Source: Talent Business

The computing power sector is ebbing! Why is the demand logic of computing chips still there?

Recently, the sentiment of "excess computing power" in the market is flying all over the sky, but there are still subdivisions that are performing strongly!

The bearish sentiment of the AIDC concept plate has gradually spread, and the reasons have been analyzed in the previous article: one is that the early rise is too high, and the market believes that some of the targets have been detached from the fundamentals, and the valuation of the targets is high in the short term, which needs to be supported by annual reports and quarterly reports; The other is that the market did not wait for enough catalysts to boost the sentiment of the sector, but waited for the bearish. Last week, Goldman Sachs and Ali Tsai Chongxin's negative views on computing power construction ignited the bears, in fact, some of the funds began to flee quietly as early as Nvidia's GTC conference and Tencent's conservative capital expenditure budget on the computing power side in 2025. Then the continuous plunge of the U.S. stock Nvidia (NVDA.O) also brought down the A-share computing power sector, of course, the "Nvidia Chain" bore the brunt, even if some individual stocks had good annual reports and quarterly results, they were not spared.

However, at the other end of the computing power sector, domestic ASICs are ushering in new opportunities.

01

The computing power sector is out of steam? Computing power chips are the priority demand!

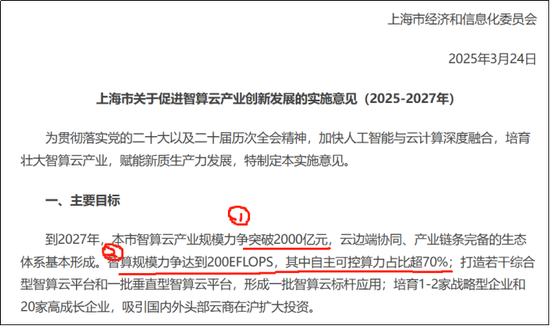

Last Wednesday, a piece of news attracted market attention after hours. Shanghai issued the "Implementation Opinions of Shanghai Municipality on Promoting the Innovation and Development of the Intelligent Computing Cloud Industry (2025-2027)", which proposes that by 2027, the scale of the city's intelligent computing cloud industry will strive to exceed 200 billion yuan, and an ecosystem with cloud-edge-end collaboration and a complete industrial chain will be basically formed, and the scale of intelligent computing will strive to reach 200EFLOPS, of which independent and controllable computing power will account for more than 70%.

There are two important concerns here: one is that by 2027, the scale of Shanghai's intelligent computing cloud industry is planned to exceed 200 billion yuan; The other is that the scale of intelligent computing is planned to reach 200EFLOPS, and its Chinese computing power accounts for more than 70%; According to statistics, by the end of 2024, the nationwide intelligent computing scale of telecom and mobile will be 35EFLOPS and 29EFLOPS respectively); In fact, at the end of 2024, Shanghai issued the "Implementation Plan on Artificial Intelligence "Molding Shencheng"", which proposed: by the end of 2025, the scale of intelligent computing power in the city will exceed 100EFLOPS, and the use of domestic computing chips in the city's new intelligent computing center will account for more than 50%. The unexpected aspect is that the scale of computing power in this scheme has doubled to 200EFLOPS compared with the previous stage; Last year, the use of domestic computing chips accounted for 50%, and this year it has increased to 70%.

Here is a rough calculation, according to the current domestic manufacturers mainly rush to buy Nvidia H20 computing power card, H20 FP16 peak computing power is 148Tflops, and 200EFlops = 200 million Tflops, then the corresponding total demand is about 1.35 million, and the current market H20 single card price is about 130,000 yuan, according to this price, to meet the demand of 200EFlops, the demand value of H20 is about 175.5 billionOf course, this is the ideal state, the higher the demand, the more expensive the price, it stands to reason that the price of H20 may be higher than 130,000. So if 70% of the computing power chips required by Shanghai are completed by domestic production, then the corresponding market share will be about 122.8 billion, which is only the demand of Shanghai.

Domestic substitution is one thing, on the other hand, Nvidia's H20 is likely to gradually withdraw from the domestic market. In July last year, the market had already expected this. On July 3, 2024, the National Development and Reform Commission and other departments issued a notice on the "Special Action Plan for Green and Low-Carbon Development of Data Centers", which put forward clear requirements for computing power energy consumption: new and renovated and expanded data centers should adopt advanced energy efficiency and energy-saving levels of energy efficiency general-purpose graphics processors, with a computing power of 14nm+ chips ≥ 0.25TFlops/W, and a computing power of less than 14nm chips ≥ 0.5TFlops/W. However, according to calculations, the energy efficiency computing power of H20 units below 14nm is only 0.37TFlops/W (148/400W), which is far lower than the specified requirement of 0.5TFlops/W.

It can be seen that this time it is not the ban on the sale of H20 on the other side of the ocean, but we take the initiative to give up this "castrated" product. Although the implementation is not so strict, according to the "plan", new construction and expansion by the end of 2025 must be in accordance with this standard. This is undoubtedly a long-term benefit to domestic computing chips.

At present, the confidence and urgency of domestic computing power chips are constantly improving, and the emergence of Deepseek in the early stage has allowed many domestic low-end computing chips to come in handy. The next day, the A-share market also gave a certain reaction, and last Thursday there was a rebound in the domestic ASIC concept sector, among which VeriSilicon (688521. SH) hit a new intraday high last Thursday, and the domestic semiconductor sector also saw a rare rise that morning.

From this point of view, Cambrian's revenue is only 1.2 billion, but it can be 10 times in 4 years, and the reason behind VeriSilicon's high valuation even if it loses 1,000 times is actually the helplessness of domestic computing chips.

02

"Hope in the Village" VeriSilicon

VeriSilicon (688521. SH) has recently performed relatively well in the market, and the biggest stimulus may be the demand for self-developed chips from large manufacturers, and I have seen a lot of research records, mainly due to Byte's order of IP and design services from VeriSilicon for ASIC chips.

According to the "grapevine", "the demand scale of bytes is about 2.5 billion, 500,000, and the unit price is 5,000 yuan, which is equivalent to doubling the original business." At present, the front-end design has officially begun, and it is expected to be taped out by the end of the year. The above has not been verified by official information and is not intended for any investment advice.

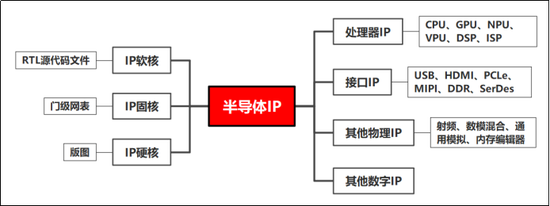

Chip IP is located in the upstream of the chip semiconductor industry chain, with the characteristics of high technical level, high concentration of intellectual property rights, and large commercial value, which is an important foundation for chip design, and IP authorization is similar to the intellectual property copyright of the chip industry. The IP provider licenses the chip IP developed by the IP to the chip design company, and the licensor needs to pay the agreed fee and comply with the relevant terms and restrictions of use. In recent years, subject to overseas monopoly restrictions, such as the aforementioned H20 withdrawal from the domestic computing chip market, the demand for domestic chip substitution has increased significantly.

VeriSilicon was listed on the Science and Technology Innovation Board on August 18, 2020, and the market share of the company's chip IP licensing business in 2023 will be the first in Chinese mainland and the eighth in the world. Although it is among the top 10 in the world, IP nest, Synopsys and ARM still account for more than 60% of the global IP market share, and the global market share of domestic chip IP, including VeriSilicon, is only 1.9%. Of course, the market pays more attention to expectations, and the current low share can bring higher expectations for the continuous penetration of domestic chip IP in the future.

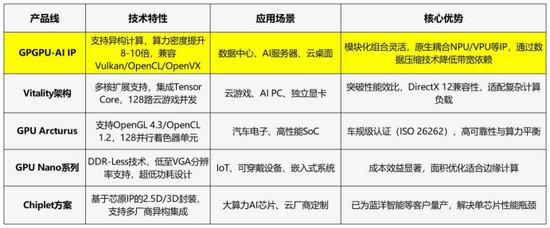

VeriSilicon's products cover the whole field of GPU/NPU/VPU/DSP/ISP. Its business has two main business models: one is the IP licensing of chips; The other is a one-stop chip customization service, that is, ASIC business. As the company's core competitive barrier, the "SiPaaS model" means that downstream customers only need to connect with VeriSilicon to complete the whole process from concept to finished product, which greatly simplifies supply chain management and communication costs. It covers the whole process from chip design to wafer fabrication, packaging and testing, and can also provide system platform solutions.

According to the latest investor relations survey records. VeriSilicon's NPUIP has been adopted in 142 AI chips from 82 customers, covering 10 market segments such as servers, automobiles, smartphones, and wearables. More than 100 million AI chips integrated with VeriSilicon's NPUIP have been shipped worldwide, leading the world in the embedded AI/NPU field. In addition, VeriSilicon's GPUs and GPGPU-AIIP for high-performance AI computing have been licensed multiple times around the world and have been used in many high-performance computing products.

From the perspective of sub-business, compared with chip design and IP fees, VeriSilicon's chip mass production business has developed rapidly, increasing from 656 million in 2020 to 1.207 billion in 2022. 2024 is also a transition period, the recovery of the chip industry is underway under the high demand for automotive electronics and servers, and the market also expects VeriSilicon's performance to gradually recover.

According to the current performance of VeriSilicon, the overall performance is relatively "ugly", but the performance is not the core point of market expectations.

The key is on the technical level. At the beginning of the article, it was analyzed that there will be a large supply and demand gap in domestic AI computing chips, NVIDIA's H20 does not meet the latest energy consumption per unit of computing power, and there is a high probability that it will withdraw from the domestic market after this year, and from the performance of H20, it belongs to the category of GPGPU, which means that domestic GPGPU will fill this gap. What about VeriSilicon's GPGPU technology?

Since there are fewer public sources, it may not be as accurate, and the point is on logic. What is certain at the moment is that there is no perfect replacement for the Nvidia H20 in the short term.

Here is a summary of some VeriSilicon's products so far, for reference only.

Strictly speaking, there is no direct comparison, but there are really not many reference targets, and here is only a rough comparison between VeriSilicon's GPPU-AI IP and NVIDIA's H20 in some aspects. In terms of computing power, the single computing power of GPPU-AI IP can be increased by 8-10 times through multi-cluster expansion and supports multi-core stacking, and the FP16 computing power can reach 16-32 TFLOPS in the server-level solution, but the computing power of FP16 NVIDIA H20 is 148TFLOPS, and the computing power of China is not superior. For more advantages in terms of energy consumption and cost, here are the Vivante 3D GPGPU IP released by the company in 2023.

To addendum: Vivante 3D GPPU IP is the infrastructure of VeriSilicon's GPU IP, based on Vivante's GPU R&D experience, initially positioned as a general-purpose compute acceleration (GPGPU) to support a wide range of scenarios from embedded devices to servers. On this basis, the GPPU-AI IP is an enhanced product line that further integrates AI acceleration modules (such as Tensor Cores) and optimized software stacks to achieve deep integration of GPGPU and AI computing, such as supporting large language models (LLAMA) and AIGC models (such as Stable Diffusion). According to the data, the energy consumption per unit of computing power of Vivante 3D GPGPU IP is 1-3TFlops/W, which has been calculated before H20, and the energy consumption per unit of computing power is 0.37TFlops/W, which is indeed not up to standard.

Moreover, in terms of cost, VeriSilicon's model is to charge a one-time IP licensing fee to reduce customer R&D costs and support small and medium-sized computing power configurations (more cost-effective than full-featured GPUs), which is more affordable to the people. However, the current problem is that GPPU-AI IP is mainly more edge computing, which can support heterogeneous computing after optimizing the structure, while H20 can directly perform high-performance computing, which is obviously not a dimension in the scene.

VeriSilicon's IP solution supports customized configurations from the edge (e.g., single-core 8-10 TFLOPS) to the cloud (multi-core scaling up to 32 TFLOPS), which is more widely adaptable. As a fixed computing power chip, H20 is more suitable for standardized ultra-large data center requirements.

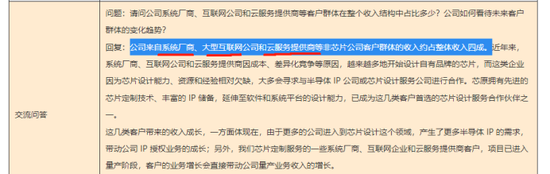

From the perspective of customers, 40% of VeriSilicon's revenue currently comes from non-chip manufacturers, including system vendors, large Internet companies and cloud service providers. In fact, this logic is not difficult to understand, after the emergence of Deepseek, the threshold for the development of large models has been lowered. By optimizing the path, that is, sparse computing, model distillation, etc., DeepSeek reconstructs the proportion of large model training and inference, and the agency infers that the proportion of inference of large models will reach 70% in the future, and the computing power requirements of the inference end for AI chips are not as strict as the training side, which significantly reduces the dependence on high-end GPUs.

Judging from institutional research, VeriSilicon's order volume has also been growing. As of the end of 2024, the company's orders are in good condition, with orders in hand of 2.406 billion yuan, an increase of nearly 13% from 2.138 billion yuan at the end of the third quarter, and orders in hand have remained high for five consecutive quarters. Under the premise that the orders are sufficient, the future transformation into performance will also guarantee the fundamentals.

Ticker Name

Percentage Change

Inclusion Date