Recently, the network security leader Qianxin (688561.SH) released its 2024 performance report, and the company's revenue not only declined, but also suffered losses again.

Securities Star noted that since its listing in 2020, the company has been in a state of loss for a long time, and the cumulative loss after deducting non-net profit has exceeded 3.3 billion yuan. Further research found that high R&D investment and high marketing were the main reasons for the company's previous losses. Although since 2024, the company has tried to improve its operating conditions through expense control and marketing reforms, but it has not been able to save the loss.

Not only that, because the company's main income comes from large government and enterprise customers, its accounts receivable remain high, and its own hematopoietic situation is not optimistic, and the net cash flow generated by operating activities has not turned positive so far.

Accounts receivable are high, and hematopoietic capacity is worrisome

According to public information, Qianxin focuses on the cyberspace security market, mainly providing a new generation of enterprise-level network security products and services to government, enterprises and institutions, and the main products are network security products, network security services, hardware and others.

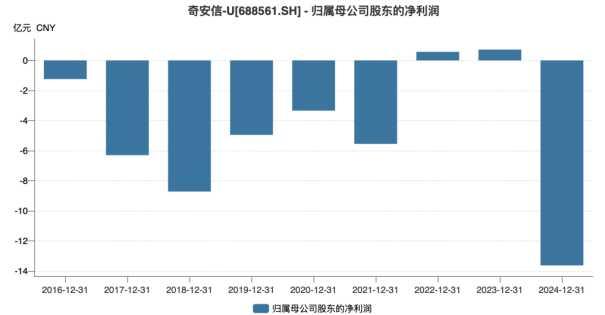

According to the 2024 performance report, the company achieved a total operating income of 4.355 billion yuan, a year-on-year decrease of 32%; The net loss attributable to the parent company was 1.363 billion yuan, turning from profit to loss year-on-year, and the net loss attributable to the parent company was 1.596 billion yuan, which aggravated the year-on-year loss. After calculation, the company's revenue in Q4 was 1.644 billion yuan, down 40% year-on-year, and it has declined year-on-year for six consecutive quarters, and the net profit attributable to the parent company was -187 million yuan, a year-on-year profit turned into a loss, and there was a loss for four consecutive quarters.

The

performance express report mentioned that the decline in Qianxin's revenue was mainly related to the general reduction of the customer's budget and the reform of the company's marketing system.

From the industry level, Qianxin's revenue mainly comes from large government and enterprise customers. In the first half of 2024, enterprise-level customers, government customers, and public security and law departments will account for 80.81%, 13.35%, and 5.84% of the main business revenue, respectively.

Since 2024, the company's customers have generally shrunk the size of their cybersecurity budgets, and their spending structure is more inclined to ensure cybersecurity operations. Against this backdrop, the client slowed down the overall progress from project initiation to acceptance quarter by quarter, especially in the fourth quarter; At the same time, the seasonal characteristics of the high proportion of revenue in the fourth quarter of the cybersecurity industry have led to the company's revenue performance in 2024 being significantly lower than expected.

In addition, due to the long payment cycle of the company's government and enterprise customers, Qianxin's accounts receivable have increased year by year, from 1.859 billion yuan in 2020 to 6.252 billion yuan in 2023, and the proportion of total assets will increase from 15% in that year to 38% in 2023. As of September 30, 2024, the company's accounts receivable was 6.293 billion yuan, accounting for 43% of total assets.

Due to the continuous rise in accounts receivable, Qianxin's own hematopoietic capacity is not optimistic, and the net cash flow generated by its operating activities has been negative for a long time. From 2020 to 2023, the company's indicators will be -689 million yuan, -1.302 billion yuan, -1.261 billion yuan, and -778 million yuan respectively.

In order to improve the quality of income and the quality of payment, the company has carried out a series of reforms in the marketing system. It is understood that since 2024, the company has adjusted the mechanism to promote the shortest path to signing, encourage core customers to sign directly with the company, and encourage non-direct signing projects to sign contracts with general distributors. According to the performance report, the company's net operating cash flow in 2024 will be about -340 million yuan, an improvement of about 440 million yuan year-on-year, but the adjustment has affected the company's revenue scale to a certain extent.

It is difficult to raise net profit for fee control, and the non-cumulative loss exceeds 3 billion

In terms of profitability, before the listing, Qianxin was in a state of loss for a long time, and since it landed on the Science and Technology Innovation Board in July 2020, the company has only maintained profitability in 2022 and 2023. Not only that, after listing, the company's non-net profit has been negative, and it has lost more than 3.3 billion yuan so far.

Qianxin mentioned in the financial report of previous years that the main reason for the company's continuous losses is the choice of a development model with high R&D investment.

Securities Star noted that before 2021, the company's R&D expenses increased year by year, from 541 million yuan in 2017 to 1.748 billion yuan in 2021, and the R&D expense ratio remained above 20%.

It is worth noting that the company's R&D expenses have also increased along with sales expenses and management expenses, which increased from 431 million yuan in 2017 to 1.761 billion yuan in 2021, catching up with R&D expenses in 2019, and the company's management expenses also increased from 232 million yuan in that year to 652 million yuan in 2021. The high cost of the three fees has always been the "pain point" of Qianxin's financial report.

Since 2022, the company has successively reduced its investment in R&D expenses, administrative expenses, and sales expenses. According to the third quarter report of 2024, the company's R&D expenses, management expenses and sales expenses were 1.039 billion yuan, 395 million yuan and 1.175 billion yuan respectively, down 20.47%, 16.76% and 29.17% year-on-year respectively.

Compared with peers, taking the sales expense rate as an example, Qianxin's sales expense ratio in the first three quarters of 2024 is 43%, which is higher than Sangfor's 41%, Venustech's 33% and Shanshi's 38%.

Not only that, but the reduction in the above three expenses did not change the company's loss in 2024. Qianxin admitted frankly in the performance express report that although the company will strictly implement the cost control in 2024, and the total amount of the three fees will drop by about 500 million yuan year-on-year, due to the unexpected fluctuations in the revenue side, the proportion of the company's three fees in revenue has increased year-on-year. At the same time, due to the company's inaccurate and timely market insight and response to the short-term demand changes of the government and some industry customers, it also affects the input-output efficiency of resources to a certain extent.

In addition, the company's overall gross profit margin in 2024 decreased from the same period last year due to factors such as intensified competition in the industry and an increase in the proportion of network security service revenue. At the same time, the company has strategically abandoned some projects with high gross profit margins but poor payment expectations, which together led to the company's losses.

The subsidiary was exposed to violations again and was banned for 3 years

Since 2024, Qianxin's subsidiary, Qianxin NetGod Information Technology (Beijing) Co., Ltd. (hereinafter referred to as Qianxin, NetGod), has been notified several times for violations.

On January 13, 2025, Fujian Mobile issued an "Announcement on the Results of the Handling of Negative Behaviors of Qianxin NetGod Information Technology (Beijing) Co., Ltd.", which stated that Qianxin NetGod violated the regulations in the bidding for the procurement project of the network security vulnerability management platform, and announced that it would prohibit cooperation with Qianxin NetGod for three years on other management software projects from the date of the announcement.

According to the data, Qianxin NetGod is an important non-wholly-owned subsidiary of Qianxin, with a shareholding ratio of 99.929%, and the company mainly provides security products, security management and security services. It is understood that Qianxin NetGod, as the main body of foreign business cooperation under Qianxin, has won many projects related to network security protection and system security support of operators.

According to the 2024 semi-annual report, Qianxin's revenue was 1.613 billion yuan, accounting for 90% of Qianxin's total revenue during the reporting period. The three-year ban will also have a negative impact on its business development to a certain extent.

Securities Star noted that this is not the first time that Qianxin NetGod has been notified. On August 27 last year, China Mobile (Hangzhou) Information Technology Co., Ltd., a subsidiary of China Mobile, also pointed out in the announcement that Qi'anxin NetGod was prohibited from participating in the 2024-2026 convergence enterprise gateway security audit service procurement project for 3 years.

In addition, on March 21, 2024, Huaneng Lancang River Hydropower Co., Ltd. announced that Qianxin NetGod had more serious bad behaviors and recommended that it be blacklisted for 1 year. (This article was first published by Securities Star, written by Li Ruohan).

$Qianxin-U(688561).

Ticker Name

Percentage Change

Inclusion Date