As the world's outstanding robot host manufacturers represented by Figure, Agility, Zhiyuan, Unitree, Leju, etc., have begun to ship one after another, 2024 has been established as the "first year of commercialization" of humanoid robots. According to statistics compiled by CITIC Securities, the number of global humanoid robot shipments will reach more than 2,000 units in 2024, and it is expected to reach 1-20,000 units in 2025.

Based on this industry trend, the robot sector is sought after in the capital market. According to the Wind Robot Index, the sector has risen by more than 80% since September, among which big bull stocks such as Eft-U (688165.SH) and Keli Sensing (603662.SH) were born.

If you carefully comb through it, it is not difficult to find that in fact, the market speculation is not only humanoid robots, but also branches such as quadruped mechanical dogs and industrial robotic arms, which have also attracted the attention of the market. Under such market sentiment, Inlifu, a robotic arm manufacturer from Quanzhou, Fujian Province, accelerated its journey to go public in the United States.

Zhitong Finance and Economics learned that after Inlifu first submitted the public version of the prospectus to the SEC on May 21, it updated the prospectus for the fifth time on December 10, which shows its rapid action.

According to the latest version of the prospectus, Inlifu applied for listing on the NASDAQ under the symbol "INLF", and it will issue 2 million common shares in the IPO at an issue price of $4-6 per share, raising up to $12 million. If the over-allotment mandate is not exercised, Inlif's issuance of 2 million common shares represents 14.03% of the company's total shares, which means that Inlif's IPO valuation is $57.02 million to $85.53 million.

From the perspective of performance, Inlif's revenue in 2022 and 2023 will be US$6.6523 million and US$12.6109 million respectively, with a growth rate of 89.6%, and the corresponding net profit during the period will be US$537,600 and US$1.3525 million respectively, with a growth rate of 151.6%. Entering the first half of 2024, Inlif's revenue increased by 39.67% to US$6.7357 million, but its net profit fell by 28.33% to US$390,000.

The market can't help but wonder, why did Inlifu's net profit decline year-on-year in the first half of 2024? Can it use the heat of the robot sector to carry out a wave of hype? The answer may be found in the company's prospectus.

Benefit from industrial development and achieve rapid growth

Robotic arms (also known as "Cartesian robots") are one of the most common types of robots in industrial applications and are commonly used in injection molding machines and computer numerical control machines ("CNC machines"). Robotic arms belong to the category of industrial robots, which are mainly divided into three categories: three-axis robotic arms, five-axis robotic arms, and multi-headed robotic arms.

As early as 2016, in order to implement the "Made in China 2025" and guide the healthy and sustainable development of China's robot industry, the Ministry of Industry and Information Technology, the Development and Reform Commission, the Ministry of Finance and other three ministries and commissions jointly issued the "Robot Industry Development Plan (2016-2020)", requiring that by 2020 a relatively complete robot industry system should be formed, and the annual output of China's industrial robots should reach 100,000 units.

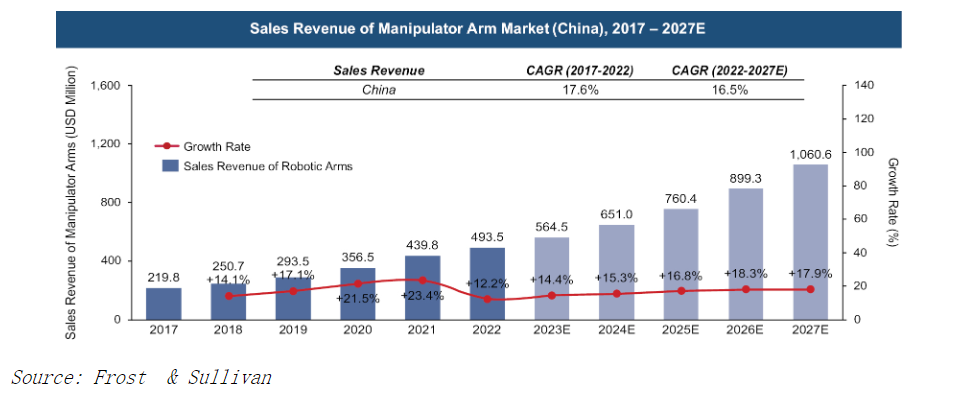

With the support of policies and the demand for reducing costs and increasing efficiency in the manufacturing industry, China's robotic arm market has ushered in rapid development. According to Frost & Sullivan data, from 2017 to 2022, the sales of robotic arms in China increased from about 35,700 units to 93,800 units, with a compound annual growth rate of 21.3%; During the same period, the sales of robotic arms in China increased from about 220 million US dollars to 490 million US dollars, with a compound annual growth rate of 17.6%.

It is worth noting that between 2020 and 2021, due to the difficulty of recruiting workers due to public health events, the penetration of automated production in the market accelerated, especially in the manufacturing industry, which further stimulated the market demand for robotic arms, so China's robotic arm market maintained a high growth trend in the past two years, and this trend will continue.

According to Frost & Sullivan's forecast, with the introduction of government support policies and the growing demand from downstream industries (such as the automobile, electronics and medical industries), the sales of robotic arms in China are expected to maintain rapid growth, reaching about 230,300 units by 2027, with a compound growth rate of 19.7% from 2022 to 2027; At the same time, the sales of domestic robotic arms will reach about $1.061 billion in 2027, with a compound growth rate of about 16.5% from 2022 to 2027.

Inlifu is one of the beneficiaries of the rapid development of the robotic arm industry. According to public information, Inlif's domestic operating entity is Eva Robot Equipment Manufacturing Co., Ltd., and Eva was established on September 28, 2016, which means that Inlif has actually been deeply involved in the robotic arm market for more than 8 years, which is engaged in the research and development, manufacturing and sales of special robotic arms for injection molding machines, while providing installation and maintenance services for robotic arms, it also sells robotic arm accessories and raw materials. Among them, the installation and maintenance service of the robotic arm is the core business of Inlifu, and the revenue of this business will account for 77.83% in 2023.

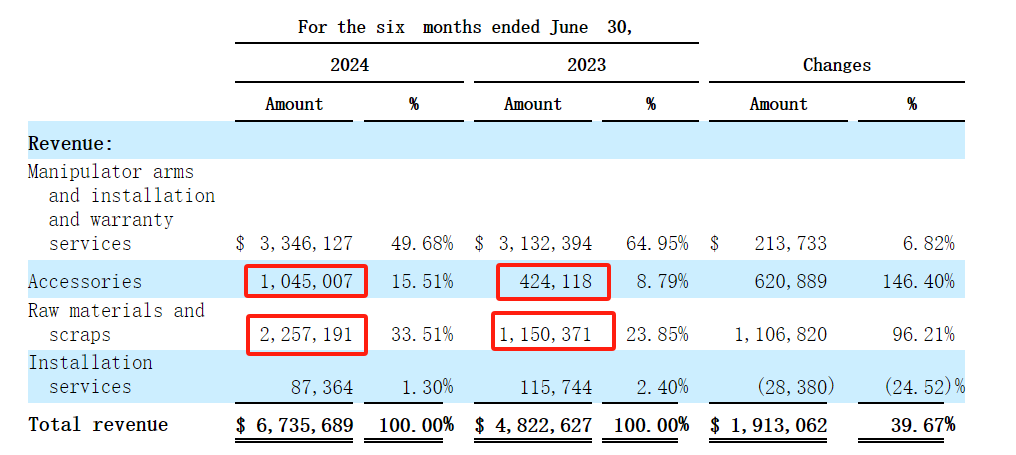

According to the prospectus, in 2022, 2023 and the first half of 2024, Inlifu's products will be sold to 101, 117 and 96 customers respectively. With the growth of the number of customers, Inlif's performance has also achieved sustained rapid growth, with revenue increasing by 89.6% to US$12.6109 million in 2023 and revenue growth of 39.67% to US$6.7357 million in the first half of 2024.

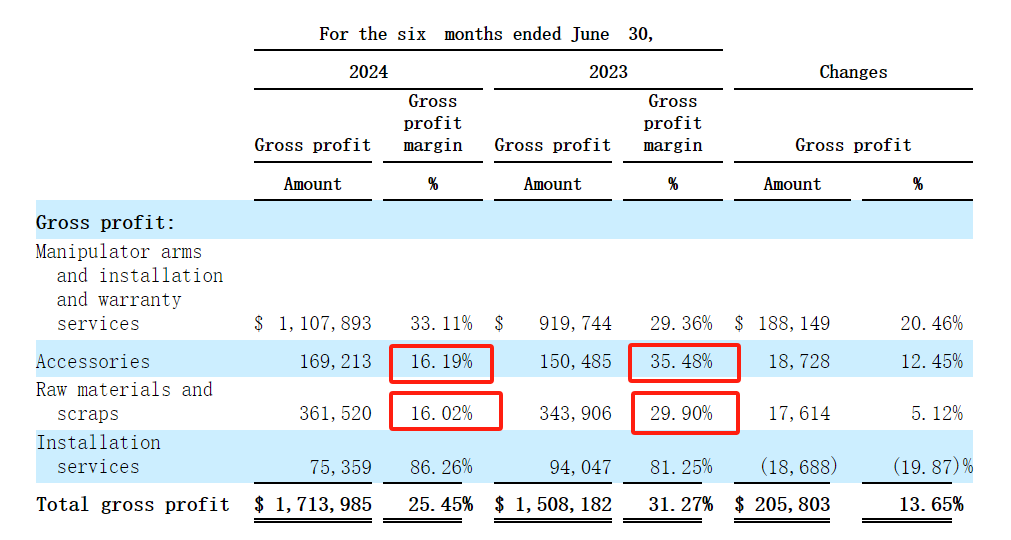

In the first half of 2024, Inlifu's net profit fell by 28.33% to US$390,000, mainly because the gross profit margin during the period decreased from 31.27% to 25.45%, coupled with a 65.85% increase in total operating expenses, and the growth rate of expenses was higher than the growth rate of revenue.

Core business stall warning risk

In fact, although Inlifu has benefited from the continuous and rapid development of the robotic arm industry, there are not a few potential business challenges it faces, and the increase in revenue and profit in the first half of 2024 is only one of them.

It is not difficult to find through the prospectus that the gross profit margin of Inlifu is on a downward trend. In 2022 and 2023, Inlif's gross profit margin will be 34.48% and 32.98% respectively, and by the first half of 2024, Inlif's gross profit margin will be 25.45%, a year-on-year decrease of nearly 6 percentage points.

In detail, the decline in gross profit margin in 2023 is mainly due to the decrease in the gross profit margin of the two major businesses of robotic arm installation and maintenance services, raw materials and corner material sales. In the first half of 2024, although the gross profit margin of robotic arm installation and maintenance services increased year-on-year, the gross profit margin of accessories sales, raw materials and scrap sales declined significantly, especially the gross profit margin of accessories fell by nearly 50%.

If combined with the performance of the income side of each business, it can be issued. According to the data, in the first half of 2024, the revenue growth rate of Inlifu's robotic arm installation and maintenance services will only be 6.82%, which is significantly "cooling" compared with the growth rate of 58.8% in the whole year of 2023, but the revenue growth rate of accessories sales, raw materials and scrap material sales is as high as 146.4% and 96.21% respectively, showing an explosive growth trend.

It is not difficult to see that when the development of the core business of robotic arm installation and maintenance services slows down, Inlifu has achieved the explosive growth of the two major businesses of parts sales, raw materials and leftover sales through the method of "price for volume", which can make the company's overall revenue growth not stall, but it has led to a significant decline in gross profit margin during the period, which has affected the company's profitability.

Based on the above judgment, it is particularly important whether the core business of robotic arm installation and maintenance services can return to rapid growth, and if the growth of this business continues to stall or even decline, it may have a further impact on the overall profitability of Inlifu.

From the perspective of the industry, the entire robotic arm industry is currently in a stage of continuous intensification of competition. Although the robotic arm market will continue to maintain double-digit rapid growth, the robotic arm market is actually quite fragmented, with about thousands of market participants, which also means that Inlif is in a very competitive environment.

According to Frost & Sullivan data, the market share of the top 10 manufacturers in China's robotic arm market in 2022 is 28% in terms of revenue. Although Inliv is one of the largest robotic arm manufacturers in Fujian Province, it ranks 10th in terms of revenue in 2022 nationwide, with a market share of only 1.4%. It can be seen how much competitive pressure Inliv is facing.

In addition, the significant increase in customer concentration is also a thorny problem that Inliv needs to solve. According to the prospectus, in mid-2022, Inlif has no customers with more than 10% of its revenue, and by 2023, the proportion of one of its customers in Inlif's total revenue has soared to 22.68%, and by the first half of 2024, Inlif's revenue from two customers will account for 34.83% and 12.05% respectively, totaling 46.88%.

Obviously, the rapid growth of Inlif's performance in 2023 is related to the significant increase in demand from one of its customers, but by the first half of 2024, Inlif's customer concentration has soared sharply again, but the growth of its core business has stalled, which indicates that Inlif may have difficulty in developing new customers. After the customer concentration has increased significantly, if the demand of large customers declines or the company's new customer development is not as expected, the business operation of Inleaf may be significantly affected.

Overall, the rapid development of the robotic arm market is still full of opportunities, but the continuous intensification of competition has also brought new challenges, because after the rapid development in 2023, the growth of its core business in the first half of 2024 has significantly stalled and the company's overall profitability is under pressure. If Inlifu can't come up with more competitive products in the market in the future, it may be difficult to reproduce the highlight moment of Inlif's rapid development.

Ticker Name

Percentage Change

Inclusion Date