In 2024, Walvax Biotech handed over a bleak answer, not only the operating income and net profit attributable to the parent company both fell, but also fell in the DuPont Triangle, under multiple pressures, whether the company can adhere to the path of innovative vaccine research and development, maintain its core competitiveness, and regain positive growth in performance, the management has a long way to go, and the market will wait and see.

On the evening of April 11, 2025, Yunnan Watson Biotechnology Co., Ltd. (300142. SZ, hereinafter referred to as "Walvax Biotech") released its 2024 annual report. As a listed company that is in a leading position in the field of biotechnology drugs, Walvax's financial performance has made investors unable to hide their disappointment.

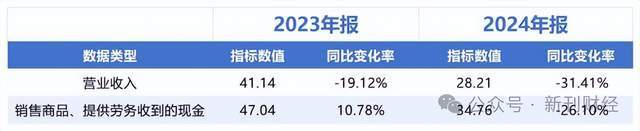

According to the data, the company's operating income in 2024 will be 2.821 billion yuan, a year-on-year decrease of 31.41%; the net profit attributable to the parent company was 142 million yuan, a year-on-year decrease of 66.10%; The weighted average return on equity was 1.51%, a decrease of 3.03 percentage points from the same period last year, and the above key financial indicators have declined for two consecutive years.

Operating income decreased significantly

Walvax's operating income has decreased significantly, and the business has shown a strong contraction. In 2024, Walvax's operating income will plummet to 2.821 billion yuan from 4.114 billion yuan in the previous year, a decrease of 1.320 billion yuan, a year-on-year decrease of 31.41%. This decline is very different from the performance of some competitors in the vaccine industry, and in 2024, Olin Biotech (688319. SH) revenue increased by 18.69% year-on-year, and CanSino (688185. SH) revenue rose by 137.01%.

It is worth noting that Walvax's product line is extremely concentrated, with independent vaccine products accounting for more than 99% of revenue in 2023, and the sum of other service revenue, intermediate products and other business revenues is less than 1%. In 2024, even though the other three major business segments have achieved an increase of more than 100%, the independent vaccine will decrease by 31.41% year-on-year, which will cause a significant drag on the overall revenue.

Source: Straight Flush iFind

Despite the decline in revenue, in the past two years, Walvax Biotech has received 4.704 billion yuan and 3.476 billion yuan in cash from the sale of goods and labor services, respectively, although it has decreased by 26.10% year-on-year, but its decline is lower than the decline in operating income by -31.41%, and the amount is greater than the revenue data of the corresponding year, and the balance of accounts receivable is also 691 million yuan less than that at the end of 2023, indicating that the company's work in recovering accounts is still fruitful.

Source: Straight Flush iFind

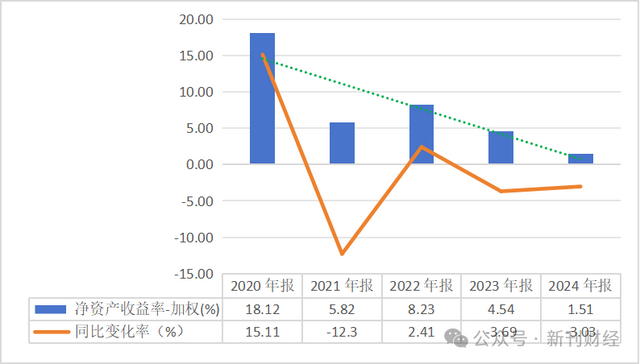

ROE continued to decline to only 1.51%.

Walvax's weighted average return on equity in 2024 is only 1.51%, a decrease of 3.03 percentage points from 4.54% in 2023, showing a significant downward trend in recent years. Through the DuPont analysis of return on equity, it can be found that Walvax Biotech is experiencing three major problems: deterioration of earnings quality, low asset efficiency, and failure to amplify returns through leverage.

Source: Straight Flush iFind

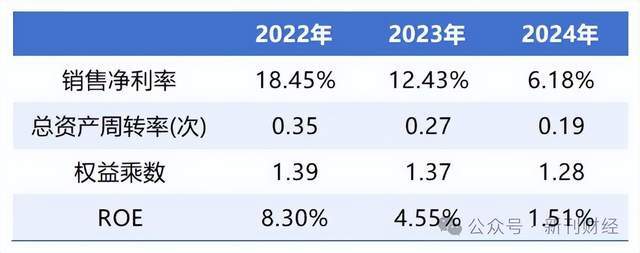

According to the 2024 financial report data, Walvax Biotech has a net profit of 174 million yuan, an operating income of 2.821 billion yuan, an average total asset of 15.157 billion yuan, and an average owner's equity of 11.452 billion yuan. Based on this, the company's net profit from sales in 2024 is 6.18%, the total asset turnover ratio is 0.19, and the equity multiplier is 1.28. Return on equity of 1.51% is the product of these three. It is significantly lower than the median value of 7.13% in the pharmaceutical and biological industry.

Source: Straight Flush iFind

Net profit margin on sales plummeted, and the expense structure was abnormal in some periods

Walvax Biotech's revenue contracted by 31.41% significantly, and its net profit fell even more, with the company's net profit falling from 511 million yuan to 174 million yuan in 2024, a year-on-year decrease of 65.89%. The company's low net profit margin on sales has been cut in half, from 12.43% in 2023 to only 6.18%. Therefore, the decline in gross profit margin is expected, with gross profit margins from 2022 to 2024 being 88.02%, 85.47% and 79.69% respectively, but basically consistent with the median level of the vaccine industry.

In this context, Walvax's management expenses have soared against the trend. The management expense ratio has risen to 14.94% in 2024, more than double the 7.23% in 2023. This anomaly may expose management problems and the company's internal controls may be gradually failing. Although the remuneration of the company's senior management team has generally decreased significantly compared with the previous year, Walvax's management expenses in 2024 have soared from 298 million yuan to 422 million yuan, an increase of 41.64%, or there are improper expenditures, which makes the company's interests outflow excessively.

On the contrary, the costs that should not be reduced are decreasing. Walvax's R&D expenses contracted for the second consecutive year, from 933 million yuan to 776 million yuan in 2023, and further to 597 million yuan in 2024, a decrease of 23.17%, contrary to the industry trend. Under the competitive logic of "R&D is king" in the biopharmaceutical industry, the contraction of Walvax's R&D expenses may indicate the weakness of the company's follow-up pipeline. The sales volume of the company's core products has declined, and the investment in new drug research and development is insufficient, and its long-term competitiveness may be further weakened. And if the company deliberately lowers R&D expenses in order to "save" profits, it will overdraft the company's future.

Asset turnover performance was sluggish

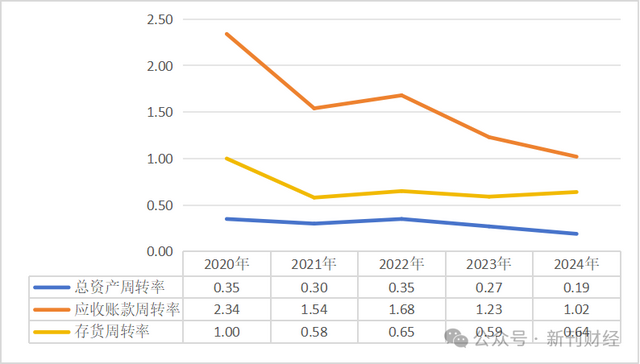

In 2024, the asset turnover rate will be 0.19 times, that is, only 0.19 yuan of revenue will be generated for every 1 yuan of assets, which is far lower than the median value of 0.45 times in the pharmaceutical and biological industry. 0.19 is also a significant decrease from the company's previous two years of 0.35 and 0.27, indicating that the company's utilization of asset generation income is continuing to decrease.

Source: Straight Flush iFind

Even so, Walvax Biotech is still insisting on increasing investment, and the company's investment net cash flow in 2024 will be -1.267 billion yuan, and in 2023 it will be -808 million yuan, which may further exacerbate the company's capacity idle risk in the context of continuous decline in revenue.

Total asset turnover declined, as did accounts receivable turnover and inventory turnover. In the past five years, the accounts receivable turnover ratio has dropped from 2.34 to 1.02, and the efficiency has dropped by more than half, indicating that the company's ability to collect payments tends to weaken overall, or there is a serious deterioration in the credit of some customers. The company's inventory turnover ratio also decreased from 1.00 to 0.64, and the turnover efficiency decreased by 36%, and the risk of unsalable goods increased significantly. As a result, asset efficiency can be described as a comprehensive decline, and asset expansion and operational inefficiency will inevitably lead to waste of resources.

The equity multiplier is not working as it should

The equity multiplier is 1.32x and the debt-to-asset ratio is 21.84%, while the median equity multiplier and the median debt-to-asset ratio of the pharmaceutical and biotechnology industry is 1.28 and the median debt-to-asset ratio is 28.29%. Walvax Biotech is significantly low, indicating that Walvax Biotech may be overly dependent on shareholder capital and fail to effectively use debt leverage.

The equity multiplier is supposed to be a booster of ROE, especially if the weighted rate of all the company's interest-bearing liabilities is lower than ROE. Now the company's return on equity has been as low as 1.51%, which is lower than the cost of most financing instruments on the market.

It is worth noting that in 2024, Walvax Biotech will also have a change in the fair value of other equity instrument investments of -46 million yuan, which cannot be reclassified into profit or loss, so it stays in the column of other comprehensive income. If this item is taken into account, the company's total comprehensive income will be 128 million yuan, and the "real" return on equity will be further reduced to 1.12%, which is closer to the edge of loss.

In 2024, Walvax Biotech handed over a bleak answer, not only the operating income and net profit attributable to the parent company both fell, but also fell in the DuPont Triangle, under multiple pressures, whether the company can adhere to the path of innovative vaccine research and development, maintain its core competitiveness, and regain positive growth in performance, the management has a long way to go, and the market will wait and see.

Written by Wei Si

Edited by Wu Xue

Ticker Name

Percentage Change

Inclusion Date