Author: Su Hang

Producer: Insight IPO

Recently, Guangdong Tianyu Semiconductor Co., Ltd. (hereinafter referred to as "Tianyu Semiconductor") submitted a prospectus to the Hong Kong Stock Exchange to be listed on the main board IPO, with CITIC Securities as its sole sponsor.

As the first domestic and global leading silicon carbide epitaxial wafer manufacturer, Tianyu Semiconductor will experience a decline in performance in the first half of 2024, and will face many problems such as intensified global competition, industry involution, and a significant reduction in procurement by overseas customers.

01

Revenue and gross profit margin declined sharply

Overseas customers reduce procurement

Tianyu Semiconductor is a professional supplier of silicon carbide epitaxial wafers and one of the first third-generation semiconductor companies in China.

As a wide bandgap semiconductor material, silicon carbide (SiC) is more suitable for high-voltage, high-temperature and high-frequency environments than traditional semiconductor materials such as silicon and other traditional semiconductor materials, such as larger bandgap, higher electric field breakdown, higher thermal conductivity, higher electron saturation drift speed and strong radiation resistance.

Epitaxial wafers are made by forming various layers on the surface of the substrate (wafer) to enhance the performance characteristics of the substrate, such as stronger current tolerance, higher voltage tolerance, and operational stability.

Silicon carbide epitaxial wafers are mainly used in the production of various power devices. It will eventually be used in new energy industries (including electric vehicles, photovoltaics, charging piles and energy storage), rail transit and smart grids, general aviation (such as eVTOL) and home appliances.

At present, new energy vehicles are the most prominent application of silicon carbide power devices, and with the development of the domestic new energy vehicle industry, the company's silicon carbide epitaxial wafer sales are rising.

In 2023, Tianyu sold more than 132,000 silicon carbide epitaxial wafers (including the company's self-made epitaxial wafers and epitaxial wafers sold on the basis of foundry services).

At present, in addition to direct sales of silicon carbide epitaxial wafers, Tianyu Semiconductor also provides silicon carbide epitaxial foundry services, epitaxial wafer cleaning services, and substrate and epitaxial wafer testing services.

From 2021 to 2023, Tianyu Semiconductor will achieve operating income of 155 million yuan, 437 million yuan, and 1.171 billion yuan respectively, and the revenue growth rate in 2022 and 2023 will be 182.49% and 168.10% respectively.

The net profit in the same period was -180 million yuan, 2.814 million yuan and 95.882 million yuan respectively.

According to Frost & Sullivan, Tianyu Semiconductor's market share in China's silicon carbide epitaxial wafer market will reach 38.8% (in terms of revenue) and 38.6% (in terms of sales volume) in 2023, ranking first in China's silicon carbide epitaxial wafer industry.

Globally, the company's epitaxial wafer market share in terms of revenue and sales volume is about 15%, ranking among the top three in the world.

However, in the first half of 2024, Tianyu Semiconductor's operating income will be 361 million yuan, a year-on-year decrease of 14.79%; The net profit was -141 million yuan, turning from profit to loss year-on-year.

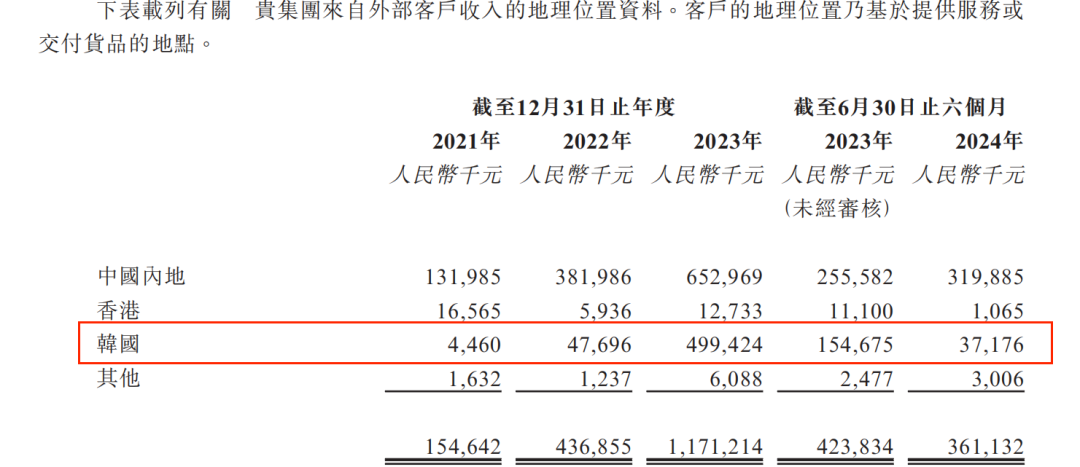

The decline in the first half of 2024 was mainly due to a significant reduction in purchases by a Korean customer in the current period.

According to the prospectus, in 2023, "Customer H", a company established in South Korea in 1998 mainly engaged in the manufacture of diodes, transistors and similar semiconductor devices, will become the largest customer of Tianyu Semiconductor, and the related sales revenue will reach 492 million yuan in 2023, accounting for 42.0% of Tianyu Semiconductor's total revenue.

According to the prospectus, "Customer H" is affected by geopolitical tensions in the semiconductor industry and will no longer buy from the company (as a Chinese manufacturer) in 2024.

During the reporting period, Tianyu Semiconductor's revenue from South Korea was 4.770 million yuan, 47.696 million yuan, 499 million yuan, 155 million yuan and 37.2 million yuan respectively. If revenue from South Korea is excluded, the company's previous revenue growth rate will be greatly reduced.

Image source: Tianyu Semiconductor prospectus

It is worth noting that Tianyu Semiconductor may face a more severe overseas business environment in the future. For example, the United States recently launched a 301 trade investigation on mature process chips (28nm and above) made in China. Tianyu Semiconductor also said that looking ahead, the company may adjust its sales strategy in overseas markets from time to time to adapt to the changing geopolitical situation and seize opportunities in emerging markets.

02

Facing the risk of overall price reduction

Insufficient capacity utilization and still insist on expanding production?

In addition to the reduction in overseas revenue in the future, the overall industry is still facing many difficulties.

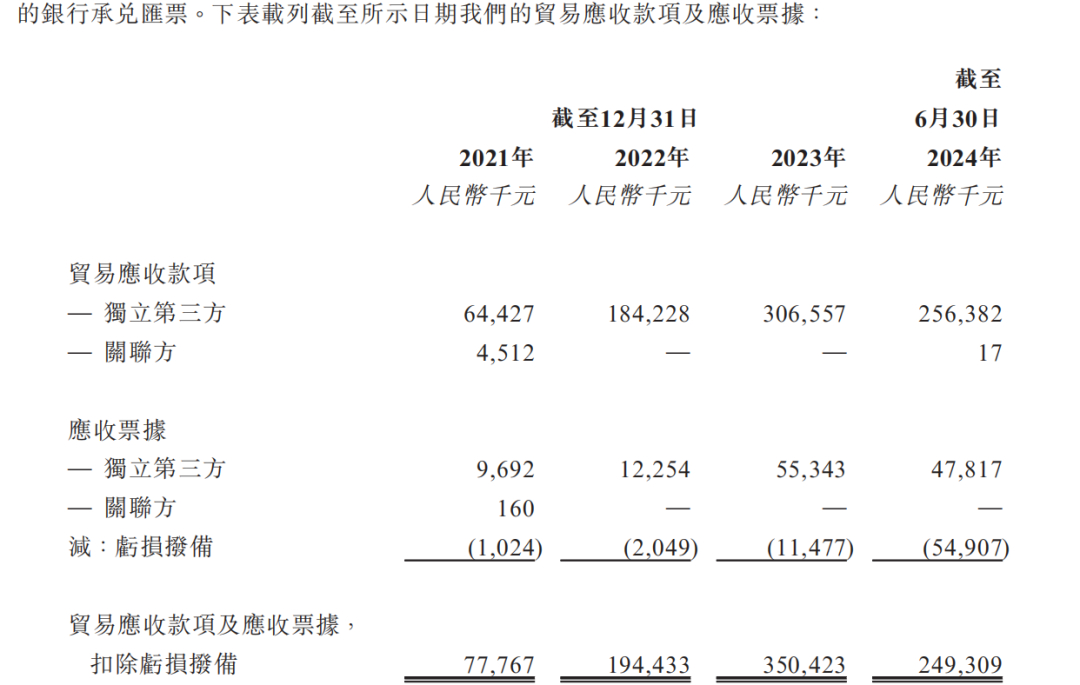

According to the prospectus, during the reporting period, Tianyu Semiconductor's trade receivables and notes receivable were 77.767 million yuan, 194 million yuan, 350 million yuan and 170 million yuan respectively, accounting for 32.76%, 19.54%, 33.47% and 21.37% of the current assets.

During the same period, the provisions for losses were 1.024 million yuan, 2.049 million yuan, 11.477 million yuan and 54.907 million yuan respectively, and the turnover days of trade receivables and notes receivable were 144 days, 115 days, 87 days and 166 days respectively.

Image source: Tianyu Semiconductor prospectus

Tianyu Semiconductor said that the significant increase in loss provisions and the increase in turnover days in 2023 and the first half of 2024 were mainly due to the delay in payment due to the deterioration of operating performance of certain downstream customers.

The global power semiconductor device industry market size has grown from $46.4 billion in 2019 to a total of $47.4 billion in 2023, with a compound annual growth rate of only 0.6%, due to the sharp decline in smartphone sales and the sharp decline in automobile sales due to dealer closures and production line shutdowns.

Among them, the global market size of the silicon carbide power semiconductor device industry has climbed from US$500 million in 2019 to US$2.7 billion in 2023, with a compound annual growth rate of 52.2%, and the penetration rate has increased from 1.1% to 5.8%.

The main reason for the low penetration rate is that the price of silicon carbide-related products is still high, even though the price has been reduced.

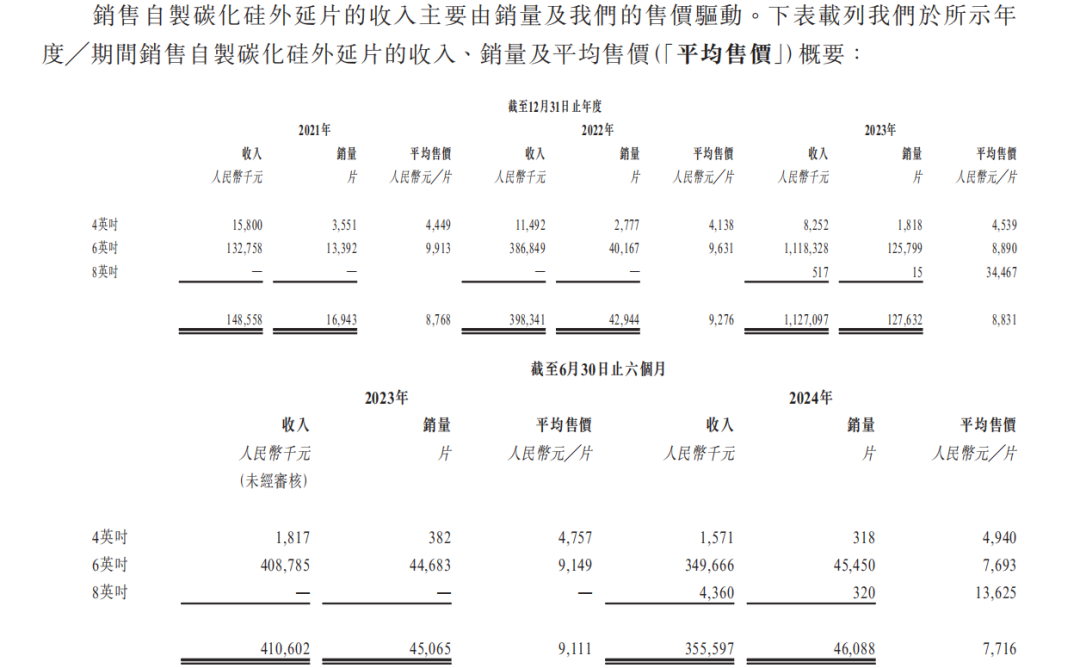

According to the prospectus, from 2021 to 2023 and the first half of 2024, the average selling price of Tianyu Semiconductor's main product 6-inch self-made silicon carbide epitaxial wafer will be 9913 yuan/piece, 9631 yuan/piece, 8890 yuan/piece and 7693 yuan/piece respectively.

Image source: Tianyu Semiconductor prospectus

During the same period, the inventories of Tianyu Semiconductor were 128 million yuan, 134 million yuan, 441 million yuan and 627 million yuan respectively. In view of the decline in the market price of epitaxial wafer products, the inventory write-down (price decline provision) in the first half of 2024 also increased significantly, with 11.051 million yuan, 14.711 million yuan, 21.301 million yuan and 63.006 million yuan respectively during the reporting period.

Affected by the decline in product unit prices and inventory depreciation losses, the gross profit margin of Tianyu Semiconductor has also decreased from 15.7% and 20.0% in 2021 and 2022 to 18.5% in 2023.

In the first half of 2024, the gross profit margin of Tianyu Semiconductor will decline from positive to negative to -12.1%. During the reporting period, the gross profit margins of its main products, 6-inch self-made silicon carbide epitaxial wafers, were 23.3%, 23.7%, 20.0% and 5.7% respectively.

More critically, the industrial chain has begun to prepare for a new round of price reductions.

On September 18, 2024, silicon carbide substrate material manufacturer Tianyue Advanced (688234. Zong Yanmin, chairman and general manager of SH), said at the performance briefing that the price of silicon carbide substrates has declined, on the one hand, due to the improvement of technology and the scale effect to promote the cost reduction; On the other hand, the current price of silicon carbide substrates is higher than that of silicon substrates, and the price decline will help downstream applications expand.

"Similar to other semiconductor materials, at present, leading companies at home and abroad will comprehensively consider pricing strategies according to market conditions, their own products, specific customers and other factors, and some new participants will also obtain the market through price reduction, which is in line with the law of industry development."

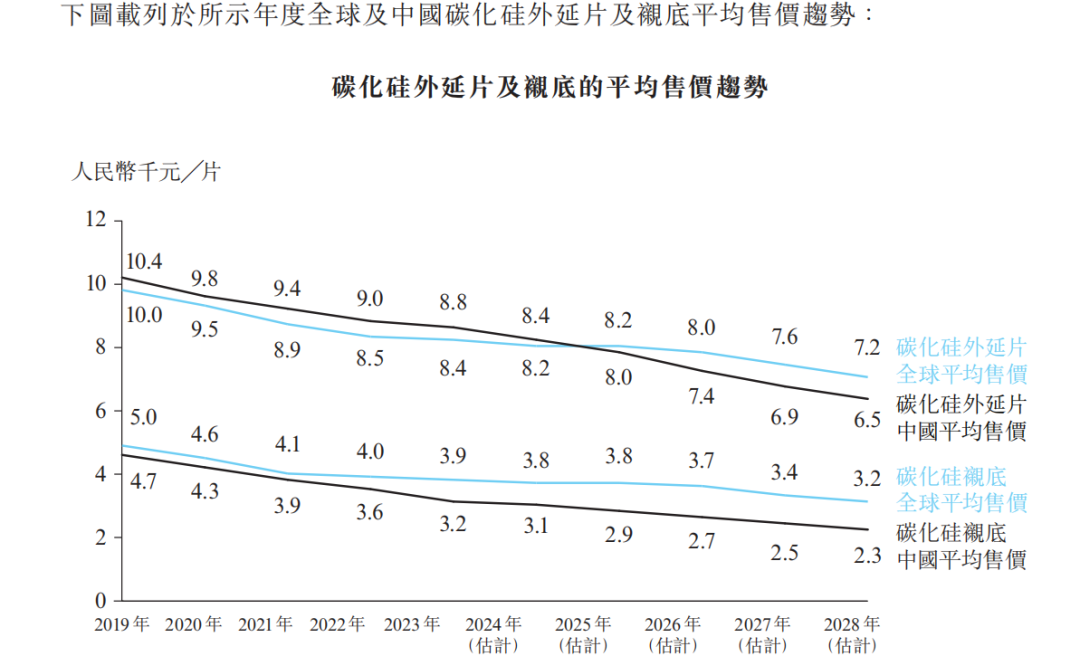

Tianyu Semiconductor said in the prospectus that it is expected that in the near future, the value chain of China's silicon carbide epitaxial wafer industry will be more mature than the global market, and the price of substrates will continue to decline, so it is expected that after 2025, the average selling price of China's silicon carbide epitaxial wafers will decline faster than the global average selling price.

The average selling price of silicon carbide epitaxial wafers in China will be about 8,800 yuan per piece in 2023 and is expected to drop significantly to 6,500 yuan by 2028.

Image source: Tianyu Semiconductor prospectus

TheSpatial proposes strategies to increase gross margins by focusing on high-value products for advanced applications, improving production efficiency, expanding production capacity to achieve economies of scale, and leveraging innovative technologies such as large-scale silicon carbide epitaxial wafers and advanced epitaxial technologies. and vertical integration and market diversification into emerging industries to further capture value and maintain profitability.

In this listing, Tianyu Semiconductor also plans to use the raised funds to expand its overall production capacity, strategic investment and acquisition. The Company expects to increase the annual planned production capacity of approximately 380,000 pieces of silicon carbide epitaxial wafers by 2025, bringing the company's total annual production capacity to approximately 800,000 pieces of silicon carbide epitaxial wafers.

However, the capacity utilization rate of Tianyu Semiconductor has decreased from 56.5%, 89.7%, and 82.6% from 2021 to 2023 to 32.0% in the first half of 2024.

03

The investment institution clears the position before submitting the statement, and the controlling shareholder takes over

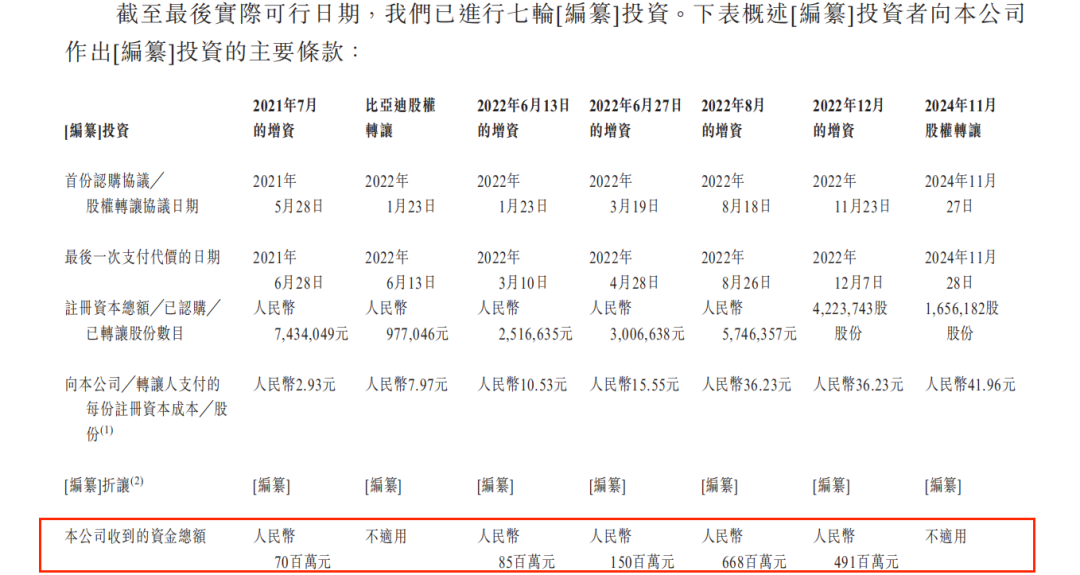

Tianyu Semiconductor has previously attracted intensive investment from investment institutions.

According to the prospectus, in just two years from 2021 to 2022, the company has carried out 5 rounds of capital increase and 1 equity transfer, with a total financing amount of about 1.461 billion yuan. Participating institutions include Huawei Hubble, BYD, Shangqi Capital, Haier Capital, Chendao Capital, China-Belgium Fund, Enthusiast Capital, Zhongguang Investment, Liwan Venture Capital, Fupu Investment, Chunyang Capital, China Merchants Capital, Yueke Xintai Equity Investment Fund, Nanchang Industrial Investment, etc.

Image source: Tianyu Semiconductor prospectus

It is worth noting that in November 2024, shortly before the submission of the prospectus, China Merchants Jianghai and Zhaohua Zhaose, both subsidiaries of China Merchants Securities, transferred all 0.2280% and 0.2280% of the company's shares held by them to Runfu Investment and withdrew from the ranks of shareholders, with a consideration of 34.75 million yuan, which is about 4.75 million yuan higher than the profit when they bought shares in 2022.

Runfu Investment is one of the controlling shareholders of the company, and the partners are all employees and former employees of the company. Therefore, although it is not explicitly stated in the prospectus, the above transfer is more like a repurchase of the company's employee stock ownership platform. In this share transfer, in terms of pricing per share, the company's valuation is about 15.24 billion yuan.

Among the 39 partners of Runfu Investment, 5 partners (i.e. Li Xiguang, Ouyang Zhong, Yin Xuefang, Han Jingrui and Li Zhuoxing) are directors, supervisors or senior management of Tianyu Semiconductor, holding a total of 83.82% of the partnership interest.

Among them, Li Xiguang is one of the founders, chairman, executive director and one of the controlling shareholders of the group. Lee Cheuk-sing, the nephew of Lee Seok-kwong, joined the Company as a Securities Commissioner after obtaining a Bachelor of Commerce degree from the Australian National University in July 2021 and has been appointed as the Secretary of the Board of Directors of the Company since December 2022 at the age of 26.

Ticker Name

Percentage Change

Inclusion Date