Is the IMF Too Bearish on China’s Medium-Term Prospects?

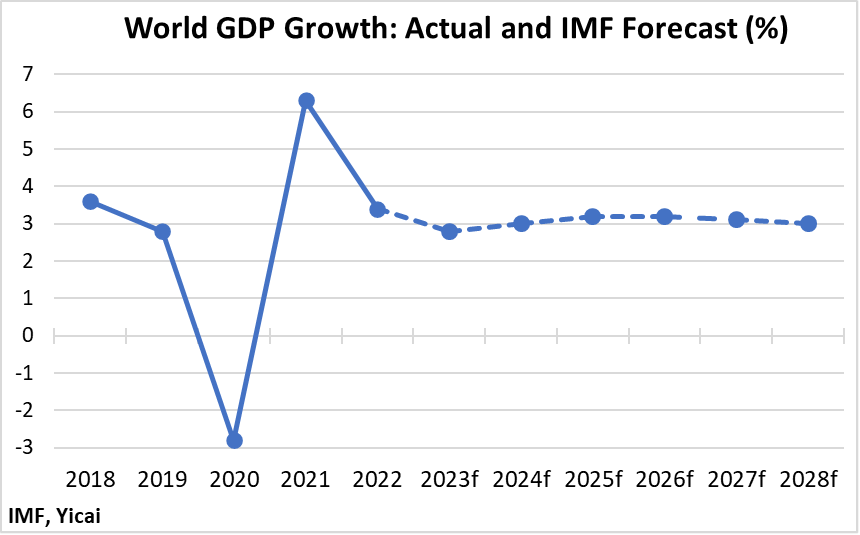

Is the IMF Too Bearish on China’s Medium-Term Prospects? (Yicai Global) April 17 -- The IMF has just released its semi-annual (WEO). The Fund expects world GDP growth to slow from the 3.4 percent recorded in 2022 to 2.8 percent this year and then remain in the 3 percent range through 2028 (Figure 1).

Figure 1

By historical standards, global growth in the 3 percent range is rather slow. Between 2010 and 2019 it averaged 3.7 percent. Indeed, this WEO’s medium-term outlook for the global economy is the weakest the Fund has forecast since 1990.

The global economy’s deteriorating prospects come from four sources. First, China and Korea are expected to grow more slowly, as they have already achieved large increases in their standards of living. Thus, the pace of their convergence to the economic frontier will decline. Second, the world’s labour force is growing more slowly. Third, geopolitical events, including Brexit, ongoing US-China trade tensions and the conflict in Ukraine are leading to an economic fragmentation that weighs on growth. Finally, the Fund sees a slower pace of economic reforms than it had expected.

Not only does the WEO’s baseline scenario contain little to cheer about, the report goes on to emphasize the considerable scope for a weaker-than-forecast outcome in 2023. The Fund is concerned that the recent banking system turbulence could result in a sharper and more persistent tightening of global financial conditions. It believes that interest rates may need to increase further to reduce stubbornly high core inflation. Since private and public indebtedness are at historically elevated levels, this could mean much slower growth.

Given these downside risks, the WEO estimates that the probability of global growth falling below 2 percent this year – an outcome that only occurred five times in the last 50 years – is 25 percent.

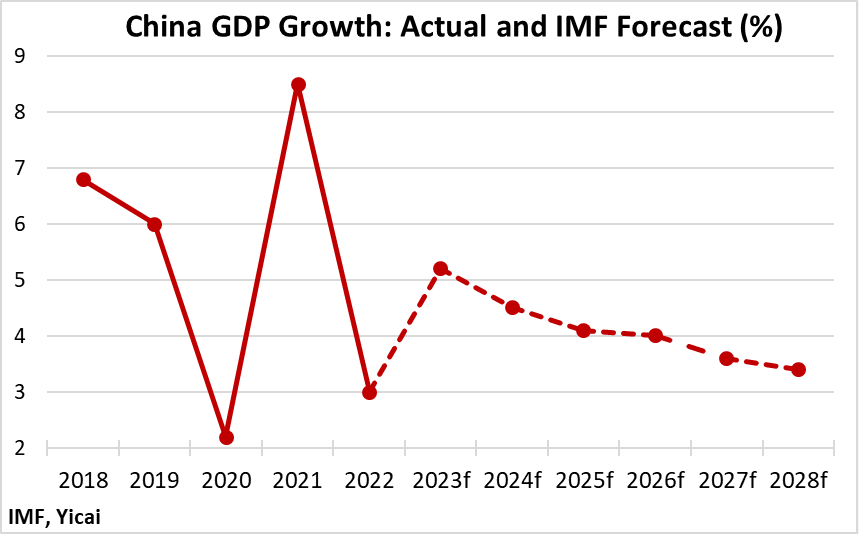

The WEO is also quite pessimistic about China’s medium-term prospects. It expects GDP growth to rebound from 2022’s 3 percent to 5.2 percent this year. However, in 2024, growth is forecast to fall to 4.5 percent and gradually decline to 3.4 percent by 2028 (Figure 2).

Figure 2

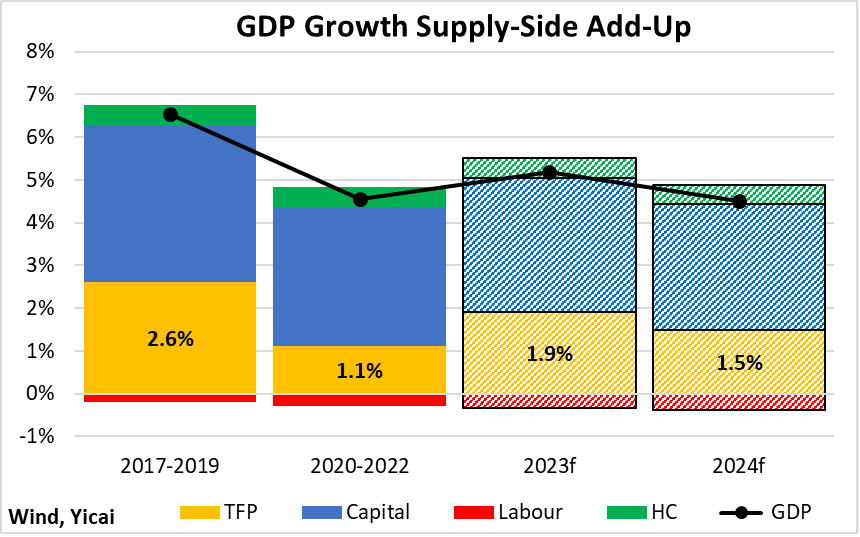

I am going to employ the venerable Cobb-Douglas production function to get some perspective on China’s growth prospects. I will model the growth of the supply side of the Chinese economy as a weighted average of the growth of the capital stock, the labour supply, human capital (HC) and total factor productivity (TFP).

In breaking down the supply side of the economy, we can find a way to directly estimate everything but TFP growth. China’s National Bureau of Statistics reports GDP growth. We can estimate the growth of the capital stock and the labour force from investment and demographic data. We estimate HC as proportional to the working population’s average years of education. We can then derive the growth of TFP indirectly as the difference between reported GDP growth and the contributions of the three factors we estimate directly.

Figure 3 shows the evolution of the supply side of China’s economy before the pandemic (2017-19) and during the pandemic (2020-22). For 2023 and 2024, we take the WEO forecast for GDP, carry forward recent trends for the growth of capital, labour and HC and derive TFP growth as a residual.

Unsurprisingly, TFP growth is expected to rebound in 2023 from its pandemic-impacted rates in 2020-22. But it appears that the WEO projection implies a drop in TFP growth in 2024. At 1.5 percent, implied TFP growth would be more than a percentage point below pre-pandemic levels. The WEO forecast likely assumes that TFP growth continues to fall over the medium term and this is what accounts for the slowing of China’s GDP growth.

Figure 3

While TFP cannot be observed directly, Bert Hofman, a respected academic who was formerly the World Bank’s Country Director for China, has done a great job of which should be correlated with China’s productivity growth. They suggest that there are reasons to be optimistic that TFP growth should rebound.

Hofman reports that China’s R&D spending grew twice as fast as the OECD average during 2019-21. In 2021, China spent 2.4 percent of GDP on R&D. This was about as much as the average OECD country and more than the EU (2.2 percent of GDP). China’s R&D spending was still well behind the global leaders – Israel (5.6 percent), Korea (4.9 percent) and the US (3.5 percent). Nevertheless, it exceeded 2.5 percent of GDP in 2022 and since the Chinese government is committed to accelerating R&D activity, I would expect China’s ranking to continue to rise over time. Hofman also notes that China doubled its number of scientific researchers in the last decade and now employs more than either the US or the EU.

Hofman believes that the quality of China’s R&D is improving rapidly. The World Intellectual Property Organization (WIPO) compiles a which is based on 81 different indicators. In 2009, when the WIPO first published its Index, China ranked 37th. In the 2022 edition, China’s ranking rose to 11th. While China trailed the US (#2), Korea (#6) and Germany (#8), it was ahead of France (#12) and Japan (#13).

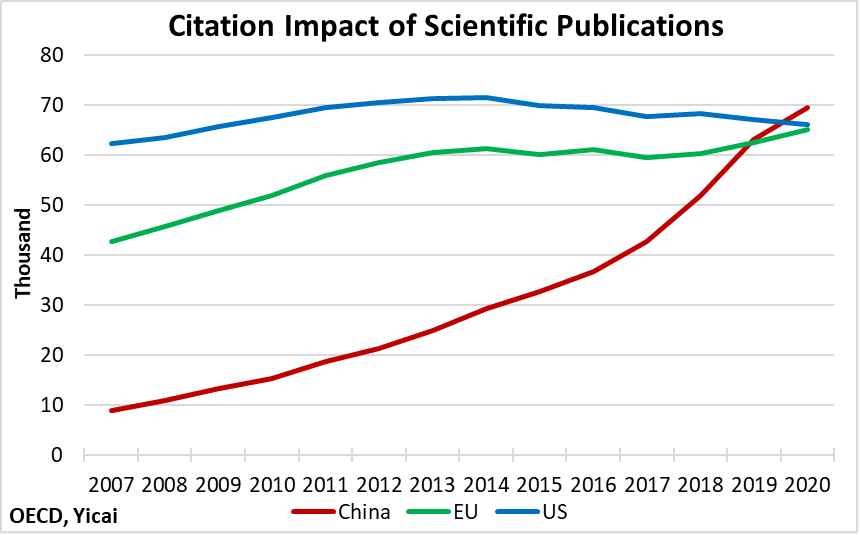

Hofman indicates that China has become a leader in both the quantity and the quality of scientific research. He cites showing that the number of scientific papers written in China doubled in the last decade. In 2020, Chinese researchers wrote 676,000 scientific research papers, compared to 622,000 in the EU and 479,000 in the US.

The OECD assesses “scientific excellence” by counting the number of papers a country publishes in the top 10 percent of those most cited in a particular field. According to this metric, the quality of China’s scientific research now ranks ahead of both the US’s and the EU’s (Figure 4).

Figure 4

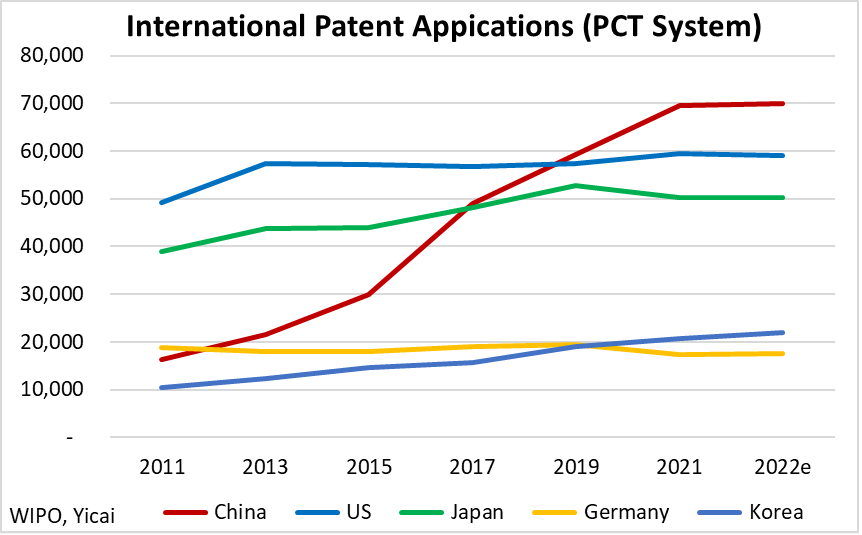

According to Hofman, China has also made great strides in creating intellectual property. The number of patents it filed in the WIPO’s Patent Cooperation Treaty (PCT) system more than quadrupled between 2011 and 2022 (Figure 5). Since 2019, China has filed more PCT applications than any other country. The WIPO’s PCT patents are enforced in all treaty-member countries and are generally seen to be of higher quality than those filed domestically.

Figure 5

My personal favourite indicator of China’s productivity is its share of global manufacturing exports. Since competition in global markets is intense, a sustained rise in China’s export share implies that Chinese firms are becoming more efficient. Figure 6 shows the jump in China’s export share since 2020.

Figure 6

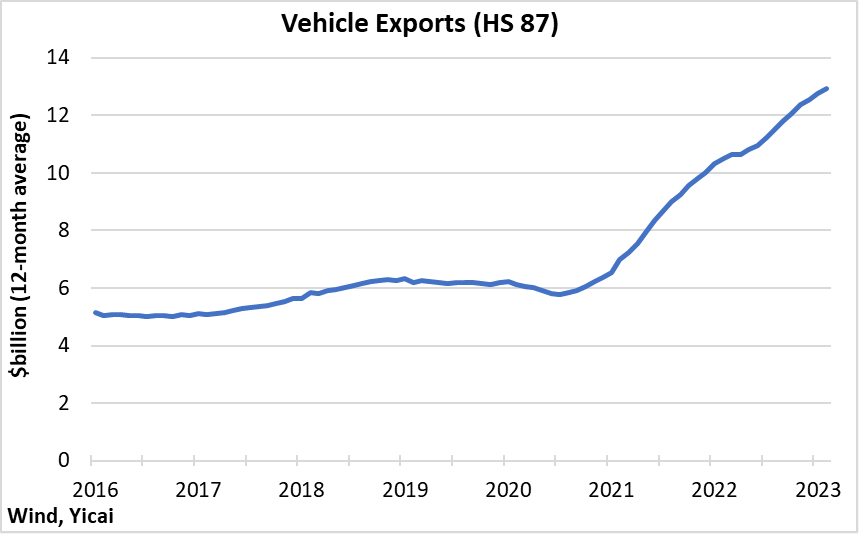

One reason that China can increase its share of global manufactured exports is that its manufacturers are moving up the value chain. This is probably best illustrated by the doubling of vehicle exports (HS code 87) in the last two years (Figure 7). Incredibly, the volume of new energy vehicle exports increased by more than 10-fold over this period!

Figure 7

I believe the indicators cited above suggest that much of the slowdown we have seen in China’s TFP growth is cyclical and that it should rebound in the years to come. Still, given China’s unfavourable demographics and the increase in its indebtedness, raising people’s living standards will increasingly depend on improving TFP growth.

In its , the IMF’s staff proposed four measures they believe could raise China’s productivity.

First, state-owned enterprises should be reformed and they should compete on an equal footing with private firms. The Fund staff estimate that closing the productivity gaps between state-owned and private firms could increase TFP by about 6 percent.

Second, local protectionism should be eliminated. The staff estimate that removing administrative borders between prefectures could raise GDP per capita by 10 percent over the long term.

Third, the market should be relied upon more to allocate resources. While the Fund staff admit there is a role for the public support of basic R&D, they warn against potentially wasteful subsidies that lead to productivity losses.

Finally, the Fund staff propose that structural reforms and new regulations should be introduced in a measured, transparent and predictable manner to avoid adverse effects on private investment.

The Chinese leadership has set the ambitious goal of per capita income reaching that of moderately developed countries by 2035. This implies a doubling of per capita incomes and GDP growth averaging 4.7 percent. However, the recent WEO forecast implies that China will be stuck in the middle-income trap. China’s ability to prove the IMF wrong rests on the growth of TFP. While this economic variable is the hardest to see, it will be the one we will be watching most closely.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.