Author: Sun Huaqiu

Author: Sun Huaqiu

Edited by Han Xun

[Introduction].

On April 8, Aojie Technology (688220. SH) disclosed its 2024 annual report. The data is eye-catching, and its operating income broke through the 3 billion yuan mark for the first time, a year-on-year increase of 30.23% to 3.086 billion yuan, with a strong growth momentum.

However, just when the revenue was soaring, the profitability of Aojie Technology did not improve, but turned down, and the net profit attributable to the parent company fell from -506 million yuan in 2023 to -693 million yuan. What's even more thought-provoking is that since 2017, Aojie Technology has been mired in losses for 8 consecutive years.

At this moment, a question is in front of investors: the revenue growth rate of Aojie Technology is considerable, even far exceeding that of many peers, but why has it been staggering on the road to profitability and has been unable to knock on the door of profitability?

On April 10, on issues such as continuous losses and product advantages, Times Business Research Institute sent a letter to the securities department of Aojie Technology and called to inquire, and its staff replied on the phone that the company does not accept media interviews and research for the time being.

[Summary].

1. The revenue of IP licensing business fell by 70% year-on-year. Arcjet's current revenue is highly dependent on chip sales, and nearly ninety percent of its revenue in 2024 will come from the sales of chip products. In addition, its high-margin semiconductor IP licensing business revenue fell by 71.44% year-on-year, dragging down the overall gross profit margin.

2. High cost erosion of profit margins. In 2024, the R&D expenses of Arcjet Technology will reach 1.242 billion yuan, and the R&D expense rate will reach 36.68%; At the same time, its sales expenses increased by 25.73% year-on-year, and administrative expenses increased by 10.12% year-on-year, eroding part of the profit margins.

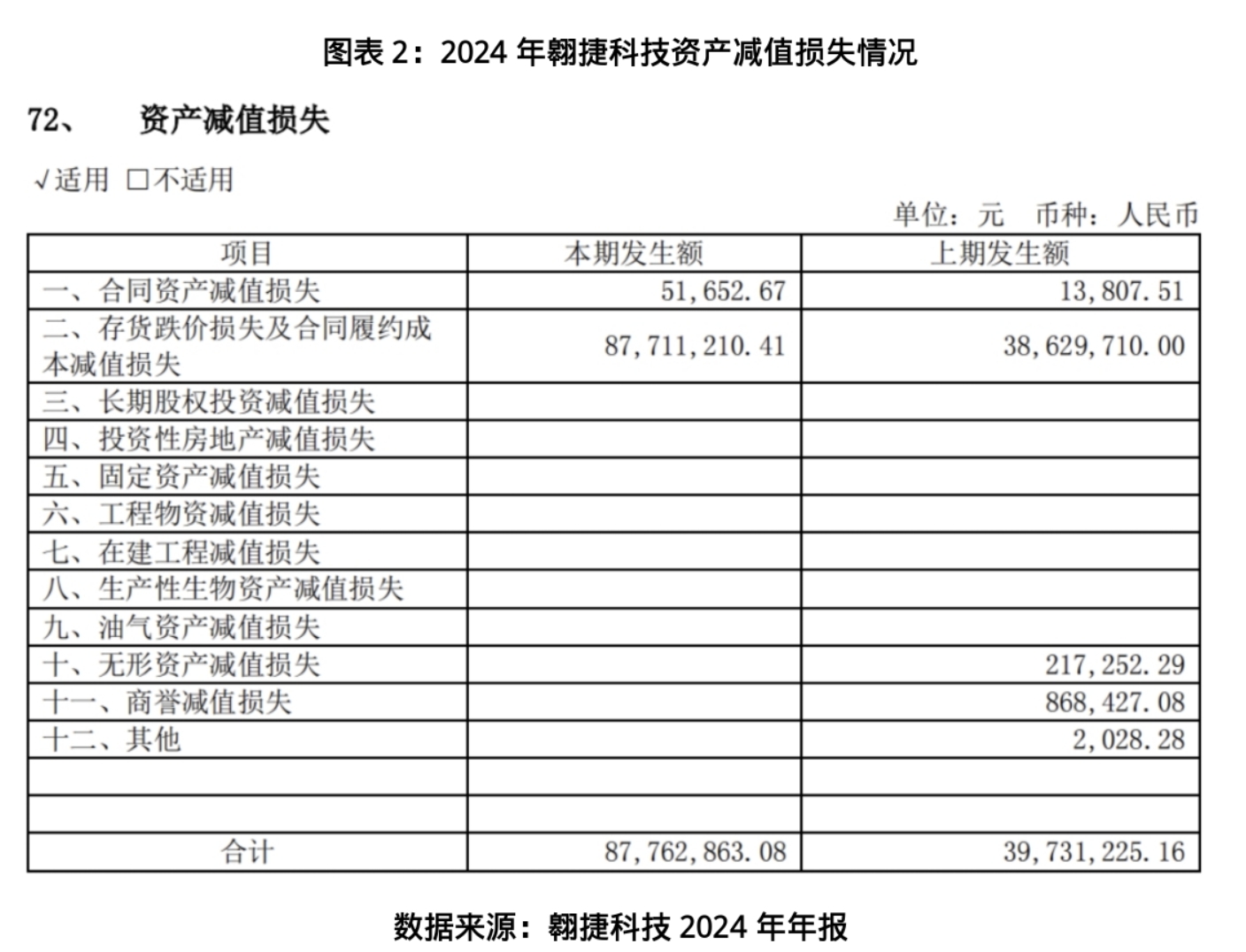

3. Asset impairment losses expanded. At the end of 2024, the book value of the inventory of Aojie Technology was 1.351 billion yuan, although it was slightly lower than that at the end of 2023, but the provision for inventory decline was significantly increased, resulting in a 120.89% increase in the impairment loss of assets in the current period to 87.7629 million yuan, which became an important factor affecting the profit of the current period.

4. In the short term, it is necessary to break the dilemma of "cost reduction + destocking". In the context of continuous losses, the core challenge of Aojie Technology is to balance "short-term survival" and "long-term investment". In the short term, Arcjet needs to improve the quality of profitability by optimizing its customer structure, controlling non-essential expenses, and accelerating inventory depletion.

[Text].

First, the business structure is relatively simple, and the revenue of IP licensing business has dropped by 70% year-on-year

As one of the few companies in China that has mastered the development capability of 5G baseband chips, it faces competition with chip giants such as Qualcomm, Huawei HiSilicon, MediaTek, and UNISOC in the field of wireless communication chips.

As an industry catch-up, Arcjet's current revenue is highly dependent on chip sales business, and its core layout of chip products, chip customization and semiconductor IP licensing three main businesses, forming a "one strong and two weak" development pattern.

The annual report shows that in 2024, the above three main business incomes of Aojie Technology will be 3.014 billion yuan, 336 million yuan and 35 million yuan respectively, accounting for 89.02%, 9.92% and 1.04% of the main business income respectively, and the business structure is significantly differentiated.

Specifically, the revenue of the chip product business was 3.014 billion yuan, a year-on-year increase of 34.17%, becoming the absolute revenue pillar, while the gross profit margin of the business was only 20.32%. Among them, cellular baseband chips contributed 2.809 billion yuan, accounting for 93.21% of chip product revenue, and the cumulative shipment of 4GCat.1 main chips exceeded 400 million.

Looking at the chip customization business, the revenue was 336 million yuan, a year-on-year increase of 48.38%, but the overall business scale is relatively small.

Although the gross profit margin of the business is as high as 100%, the revenue is only 35 million yuan, a year-on-year decrease of 71.44%, and the proportion of revenue will drop from 4.75% in 2023 to 1.04%, mainly because some projects are in the implementation period and the newly upgraded IP is in the process of customer introduction.

From the perspective of gross profit margin, in 2024, the gross profit margin of the above three major businesses of Aojie Technology will increase, but the revenue of the semiconductor IP licensing business with high gross profit will shrink significantly, which will drag down the overall gross profit margin to a certain extent, resulting in the comprehensive gross profit margin of Aojie Technology falling from 24.05% in 2023 to 23.19%.

Second, high cost erosion of profit margins

From the perspective of expenses, in 2024, Arcjet Technology will continue to invest in high-intensity R&D, with annual R&D expenses reaching 1.242 billion yuan, a year-on-year increase of 11.30%; The R&D expense ratio remained high at 36.68%, while the R&D expense ratio in 2023 was as high as 42.92%.

According to the annual report, in 2024, the R&D resources of Aojie Technology will be concentrated in 18 key projects, of which 12 projects, including 5G smartphone SoC chips, 5G lightweight intelligent terminal chips, and 4G smartphone chips, are still in the promotion stage, and have not yet been commercialized, and it is difficult to contribute profits in the short term.

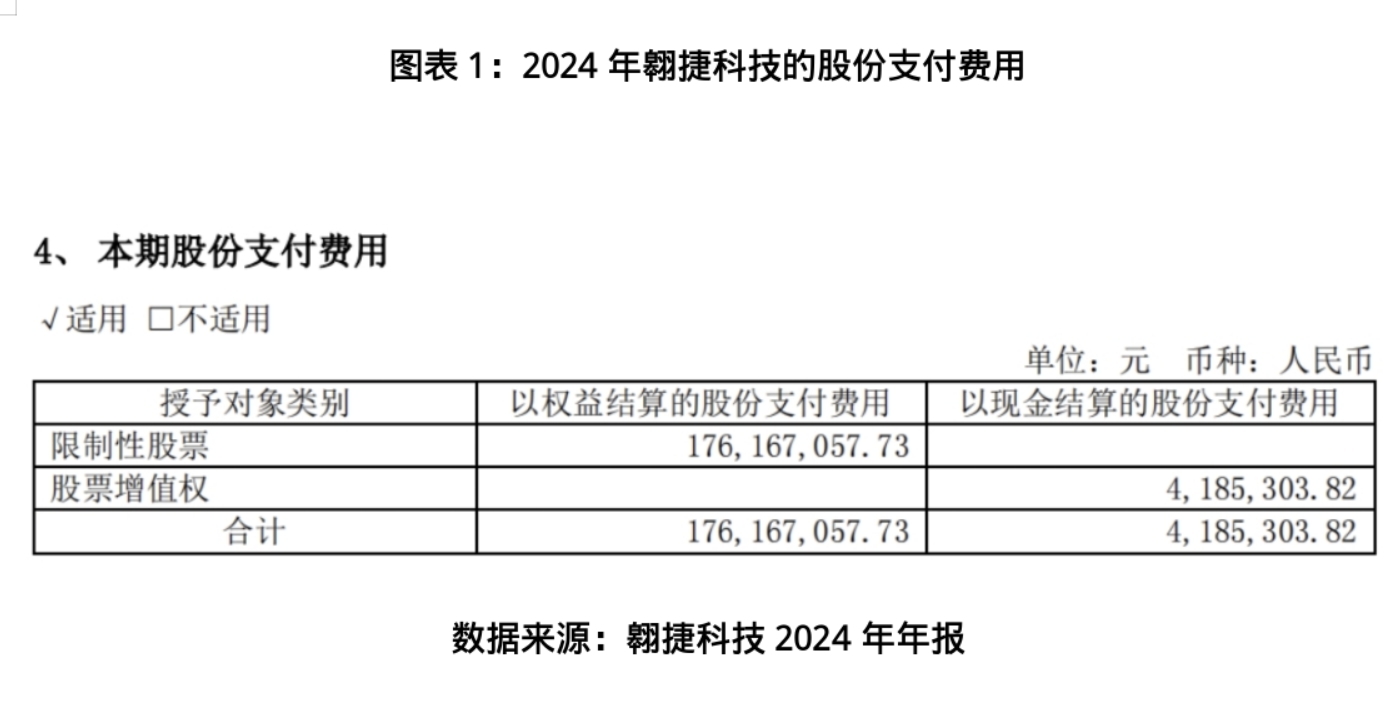

During the same period, the sales expenses of Aojie Technology increased by 25.73% year-on-year, and the administrative expenses increased by 10.12% year-on-year, mainly due to the increase in share-based payment expenses generated by equity incentives. In 2024, the share payment fee of Aojie Technology will be as high as 180 million yuan, eroding part of the profit margin.

It can be seen that although the high R&D investment has consolidated the technical reserves, the current high cost has squeezed the profits of Aojie Technology, highlighting the phased pressure on profitability on the expense side.

Third, the asset impairment loss expanded, and the pressure of inventory decline was highlighted

Affected by factors such as intensified competition in the industry and accelerated iteration of product technology, the inventory management of Aojie Technology is facing great challenges.

According to the annual report, at the end of 2024, the book value of Aojie Technology's inventory was 1.351 billion yuan, although it was slightly lower than that at the end of 2023, but the provision for inventory decline was significantly increased, resulting in a 120.89% increase in the current asset impairment loss from 39.7312 million yuan in 2023 to 87.7629 million yuan, which became an important factor affecting the current profit.

Fourth, the core view: in the short term, it is necessary to break the dilemma of "cost reduction + destocking", and rely on the commercialization of technology in the long term

The gross profit margin of the core business of Arcjet Technology is only about 20%, while the R&D investment is high, the R&D expense ratio is maintained at about 40% all year round, and the management and sales expenses are rising, and multiple cost pressures have caused it to fall into losses for eight consecutive years, and it has not been able to knock on the door of profitability.

In the context of continuous losses, the core challenge of Aojie Technology is to balance "short-term survival" and "long-term investment".

Times Business Research Institute believes that in the short term, Aojie Technology needs to improve the quality of profitability by optimizing customer structure, controlling non-essential expenses, and accelerating inventory depletion. In the medium and long term, it needs to reshape the three-wheel drive model of "chip sales + customized design + IP licensing", promote the high-end breakthrough of 5G smartphone SoC chips, automotive-grade chips and other products, increase the proportion of high gross profit business revenue, and rely on 5GRedCap chips, self-developed baseband IP and other technical reserves to promote commercialization and open up new growth space.

It is recommended that investors pay close attention to the progress of new product order delivery and gross profit margin changes in 2025, and if the new product expansion effectively improves the profitability, it is expected to usher in valuation repair opportunities.

Ticker Name

Percentage Change

Inclusion Date