Number of words: 2409 words Intensive reading time: 4-10 minutes

On March 17th, BGI Nine Days (301269. SZ) issued a suspension announcement to acquire Xinhe Semiconductor Technology (Shanghai) Co., Ltd. (hereinafter referred to as "Xinhe Semiconductor") by issuing shares and paying cash, and disclosed the transaction plan on March 31.

A few days later, on the 28th, another domestic EDA listed company, Primarius Electronics (688206.SH), issued a suspension announcement to purchase a controlling stake in Chengdu Ruichengxin Micro Technology Co., Ltd. (hereinafter referred to as "Ruichengxin Micro") by issuing shares and paying cash.

The announcement of two blockbuster transactions in the EDA field almost at the same time slowly kicked off the second half of the domestic EDA field, and also allowed us to take a look at the M&A strategic choices of EDA companies.

01

M&A idea 1: Expand single-point EDA tools and build a full-process solution

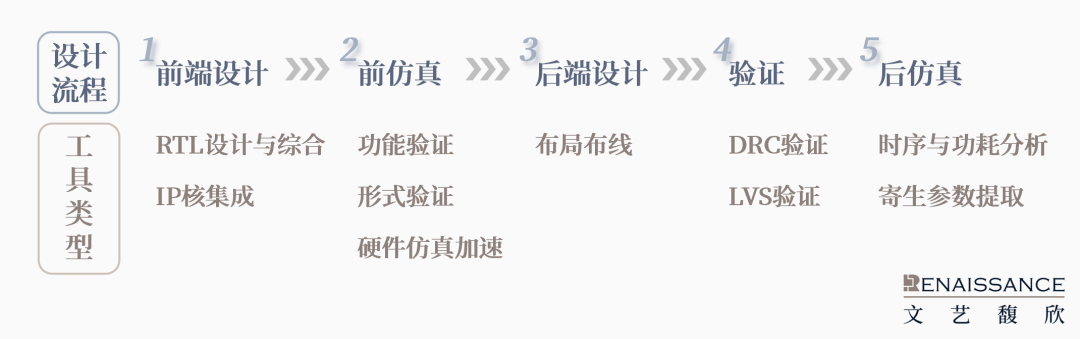

From the perspective of technical architecture, the EDA tool system covers multiple professional nodes, and the technical barriers between each single point tool are significant. A complete chip design process typically includes the following:

As a latecomer to the industry, domestic EDA manufacturers usually follow a clear development path: first develop a single-point tool to quickly enter the market, and then gradually evolve to a full-process tool platform; At the same time, in terms of product layout, it often focuses on the design requirements of specific types of chips first, and then gradually expands to other categories of chips and systems.

As the chip manufacturing process continues to advance, advanced processes are fundamentally reshaping the chip design paradigm. At present, the realization of chip functions is no longer limited to a single design link, but increasingly relies on the systematic collaboration of multiple elements such as chip architecture, packaging technology, and manufacturing process. In this context, the concept of EDA tool R&D is undergoing a key transformation: from the traditional Design-Technology Co-Optimization (DTCO) to a more comprehensive System-Technology Co-Optimization (STCO). This evolution essentially reflects the strategic leap of the industry from single-point optimization to full-process and system-wide collaborative optimization. This evolution has had two impacts: on the one hand, it has led to the emergence of a variety of new technologies and products in the EDA field to address more complex design challenges; On the other hand, there is also a structural shift in end-user needs – they are no longer satisfied with disparate point tools, but urgently need a seamlessly integrated end-to-end solution to ensure consistency and synergy across the process. This dramatically increases the requirements for EDA vendors' full-stack integration capabilities.

At present, the domestic EDA market pattern has gradually become clear. With the advantages of product value and quantity, mature capital operation capabilities and abundant financing strength, leading enterprises have established a dominant position in the competition and accelerated their evolution to a full-process integrated platform.

However, the R&D of EDA tools generally faces industry challenges such as long investment cycles and scarcity of technical talents. In this context, for leading enterprises that have already established a scale, it has become a key path to accelerate development by quickly obtaining complementary point products through strategic mergers and acquisitions and forming a complete solution. This can not only make up for the gap in its own product line, but also effectively shorten the technology accumulation cycle and consolidate its leading position in the market.

The acquisition of Xinhe Semiconductor by Empyrean is a model case of this strategy. Founded in 2010, Xinhe Semiconductor has significant technical advantages in chip-level high-frequency electromagnetic simulation, package-level signal integrity (SI/PI), system-level performance optimization, and other fields. This acquisition will enable Empyrean to achieve breakthroughs in the field of RF chip and chiplet design, and build a full-link solution from chip to package, module, PCB board level, interconnection and system.

02

M&A idea 2: Integrate EDA and IP ecology to reconstruct the business model

The strategic emphasis of EDA global giants on IP business stems from the unique advantages of the IP core business model. Traditional EDA software mainly adopts the license + annual maintenance fee model (the maintenance fee is usually 15-25% of the license fee). Despite the industry's gradual shift to a subscription-based approach in recent years, revenue caps are still limited by the number of customers.

In contrast, the IP core model is more resilient for growth. Leading overseas companies adopt a dual-track fee of "front-end licensing + back-end royalty" for IP products: the licensing fee is a one-time delivery fee, while the royalty is charged proportionally based on the sales volume of the customer's product. This model directly links the revenue of the IP supplier to the sales performance of the customer, rather than just the design cost, which significantly improves the revenue elasticity and growth space.

From the perspective of technology ecology, there is a natural synergy between EDA tools and IP cores, which can effectively enhance customer stickiness: EDA companies have mastered the core technology of the whole chip design process, so that they can develop IP cores that are highly compatible with their own tools, ensuring seamless connection in design, verification, synthesis and physical implementation, and greatly reducing customer design risks. By providing both tools and IP, companies can build a "one-stop chip design platform" to meet customers' needs from design to verification, simplifying supply chain management and accelerating time-to-market to create significant value for customers.

The

global semiconductor IP industry is highly concentrated, with ARM, Synopsys and Cadence accounting for more than 60% of the market, and their product matrix covering major IP categories. Other large IP vendors, such as SST, Imagination, CEVA, eMemory, etc., focus on specific segments.

Synopsys and Cadence's rich IP portfolio is built primarily through a systematic M&A strategy

The acquisition of Primarius Micro will make it a company with deep integration of EDA tools and semiconductor IP. As the second largest semiconductor IP supplier in China, Ruichengxin's technology accumulation in the fields of analog and digital-analog hybrid IP (the first in China), embedded memory IP (the top three in China), and radio frequency communication IP (the first in China) will directly improve Primarius' design ecosystem and enhance its comprehensive competitiveness.

03

Industry outlook: The prelude to mergers and acquisitions in the EDA industry has begun

China's EDA industry is in a critical period of rapid development and integration. According to the statistics of "ittbank", there are more than 80 domestic EDA companies, and only 3 EDA companies are currently listed on the A-share market.

Among the three listed companies, Empyrean and Primarius have clearly announced their mergers and acquisitions, while another listed company, Guangli Micro, has a special feature - its EDA products are mainly for wafer fabs, which are significantly different from the EDA tools used by design companies. In 2023, Guangli Micro's test equipment revenue will account for more than 80% of the total revenue, and the author believes that it is essentially a semiconductor test equipment provider.

Among the unlisted companies, Hejian Gongsoft and Xinhuazhang, as "star enterprises" in the field of digital chip EDA, are also actively expanding their product lines and technical strength through mergers and acquisitions.

In addition to the above-mentioned leading enterprises, many small EDA manufacturers focusing on point tools will face strong survival pressure: limited product value is difficult to support continuous R&D investment, market expansion, customer service and team building. Without capital market support, it is also difficult for these companies to gain talent and financial synergies through mergers and acquisitions.

In the foreseeable future, as the competitive landscape in the EDA field becomes clearer and clearer, leading companies will accelerate the pace of mergers and acquisitions and integrate high-quality technical teams and product resources. After all, good products and teams are the core resources of an EDA company, and such resources are always the most scarce.

Statement

Without the permission of Wenyifuxin, no institution or individual may forward, reproduce, copy, publish or quote all or part of the content published by this subscription account in any form, nor may it forward, reprint, copy, publish or quote all or part of the content published by this subscription account from any institution, individual or media platform operated by Wenyi Fuxin without the written authorization of Wenyi Fuxin. If you need to authorize reprinting, please contact the editor of Literature and Art Fuxin.

We do not make any express or implied warranty as to the accuracy, reliability, timeliness and completeness of the information contained in this Subscription Account, and under no circumstances does it constitute any investment advice to the audience receiving the content of this Subscription Account, and we shall not be liable for any loss caused by the use of any content contained in this Subscription Account by any party.

Ticker Name

Percentage Change

Inclusion Date