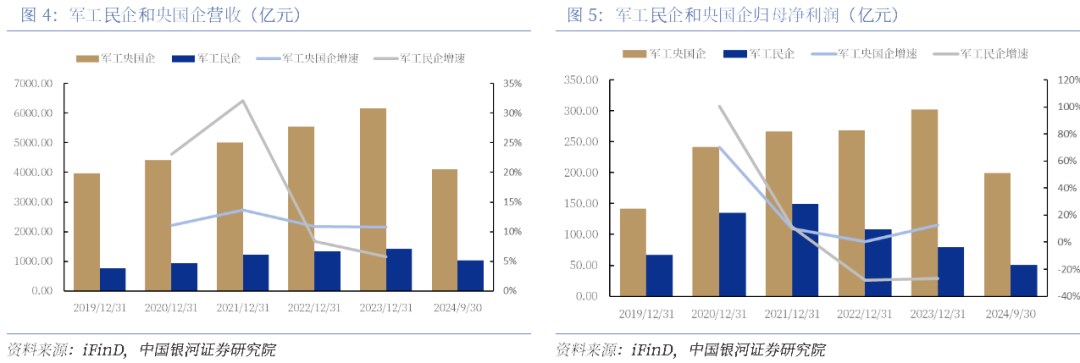

The performance of the military sector is dominated by state-owned enterprises. In 2023, the total revenue of central state-owned enterprises in the military sector will be 615.059 billion yuan, and the revenue of military private enterprises will be 140.951 billion yuan, accounting for 81.36% and 18.64% of the sector respectively. The net profit of central state-owned enterprises was 30.172 billion yuan, and the net profit of private enterprises was 7.907 billion yuan, accounting for 79.24% and 20.76% of all military sectors respectively, and the performance of the sector was driven by central state-owned enterprises. In the first three quarters of 2024, the revenue and net profit attributable to the parent company of the sector were 513.985 billion yuan and 24.970 billion yuan respectively, and the revenue and net profit attributable to the parent company of central state-owned enterprises accounted for 79.80% and 79.87% respectively.

The performance elasticity of central state-owned enterprises is low, but the ability to resist risks is strong. From the perspective of annual growth rate, the revenue CAGR of military central state-owned enterprises from 2019 to 2023 is 11.58%, and the net profit attributable to the parent company is 20.73%. From 2019 to 2023, the CAGR of revenue and net profit of military and private enterprises will be 16.87% and 4.17%, respectively. In the year of higher prosperity, the performance elasticity of private enterprises is greater and the growth rate is faster, while in the downturn of the industry, private enterprises are more obviously affected by the macro environment, and the performance declines faster.

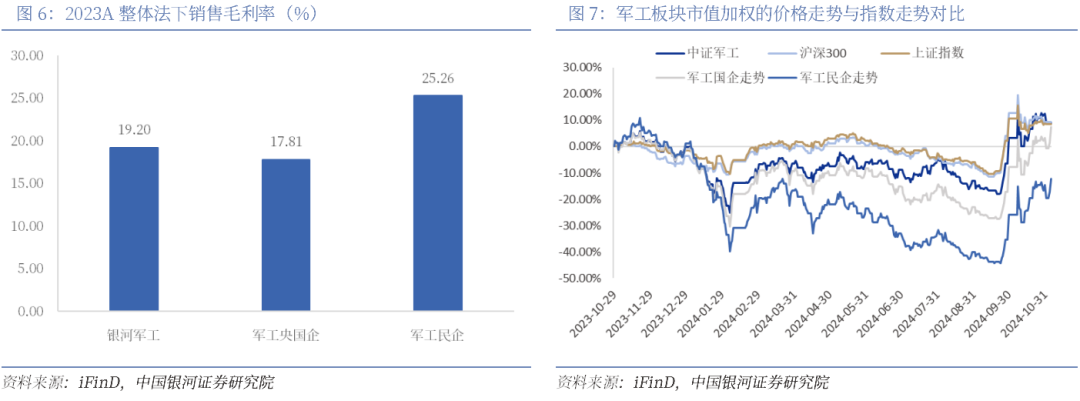

In addition, in 2023, the gross profit margins of the military sector, military state-owned enterprises, and military private enterprises will be 19.20%, 17.81%, and 25.26%, respectively. There is still a certain gap between the cost control ability of central state-owned enterprises and private enterprises.

In terms of stock price performance, the military sector has been declining since the beginning of the year, driven by the policy, market and industry, showing a significant recovery trend in September. In the downward channel, the former fell significantly less than the latter, showing resilience, but in the rebound in January and September 2024, the stock prices of military and private enterprises performed better than those of central state-owned enterprises, and the elasticity characteristics were highlighted.

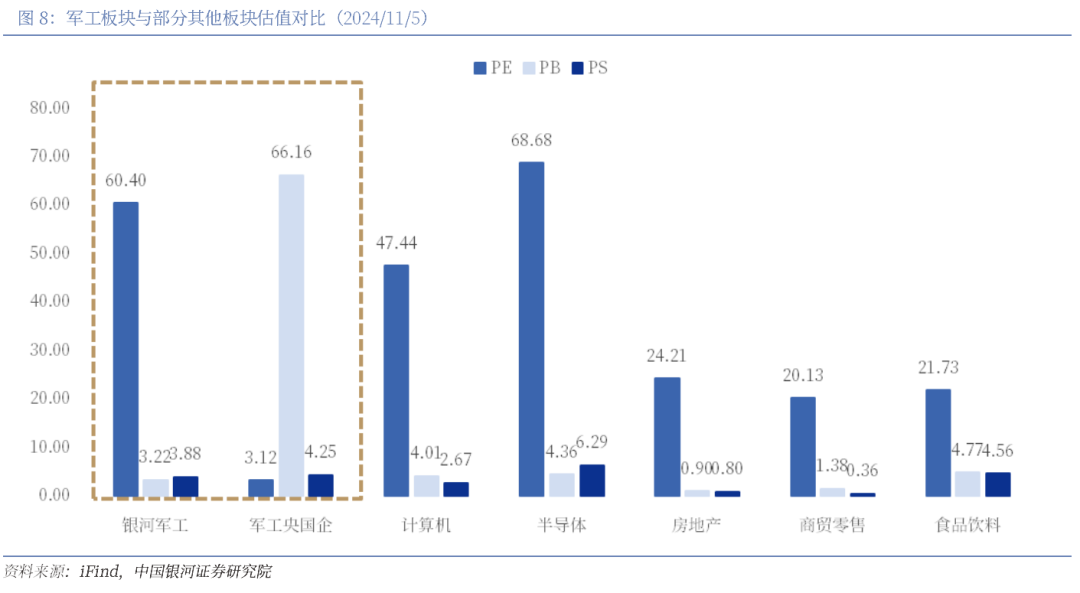

In terms of valuation, high growth brings high valuation of the military sector. As of November 5, 2024, the overall price-to-earnings ratio of A-shares is 14.02x. The P/E ratio of the military sector is 60.40x, and the P/E ratio of the military industry of central state-owned enterprises is 66.16x, and the valuation of military state-owned enterprises leads the overall level of the sector.

Second, the reform of military state-owned enterprises has achieved quite a lot

In the future, the reform will be further deepened

(1) The reform of military central state-owned enterprises has achieved fruitful results

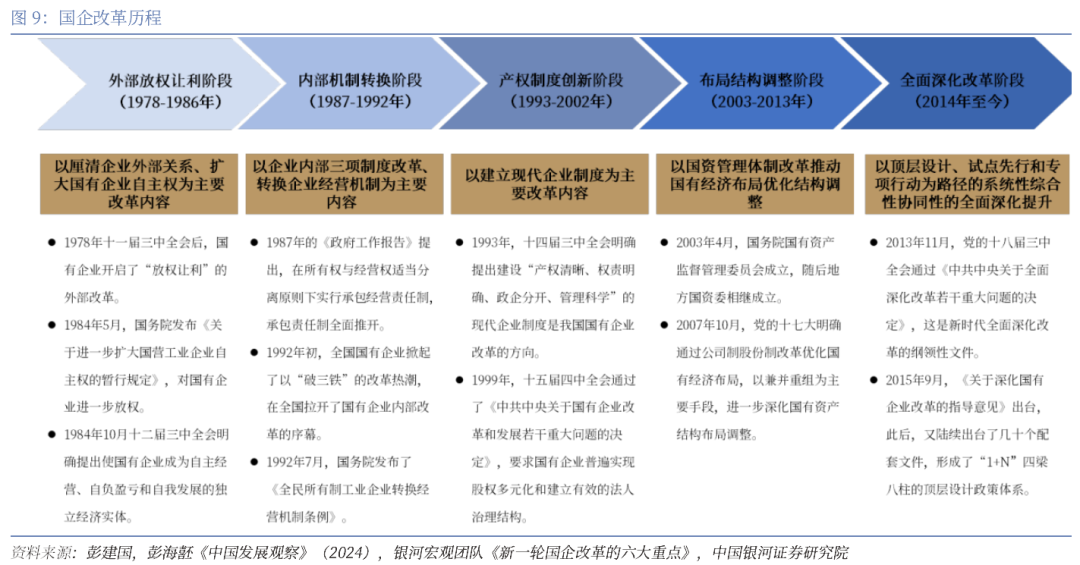

The reform of state-owned enterprises has always been an important link in the reform of China's economic structure. The reform of China's state-owned enterprises has adopted a positive, prudent, and gradual approach, and has successfully embarked on a road of reform with Chinese characteristics and fruitful results. Throughout the development process of China's state-owned enterprise reform over the past 40 years, it can be roughly divided into five stages: external decentralization and profit concession, internal mechanism transformation, property rights system innovation, layout and structural adjustment, and comprehensive deepening of reform.

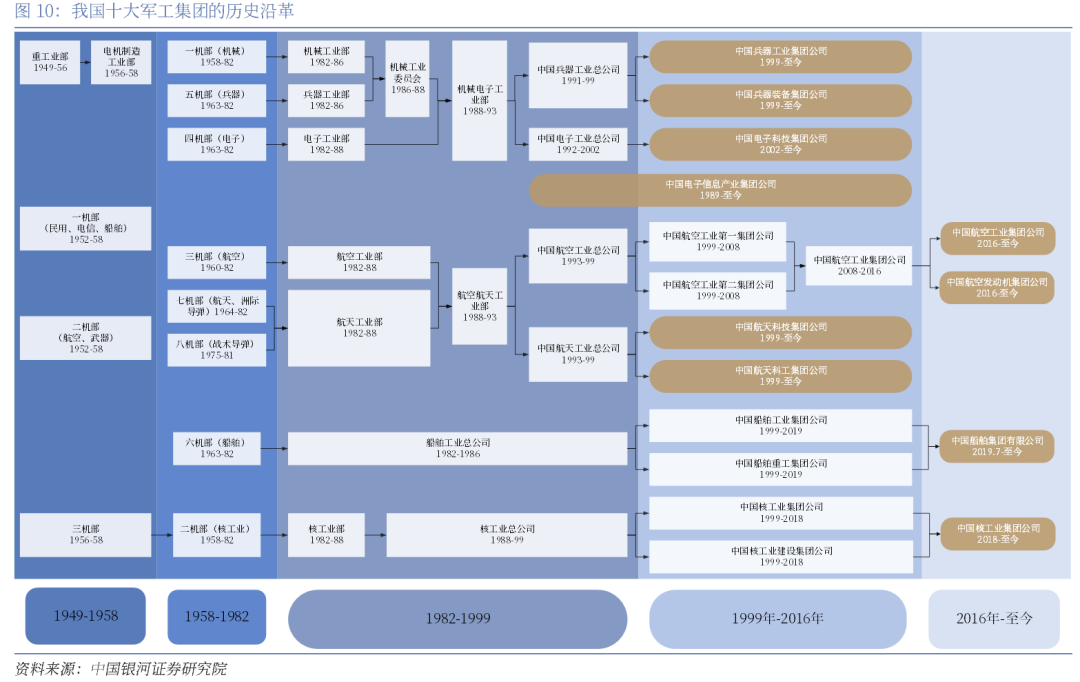

In the above-mentioned wave of reform, China's military industry has also undergone three large-scale reforms and reorganizations, forming the current military industry system dominated by the ten major military industrial groups. From 1986 to 1998, China's military industrial system entered the first period of large-scale reorganization. During this period, the central government reorganized many departments related to the military industry into five major state-owned military industrial corporations, making the originally huge and complex military industrial system more organized, systematic, and efficient. From 1999 to 2008, China's military industrial system underwent the second large-scale reorganization, breaking through the form of asset operation, forming 11 major military industrial groups, covering six major fields of electronics, nuclear industry, weapons, shipbuilding, aerospace and aviation. Since 2016, based on the support of key military industries and the resolution of excess capacity, the third large-scale restructuring began to surface, this time through mergers and splits, the formation of the current ten major military industrial groups, respectively undertake the production and operation functions of major national defense construction projects and national defense research and production tasks, for the national armed forces to provide a variety of weapons and equipment development and production and business activities. Subsequently, the corporate restructuring of each military industrial group was also completed around 2018, realizing the separation of the ownership of investors and the property rights of corporate legal persons, giving enterprises independent legal person property rights, and promoting them to become independent market entities.

The Three-Year Action Plan for the Reform of State-owned Enterprises (2020-2022) calls for promoting industrial restructuring and improving the stability and competitiveness of industrial and supply chains. After the end of the three-year action of state-owned enterprise reform, the reform of state-owned enterprises has entered the deep water area, and it is necessary to further strengthen the top-level design and pay more attention to the systematic, coordinated and coordinated nature of the reform. We believe that promoting mergers and acquisitions may become one of the effective ways to achieve this goal, and the cross-group integration of the military industry and the merger of central enterprises are still the general trend, as evidenced by the overall merger of China Potevio Information Industry Group into China Electronics Technology Group in June 2021.

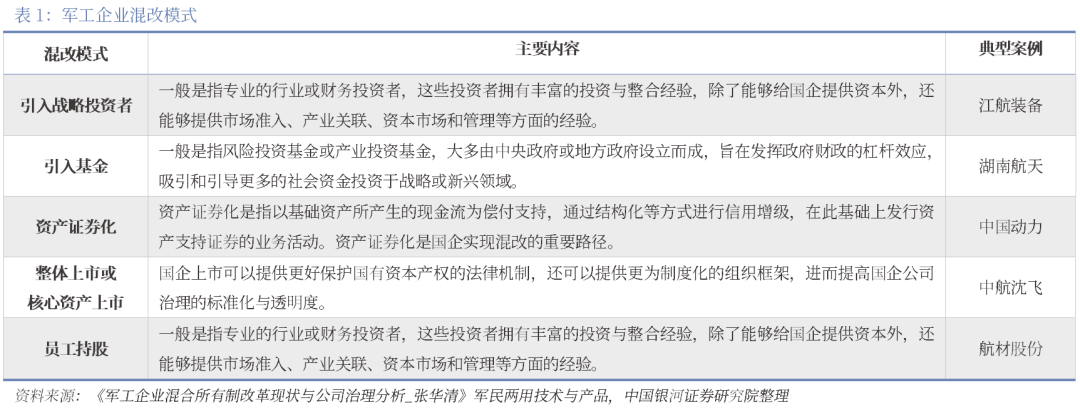

In terms of the path of reform, military enterprises are mainly realized through the introduction of strategic investors, the introduction of funds, asset securitization, overall listing or core asset listing, and employee stock ownership, among which employee stock ownership is more used as a supporting incentive to assist the development of other models. Through a series of reform measures, the shareholding structure of military enterprises is expected to be more diversified, and more external shareholders will participate in the corporate governance structure of enterprises, injecting new vitality into the development of enterprises and bringing new investment opportunities to the capital market.

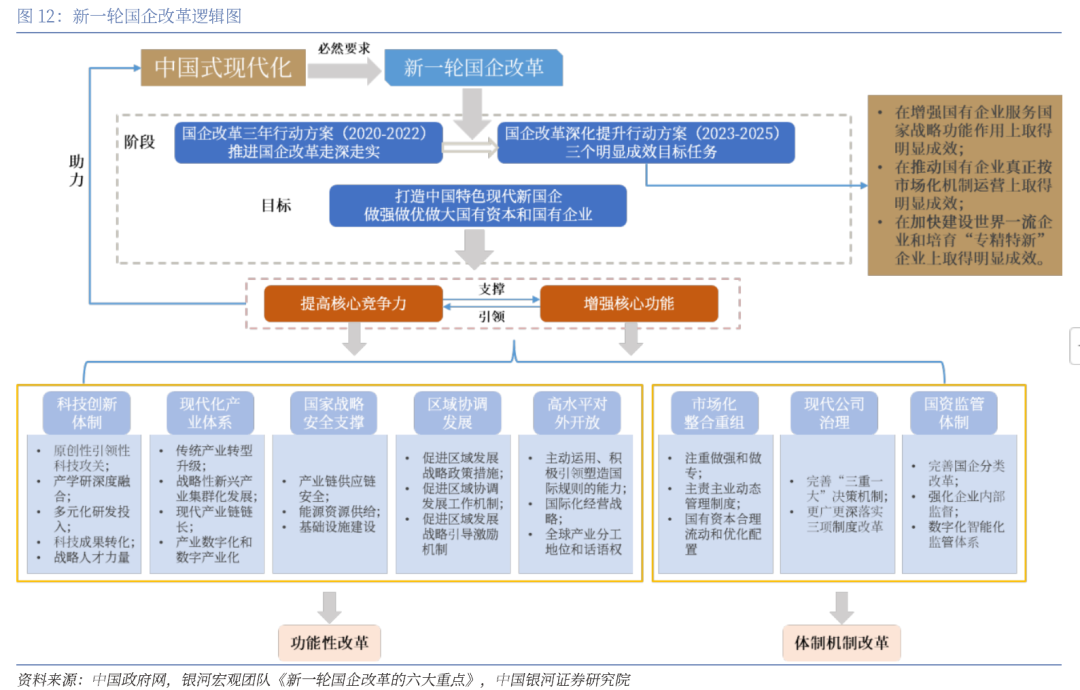

(2) Interpretation of the latest requirements for the reform of state-owned enterprises: The new round of national reform will have both institutional reform and functional reform

The new round of reform of state-owned enterprises will have both institutional and functional reforms, pay more attention to serving the national strategic orientation, improve core competitiveness and core functions, and fulfill important missions in building a modern industrial system, building a new development pattern, promoting high-quality development, and promoting Chinese-style modernization.

The central state-owned enterprises of the military industry have strengthened the guarantee in key areas to support the national strategic security. As an important cornerstone of maintaining national strategic security, state-owned enterprises must take the maintenance of industrial and supply chains and the security of energy and resources as a major mission and responsibility, and promote the further concentration of state-owned capital in areas related to national security and the lifeline of the national economy. High-end equipment in the defense industry, such as aero engines, satellite Internet, and aircraft, are all areas that need to be strengthened in this round of reform, so as to strongly support national strategic security.

Most of the leaders in the military industry are central state-owned enterprises, and most of the industries are led by central state-owned enterprises. In the new round of reform, the military central state-owned enterprises need to give full play to the leading role of the industry to help the construction of China's modern industrial system. As the main force in building a modern industrial system, state-owned enterprises must adhere to the foundation of the real economy, actively lay out new industrial tracks, vigorously cultivate new momentum for development, and promote the formation of a modern industrial system that is independent, controllable, safe and reliable, and highly competitive.

· Leading the transformation and upgrading of traditional industries. We will further implement the industrial base reengineering project and the special work of high-quality development, accelerate technological transformation and equipment upgrading, optimize the layout of major productive forces, promote the high-end and intelligent development of traditional industries, and comprehensively improve the level of upgrading the foundation of China's military industry and modernizing the industrial chain.

· Be the leader of the modern industrial chain. We will give full play to the leading role of central state-owned enterprises, effectively improve the resilience and security of industrial and supply chains, enhance the independent and controllable ability of industrial and supply chains, and grasp the strategic initiative in the context of the deteriorating global geopolitical landscape.

Third, the capital operation is expected to increase

The valuation of the military listing platform can be expected to be reshaped

(1) The wave of mergers and acquisitions of US military enterprises is still continuing

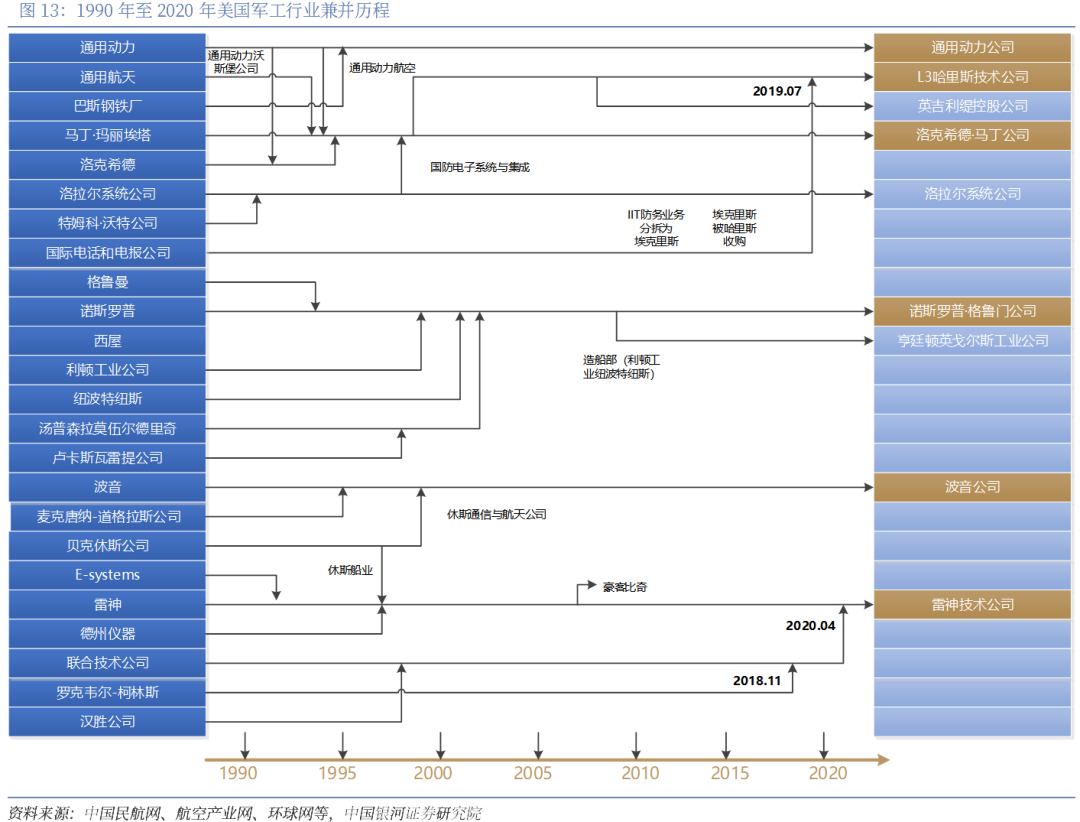

Compared with the United States, the wave of mergers and acquisitions of American military enterprises that began in the 90s is still continuing. The U.S. defense industry has always been at the forefront of the world's defense industry, and reorganization and merger have always been the main theme of its development, and it has the characteristics of a clear main line of industrial integration. The U.S. Department of Defense has clearly pointed out that weapons and equipment suppliers should be transformed into a kind of military service system provider, and become a provider of the required combat effects (capabilities). After the transformation of the world defense industry in the 90s of the 20th century, the number of US main contractors for weapons and equipment has sharply decreased. Many traditional weapons and equipment main contractors are faced with two situations: either withdraw from the military industry or be merged by other military enterprises, while the remaining surviving military enterprises gradually expand their industrial scale. In 1990, there were 62 major arms manufacturing contractors in the United States, and since 2002, only six remain, namely Lockheed Martin, Boeing, Northrop Grumman, Raytheon Technologies, General Dynamics, and L3 Harris Technologies. These six highly centralized cross-service and cross-platform system integrators and combat capability providers have strongly supported the new military transformation of the United States.

To this day, the consolidation of the US military-industrial complex continues. In November 2018, United Technologies announced the completion of its acquisition of Rockwell Collins. In July 2019, L3 Technologies completed its merger with Harris to become the sixth-largest defense contractor in the United States. On April 3, 2020, Raytheon and United Technologies merged to become Raytheon Technologies.

At the beginning of China's "13th Five-Year Plan", we advocated comprehensively promoting the efficiency-oriented construction of the core capability system of the military industry, and forming a dynamically balanced and flexible national defense science and technology industrial base. During the "13th Five-Year Plan" and "14th Five-Year Plan" period, China has carried out a series of professional integration in many fields, and the establishment of the Star Network Group is a major breakthrough, but there is still a certain gap compared with the U.S. capability-based defense industrial base. We believe that during the "15th Five-Year Plan" period, the internal restructuring and cross-group integration of the military industry group is one of the effective ways to realize the efficiency construction of the core competence system of the military industry and improve the stability and competitiveness of the industrial chain and supply chain, which is still the trend of the times.

(2) The pace of military mergers and acquisitions is expected to accelerate, and cross-group reform and merger of central enterprises are the general trend

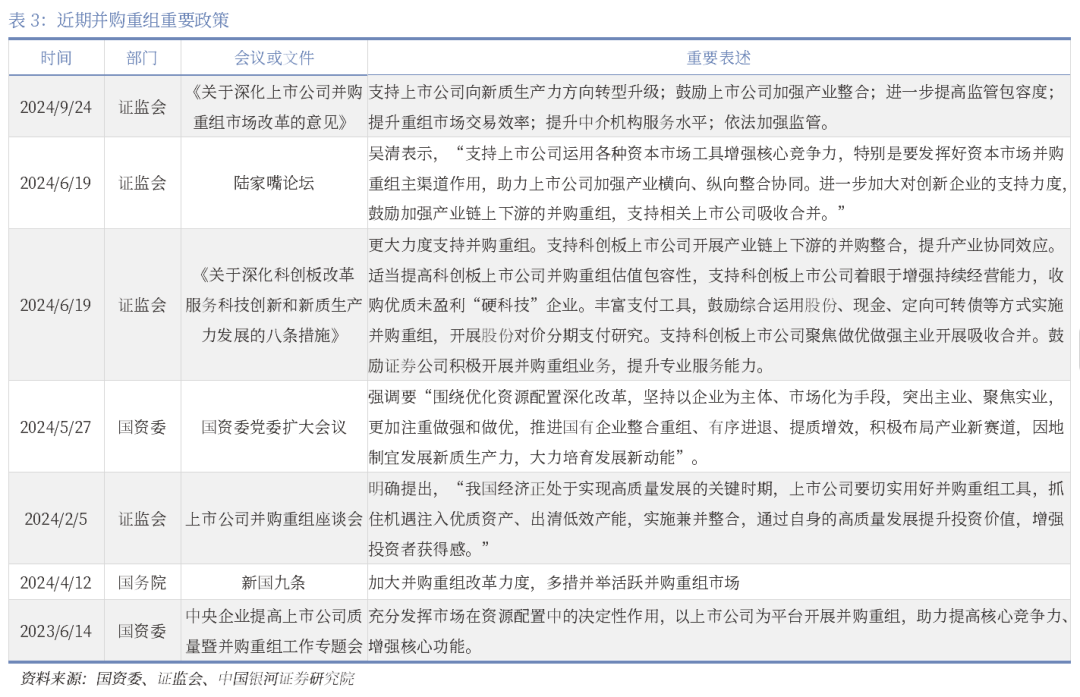

The new round of state-owned enterprise reform and upgrading actions will focus on improving core competitiveness and enhancing core functions, and continuously optimize the layout and structure of the state-owned economy, and restructuring and integration will be an important starting point. In order to continue to play the leading role of state-owned capital in the national economy, judging from the recent policy guidance, strategic restructuring will still be the focus of the new round of comprehensively deepening the reform of state-owned enterprises, and the pace of mergers and acquisitions is expected to accelerate. On September 24, the China Securities Regulatory Commission issued the "Opinions on Deepening the Reform of the M&A and Restructuring Market of Listed Companies" to further stimulate the vitality of the M&A and restructuring market.

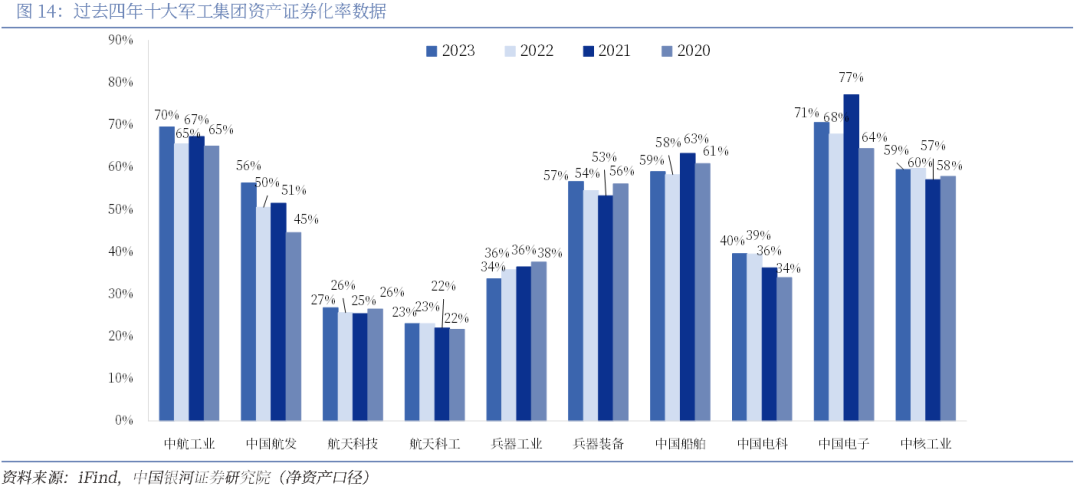

In recent years, the asset securitization operation of the military industrial group has continued to advance, including independent IPOs, backdoor transactions, agreement transfers, and injection into listed companies in different sectors, and the asset securitization rate has continued to increase. According to the data of 2023, in terms of sub-groups, there are 6 companies with asset securitization rates of more than 50%, namely AVIC, AECC, Ordnance Equipment Group, China Shipbuilding Group, China Electronics Information Group and China Nuclear Industry Group, of which AVIC and China Electronics Information Industry Group are the highest, with 70% and 71% respectively. AVIC started early, the capital operation is active, and the shipbuilding group has caught up with the latter, and has also made great progress in recent years. There are two military industrial groups with an asset securitization rate of 30% or below, namely China Aerospace Science and Industry Corporation and China Aerospace Science and Technology Corporation.

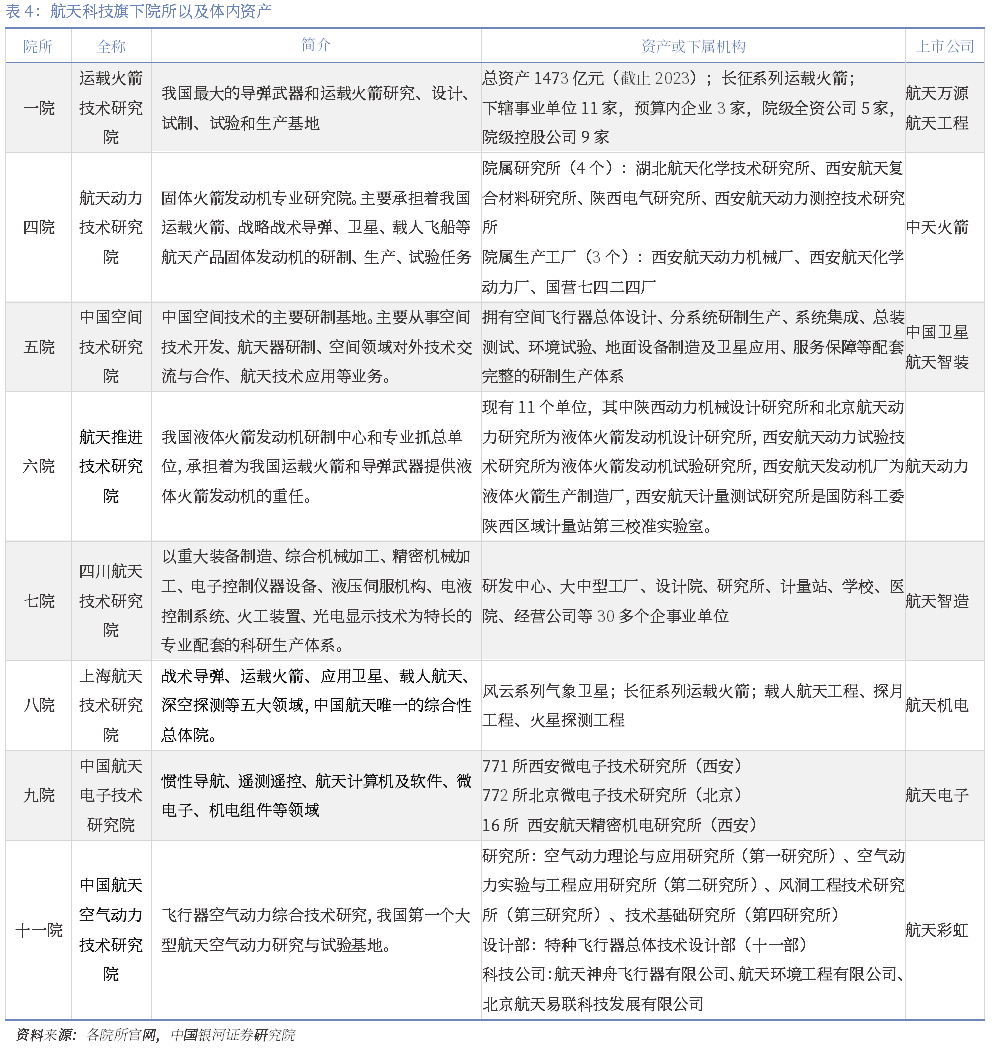

(3) Aerospace science and technology: the asset securitization rate is only 27%, and reform is on the way

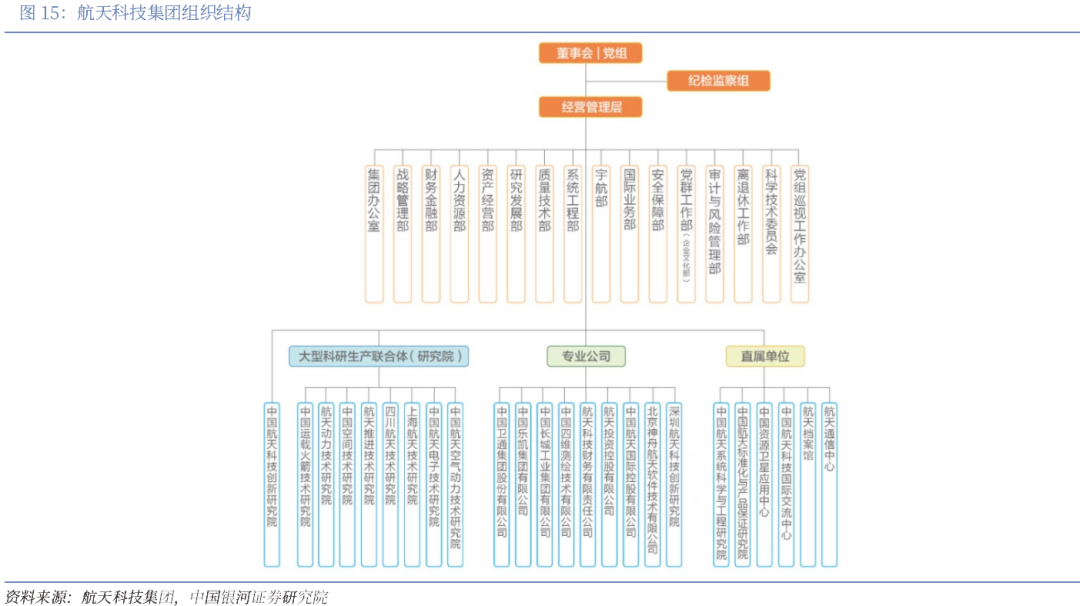

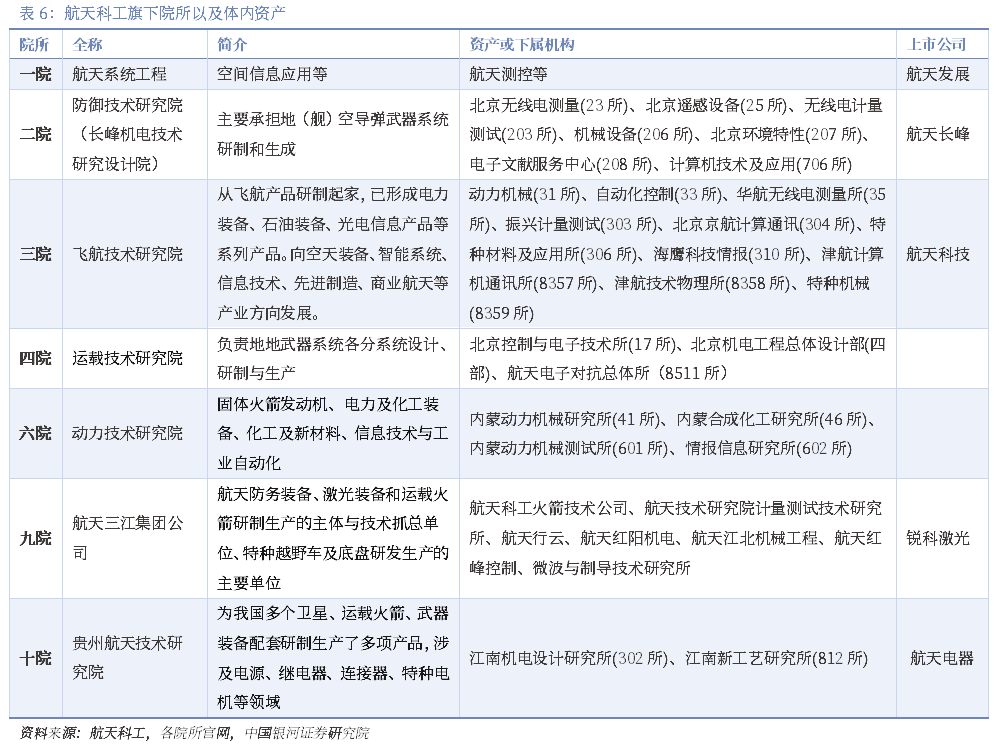

The core industries of the Aerospace Science and Technology Group include four major sectors: aerospace products, missile weapons, aerospace technology applications and aerospace services. Aerospace products include launch vehicles, various satellites, manned spacecraft, cargo spacecraft, deep space probes, space stations; Missile weapons include research, design, production, testing, and launch services for strategic missiles, tactical missiles, unmanned systems, and other weapon products. At the same time, relying on core aerospace technologies and resources, we will vigorously develop aerospace technology application industries such as satellite applications, unmanned systems and high-end equipment manufacturing, and new materials, as well as aerospace service industries such as industrial investment, financial services, and product import and export.

At present, the group has 1 innovation institute, 8 research institutes, 9 professional companies and 6 directly affiliated units, and has 15 domestic and foreign listed companies, forming a regional layout with Beijing, Shanghai, Xi'an and Chengdu as the core and Beijing-Tianjin-Hebei, Yangtze River Delta, Guangdong-Hong Kong-Macao Greater Bay Area, Hainan Free Trade Port as the support.

As of 2023, the group's revenue will be 291.124 billion yuan, the net profit attributable to the parent company will be 6.595 billion yuan, the net assets will be 359.288 billion yuan, and the asset securitization rate of the group's net assets will only be 27%, ranking low in the military industrial group, and there are still a large number of group assets that have not been included in the flag of listed companies (Jin Qilin analysts).

1. Aerospace business

The

launch vehicle is a basic and key part of the space system, which can be used as a medium to send various military and civilian payloads such as small satellites, aerial spacecraft, and space probes into predetermined orbits. The Long March series carrier rockets of the Aerospace Science and Technology Corporation have carried out more than 500 launch missions, and have the ability to launch space vehicles in low-earth orbit, sun-synchronous orbit, geostationary transfer orbit and Earth-Moon transfer orbit, and their reliability, safety and orbit entry accuracy have reached the world's leading level.

The First Academy of Aerospace Science and Technology is the main executive body of the group's launch vehicle business and the largest launch vehicle manufacturer in China, responsible for the overall development of rockets, including the research and design of structural systems, control systems and power plant systems. The Fourth Academy of Astronautics, the Sixth Academy of Astronautics, the Eighth Academy of Astronautics, and the Ninth Academy of Aerospace Sciences are responsible for the development of some subsystems.

· The listed companies under the First Academy include China Aerospace Wanyuan, a Hong Kong-listed company, and Aerospace Engineering, an A-share listed company. China Aerospace Wanyuan is a new energy enterprise with equipment R&D, production, wind farm design, construction and operation capabilities across the entire wind power industry chain. The main business of the aerospace engineering company is to take the aerospace pulverized coal pressurized gasification technology as the core, specializing in the research and development, engineering design, technical services, complete equipment supply and general contracting of coal gasification technology and key equipment.

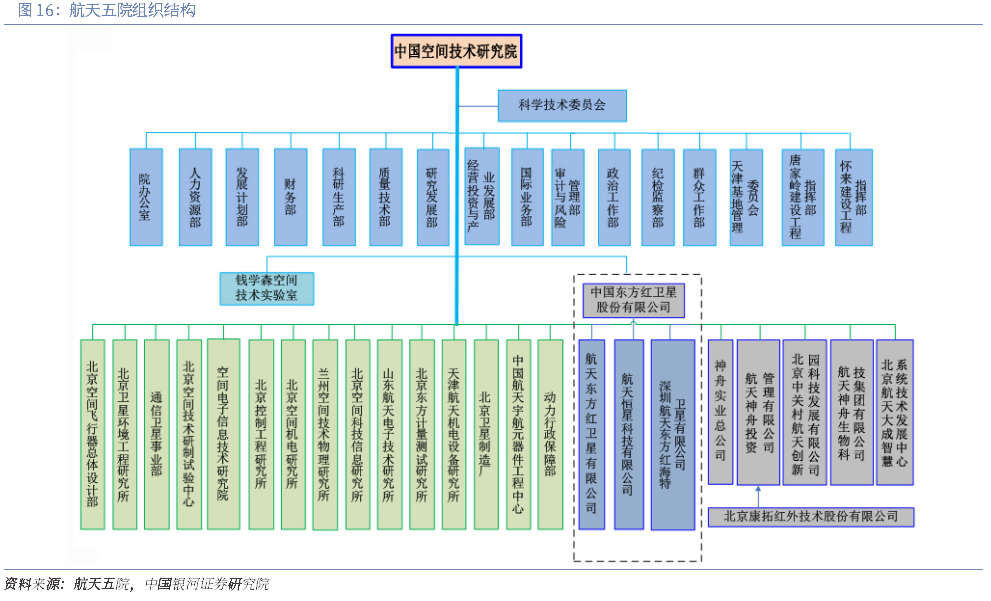

The Fifth Academy of Aerospace Science and Technology Group is mainly responsible for the overall development of satellites and manned spacecraft, while the Fourth Academy of Aerospace Sciences, the Sixth Academy of Aerospace Sciences, the Eighth Academy of Aerospace Sciences, and the Ninth Academy of Aerospace Science and Technology are responsible for the development of subsystems.

· The Fifth Academy of Aerospace: In 2019, two companies under the 502 Institute of the Fifth Academy of Aerospace Science and Technology, Xuanyu Space and Xuanyu Intelligence, were injected into Kangtu Infrared (now Aerospace Intelligent Installation), and Kangtu Infrared became the main platform in the field of intelligent equipment business of the aerospace technology application industry of the Fifth Academy of Aerospace Technology. Since then, the Fifth Academy of Sciences has completed the reform in 2020, through the reorganization of Qian Xuesen's Space Technology Laboratory, the General Design Department, and the Communication and Navigation Satellite General Department, and the establishment of the Remote Sensing Satellite General Department, to create a top-level structure of "one innovation center + two types of overall units". The business line has been sorted out, and its listed company, China Satellite, is the listing platform of the aerospace industry of the Fifth Academy, and the follow-up impact of the reform is worth paying attention to.

2. Missile weapons

The Group's missile weapons business is divided into strategic nuclear missiles, conventional surface-to-surface missiles, air defense and anti-missile equipment, unmanned aerial vehicles and other equipment. The main body of the research and development of missile systems in the group is mainly the First, Fourth and Eighth Aerospace Institutes. The main body of the research and development of the rocket system is mainly the Seventh and Ninth Aerospace Institutes. The overall unit responsible for the development of UAVs in the group is the 11th Academy of Aerospace.

· In terms of strategic nuclear missiles: Aerospace science and technology is China's intercontinental strategic nuclear missile development and production unit, which has realized the leap from single-stage to multi-stage, from liquid to solid, from land-based to land-sea, from fixed launch to mobile launch, and from medium- and long-range to intercontinental, and has formed a strategic nuclear deterrence equipment system with both solid-liquid coexistence, range connection, land and sea possession, and markedly enhanced power and effectiveness.

· Conventional surface-to-surface missiles: The conventional surface-to-surface missiles developed by aerospace science and technology have made a leap from traditional ballistic to maneuvering gliding, and are at the forefront of the world in terms of hitting accuracy, penetration capability, and multiple target destruction technologies and capabilities.

· Air defense and anti-missile equipment: As the core unit of our army's air defense and anti-missile weapons and equipment construction, aerospace science and technology has formed an air defense and anti-missile equipment system that matches the high, medium and low levels, and connects the long, medium and short ranges to meet the needs of different situations such as regional and field accompanied air defense.

· Unmanned aerial vehicles (UAVs) and other equipment: According to market demand and its own technical advantages, aerospace science and technology actively extends to UAVs, rockets, guided bombs and other fields. After years of development, the product spectrum has been increasingly improved, creating a number of internationally renowned brands such as Rainbow, Guard, Feiteng, etc., which not only equip domestic troops, but also export related products to more than 30 countries and regions in Asia, Africa, Europe, etc. In 2018, the 11th Academy of Aerospace completed the listing of drone-related assets through major asset restructuring, and was injected into the company's Nanyang Technology and renamed Aerospace Rainbow.

3. Aerospace technology application and aerospace technology service industry

Giving full play to the advantages of aerospace technology, aerospace science and technology has formed a military-civilian integrated development pattern in key areas such as satellite applications, special equipment, energy-saving and environmental protection equipment, advanced materials and applications, and electronic information products, and cultivated an aerospace industry chain integrating space and earth. In addition, the group company vigorously develops five major sectors, including satellite and its ground operation services, financial services, international services, information and software services, and supporting development of industrial bases, so as to realize the transformation of the group company from product manufacturing as the center to the combination of manufacturing and services.

The relevant entities of the sector include listed companies such as China Satcom, Beijing Shenzhou Aerospace Software Technology Co., Ltd. (the only specialized software enterprise controlled by the group) and other enterprises.

(4) Aerospace science and industry: the asset securitization rate is only 23%, and there is huge room for improvement

China Aerospace Science and Industry Corporation is the backbone of China's aerospace industry and national defense science and technology industry, and the main force in the construction of a space power and national defense weapons and equipment. Formerly known as the Fifth Research Institute of the Ministry of National Defense established in October 1956, it has experienced the historical evolution of the Seventh Ministry of Machinery Industry (merged into the Eighth Ministry of Machinery Industry in September 1981), the Ministry of Aerospace Industry, the Ministry of Aerospace Industry, and the China Aerospace Industry Corporation. In July 1999, China Aerospace Electromechanical Corporation was established; In September 2001, it was renamed China Aerospace Science and Industry Corporation; In November 2017, it was restructured and renamed China Aerospace Science and Industry Corporation. At present, the group has 24 secondary units, 8 listed companies, about 500 sub-units at all levels, and nearly 150,000 employees.

The main business of aerospace science and industry includes five categories: defense equipment, aerospace industry, information technology, equipment manufacturing and modern service industry. As of the end of 2023, the assetization rate of the net assets caliber group is only 23%, and many assets including missiles, flight products, commercial aerospace and other assets have not been securitized. We believe that China's commercial aerospace industry has ushered in a period of rapid development, but the relevant listed companies are limited, especially in the overall satellite manufacturing and rocket launches, and the group may give priority to the mixed reform and listing of such assets.

1. Aerospace defense equipment industry

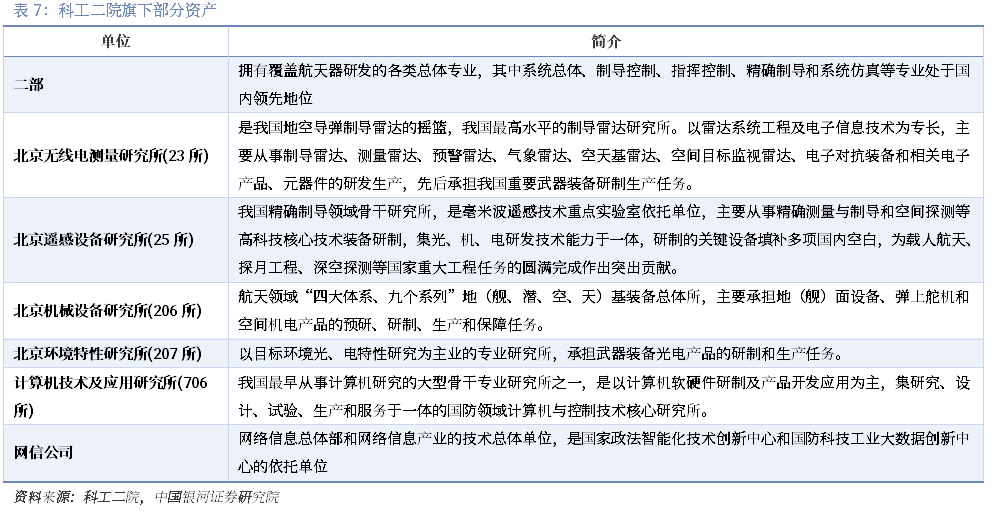

The group has always been the main unit of the development and production of national missile weapon systems, and has established a complete development and production system of air and space defense missile weapon systems, flight missile weapon systems, and ballistic missile weapon systems. The overall level of weapons and equipment is leading in China, and some professional technologies and products have reached the world's advanced level. The main business entities include the Second Institute of Science and Industry, the Third Institute of Science and Industry, and the Fourth Institute of Science and Industry.

· China Aerospace Defense Technology Research Institute of the Second Academy of Sciences: Responsible for the development and production of various subsystems of air defense weapons, it has undertaken and successfully completed the development and production of China's early surface-to-surface missile control system, China's first, second and third generation ground-to-air missile weapon system, China's first solid submarine-to-surface strategic missile, and solid land-based mobile strategic missile.

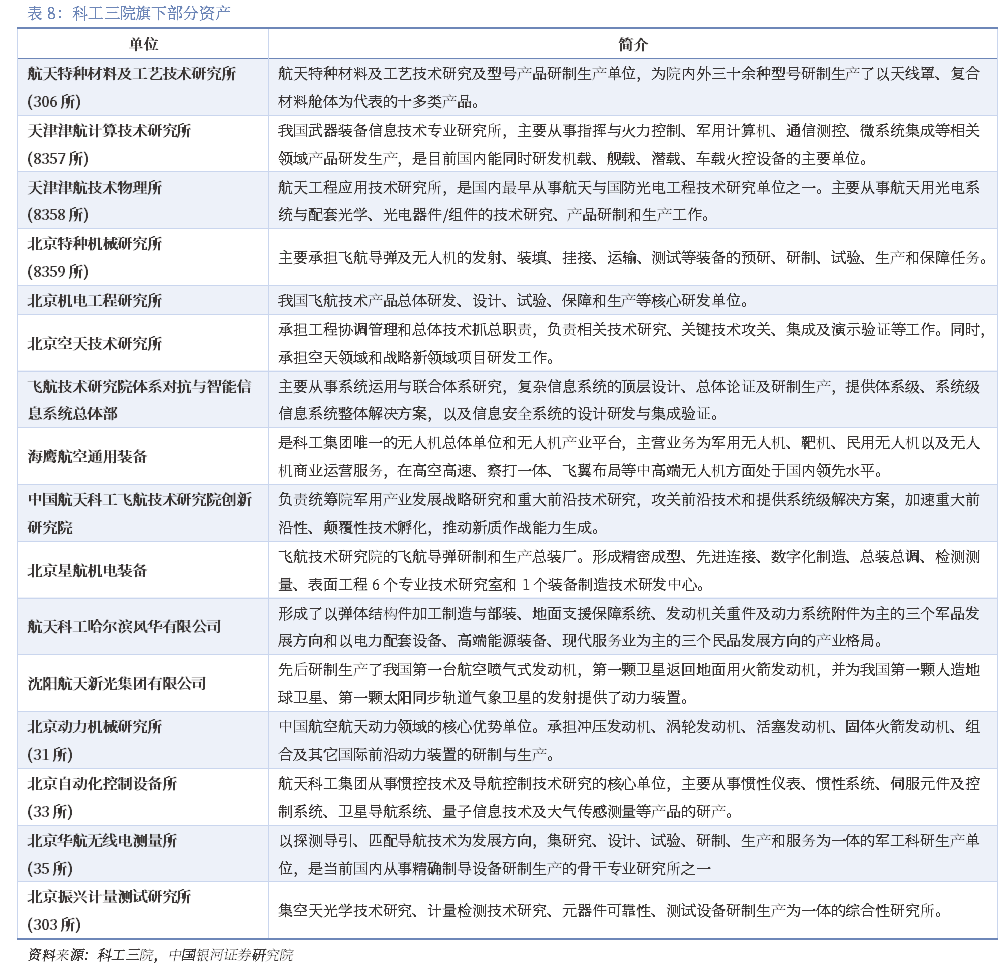

· The Aviation Technology Research Institute of the Third Academy of Sciences: It is a flight technology research institute integrating pre-research, development, production and support in China, with complete supporting facilities and complete categories, specializing in the overall design of flight products, power, inertial navigation, radar measurement and control, infrared laser, special materials, computers and other fields. There are 34 units directly under the three institutes, including 6 overall design units, 1 innovation research institute, 10 research institutes, 16 wholly-owned and holding companies (including 1 listed company aerospace science and technology), and 1 comprehensive support unit.

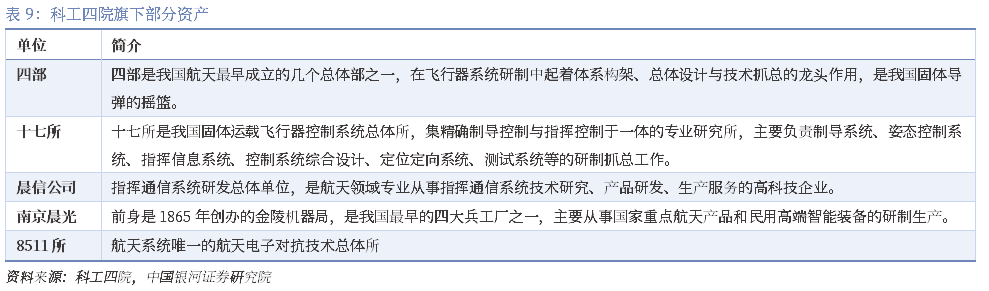

· The Fourth Academy of Aerospace Vehicle Technology Research Institute: In July 2024, the Science and Industry Group will implement reform and adjustment, and establish a new Fourth Research Institute of China Aerospace Science and Industry Corporation, and in November of the same year, the 8511 Research Institute will be merged into the Fourth Academy.

2. Aerospace industry

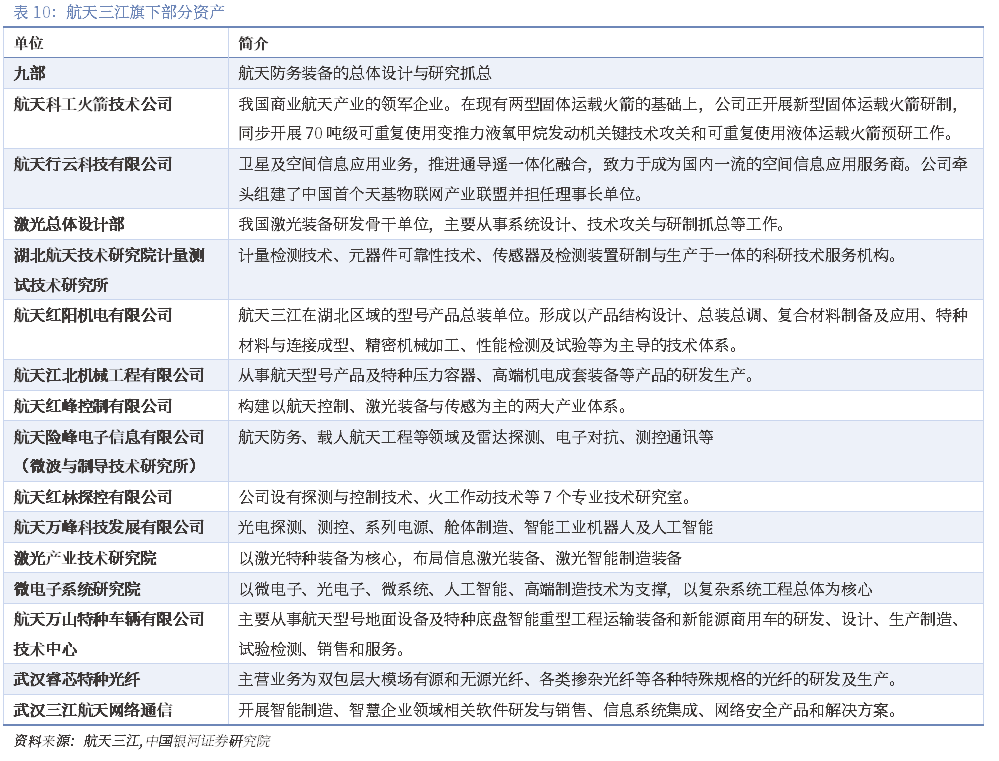

Dozens of technical products independently developed by the group escorted the "Shenzhou" flight, "Tiangong" docking, "Chang'e" lunar exploration, "Beidou" networking, "Tianwen" fire exploration and space station construction, effectively ensuring the successful completion of major national aerospace engineering tasks; The Kuaizhou-1A and Kuaizhou-11 solid launch vehicles were successfully developed to promote the continuous improvement of rapid response space capabilities. Successfully developed and launched the Tiankun series of satellites and low-orbit broadband communication technology verification satellites, established the Tianmu meteorological detection satellite constellation, and realized the on-orbit verification and application of characteristic space platforms and payload technologies; Facing the national economic construction and social development, it provides systematic services with satellite applications as the traction. The main body of business execution is Aerospace Sanjiang, and the Kuaizhou-1A carrier rocket developed by it has realized the performance ability of the normal launch of the commercial space launch market, and has preliminarily constructed the Kuaizhou series of solid launch vehicles.

· The Ninth Academy (Aerospace Sanjiang Group Co., Ltd.) is the main body and technical unit for the development and production of aerospace defense equipment, laser equipment and launch vehicles in China. Aerospace Sanjiang was formerly known as the O 66 base; In November 2006, the O 66 base was renamed the Ninth Research Institute of China Aerospace Science and Industry Corporation; In November 2011, it was merged and reorganized with the former Fourth Academy of Aerospace Science and Industry; In November 2017, it was restructured from a nationally owned enterprise to a company-based enterprise Aerospace Sanjiang; In July 2024, the Science and Industry Group will implement reform and adjustment and establish a new Ninth Research Institute of China Aerospace Science and Industry Corporation. Its listed company is Ruike Laser.

3. Other services

Information technology accounts for about 20%. The main business of the information technology sector of the group company is concentrated in the field of smart industry and independent controllability, and the main business undertaking includes the Sixth Academy of Science and Industry and the aerospace information of listed companies.

The

equipment manufacturing segment accounted for about 18% of the revenue, and its main business was concentrated in high-end equipment, special vehicles and auto parts, petrochemical equipment, power equipment, emergency equipment, industrial basic parts and new materials. The main body of business undertaking is the Second Academy of Science and Industry, the Fourth Academy, the Sixth Academy and the listed company Aerospace Chenguang.

(5) Future prospects: The listing of the core assets of the Department of Aerospace and the Department of Electrical Science is gradually approaching

At present, the level of asset securitization of military central enterprises is gradually improving, and the aviation, aviation development, shipbuilding and weapons groups have basically completed the overall listing of core assets, while the listing process of the core assets of the two major aerospace groups and the electric technology group is lagging behind. At present, the two major aerospace groups and the listed companies under the power group have a situation of "small but not strong" or "large but not excellent", most of the high-quality assets are free from the listed companies, and the asset quality of listed companies has huge room for improvement, and the future injection is expected to rise. From the perspective of the evolution process of the nature of the injected assets, the overall process shows a gradual injection process from the early peripheral component assets to the system-level assets and then to the core military products and assembly assets.

It is expected that with the improvement of the quality and efficiency requirements of the State-owned Assets Supervision and Administration Commission for listed companies of central enterprises, after 2025, the obstacles to the restructuring of scientific research institutes will be gradually removed, and the restructuring of institutes is expected to adhere to the principle of "mature batch, promote a batch", from "non-core" to "core", "tactical" equipment to "strategic" equipment field, and the asset securitization of military industrial groups is expected to enter the 2.0 era of transition from enterprise assets to institution assets.

From the perspective of subdivisions, China's commercial aerospace has ushered in a period of rapid development, but the relevant listed companies are limited, especially in the overall satellite manufacturing and rocket launches.

Fourth, market value management solutions have emerged

The innovation mechanism has been continuously improved

(1) Market value management is on the table, and the valuation of military central state-owned enterprises can be expected to be repaired

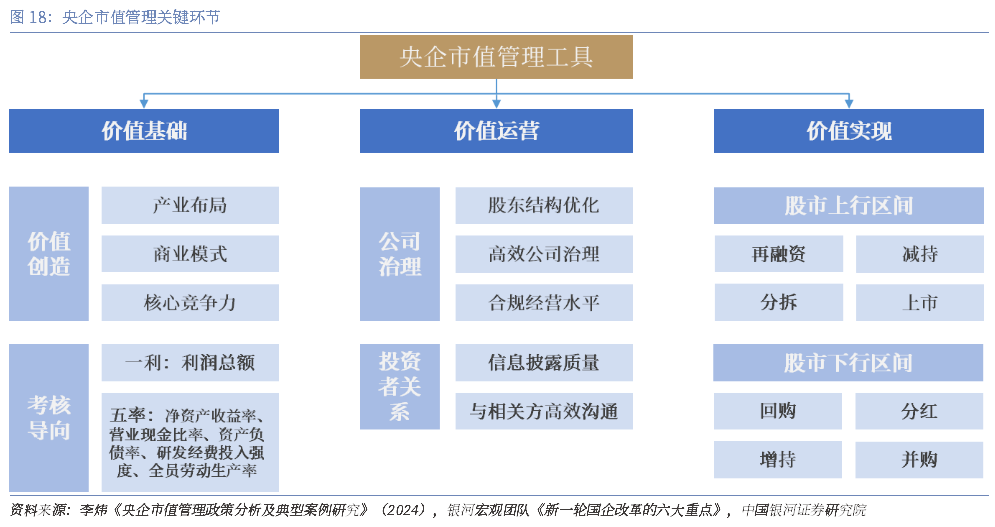

As the stabilizer and ballast of the national economy, state-owned listed companies are an important force in promoting China's modernization, but the current valuation level of state-owned enterprises in various industries is not consistent with their strategic position. Strengthen the assessment of market value management, guide state-owned enterprises to refine and optimize the assets of listed companies, improve the standard operation level of listed companies, promote valuation repair, and guide state-owned enterprises to focus on enhancing core functions and enhancing core competitiveness, so as to better achieve an effective path for high-quality development.

Strengthening the management of the market value of state-owned listed companies is an important part of improving the current management of state-owned assets in China. In the future, state-owned listed companies can strengthen market value management by increasing holdings in the market and encouraging buybacks. With the deepening of market value management, the core competitiveness of state-owned listed companies will continue to be enhanced, and their position in the capital market will be further enhanced, which is of great significance for enhancing the stability of the capital market. At the same time, the continuous deepening of market value management will force the optimization and adjustment of market structure, stimulate the innovation potential of state-owned enterprises, and promote them to increase the layout of strategic emerging industries such as new generation information technology, new energy, and new materials.

The market value management assessment of central state-owned enterprises will be fully launched during the year, and the process of valuation reshaping is expected to accelerate. "Market value management" has been included in the performance appraisal of central enterprises and has become a milestone event in the revaluation of central enterprises. On January 24, 2024, the State-owned Assets Supervision and Administration Commission (SASAC) announced that it would "further study the inclusion of market value management in the performance appraisal of the heads of central enterprises". This is the first time that SASAC has mentioned the inclusion of "market value management" in the performance appraisal system. On January 29, the State-owned Assets Supervision and Administration Commission further proposed that "all central enterprises should be more prominent, accurate and effective, promote the full implementation of the 'one enterprise and one policy' assessment, and comprehensively promote the market value management assessment of listed companies".

At the end of May, the Aerospace Science and Technology Group, China National Nuclear Corporation, and China Shipbuilding Group all organized their listed companies to hold a collective performance briefing on the Shanghai Stock Exchange, indicating that the central enterprise group companies actively responded to and implemented the instructions of the State-owned Assets Supervision and Administration Commission on improving the quality of listed companies controlled by central enterprises, and continuously deepened the implementation of the new "National Nine Articles" on promoting listed companies to enhance investment value and strengthen market value management.

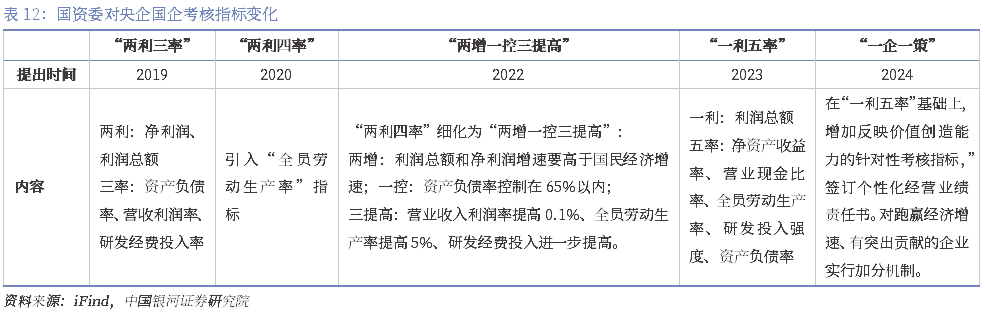

Previously, in 2023, the State-owned Assets Supervision and Administration Commission (SASAC) will optimize the operating index system of central enterprises from "two interest and four rates" to "one profit and five rates", with the overall goal of "one increase, one stability and four improvements": "one increase" means that the growth rate of total profits is higher than the national GDP growth rate; "One stability" means that the asset-liability ratio should be generally stable; The "four improvements" are the four indicators of return on net assets, R&D investment intensity, labor productivity of all employees, and operating cash ratio to be further improved.

(2) The actions of "improving quality and efficiency, emphasizing returns" and "double improvement of quality returns" have been comprehensively promoted

1. More than 30 military state-owned enterprises issued an action plan for improving quality and efficiency and emphasizing returns

Since 2024, a number of state-owned enterprises have issued action plans for improving quality and efficiency. According to our statistics, as of November 16, 2024, a total of 53 enterprises in the military sector have issued the plan of "Improving Quality and Efficiency and Valuing Returns", of which 32 are state-owned enterprises. China Shipbuilding, CSSC Defense, AVIC Shenfei, AVIC Heavy Machinery, Zhongzhi Co., Ltd. and other OEMs have issued action plans, mainly focusing on improving value creation capabilities, high-quality development of their main businesses, improving scientific and technological innovation capabilities, lean management, attaching importance to investor returns, and improving company value.

AVIC Shenfei's 2024 action plan of "Improving Quality and Efficiency and Emphasizing Returns" proposes that in 2024, the company will focus on accelerating scientific and technological innovation. Improve the scientific and technological innovation system, explore the establishment of a multi-level and distributed scientific and technological innovation system, and build a new scientific and technological innovation ecology; Deepen the development of equipment, give full play to the role of "chain master", formulate and implement a systematic and systematic industrial chain research plan, focus on "primary responsibility, main responsibility, and main business", accelerate the construction of a coordinated development pattern of military aircraft and civil aircraft, accelerate the construction of a world-class enterprise, and strive to promote the high-quality development of the aviation industry. In addition, AVIC Shenfei released the "AVIC Shenfei Environmental, Social and Corporate Governance (ESG) Report" for the first time, and its 2023 Wind ESG rating was upgraded from A to AA. We expect that more military state-owned enterprises will publish ESG and other social responsibility reports to promote investment value and enhance investor returns.

From the perspective of investor relations, a number of military state-owned enterprises have strengthened their investment and customs work in accordance with the action plan of "improving quality, efficiency and return". In line with the core concept of "respecting investors, rewarding investors and protecting investors", AVIC has taken multiple measures to manage investor relations, continuously strengthened communication with investors, actively responded to investors' concerns, actively participated in strategy meetings, and strengthened exchanges with analysts.

2. Double improvement action of quality return

Since 2024, a total of 7 listed companies in the military sector have issued action plans for "double improvement of quality returns", of which 4 are state-owned enterprises, including AVIC Optoelectronics, Zhenhua Technology and AVIC, mainly to strengthen R&D investment, innovation-driven development, improve corporate governance, protect the rights and interests of shareholders, improve the quality of information disclosure, and continue to standardize operations.

(3) Investor relations are valued, and dividends help increase the intrinsic value of state-owned enterprises

1. Military state-owned enterprises pay more and more attention to investor relations management

Investor relations management is an inevitable choice for the sustainable development of the national defense and military industry. Due to the high technical risk and low degree of information disclosure in the military industry, it is difficult for external investment institutions to reliably assess the intrinsic value of enterprises, resulting in investors being cautious about investing in the military industry. It is an inevitable choice to promote the development of the military industry how to promote investors' understanding and recognition of the military industry through investment management and compliance, and how to enhance the market image of listed military enterprises to attract investors. In terms of the capital market, due to the constraints of military secrecy management, it is inconvenient to interpret and visit important projects related to business outlook such as revenue and profits, which exacerbates the dilemma that investors cannot approach, understand and see clearly. Especially in recent years, uncertain matters such as competitive procurement of weapons and equipment, price control reform, etc., have not only had a great impact on the operation of enterprises, but also brought uncertainty to market valuation.

Since 2024, a number of military state-owned enterprises have released market value management plans, focusing on improving investor relations management. According to the work report of the board of directors of AVIC West Airlines, in 2024, it will strengthen market value management to enhance market recognition and value realization. The company will implement the relevant requirements of the State-owned Assets Supervision and Administration Commission of the State Council on market value management assessment, and improve the company's market value management performance appraisal and evaluation system. Optimize the working mechanism of market value management, strengthen investor relations management and external publicity, and actively cultivate "cornerstone investors". The market value management work in 2024 will be carried out from the three dimensions of "value creation, value realization, and value management" to enhance market recognition and increase the company's market value. AVIC Heavy Machinery actively implements the Work Plan for Improving the Quality of Listed Companies Controlled by Central Enterprises issued by the State-owned Assets Supervision and Administration Commission of the State Council and related requirements, formulates a work plan, and will adhere to the market value management concept with value creation as the core, further enhance the value realization ability, and effectively promote the high-quality development of the company.

From the perspective of information disclosure evaluation, from 2023 to 2024, the information disclosure evaluation results of 36 national defense and military industry companies will be Class A, and the information disclosure evaluation results of 10 companies such as China Bo Electronics, Zhenhua Fengguang, and Zhongtian Rocket will be upgraded.

2. State-owned enterprises are the main force of dividends in the industry, and there is room for further improvement in the dividend rate of more state-owned enterprises

The

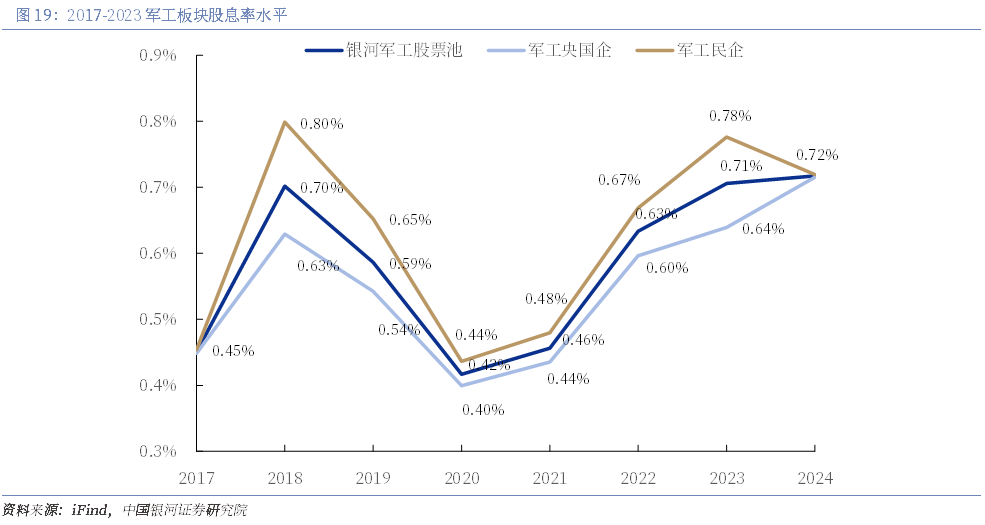

dividends and dividends of the military sector are lower than the average level of all A-shares, and there is still a lot of room for improvement. In 2023, all A-shares will pay a total dividend of 2,197.57 billion yuan, of which central state-owned enterprises will account for 67%. In the past 12 months, the average dividend yield of military central state-owned enterprises is 0.67%, and that of military and private enterprises is 0.69%, which is not much different, both are far lower than the average of 1.67% of A-shares, and there is still a lot of room for improvement.

The national defense and military industry will pay a total of 15.724 billion yuan in dividends in 2023, of which 12.655 billion yuan will be distributed by Chinese enterprises, accounting for 80.5% of the total dividends; A total of 60 of the 76 state-owned enterprises paid dividends. AVIC Optoelectronics, AVIC Airborne, and AVIC Shenfei are among the top dividends: the total cash dividends of AVIC Optoelectronics are 1.272 billion yuan, accounting for 38.1% of the net profit attributable to the parent company; In 2023, the total cash dividends of AVIC Airborne will be 609 million yuan, accounting for 32.32% of the net profit attributable to the parent company, and the total cash dividends of AVIC Shenfei will be 1.102 billion yuan, accounting for 36.66% of the net profit attributable to the parent company. From the perspective of dividend ratio, Inner Mongolia has a higher dividend ratio, reaching 50%, and most state-owned enterprises have a dividend ratio of more than 30%.

The dividend ratio of many state-owned enterprises has increased year by year. From 2019 to 2023, AVIC Shenfei has paid a total of 3.239 billion yuan in cash dividends, and the total annual cash distribution has increased from 210 million yuan in 2019 to 1.102 billion yuan in 2023. The company has formulated the "Shareholder Dividend Return Plan for the Next Three Years (2023-2025)", and established a sustainable, stable and scientific dividend return mechanism for investors. From the perspective of dividend rate, the average ratio of cash dividends to net profit in 2021-2023 is 38.42%. At present, the proportion of military state-owned enterprises with dividend rates below 30% is still large, and we expect more state-owned enterprises to increase their dividend rates year by year.

(4) The scientific and technological innovation system has been continuously improved, and the R&D investment has continued to increase

From the perspective of the reform of the system and mechanism of scientific and technological innovation, the key to Chinese-style modernization lies in scientific and technological modernization, and the key to building a modern socialist country in an all-round way lies in scientific and technological self-reliance and self-reliance. As an important part of the national strategic scientific and technological forces, state-owned enterprises must accurately grasp the strategic positioning in the overall situation of China's scientific and technological innovation, regard scientific and technological innovation as the "number one task", accelerate the research of key core technologies, and provide important support for the development and expansion of national strategic scientific and technological forces. The key to the reform of military state-owned enterprises is to strengthen original scientific and technological research, accelerate the construction of R&D platforms, increase diversified R&D investment, build strategic talent forces, promote the improvement of the system of military state-owned enterprises to support scientific and technological innovation, and help achieve high-level scientific and technological self-reliance and self-reliance.

A number of military industrial groups have improved the system and mechanism of scientific and technological innovation from the group level. China North Industries Group Co., Ltd. focuses on enhancing core functions and improving core competitiveness, building a "3+3+1+X" reform system, in-depth implementation of the deepening and upgrading of the reform of state-owned enterprises, and has achieved remarkable results in the key tasks of strengthening the army and protecting the army, and has made significant progress in military scientific research. In 2023, the total profit of Ordnance Industry Group will be 25.2 billion yuan, a year-on-year increase of 4.68%, and the economic added value and scientific and technological investment will increase by 10.80% and 27.44% year-on-year respectively, and the operating performance and scientific research efforts will be greatly improved. Aviation Industry Corporation of China (AVIC) is committed to the mission of becoming an aviation power, formulating and releasing the "30 Innovation Decisions", the reform of the scientific and technological innovation system and mechanism, and the full-cycle action of scientific and technological innovation, focusing on building a complete and effective innovation system and creating "leading innovation".

From the perspective of R&D investment, according to our statistics, the overall R&D expenditure of the military sector in the first three quarters of 2024 was 22.644 billion yuan, a year-on-year decrease of 1.37%; The R&D expense ratio was 5.84%, up 0.30pct year-on-year. Its R&D expenses of Chinese enterprises were 13.579 billion yuan, down 7.89% year-on-year; The R&D expense ratio was 5.37%, up 0.22pct year-on-year. In the first three quarters of 2024, the revenue of state-owned enterprises in the military sector fell by 11.60% year-on-year, and the net profit fell by 28.75% year-on-year. In absolute terms, state-owned enterprises are still the absolute main force in R&D investment in the military sector.

5. Investment suggestions: pay attention to improving quality and efficiency

"Large compounds and small platforms" are two-dimensional

China is exploring a valuation system with Chinese characteristics, and there is still a lot of room for improvement in military central enterprises. First of all, the reform of state-owned enterprises has entered the deep-water area, the requirements for improving the quality and efficiency of central enterprises are even greater, and the operating quality of military central enterprises has been steadily improved; Secondly, the overall asset securitization rate of military central enterprises is low, and the value revaluation is achieved through high-quality asset injection/spin-off, accelerating the integration of the industrial chain and listing; Thirdly, the market value assessment and management measures of central enterprises have been fully implemented, and the assessment and management measures of "one enterprise and one policy" will provide assistance for the revaluation of the value of central enterprises.

We recommend paying attention to:

(1) The beneficiary target of state-owned enterprise reform to improve quality and efficiency: AVIC Shenfei (600760.HK) SH), AVIC West (000768. SZ), AVIC Optoelectronics (002179. SZ), Aerospace Electric (002025. SZ) and Northern Navigation (600435.SH);

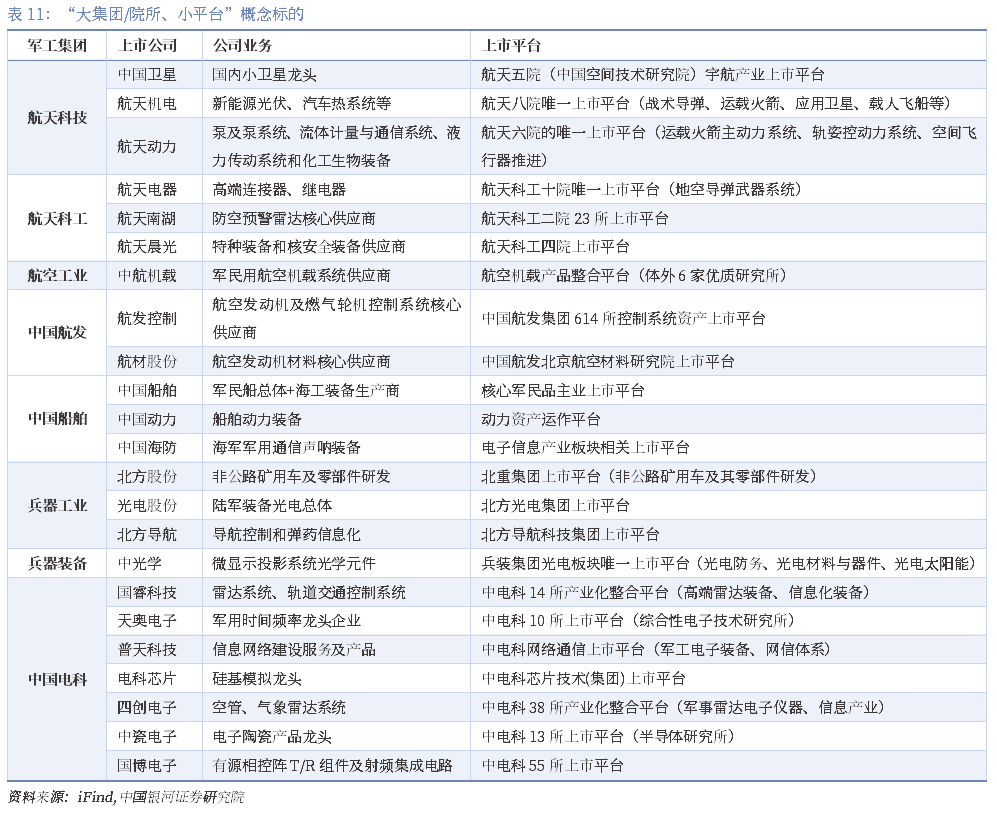

(2) "Large groups/institutes, small platforms" listed companies: Guorui Technology (600562. SH), Guobo Electronics (688375. SH), Aviation Materials Co., Ltd. (688563. SH), Aviation Development Control (000738. SZ), China Coastal Defense (600764. SH), Aerospace Electromechanical (600151. SH), Aerospace Nanhu (688552. SH) and Aerospace Chenguang (600501.SH).

6. Risk Warning

Risk that the reform/restructuring of central SOEs is less than expected: The organizational structure of central SOEs is complex, and military enterprises have confidentiality needs, which makes it difficult to reform and reorganize, or the progress may be affected by multiple factors.

Military review pricing risk: According to China's relevant system for the management of military product purchase prices, the sales price of some of the company's military products must be priced by military review, and it may be necessary to refund the difference with the customer on the product of the cumulative sales quantity of the relevant products in the early stage and the price difference when determining the military review price. Due to the uncertainty of the finalization and price review cycle of military products, it is difficult to reasonably predict the time and results of the price review, which may have a partial impact on the performance of some companies.

Risk of fluctuation in the purchase price of raw materials: military products are mostly in the manufacturing industry, the cost of raw materials accounts for a high proportion of business costs, and raw materials are widely used in many fields, and their supply, demand and prices are affected by various factors such as upstream supply, downstream demand, mining and production technology development, commodity trading, geopolitics, and national policies.

The risk that downstream orders are less than expected: The main products of the military industry are used in aviation, aerospace, weapons, ships and other fields, and the military's annual orders may change according to national policies and macro environment.

The risk of intensified competition in the industry: With the adjustment and opening up of the national industrial policy and the improvement of the overall R&D and manufacturing level of China's military products, there may be more competitors entering the military sub-industry in the future, and the industry competition may intensify, which may have an adverse impact on the product sales, price, market share and gross profit margin of the company in the current industry.

This article is excerpted from: China Galaxy Securities released a research report on November 25, 2024 "[Galaxy Military Industry] Asset Integration Deepens Again, Improves Quality and Efficiency and Rejuvenates the New Look - Military Central State-owned Enterprises Leading the Special Topic".

Analysts: Li Liang, Hu Haomiao

Rating Criteria:

Recommended: More than 10% increase relative to the benchmark index.

Neutral: The relative benchmark index has risen between -5%~10%.

Avoidance: Relative to the benchmark index fell by more than 5%.

Recommended: More than 20% increase relative to the benchmark index.

Cautious recommendation: relative to the benchmark index increase between 5% ~ 20%.

Neutral: The relative benchmark index has risen between -5%~5%.

Avoidance: Relative to the benchmark index fell by more than 5%.

Ticker Name

Percentage Change

Inclusion Date