Is China’s Economy Heading From Miracle to Malady?

Is China’s Economy Heading From Miracle to Malady?(Yicai Global) May 4 -- is among the most respected of China watchers.

Currently the Tolani Senior Professor of Trade Policy at Cornell University, he was previously chief of the Financial Studies Division in the IMF's Research Department and the head of the IMF's China Division.

Prasad has recently published an informative on the Chinese economy. Entitled “Has China’s Growth Gone From Miracle to Malady?”, the paper reviews China’s development experience, assesses its vulnerabilities and discusses policies needed to support future growth.

Prasad says that, as a result of China’s “miracle”, its per capita incomes rose to $13,000 in 2022, or 17 percent of US levels (at market exchange rates). This is up sharply from less than 2 percent in 1990. He believes that China’s economic growth over 1977-2010 has been “spectacular and unique.” While China’s growth has decelerated, the economy did expand at 6 percent, on average, between 2011 and 2022. This, he says, can be considered slow “only by China’s own historical standards”.

Prasad notes that, for many years, the Chinese government has attempted to rebalance the economy across many dimensions: from investment to consumption, from manufacturing to services and from extensive to intensive growth.

He concludes that, while the path has not been a smooth one, China has made significant progress towards raising the share of consumption in GDP and shifting production from manufacturing toward services.

Looking forward, Prasad recognizes the pressures that unfavorable demographics, high debt levels and an inefficient financial system can put on GDP growth.

He cites United Nations data indicating that, by 2030, China’s working-age population is expected to shrink at the rate of 1 percent per year. suggest that this would lead to GDP growth slowing by ½ a percentage point per year.

Prasad rightly believes that investment in education – increasing human capital – can provide an important offset to a shrinking labor force. I think he is right. Let me illustrate.

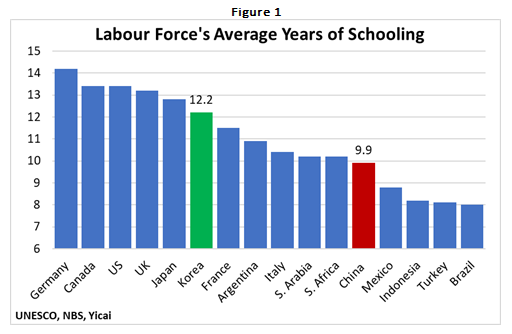

According to the , China’s working-age population had, on average,10 years of schooling in 2020, up from 9 years a decade earlier. Let’s assume that, by 2050, this rises to 12.2 years – where Korea is today (Figure 1). That’s an increase of 23 percent or 0.7 percent per year. If human capital is proportional to years of schooling, then the standard models suggest that more education can raise growth by 0.4 percentage points per year and offset four-fifths of poor demographics’ drag on growth.

Prasad is correct in saying that maintaining a high rate of productivity growth is key to ensuring robust economic development. He notes that China’s productivity growth had been fairly rapid but it slowed in the last decade. Productivity is difficult to measure and it remains to be seen how much of the recent slowdown is related to Covid and how much is due to longer-term structural factors.

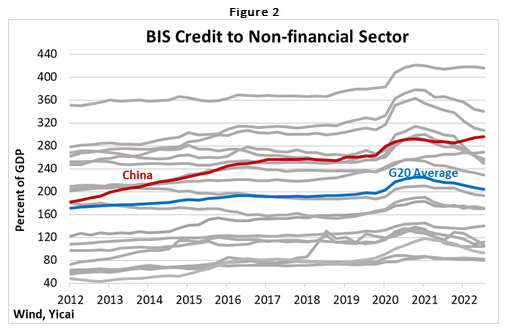

Of all of China’s vulnerabilities, the most eye-catching has been the rapid increase in its economy-wide indebtedness. Figure 2 shows the credit to the non-financial sector data for the G20 countries as compiled by the Bank for International Settlements. In 2012, the debt of China’s government, household and corporate sectors, expressed as a percent of GDP, ranked in the middle of the G20. By the third quarter of last year, China’s economy-wide indebtedness was the group’s fourth highest.

Prasad notes that most of China’s debt is denominated in renminbi and owned domestically, by banks and investors. This creates a lower level of fragility than external debt denominated in foreign currency and owed to foreigners. Foreign investors’ claims on China are 16 percent of GDP, far less than in most other emerging market countries. Moreover, less than half of this debt is denominated in foreign currency.

Even though China’s economy-wide debt is not an outlier, the high leverage in its real estate sector could be problematic. Property accounts for 60 percent of household wealth in China, double the share in the US. And mortgages have grown from about 30 percent of GDP a decade ago to slightly more than 60 percent more recently. Still, household savings rates are high and household deposits in the banking system were 94 percent of GDP in 2021, suggesting to Prasad that the risks are manageable.

Prasad believes it is unlikely that China’s financial system will suffer a meltdown as a result of the problems of highly-levered developers like Evergrande. With much of the banking system under state control, he feels the government has the resources to prevent a crisis.

In summary, Prasad says, “strains in financial and property markets could result in significant volatility but a financial or economic collapse is not in the cards.”

Turning to policy, Prasad uses tough language to emphasize the need to reform China’s financial system and make it better able to allocate capital and improve productivity. Indeed, he believes that China has generated sustained growth, improved the living standards of its people and avoided financial crises without a “well-functioning financial system.”

Prasad says that one of the key roles of the financial system involves “allocating capital to the more productive, dynamic, and employment-generating parts of the economy.” He believes that China’s financial system has been inefficient and that “many resources have been wasted over time.”

Is he right?

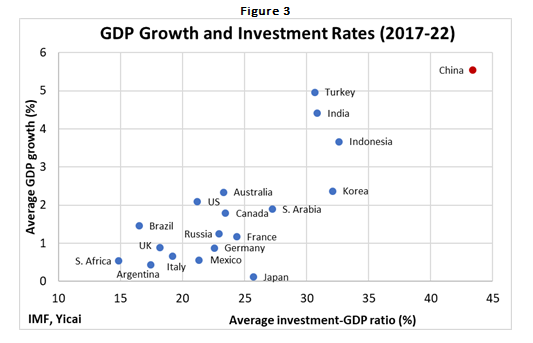

Figure 3 compares GDP growth and investment rates among the G20 countries. It uses average rates over 2017-2022. China stands out by having both the highest growth rate and the highest investment rate. The question is whether the growth China achieved was high enough given the resources it devoted to building the economy. If China’s misallocation of capital was egregious, then we would have expected it to have grown even faster.

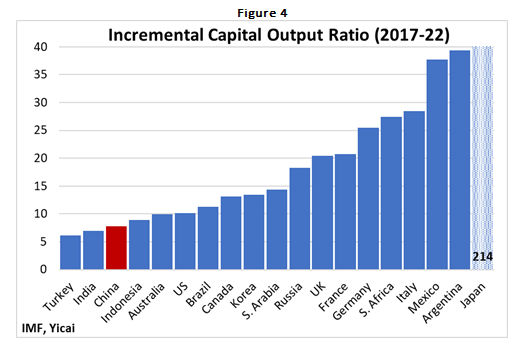

Economists have a way of assessing the efficiency of capital allocation at the macroeconomic level. It is called the Incremental Capital Output Ratio (ICOR). It can be calculated by dividing the investment rate by GDP growth. A lower number is better because less investment is needed per unit increase in GDP.

The ICORs for the G20 countries over the period 2017-2022 are presented in Figure 4. Note that I have truncated the observation for Japan because it is so high. Despite much more elevated investment rates than its peers, China’s ICOR is third lowest in the group. Moreover, it is about half of the G20 median. China’s low ICOR implies relatively little investment is needed to generate relatively high rates of growth. It suggests that, at the macro level, China’s capital is fairly well allocated.

Still, China’s ICOR has grown over time, in part, reflecting its slowing productivity growth. Like Prasad, I believe that it is crucial to raise productivity and that increasing financial sector efficiency is an important way to do this.

China’s financial system is bank dominated and Prasad sees bankers as responding to distorted incentives. They prefer to lend to state-owned enterprises, even if they are less credit-worthy than private firms. This is because the bankers believe the government will ultimately bail state-owned firms out if they get into trouble. Prasad says that solving this problem requires “weaning” state-owned enterprises off of bank credit.

I think that he is on to something here.

Banks have typically been seen as contributing to financial system efficiency because they have the incentive to monitor the behavior of borrowers and ensure that their loans are repaid. To the extent that China’s banks rely on the implicit guarantees inherent in state ownership, they cease to perform this important function.

I would propose that listed state-owned companies raise funding by selling bonds in financial markets, rather than by borrowing from banks. These enterprises are typically well-known firms that already provide information to the equity exchange. It should be easy for them to obtain credit ratings. Requiring them to sell bonds in financial markets would create space on bank balance sheets to lend to more productive private firms. At the same time, this would deepen China’s fixed-income markets.

Prasad says, “China’s growth model and approach to reforms have not hewed to conventional norms … .” Thus, the “underpinnings of China’s growth seem fragile from historical and analytical perspectives.”

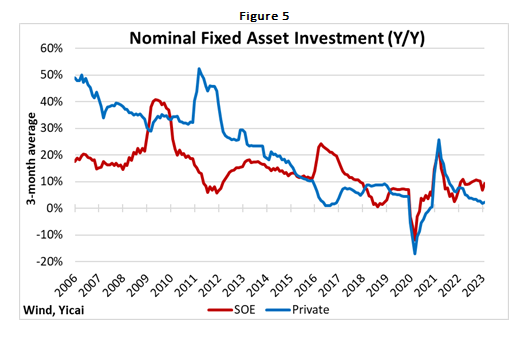

Much of China’s unique approach stems from its use of state-owned enterprises to provide counter-cyclical support to the economy when private investment demand is weak. This was done in 2009, 2016 and 2022 (Figure 5). In contrast, most advanced economies rely on monetary policy – often going to extraordinary lengths to get monetary conditions loose enough to stimulate demand. The fiscal and monetary approaches each have costs and benefits. Policymakers should carefully assess local conditions before they choose their poison.

To continue the miracle and avoid the malady, China needs to keep productivity growth high while reining in financial risks. These are the objectives that “high-quality development” is designed to achieve.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.