Are Better Days Ahead for American Companies in China?

Are Better Days Ahead for American Companies in China?(Yicai Global) March 24 -- Earlier this month, the American Chamber of Commerce in the People's Republic of China (AmCham) released its 2023 China Business Climate Survey Report. The AmCham is a non-profit, non-governmental organization, whose membership comprises tens of thousands of individuals from nearly 1000 companies operating across China.

The AmCham has been publishing its Business Climate Survey Reports for 25 years. I am an avid reader of these valuable documents, which give us American companies' on-the-ground perspective.

Last year was a tough one for US firms operating in China.

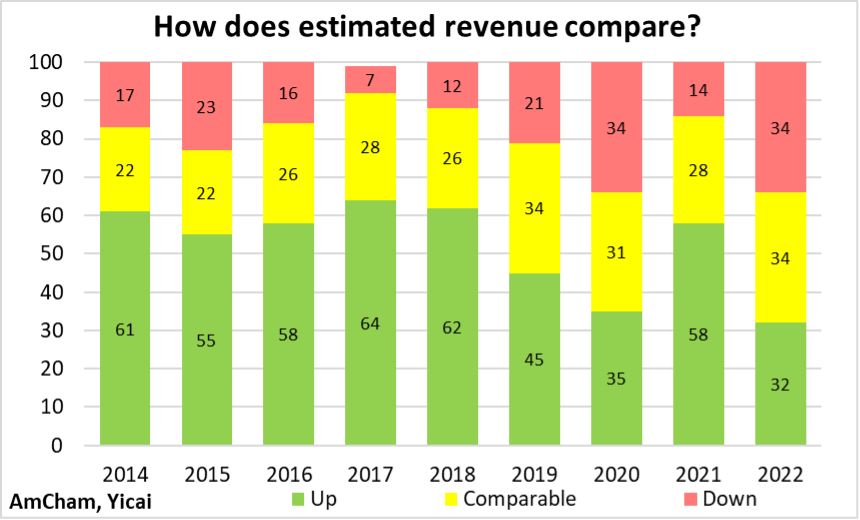

Only 32 percent of the survey respondents estimated that 2022’s revenue from their China operations would be higher than 2021’s (Figure 1). Between 2014 and 2019, on average, 58 percent of the respondents estimated year-over-year revenue increases. Unsurprisingly, much of the difficulty the firms faced last year came from the measures to control the pandemic. Three-quarters of the respondents said that Covid control reduced their profitability and, for a third of these firms, the impact was significant.

Figure 1

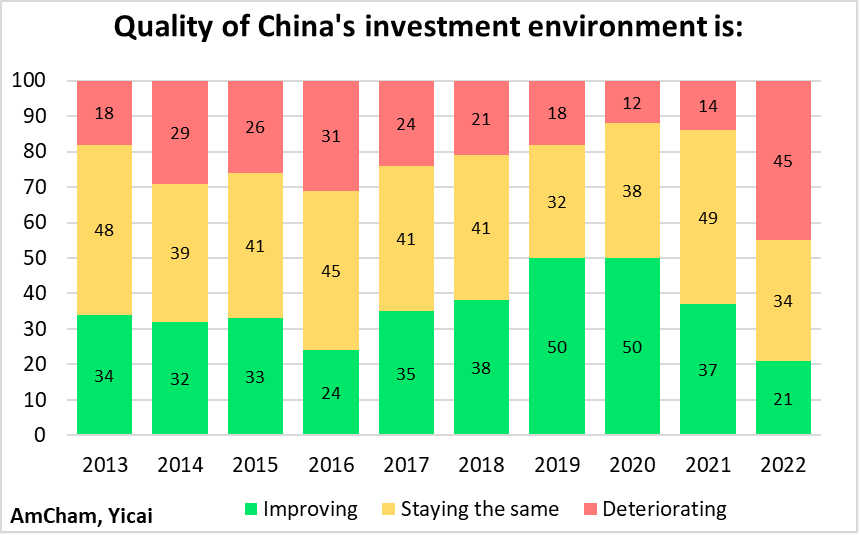

Perhaps an even more sobering result was that 45 percent of the survey respondents indicated that the quality of China’s investment environment deteriorated in 2022. This was, by far, the greatest proportion of respondents noting a worsening investment environment in the last decade (Figure 2).

Figure 2

Foreign investment is a key channel through which international best practices are disseminated to China. China needs to learn from the rest of the world to keep moving toward the technological frontier and an inhospitable investment environment would slow its convergence to advanced-country productivity levels.

Will a deteriorating investment environment lead American firms to desert China?

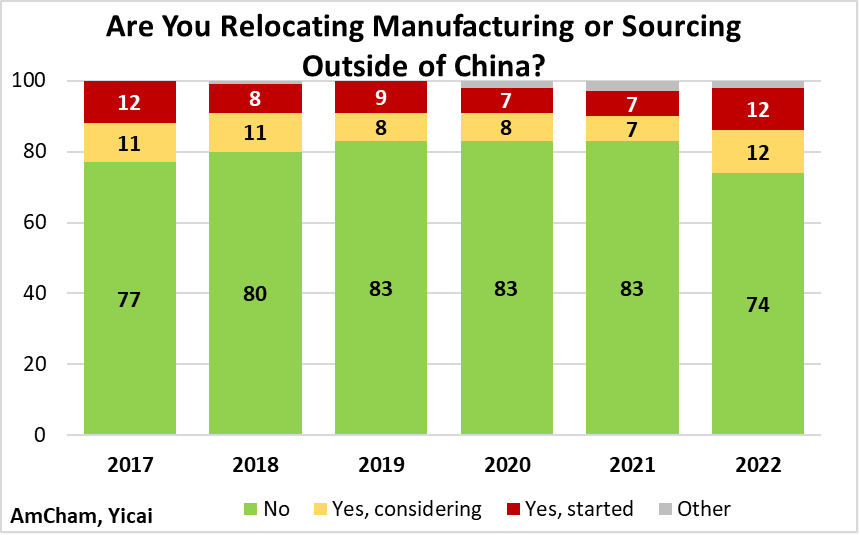

While close to three-quarters of AmCham’s members reported that they will remain here, there was a noticeable increase in the share that said that they are, or are considering, relocating manufacturing or sourcing outside of China (Figure 3).

The top reasons that firms gave for leaving China, or considering so doing, are risk management (noted by 60 percent of respondents), Covid prevention measures (57 percent) and rising US-China tensions (43 percent).

Figure 3

AmCham appears to have conducted its survey before China relaxed its public health measures in December. Subsequently, firms’ operating environment has returned to normal. Moreover, with China again issuing visas, regular business travel is resuming and a key challenge noted by US companies is being resolved.

We hope the disruptive effect of Covid was a one-time event. Thus, American companies’ sentiment toward doing business in China will now depend on other factors. Key among these is the policy and regulatory setting in which these firms operate.

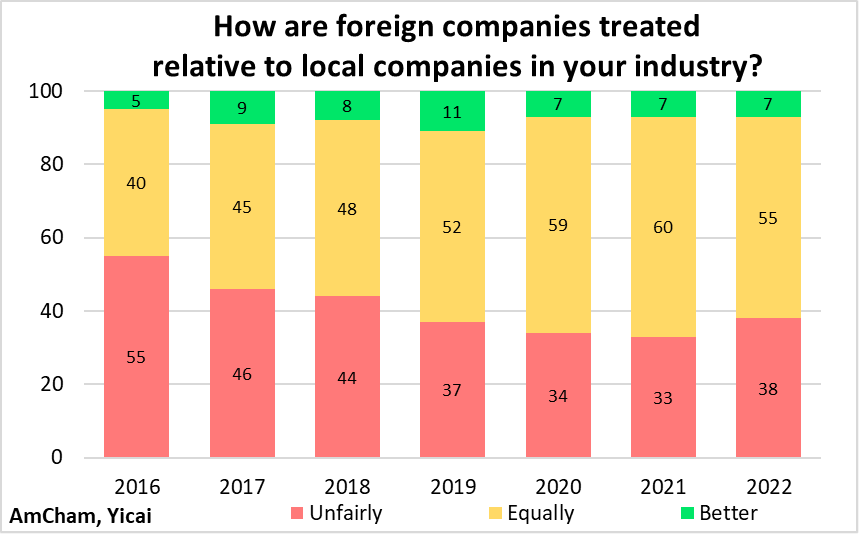

AmCham has long asked its members if China’s policies and their enforcement treat foreign companies fairly. In the most recent survey, 38 percent of the respondents felt that foreign companies are treated unfairly compared to domestic firms (Figure 4). This is a slightly higher share than in the last three years, but it remains significantly lower than what the members reported in 2016-18.

Figure 4

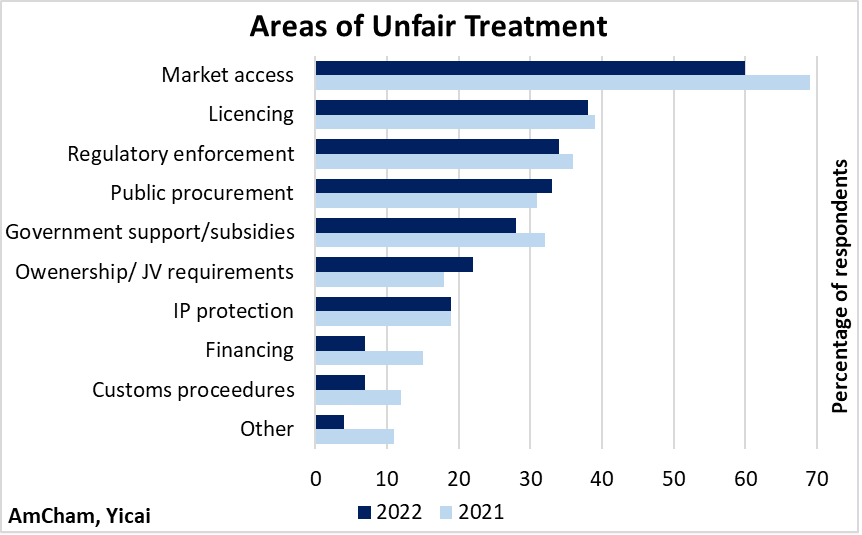

Given the importance of foreign investment for China, we should try to understand what is driving the perception of increasing unfairness. AmCham’s survey asks members to identify the specific areas of unfair treatment. However, in comparing the last two surveys, respondents did not flag a significant increase in any specific area of unfair treatment in 2022 (Figure 5).

Market access remained AmCham members’ top concern but the proportion flagging it fell to 60 percent from 69 percent in 2021. Public procurement (+2 percentage points) and ownership/joint venture requirements (+4 percentage points) were the only two areas where a greater share of the membership reported concerns. In the other eight areas, fewer members expressed concerns. It is, therefore, hard to pinpoint what gave rise to respondents’ perception of increasing unfairness.

Figure 5

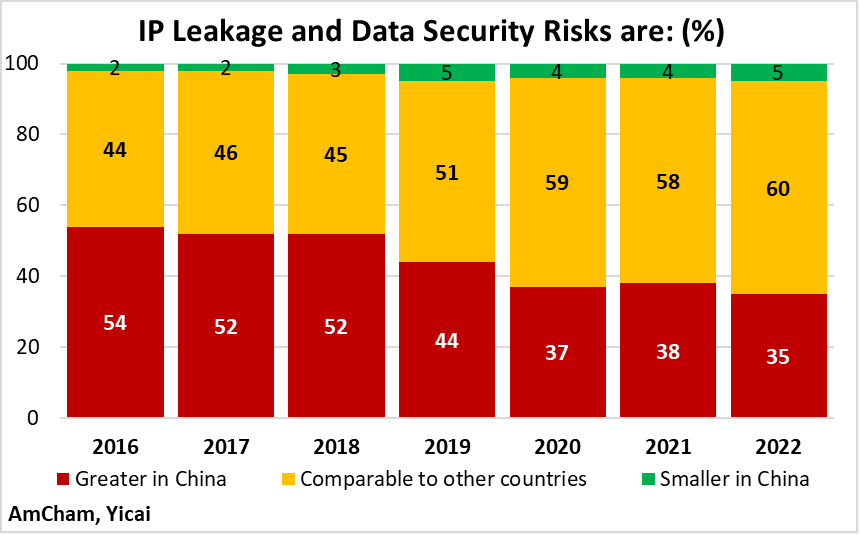

For many years, American firms operating in China have worried that their intellectual property (IP) could be stolen. Between 2016 and 2018, a majority of AmCham’s survey respondents felt that the risks of IP theft and data loss in China was greater than in other countries (Figure 6). This proportion has fallen in recent years and declined to 35 percent in the most recent survey.

Figure 6

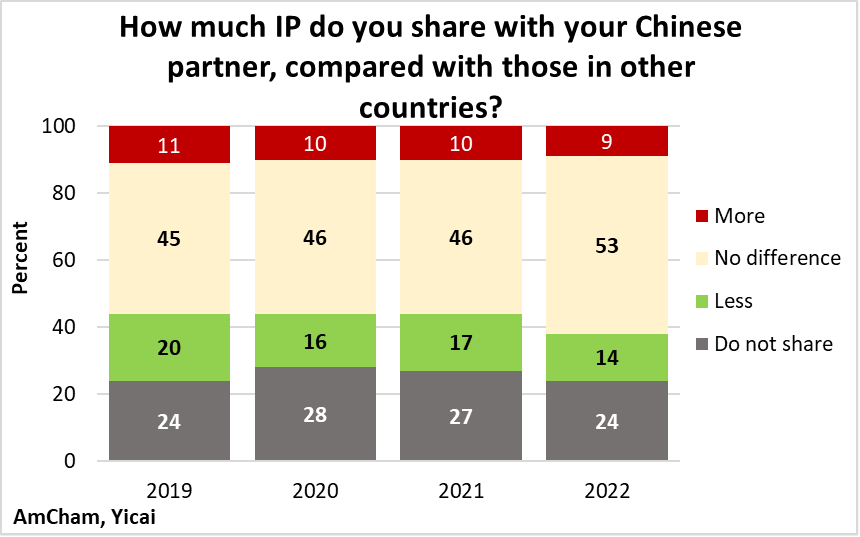

Forced technology transfer has also been a contentious bilateral issue. In the most recent survey, respondents did not indicate that forced technology transfer became more of a problem in 2022.

A greater share of respondents said that the amount of IP that they share with their Chinese partners was similar to those in other countries. And a smaller share said that they shared more IP with their Chinese partners (Figure 7). Moreover, the proportion that said they shared information voluntarily rose slightly while the proportion of those who did so out of informal pressure dropped.

Figure 7

My reading of the survey responses is that the perceived deterioration in China’s investment environment is most likely related to the public health policies implemented to contain the spread of Covid and not an increasing anti-foreign attitude on the part of policymakers and regulators. If this is so, then we can expect AmCham’s members’ perception of China’s investment environment to improve this year.

As noted above, risk management and rising US-China tensions – in addition to Covid prevention measures – are also leading AmCham members to leave, or consider leaving, China.

I am not sure how risk management can be improved by leaving China. It is very costly for a company to de-risk its supply chain by building a parallel one in another country. Increasing inventories of critical materials and components, in most cases, is likely to be a more workable solution. Moreover, the experience of the last three years shows that China’s supply chain was much more resilient than those in other countries. Firms producing in China can benefit from extensive world-class infrastructure, a dense network of suppliers and a very flexible labour force.

More than 96 percent of AmCham’s members believe that positive bilateral relations are important for the continued growth of their business. Unfortunately, they anticipate that these relations will deteriorate this year. Sixty percent of survey respondents hope that improved relations will lead to a further opening of the Chinese market to foreign firms and 43 percent are looking for further reductions in tariffs.

As was the case in the previous year’s survey, respondents’ primary ask of the US government is that it will refrain from engaging in aggressive rhetoric and tit-for-tat actions. Their number one ask from the Chinese government was to ease the Covid-related restrictions.

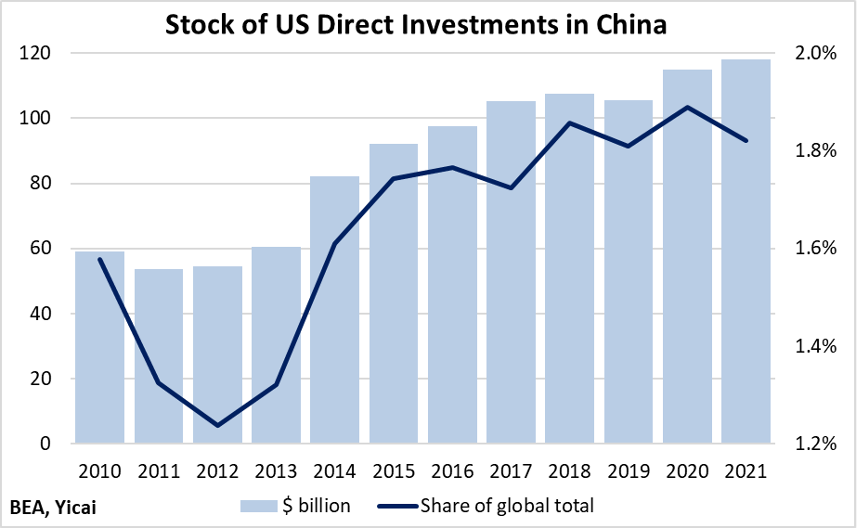

It is easy to be pessimistic about the future of US firms’ business in China. But it is worth noting that – notwithstanding the uncomfortable geopolitics – the stock of US direct investment in China rose to just under $120 billion in 2021, the last year for which the US Bureau of Economic Analysis (BEA) has data (Figure 8). It essentially doubled from 2013’s level, growing at an average annual rate of 9 percent, as China became a relatively more important destination for US direct investment abroad.

Figure 8

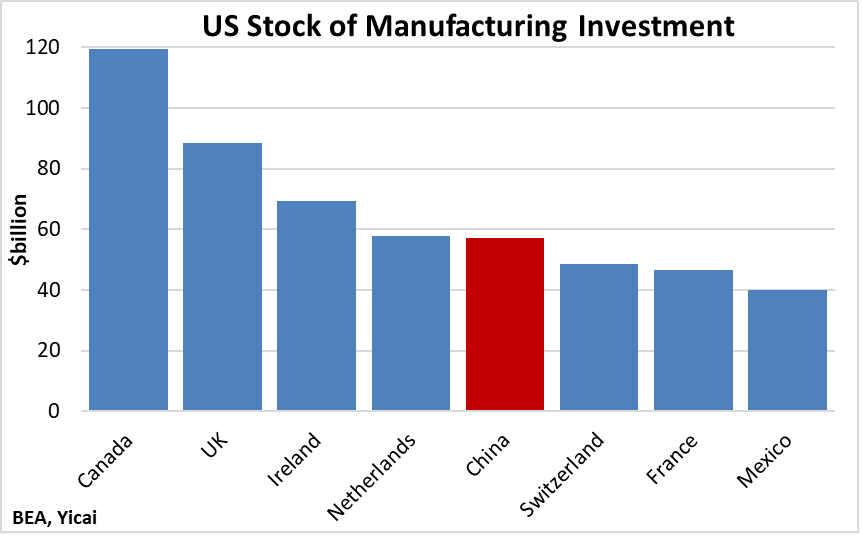

The US’s investments in China are very different from those it makes in the rest of the world. Only 14 percent of the US’s global direct investment stock is in manufacturing. But manufacturing accounts for close to half of American direct investment in China. China is the US’s fourth most important destination for manufacturing investment (Figure 9). Wholesale trade accounts for 15 percent of the US’s direct investment in China but only 4 percent of its global direct investment. This reflects the important role that China plays in providing cost-competitive goods to the US market.

Figure 9

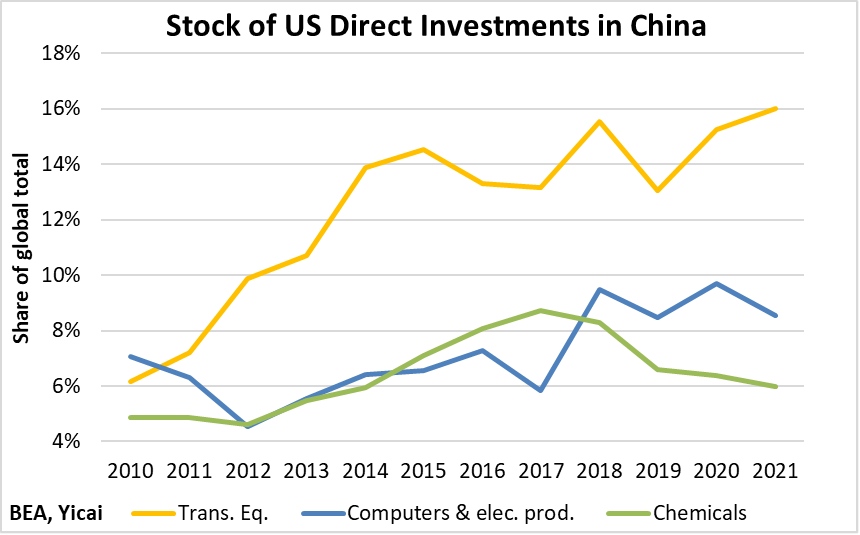

Transportation equipment is the most important manufacturing sub-sector. China accounts for 16 percent of the US’s global investment in transportation equipment. By comparison, Canada and the EU each account for 22 percent. Computer and electronic products and chemicals are also important areas of US investment in China’s manufacturing industry (Figure 10).

Figure 10

The frustration and pessimism expressed by AmCham survey respondents are understandable. While Zero Covid saved many lives, it did make doing business in China difficult. Now the economy has reopened and Premier Li Qiang recently emphasized that China will only open itself wider to the world and that foreign investors are very welcome. Hopefully, this means that better days lie ahead for American companies in China.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.