What Can We Learn from China’s Provincial-Level GDP Targets?

What Can We Learn from China’s Provincial-Level GDP Targets?(Yicai) March 2 -- China’s GDP target for 2026 is due to be announced during March’s Two Sessions, the annual meetings of the National People’s Congress and the National Committee of the Chinese People's Political Consultative Conference.

The GDP target is the cornerstone of China’s macroeconomic management. While China is not unique in targeting an annual rate of GDP growth, most major economies target inflation and there are both similarities and differences between these frameworks.

Inflation targeting aims for a stable growth of prices by keeping aggregate demand in line with aggregate supply (potential output).

Aggregate supply depends on the rather slow-moving trends in capital, labour and technology. Due to shifting expectations of domestic investors and consumers and idiosyncratic developments abroad, aggregate demand is more volatile.

Inflation targeting relies on a single tool, monetary policy. Central banks adjust monetary conditions – the levels of interest rates and the exchange rate – to minimize the deviation between aggregate demand and aggregate supply.

Most central banks target a given rate of inflation, say 2 percent. Annual deviations from this target are tolerated within a prescribed range, say 1 percentage point on either side of the target.

China’s GDP targeting framework has evolved over the last 20 years.

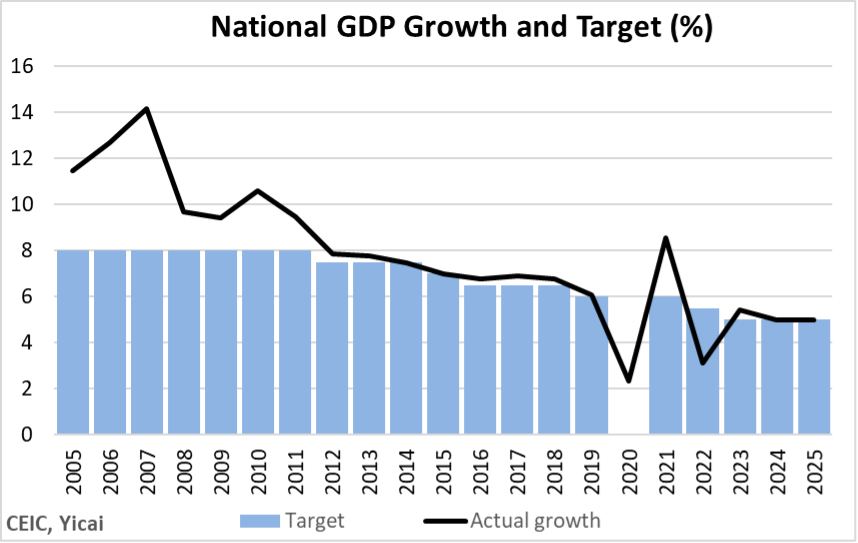

Between 2005 and 2011, the authorities targeted 8 percent GDP growth (Figure 1). Eight percent was seen as the minimum rate of GDP growth needed to provide enough employment for the large number of new entrants into the labour market. During this period, actual GDP growth exceeded 8 percent. Rather than a forecast, the target was seen as the floor that would trigger a policy response should it be breached.

China’s working-age population peaked in 2012 and the authorities began reducing the GDP target in line with the slowing of aggregate supply. Note that no target was set in 2020.

Figure 1

The authorities continue to take a long-term view on the growth of aggregate supply. For example, over the next ten years, they expect GDP to grow at an average annual rate of 4.17 percent. The authorities connect this long-term view with recent actual growth and they obtain an annual profile for aggregate supply growth.

To ensure that aggregate demand converges with aggregate supply, China’s policymakers use fiscal as well as monetary policy. Through the targeting process, sub-national growth targets are aligned with those at the national level. This allows the authorities to marshal local as well as national fiscal resources to ensure that the targets are met.

China’s GDP growth targets are meant to be achieved on an annual basis and there has typically been limited tolerance around the target.

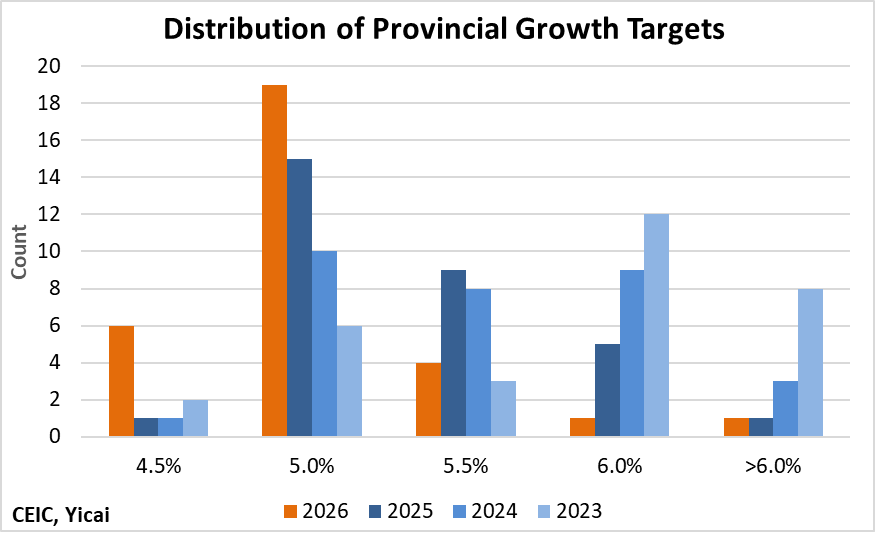

All 31 of China’s province-level governments have released their growth targets for 2026. Since China’s fiscal policy is decentralized, with local governments accounting for 85 percent of on-the-books government spending, we should expect that the provincial-level GDP growth targets tell us something about the national target.

Over 2023-2025, the central government’s target has been steady at around 5 percent. Nevertheless, the median provincial-level target fell from 6.0 to 5.5 to 5.0 percent over this period. While the median provincial-level target has remained at 5 percent this year, those of the individual provinces have clustered more tightly around 5 percent (Figure 2). Only six provincial-level governments are targeting rates above 5 percent, compared to fifteen last year. Moreover, six expect growth below 5 percent, compared to only one or two in recent years.

Figure 2

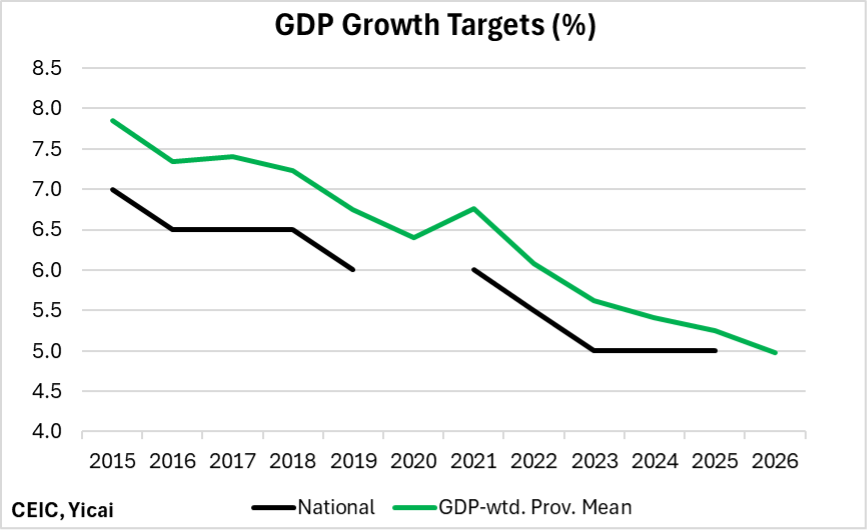

China’s province-level jurisdictions are far from equal in economic size. The GDPs of the two biggest, Guangdong and Jiangsu, are each roughly as big as the eleven smallest. So, perhaps a GDP-weighted mean is better than the median in thinking about the impact of the provincial-level targets. On this basis, the provincial-level targets have exceeded the national target by 0.67 percentage points, on average, over the last decade (Figure 3).

In 2025, the provincial-level GDP-weighted mean was 5.25 percent, compared to the 5 percent national target. This year, the GDP-weighted mean target is 5.0 percent. Recent differences between the provincial-level GDP-weighted mean and the national target suggest that the central government could be looking for growth in the 4.5 to 4.75 percent range.

Figure 3

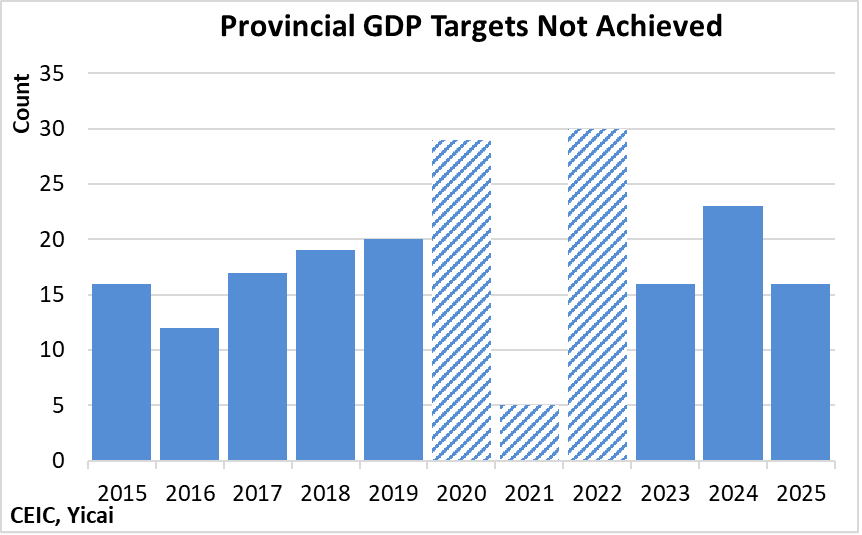

It is important to note that the provincial-level jurisdictions rarely meet their GDP targets. Last year, 16 of the 31 province-level jurisdictions failed to achieve them. Abstracting from the Covid years, this failure rate was not uncommon (Figure 4).

Figure 4

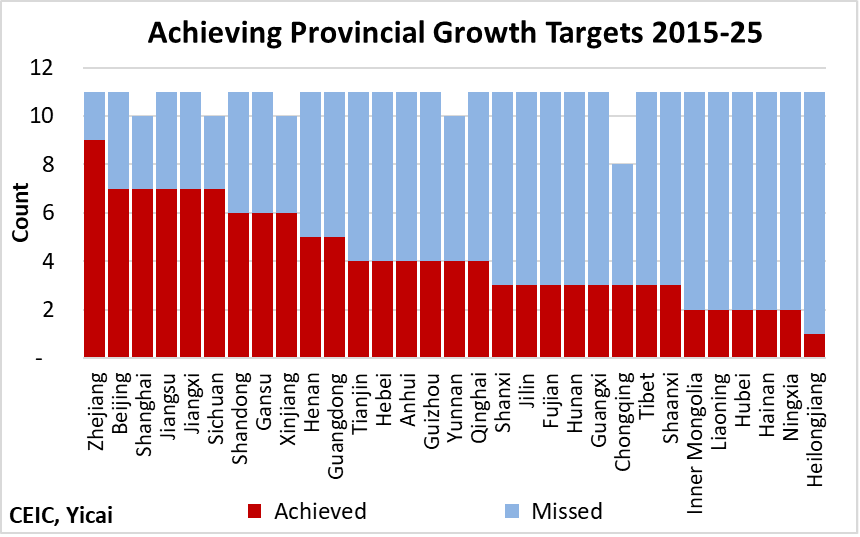

Some provincial-level jurisdictions have been better than others at meeting their GDP targets over the last 10 years (Figure 5). Zhejiang has an 82 percent success rate, while Heilongjiang only met its target once out of the last eleven tries. In general, it seems that richer jurisdictions are more successful than the poorer ones.

Figure 5

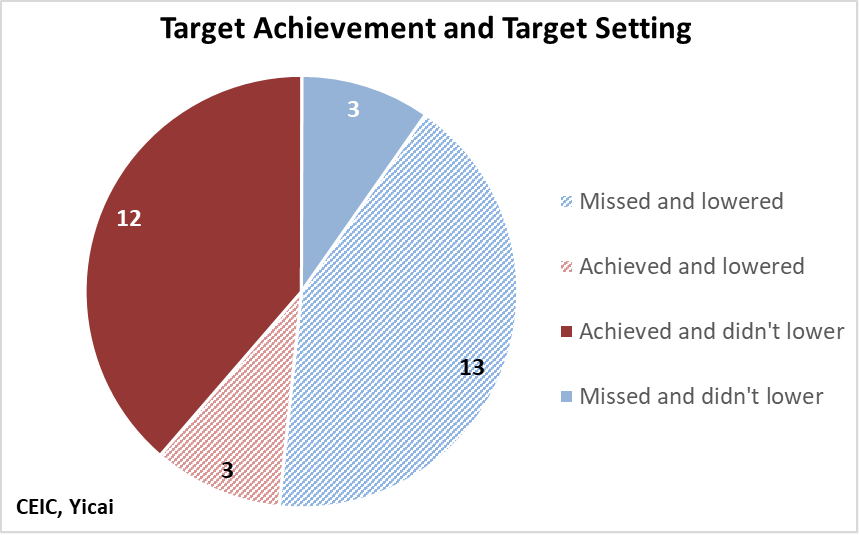

Most of the provincial-level jurisdictions that missed their targets last year set lower ones this year (Figure 6). But Shanxi, Hainan and Qinghai were undeterred by their failure and kept their targets unchanged. Most of the jurisdictions that achieved their targets in 2025 kept them unchanged in 2026. However, Zhejiang, Henan and Anhui lowered their 2026 targets despite their success in 2025. No jurisdiction raised its target this year.

Figure 6

As noted above, provincial-level targets typically exceed those set for the country as a whole. Some observers have suggested that this aiming high gives local governments the ability to over-achieve while reducing the penalty for failure as long as local growth exceeds the national target.

However, this strategy may not be costless. Zheng et al suggest that, in order to meet their growth targets, local governments frequently sell land to finance additional investment. While the local economy grows, it does so at the expense of increased urban sprawl and a loss of high-quality arable land. The authors note that with the shift to “high-quality development” in 2017, the incentives for local officials changed and the impact of targets on urban sprawl was reduced.

Similarly, looking across cities, Chang et all find that when a jurisdiction’s actual GDP growth fell one percentage point below its target, the local government increased its debt-to-GDP ratio by 0.76 percentage points. The authors say that while the additional debt finance stabilized economic output, it did so by increasing financial fragility.

So, what do the provincial-level GDP targets tell us?

First, the GDP-weighted mean suggests that the national GDP target will be set in the 4.5 to 4.75 percent range.

Second, the shrinking gap between the provincial-level and national targets suggests that there will be less pressure on local governments to over-achieve and that this should improve the quality of growth.

Inevitably, some will look at the data in Figure 1 and conclude that it is impossible for the Chinese authorities to always hit their targets and, therefore, the data are manipulated. Indeed, this is an open question among academics.

In assessing China’s data veracity, we must remember that the Chinese policymakers have more and more powerful tools at their disposal for macroeconomic management than their counterparts in other major economies.

My own view, based on data arms-length from the government, is that the Chinese authorities have not overstated GDP growth in recent years. My assessment squares with a recent paper by economists at the Federal Reserve’s Board of Governors. They conclude that the official figures have not recently been overstating GDP growth for three reasons. First, the GDP data have become less smooth since the pandemic. Second, their alternative indicator closely tracks official GDP. Third, the supply side of China's economy has performed remarkably well in the context of robust demand for Chinese goods and industrial policies promoting self-reliance.

There could be a case for the authorities to target a range for GDP growth on an annual basis, say 4.5 to 5.0 percent. Given all the shocks to which an economy is subject, targeting a range would permit a more gradual policy response while still achieving the target for aggregate supply over the medium term.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.