Source: Under the Sycamore Tree V Text/West Wind

On the evening of March 7, the Beijing Stock Exchange announced its decision to terminate the review of the IPO of Changzhou Jinkang Seiko (831978). Changzhou Jinkang Seiko was approved by the Listing Committee of the Beijing Stock Exchange on January 25, 2024, but it has not been able to submit for registration until it was terminated for review. The sponsor of the company's IPO is Northeast Securities. The author noted that the non-net profit deducted by the four comparable companies in the same industry listed by the company in 2024 will all decline sharply year-on-year.

1. The two actual controllers control 96.65% of the voting rights of the company's shares in total

The predecessor of the company, Co., Ltd., was established in October 2001 and changed to a joint-stock company in July 2014. On February 17, 2015, the company's shares were listed on the New Third Board. The company currently has a registered capital of 55.08 million yuan. The controlling shareholders and actual controllers of the company are Zhong Renkang and Wan Yijin. Zhong Renkang and Wan Yijin currently hold 43.64% of the company's total share capital. The two hold a total of 87.28% of the equity of the issuer, and control the voting rights of a total of 9.37% of the shares of the issuer directly held by Changzhou Yiren, Zhong Huili, Wan Li and Zhong Lixin through a concerted action agreement, and the two together control 96.65% of the voting rights of the issuer's shares. Mr. Zhong Renkang, born in September 1969, is currently the chairman of the company. Wan Yijin was born in December 1947 and is currently a director of the company.

In addition, Zhong Huili, the person acting in concert, is the executive partner of Changzhou Yiren, a shareholder of the issuer, and has a father-daughter relationship with Zhong Renkang, and Wan Li and director Wan Yijin have a father-daughter relationship.

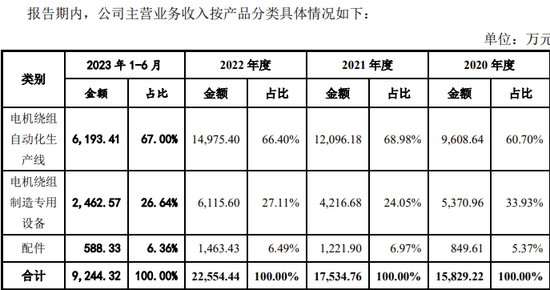

2. The company is an overall solution provider of special equipment for motor winding manufacturing

The company is a total solution provider of special equipment for motor winding manufacturing, mainly engaged in the research and development, production and sales of motor winding automatic production lines and high-end equipment, with advanced capabilities in the design and production of a full set of motor manufacturing equipment and automated motor equipment production lines from winding to final forming, and its technology and products are widely used in new energy vehicle motors, industrial motors, household motors and other fields.

The company has won the honors and recognition of high-tech enterprises, Jiangsu Province Micro Motor Winding and Embedding Automation Equipment Engineering Technology Research Center, Jiangsu Province Specialized and Special New Small and Medium-sized Enterprises, Jiangsu Province Service-oriented Manufacturing Demonstration Enterprises, Jiangsu Province Private Technology Enterprises, Jiangsu Province Enterprise Technology Center, and the Fifth Batch of National Specialized and New "Little Giant" Enterprises The project has been supported by the special fund for the transformation of scientific and technological achievements in Jiangsu Province, and the project products have been recognized by the Jiangsu Provincial Economic and Information Technology Commission as the first (set) major equipment product in Jiangsu Province and a specialized and special new product in Jiangsu Province.

In the field of industrial motors, the company has become an important supplier of special equipment for motor winding manufacturing from major manufacturers in the field of domestic industrial motors (such as Siemens Motors, Huali Motors, Dazhong Motors, Jiangte Motors, Lu'an Jianghuai Motors, etc.) and major manufacturers in the field of new energy vehicle drive motors (such as Shanghai Electric Drive, Wolong Electric Drive, BYD Automobile, etc.).

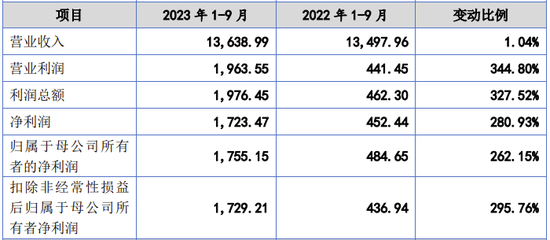

3. In 2022, the non-net profit will be 31.17 million yuan, and the revenue from January to September 2023 will increase by 1% year-on-year, but the non-net profit will increase by 295% year-on-year

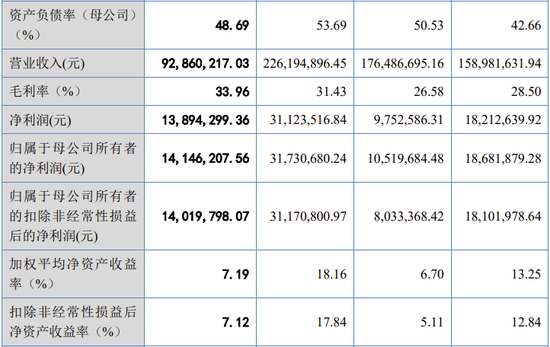

In 2020, 2021 and 2022, the company will achieve operating income of 158.98 million yuan, 176.49 million yuan and 226.19 million yuan respectively, and the net profit deducted from non-attributable to the parent company will be 18.1 million yuan, 8.03 million yuan and 31.17 million yuan respectively.

The reviewed financial data from January to September 2023 shows that from January to September 2023, the company's operating income increased by 1.04% year-on-year, but the net profit after deducting non-attributable to the parent company was 17.29 million yuan, a year-on-year increase of 295.76%.

The prospectus explains: The company's net profit attributable to the parent company from January to September 2023 is higher than the growth rate of operating income, which is mainly affected by the increase in gross profit margin from January to September 2023. From January to September 2023, the gross profit margin increased from 26.78% to 36.43%, mainly due to the decrease in large loss-making orders. From January to September 2022 and from January to September 2023, the issuer's loss-making orders of more than 2 million yuan amounted to 19.6009 million yuan and 2.2425 million yuan respectively, accounting for 14.52% and 1.64% of the current operating income respectively, and the gross profit margin was -12.85% and -0.29% respectively, and the reduction of large loss-making orders increased the issuer's gross profit margin from January to September 2023. Affected by the increase in gross profit margin from January to September 2023, the company's net profit growth rate from January to September 2023 was higher than the growth rate of operating income.

The specific listing criteria selected by the issuer are the first criterion of Article 2.1.3 of the Rules Governing the Listing of Stocks on the Beijing Stock Exchange (for Trial Implementation): "The expected market capitalization shall not be less than 200 million yuan, and the net profit in the last two years shall not be less than 15 million yuan and the weighted average return on equity shall not be less than 8%, or the net profit in the most recent year shall not be less than 25 million yuan and the weighted average return on equity shall not be less than 8%. ”

4. The company plans to raise 118.88 million yuan for a fund-raising project, and the necessity is the focus of the listing committee meeting

The company plans to raise a net amount of 118.88 million yuan, all of which will be used for the motor special equipment manufacturing project (phase II). The construction period of the project is 24 months.

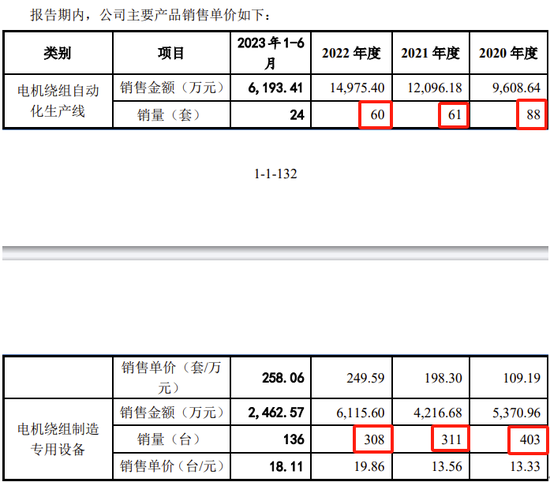

This project plans to improve the production capacity of special manufacturing equipment for motors and solve the contradiction of insufficient production capacity by building a new production base and introducing advanced production equipment and software systems. After the project is completed and put into production, it is expected to achieve an annual production capacity of 235 sets (sets) of special equipment for motor winding manufacturing (including 55 automatic production lines).

However, in 2020, 2021, and 2022, the number of sales of motor winding automation production lines will be 88 sets, 61 sets, and 60 sets, respectively, and the sales of special equipment for motor winding manufacturing will be 403 sets, 311 sets, and 308 sets, respectively, all of which will continue to decline.

At the meeting of the Listing Committee on January 25, 2014, the Listing Committee deliberated on the necessity of the fundraising project and the feasibility of capacity digestion. The issuer is requested to explain the necessity of adding 235 units (sets) to the fund-raising project under the condition of the decline in the output and sales volume of major products during the reporting period, and whether the specific measures and related measures for the digestion of the fund-raising and investment capacity are feasible.

5. The non-net profit deducted by 4 comparable companies in the same industry will decline sharply year-on-year in 2024, and 1 comparable company listed on the New Third Board will decrease by 50% year-on-year from January to June 2024

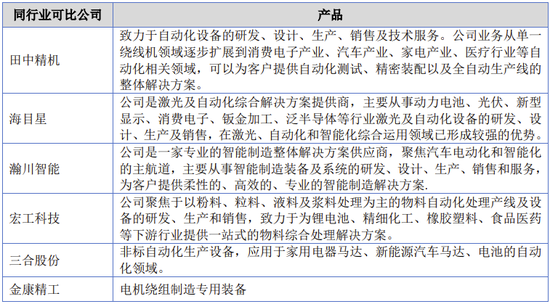

The company's latest results are for January-September 2023. However, judging from the timing of the withdrawal of the declaration, it is estimated that the performance will be poor in 2024. Let's take the 2024 performance of comparable companies in the same industry listed in the prospectus for reference. The company listed five companies, including Tanaka Seiki (300461), Hymson (688559), Hanchuan Intelligent (688022), Honggong Technology (GEM IPO application enterprise), and Sanhe Co., Ltd. (871097), as comparable companies in the same industry.

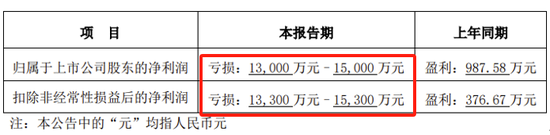

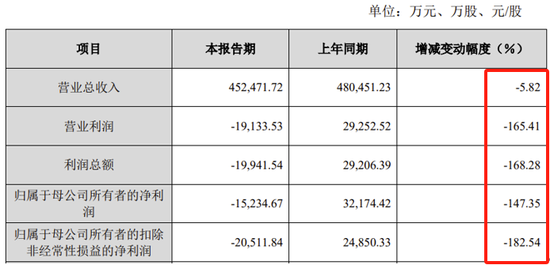

According to Tanaka Seiki's 2024 annual performance forecast, the company's net profit deducted from non-attributable to the parent in 2024 will be a loss of 133 million yuan to 153 million yuan, while its profit in 2023 will be 3.77 million yuan.

According to the announcement of the 2024 annual performance express report, Hymson will deduct the net profit of non-attributable to the parent company in 2024 to -205.12 million yuan, a year-on-year decrease of 182.54%.

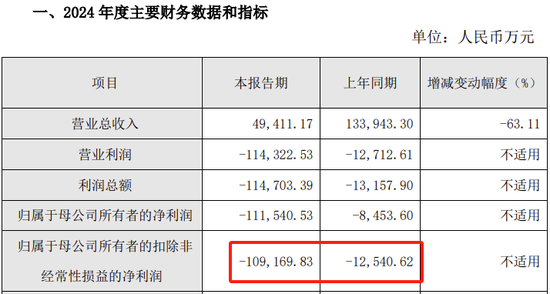

According to the performance express announcement, Hanchuan Intelligence's operating income in 2024 will decrease by 63.11% year-on-year, and the net profit deducted from non-attributable to the parent will be -1.092 billion yuan, a year-on-year decrease of 770.57%.

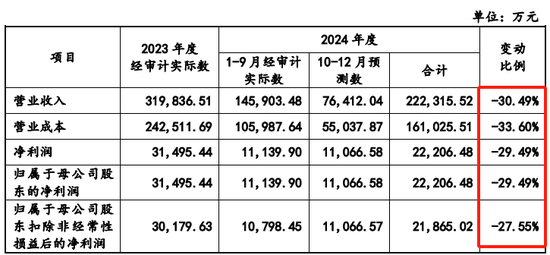

According to the prospectus (registration draft) released by Honggong Technology on December 16, 2024, according to the audited actual figures from January to September 2024, Honggong Technology predicts that the annual operating income in 2024 will decrease by 30.49% year-on-year, and the net profit deducted from non-attributable to the parent company will decrease by 27.55% year-on-year.

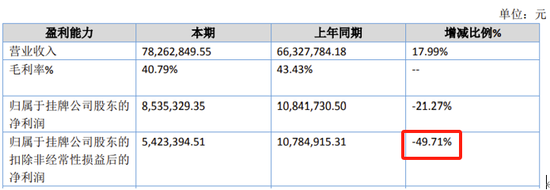

Sanhe Co., Ltd. is a company listed on the New Third Board, and it is not required to publish the third quarterly report according to the regulations, and only the 2024 interim report has been announced. From January to June 2024, Sanhe Co., Ltd. achieved a net profit of 5.42 million yuan after deducting non-attributable to the parent company, a year-on-year decrease of 49.71%.

The 2024 annual performance of 5 companies in the same industry is a sharp year-on-year decline, and the issuer's performance in 2024 is likely to be bad, which should be the main reason why the company has to withdraw its declaration.

6. The main issues raised by the Listing Committee meeting on the company's deliberation opinions and deliberation meetings

(i) Deliberations

1. The issuer is requested to further comprehensively analyze and simulate the impact on the issuer's operating performance in each period in combination with the proportion of bad debts accrued for accounts receivable of comparable companies in the same industry, the adequacy of the provision for inventory decline at the end of each period, and the outsourcing processing of related parties, explain the specific basis and reasonableness of the conversion of construction in progress, the impact of the relocation of business premises, depreciation and capacity digestion of fund-raising projects on the issuer's operating performance after the period, and explain whether the relevant risk disclosure is sufficient. Please ask the sponsor institution and the reporting accountant to check and give a clear opinion.

2. The issuer is requested to disclose the specific distribution of orders in hand at the end of the period, the relevant orders of the IE5 energy efficiency motor production line, the market competition pattern of the IE5 energy efficiency motor production line and the competitive advantage of the issuer.

(ii) Review the main questions posed by the Conference

1. About business performance. Issuers are requested to: (1) explain whether the relevant revenue recognition of the trader customers is compliant, and the reasons and reasonableness of the gross profit margin of the trader customer being higher than the gross profit margin of the manufacturer's customer, taking into account the type, amount, gross profit margin of the products sold to the trader, and the agreement and specific implementation of the contract terms related to installation, commissioning, acceptance and payment with the trader's customer and its end customers. (2) Combined with the situation of the same industry, the overdue accounts receivable at the end of each period, and the latest collection after the period, explain the reasons for the large accounts receivable at the end of each period, whether it is in line with industry practice, whether there is a situation where the credit policy is relaxed to stimulate sales, and whether the provision for bad debts in each period of the reporting period is sufficient. (3) Explain whether there is a long-term uncarried cost based on the establishment of the internal control management system for the issued commodities, the commodities issued at the end of each period of the reporting period, the inventory commodities, the order coverage of the products, the cost carry-over and the revenue recognition after the period. (4) Calculate in detail the impact of the overall relocation of the issuer's business premises on the company's costs and operating results based on the consolidation of the construction in progress and the impact on the company's operating results after all the conversion, explain whether there is a material adverse impact on the issuer's ability to continue operations, and make full risk disclosure. (5) Explain the reasonableness of the low production and sales rate and the significant increase in the inventory at the end of the period in 2021, combined with the average cycle of products from procurement, production to installation and commissioning, explain the reasonableness of the revenue recognition in 2021 concentrated in the fourth quarter, whether there is a situation of revenue recognition in advance, and further explain the reasons for the inconsistent trend of revenue and net profit changes in 2021.

2. On the necessity and reasonableness of related party transactions. The issuer is requested to: (1) explain the pricing method and basis of the related party transactions between the above-mentioned companies and the issuer in combination with the actual operation of Changzhou Xianda Machinery Co., Ltd. and Changzhou Jieying Machinery Co., Ltd. since their establishment, the source of personnel composition and the method of obtaining remuneration, the provisions of the company's articles of association, the verification of funds with their related parties, and the fair market price of comparable products of the same type, the price of the third party market, the price of related parties and other trading parties, etc., and whether the pricing method and basis of the related party transactions between the above-mentioned companies and the issuer are actually controlled by the issuer; Whether the business mainly relies on the issuer, whether there are other benefit arrangements or agreements other than the distribution contract, whether there is any use of related party transactions to transfer costs and disbursement fees, and whether the relevant transactions have fulfilled the procedures for review and disclosure of related party transactions. (2) Explain whether the issuer and its actual controllers, directors, supervisors, senior management and employees have abnormal capital transactions with the above-mentioned related parties and their actual controllers. (3) Combined with the situation of comparable companies in the same industry, explain the matching relationship between fixed assets and production scale, how the issuer copes with the growth of order scale when the capacity utilization rate is saturated in the reporting period, and the selection criteria and quality control measures of outsourcing manufacturers; In addition to Changzhou Xianda Machinery Co., Ltd. and Changzhou Jieying Machinery, whether the outsourcing manufacturers have not yet disclosed related parties.

3. On the necessity of fundraising projects and the feasibility of capacity digestion. The issuer is requested to explain the necessity of adding 235 units (sets) to the fund-raising project under the condition of the decline in the output and sales volume of major products during the reporting period, and whether the specific measures and related measures for the digestion of the fund-raising and investment capacity are feasible.

Sina Statement: This news is reprinted from Sina's cooperative media, and the publication of this article on Sina.com is for the purpose of conveying more information, which does not mean that it agrees with its views or confirms its description. The content of this article is for informational purposes only and does not constitute investment advice. Investors act accordingly at their own risk.

Ticker Name

Percentage Change

Inclusion Date