Transferred from: Prospective Industry Research Institute

Major listed companies in the industry: Inovance Technology (300124), SUPCON Technology (688777), Megmeet (002851), INVT (002334), Kerui Technology (002957), Bojie (002975), etc

The core data of this paper: industrial automation industry chain; industrial automation market size; the development trend of industrial automation, etc

Industry Overview

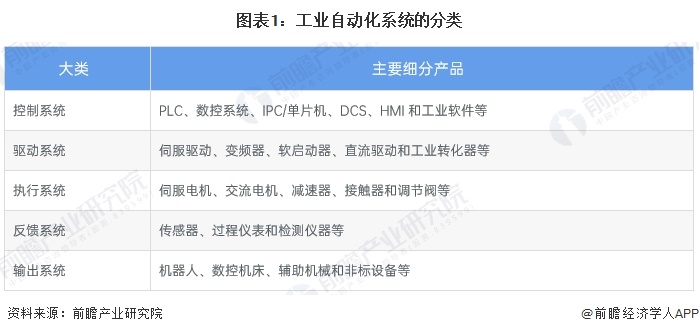

1. Definitions and Classification

Industrial automation refers to the application of automation technology in the manufacturing process of machinery industry to achieve automatic processing and continuous production, improve the efficiency and quality of mechanical production, and release productivity. The development of industrial automation relies on the deep integration of information technology, computer technology and communication technology, and automation technology has largely reversed the traditional operation mode and accelerated the transformation of traditional industrial technology.

Industrial automation products can be divided into control systems, drive systems, actuation systems, feedback systems and output systems. The control system includes PLC, numerical control system, IPC/microcontroller, DCS, HMI and industrial software, etc., and the drive system includes servo drive, inverter, soft starter, DC drive and industrial converter. The actuation system includes servo motors, AC motors, reducers, contactors and control valves, etc., while the feedback system includes sensors, process instruments and testing instruments. The output system includes robots, CNC machine tools, auxiliary machinery and non-standard equipment.

2. Analysis of the industrial chain: the industrial chain is long and all links are closely linked

From the perspective of industrial chain structure, the upstream of the industrial automation industry chain is mainly all kinds of power electronic components, including semiconductor components such as IGBT, electronic components such as resistors and capacitors, as well as raw materials such as permanent magnet materials, insulating materials, and structural parts.

The midstream is an industrial automation product, which can be divided into a control layer, a drive layer, an execution layer, and a sensing layer according to its function. The control layer realizes the analysis, processing and distribution of tasks, such as PLC, DCS, etc.; The drive layer decodes the tasks of the control layer and turns them into signals that can be recognized by motors, valves, etc., such as frequency converters and servo drives. The execution layer performs the corresponding tasks, such as various motors, valves, etc.

The downstream is the application field of industrial automation system, which can be divided into OEM industry and project industry, of which OEM industry mainly includes lithium battery, electronic manufacturing, semiconductor, machine tool, packaging, etc.; Project-based industries mainly include metallurgy, chemical industry, petrochemical, electric power, etc.

From the perspective of representative enterprises in each link of the industrial chain, the upstream is mainly semiconductor component suppliers such as Silan Micro, Jinxin Electronics, and Ziguang Tongchuang, electronic component suppliers of Torch Electronics, Fenghua Hi-Tech, and Sanhuan Group, as well as other material suppliers such as Pengding Holdings and Zhenghai Magnetics; Midstream industrial automation companies mainly include Inovance Technology, ZKTeco, INVT, Advantech, etc.

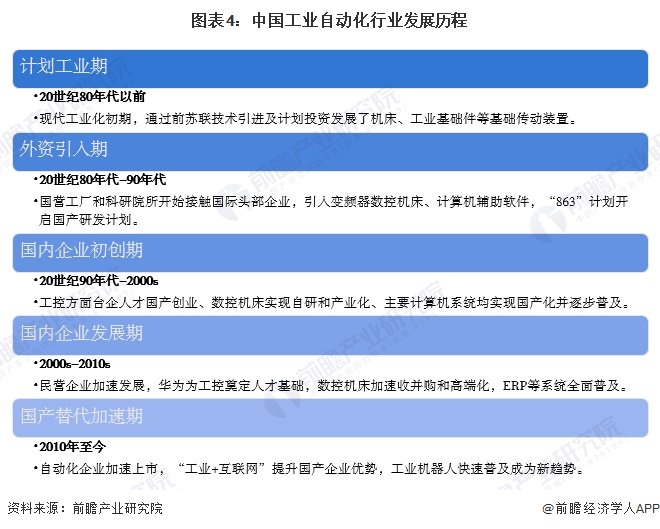

Industry development history: in the accelerated period of domestic substitution

The development of China's industrial automation has gone through the process from traditional manual operation to automation, digitalization and then to intelligence, and gradually introduced the Internet, Internet of Things and big data technology, through the application of automation equipment, industrial robots and artificial intelligence and other technologies, to achieve the digital transformation of the monitoring and management of the production process, improve production efficiency and product quality, and promote industrial transformation and upgrading. In the future, China's automated factories will be further developed into intelligent factories to achieve a higher level of automation and intelligence, and bring more innovation and competitive advantages to the factory.

Industry policy background: policy support to help the high-quality development of the industrial automation industry

As the focus of promoting the deep integration of informatization, intelligence and industrialization, industrial automation is the development direction that China continues to pay attention to. In recent years, the development of industrial automation has continued to receive national attention, including the State Council, the Ministry of Industry and Information Technology, the National Development and Reform Commission, the Ministry of Science and Technology and other relevant departments have issued a series of policies to encourage and support the development of the industrial automation industry. As of November 2024, the key policies of China's industrial automation industry are summarized as follows:

Industry development

1. The

production and sales of industrial robots are growing rapidly

Industrial robots are one of the core products of industrial automation. At present, China's high-end industrial robot market is still in short supply, but the low-end market has the risk of overcapacity, enterprises should improve the production level to improve high-end production capacity is the focus of development at this stage. In 2020, the output of industrial robots in China will be 237068, an increase of 26.8% year-on-year compared with the same period in 2019. In 2023, the output of industrial robots in China will reach 430,000 units, a slight decline. From January to October 2024, the output of industrial robots will reach 466,000 units, which has exceeded the annual output in 2023.

In terms of sales, since 2016, the cumulative sales of China's industrial robots have ranked first in the world, and the development speed is unprecedented. In 2019, China was still the world's largest robot market, with a total of 144,000 industrial robots, down 8.6% from 2018. According to the latest statistics from Industry Online, from January to October 2024, the sales volume of industrial robots in China will reach 458,000 units.

Note: The output data comes from the National Bureau of Statistics, the sales data from 2019 and before the International Federation of Robotics, and the source of 2020 and after is Industry Online

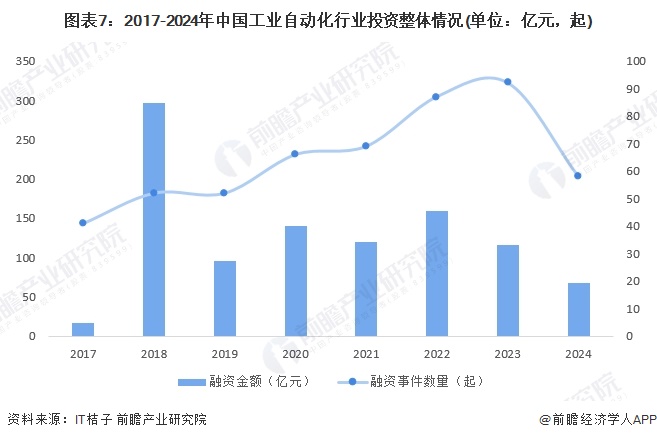

2. The industry investment is hot

From 2017 to 2023, the financing scale of China's industrial automation enterprises fluctuated, and the number of financing events increased as a whole. In 2023, a total of 92 financing events will occur in China's industrial automation industry, with a financing scale of 11.538 billion yuan, a year-on-year decrease of 27.5%. From 2017 to 2024, a total of 517 investment events occurred, with an investment amount of 101.145 billion yuan, and a large amount of capital investment catalyzed the rapid development of industrial automation technology and the improvement of market application, which also promoted the rapid development of a number of enterprises that attach importance to industrial automation.

Note: The data comes from the "Industrial Automation" tab in the IT Orange Investment Event Library; The above statistics are as of December 17, 2024

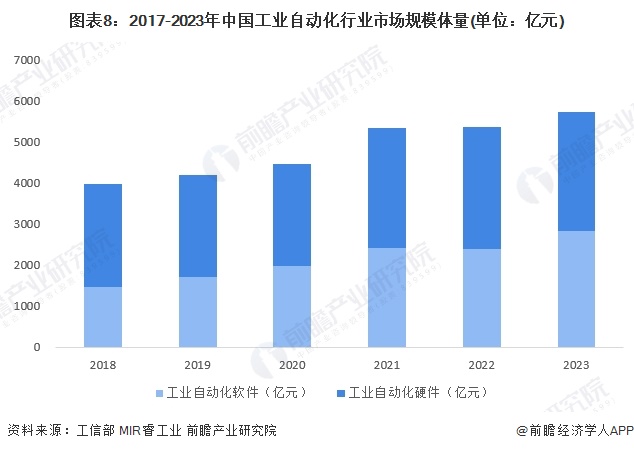

3. The scale of the industrial automation market fluctuates and grows

In recent years, with the development of new technologies such as artificial intelligence, 5G, and the Internet of Things, the intelligent level of industrial automation has gradually improved, which is an important driving force for the transformation and upgrading of the manufacturing industry. According to the statistics of the Ministry of Industry and Information Technology and MIR Rui Industry, the market size of China's industrial automation industry is growing as a whole, and the market size will increase from 397.7 billion yuan to 573.4 billion yuan from 2018 to 2023, with an average annual compound growth rate of 7.6%.

The competitive landscape of the industry

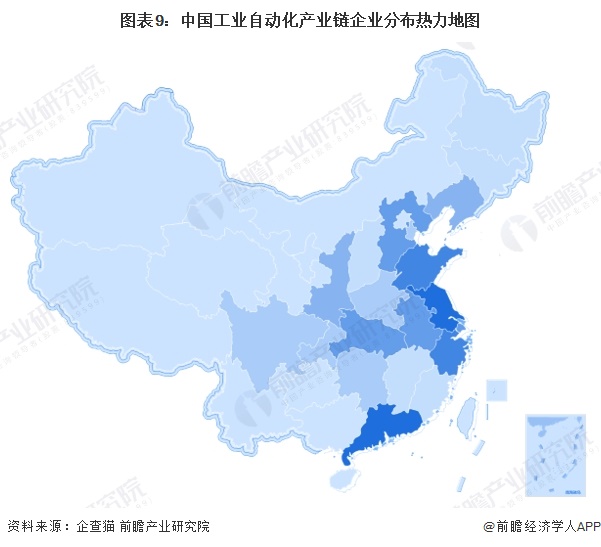

Regional competition: Guangdong and Jiangsu are the most concentrated

From the perspective of the regional distribution of industrial automation industry chain enterprises, the distribution of industrial automation enterprises in China is relatively concentrated, mainly distributed in the economically developed eastern coastal areas, represented by Jiangsu Province, Guangdong Province, Shandong Province and Zhejiang Province. The number of industrial automation enterprises in the western region is relatively small.

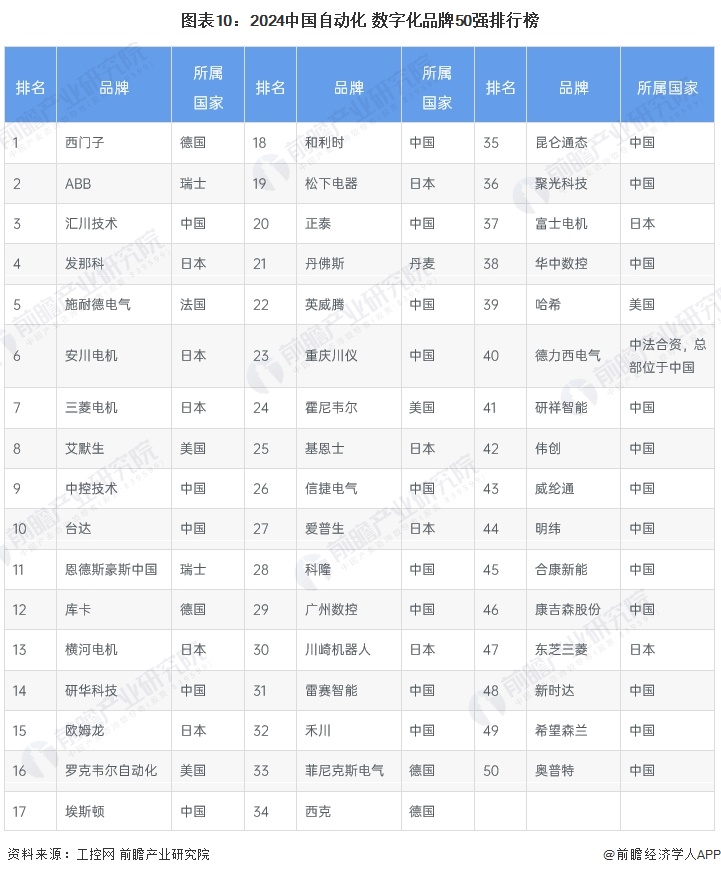

Enterprise competition: European and American brands are firmly in the top position, and domestic brands are catching up

In March 2024, China Industrial Control Network announced the "2024 China Top 50 Automation + Digital Brand Rankings". Compared with the list of the top 50 brands in the previous year, the overall ranking of the 2024 China Top 50 Automation + Digital Brands list has changed significantly, showing that the market competition is becoming more and more fierce, showing a three-legged competition pattern: European and American brands are firmly in the top position, Japanese, South Korean and Taiwanese brands are actively defending the middle and upper positions, and Chinese mainland brands have won more and more market share and user recognition, becoming the largest group in the list.

Industry development prospects and trend forecasts

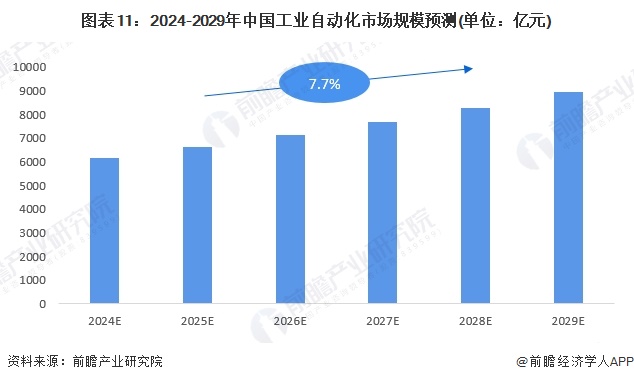

1. The market size will exceed 380 billion yuan in 2029

With the vigorous promotion of the 14th Five-Year Plan for high-quality development and the country's great journey towards Chinese-style modernization, the industrial automation market will continue to flourish. Fast-growing industries such as oil and gas storage and transportation, smart mining, new energy materials, bio-based materials, and robotics have brought new growth to automation products. Technologies such as 5G, industrial Internet, AR, VR, big data, and generative artificial intelligence (AIGC) continue to be introduced and applied to the industrial field, and the obvious enabling effect will attract more industrial enterprises to increase investment, which will greatly promote the demand for intelligent manufacturing that integrates automation, digitalization, and intelligence. It is estimated that by 2029, the scale of China's industrial automation market will exceed 890 billion yuan, with a CAGR of about 7.7% from 2024 to 2029.

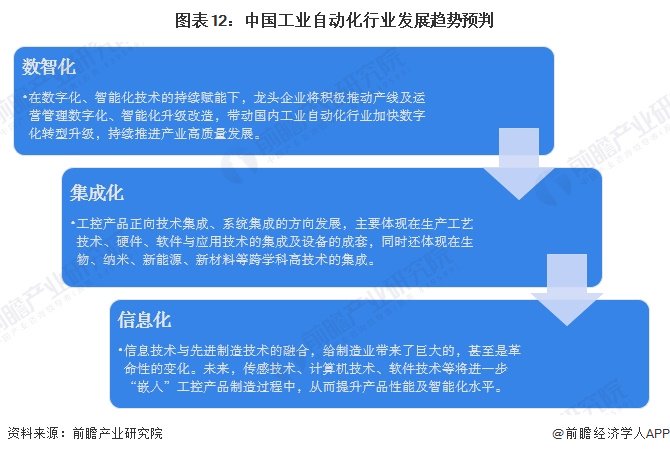

2. Industry trend analysis

With the continuous empowerment of digital and intelligent technology, industrial automation enterprises will actively promote digital transformation, accelerate the construction of smart factories, smart supply chains and other projects, promote the digital and intelligent upgrading of production lines and operation management, and help the high-quality development of the industry. At the same time, industrial automation products will also be further integrated with information technology, and product performance and intelligence level will be further improved.

For more research and analysis of this industry, please refer to the "Global and China Industrial Automation Industry Market Prospect and Investment Strategic Planning Analysis Report" of the Prospective Industry Research Institute

At the same time, the Prospective Industry Research Institute also provides solutions such as industrial new track research, investment feasibility study, industrial planning, park planning, industrial investment, industrial map, industrial big data, smart investment promotion system, industry status certificate, IPO consulting/fundraising feasibility study, specialized and special new small giant declaration, and the 15th Five-Year Plan. If you want to reprint and quote the content of this article, please indicate the source (Qianzhan Industry Research Institute).

More in-depth industry analysis is available in the [Prospective Economist APP], and you can also communicate and interact with 500+ economists/senior industry researchers. More enterprise data, enterprise information, and enterprise development are all in the [Qichamao APP], the most cost-effective and most comprehensive enterprise query platform.

Ticker Name

Percentage Change

Inclusion Date