What Do March’s Two Sessions Tell Us About China’s Economic Policies?

What Do March’s Two Sessions Tell Us About China’s Economic Policies?(Yicai) March 16 -- China’s Two Sessions – the annual meetings of its legislative and advisory bodies – are always informative as they set out the key policy priorities for the current year. With the unveiling of the 15th Five-Year Plan, this year’s meetings also established the economic and social development goals for 2026-30.

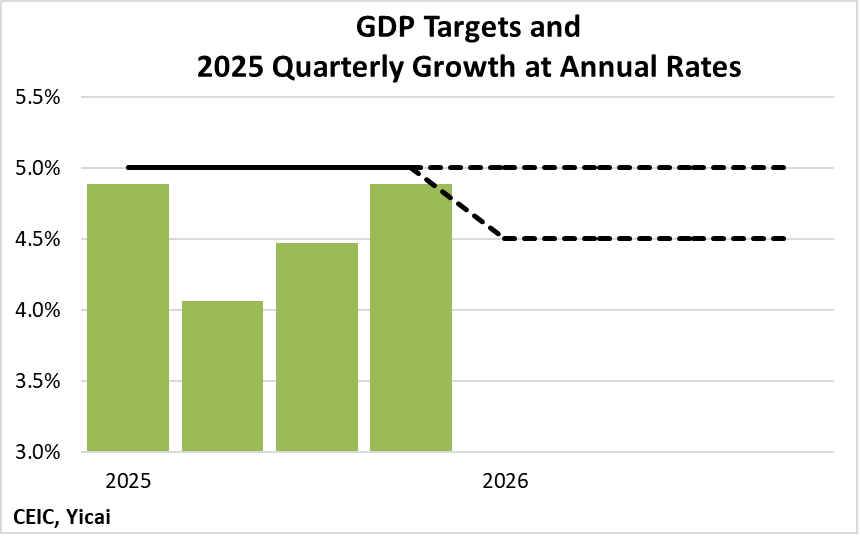

The government’s target for GDP growth is the keystone for its near-term macroeconomic framework. This year’s target was set as a range – between 4.5 to 5.0 percent – broadly in line with expectations following the release of the provincial-level targets. The target for 2025 was “around 5 percent”, so 2026’s target shows that policy makers are comfortable with somewhat slower growth.

This is the third time in recent years that policymakers have set the growth target as a range instead of a point. They choose a range when the economic outlook is unusually uncertain. Following the financial market turbulence in 2015, a range of 6.5 to 7 percent was set in 2016. Similarly, in 2019, a range of 6 to 6.5 percent was set after President Trump had imposed large tariffs on China in 2018. No target was set in 2020 because of the pandemic.

The best predictor for GDP in 2026 is the quarter-over-quarter growth in 2025, expressed at annual rates (Figure 1). The average of the four quarters was 4.6 percent, which is at the lower end of 2026’s range. Moreover, growth in Q2 and Q3 fell below 4.5 percent. This recent momentum suggests the target could be difficult to achieve.

Figure 1

However, there are some signs that this year will be less challenging than 2025.

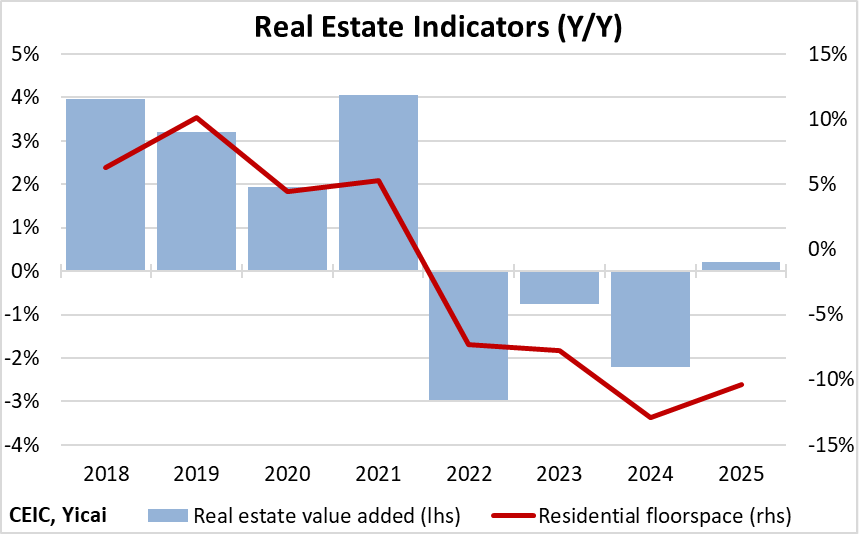

First, the worst may be behind us in the residential property market.

The value added of the real estate sector, which includes existing, as well as newly-built property, turned slightly positive in 2025, following three years of decline. Residential floorspace under construction continued to fall rapidly in 2025, but its rate of decline was smaller than in 2024, indicating that it took less off of growth (Figure 2).

Figure 2

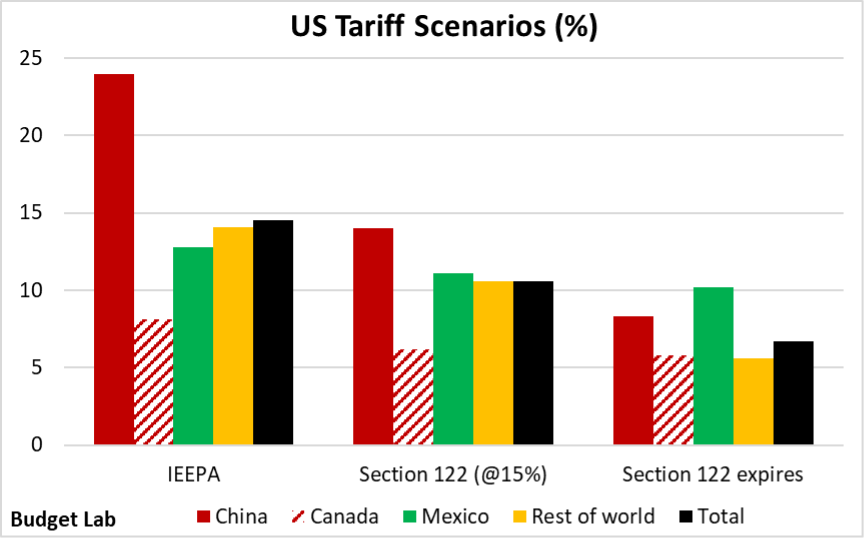

Second, China’s relationship with the US is improving.

Presidents Xi and Trump had a positive meeting in Busan, South Korea in October at which they agreed to de-escalate trade tensions. There were useful follow-up phone calls in November and February. And President Trump is due to visit Beijing later this month.

In addition, China appears to be a major beneficiary of the US Supreme Court’s decision to eliminate the International Emergency Economic Powers Act (IEEPA) tariffs. Before the Supreme Court decision, the tariffs applied against China were significantly higher than those on other countries (Figure 3). Under the Section 122 tariffs, that gap shrinks significantly. The Section 122 tariffs are time-limited. Should they be allowed to expire, the gap would shrink even further, with the rate on China falling below that on Mexico.

Figure 3

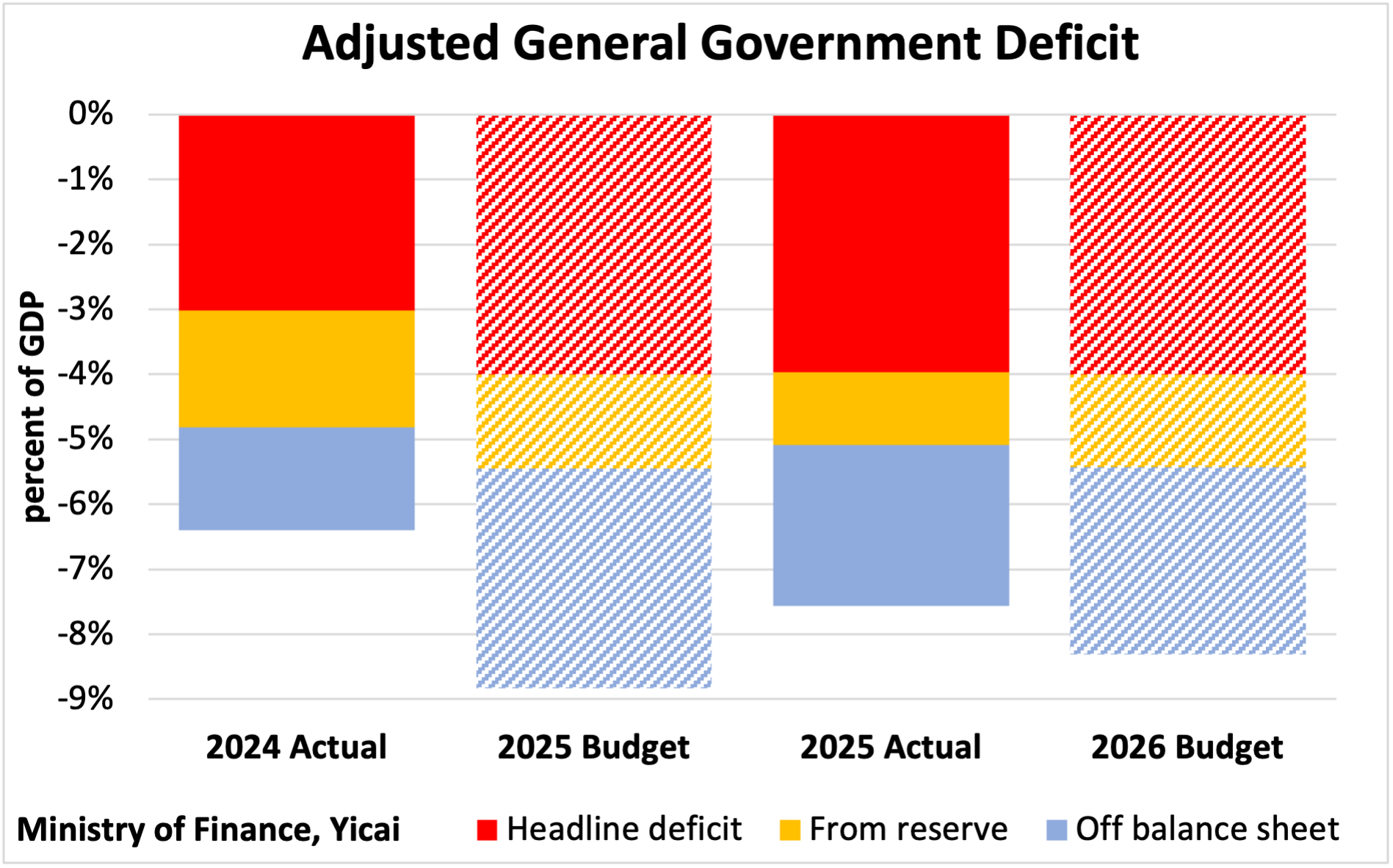

It is clear from the Budget document that policymakers feel the economy’s cyclical position remains weak. They plan continued fiscal support, albeit less than in 2025.

Adding the drawdown from fiscal reserves to the headline deficit gives the fiscal balance on a cash basis, which is a better measure of its macroeconomic impact than the accrual deficit. For a complete picture of the fiscal impulse, Figure 4 consolidates the three off-balance sheet accounts – those of the government managed funds, the state capital budgets and the social security system – with the cash deficit.

Fiscal stimulus can be estimated as the difference in the adjusted government deficit as a percent of GDP from period to period or from budget to previous period. On this basis, it is worth noting that fiscal policy was much less stimulative than planned last year. The budgeted stimulus was 2.4 percent of GDP (2025 Budget minus 2024 Actual). But the actual stimulus was only 1.2 percent of GDP (2025 Actual minus 2024 Actual). This year, the planned stimulus is 0.8 percent of GDP (2026 Budget minus 2025 Actual).

Figure 4

Not only will fiscal policy be stimulative, according to Premier Li Qiang’s Work Report, monetary policy will also be “appropriately accommodative”. Policymakers are targeting 2 percent inflation, which will be a challenging goal since the increase in the consumer price index has been close to zero for the past three years.

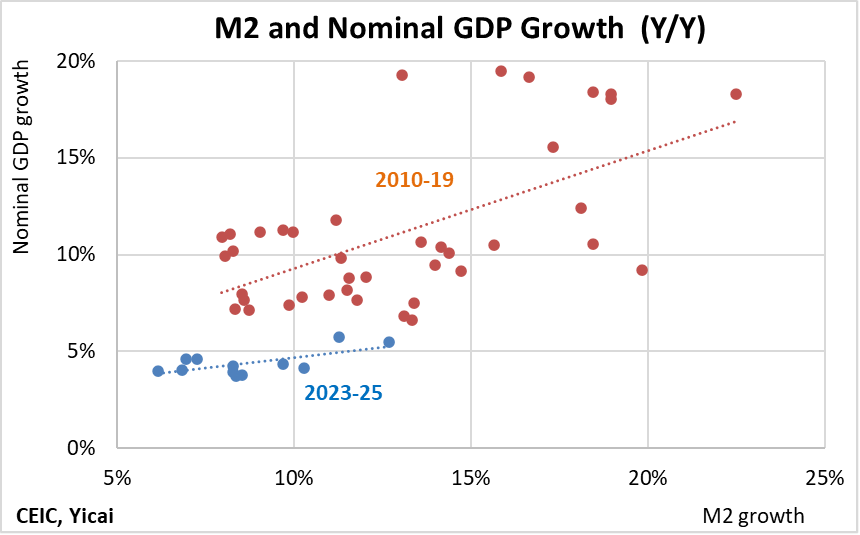

The data show that monetary policy has lost power since the pandemic. Between 2023 and 2025, about three times as much growth in M2 was needed to produce the same increase in nominal GDP as over 2010-19 (Figure 5). Policymakers understand this and, in order to smooth the channels of monetary transmission, they commit to developing “new and better structural monetary policy instruments, scale them up as needed, and refine the ways they are used.”

Figure 5

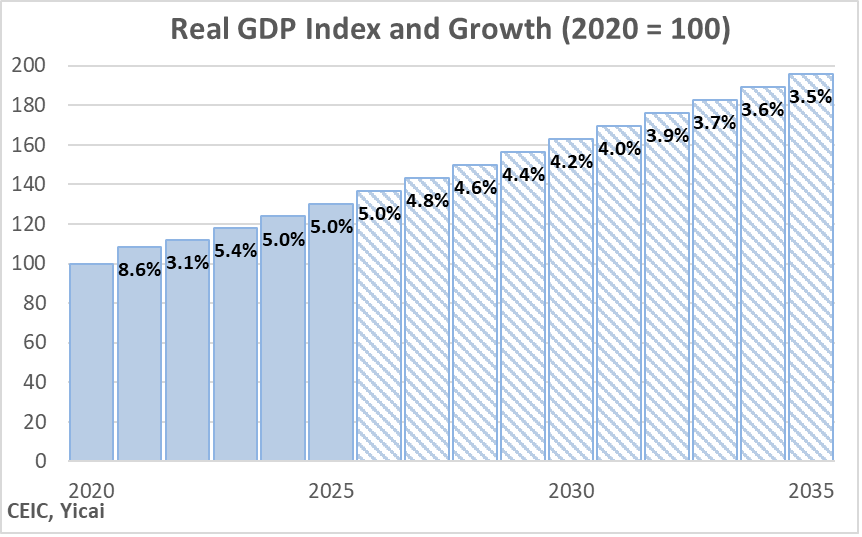

The 14th Five-Year Plan did not specify a GDP growth target. Similarly, no growth target is set for 2026-30 under the 15th Plan. The policy anchor here is reaching moderately developed country status by 2030. Policymakers operationally define this objective as doubling per capita income between 2020 and 2035. Given actual growth between 2020 and 2025, China's economy would need to grow at an average annual rate of 4.17 percent from 2026 to 2035, which covers the 15th and 16th Five-Year Plan periods.

Using a linear interpolation for real GDP between 2025 and 2035, growth would have to remain in the 4.5 to 5.0 percent range for the next three years before slowing gradually to 3.5 percent as the target is reached (Figure 6).

Figure 6

Perhaps more important than the growth of the economy is the way in which this growth is achieved. In his Work Report, Premier Li sets out four strategic tasks for the 15th Five-Year plan.

First, high-quality development will be pursued. The industrial system will be modernized with an emphasis on advanced manufacturing. Innovation and breakthroughs in core technologies are sought. There is a recommitment to peaking carbon emissions before 2030.

Second, the domestic economy will be strengthened. Investments will be made in both physical assets and people to raise household consumption as a share of GDP and expand effective capital spending. Local protectionism and market segmentation will be eliminated and a unified national market will be developed.

Third, common prosperity for all will be advanced. China will be made more childbirth-friendly. The average years of schooling will be raised. Life expectancy will be increased. The system of income distribution will be improved.

Fourth, both development and security will be ensured. The supply capacity for food, energy and resources will be improved. The risks arising from real estate, local government debt and medium-sized local financial institutions will be addressed.

There is a sense among some western analysts that the 15th Five-Year Plan is too focused on the supply side and doesn’t do enough to boost domestic consumption so as to address over-capacity and reduce trade tensions. Some point to low government spending on education, health and social security as leading to excessive precautionary saving and insufficient household consumption.

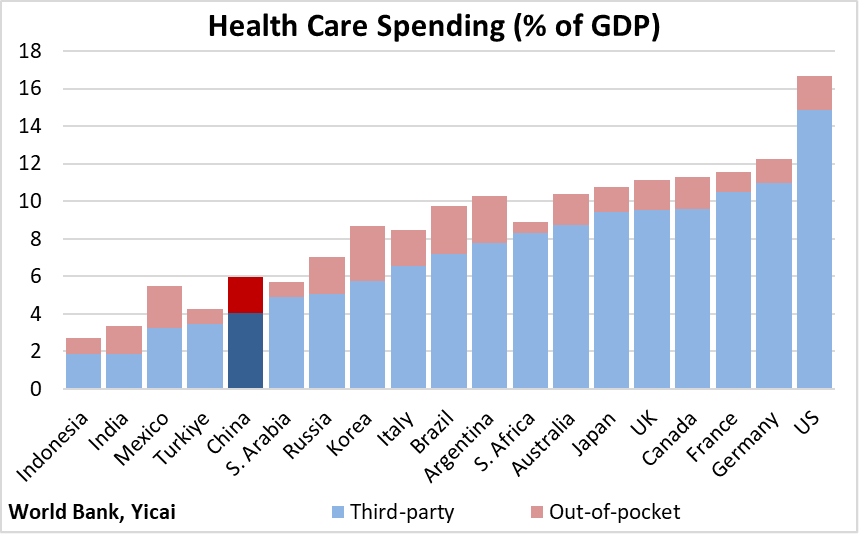

China’s social spending is low by global standards. Nevertheless, while inputs are modest, outputs are reasonable, suggesting a high degree of efficiency.

China’s third-party spending on health – through private or public insurance schemes – is low compared to other G20 countries (Figure 7). Moreover, the share of out-of-pocket spending born by patients to overall health spending is the fourth highest among its G20 peers.

Figure 7

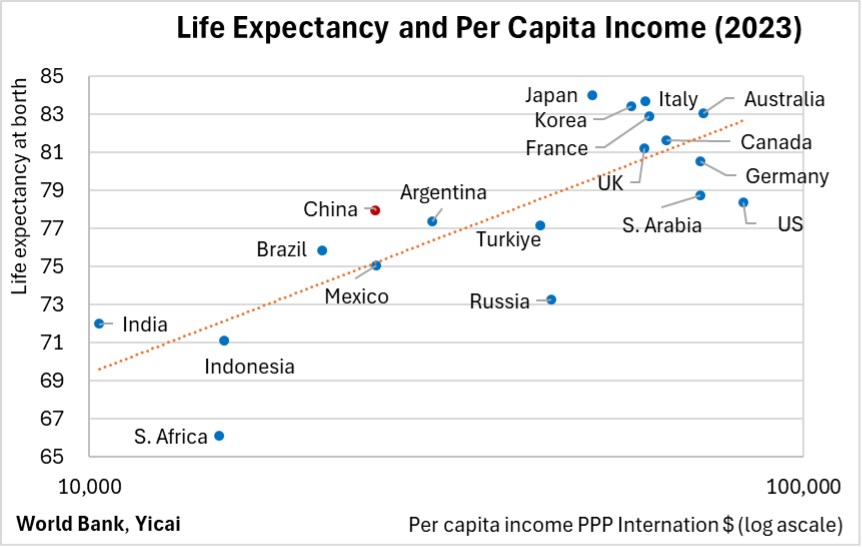

Nevertheless, China’s health care outcomes are pretty good. Figure 8 shows that life expectancy rises with per capita income across the G20 countries. Still, there is a lot of individual country-variance around this trend. Life expectancy in China is 2.3 years higher than one might expect for a country at its level of per capita income. Japan, Italy and Korea are also outliers in this regard. On the other hand, life expectancy in Russia, South Africa and the US is significantly less than these countries’ per capita income would predict.

Figure 8

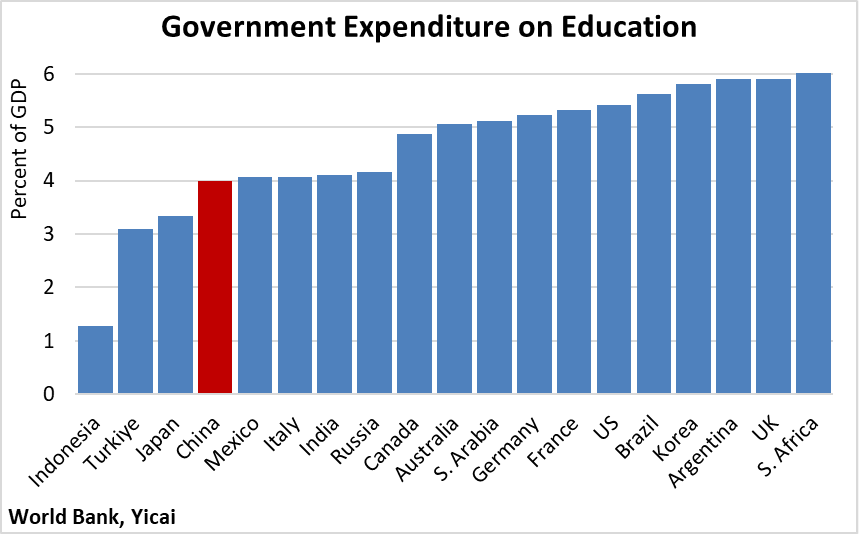

The Chinese government spends 4 percent of GDP on education. This is less than the G20 median of 5.1 percent of GDP (Figure 9).

Figure 9

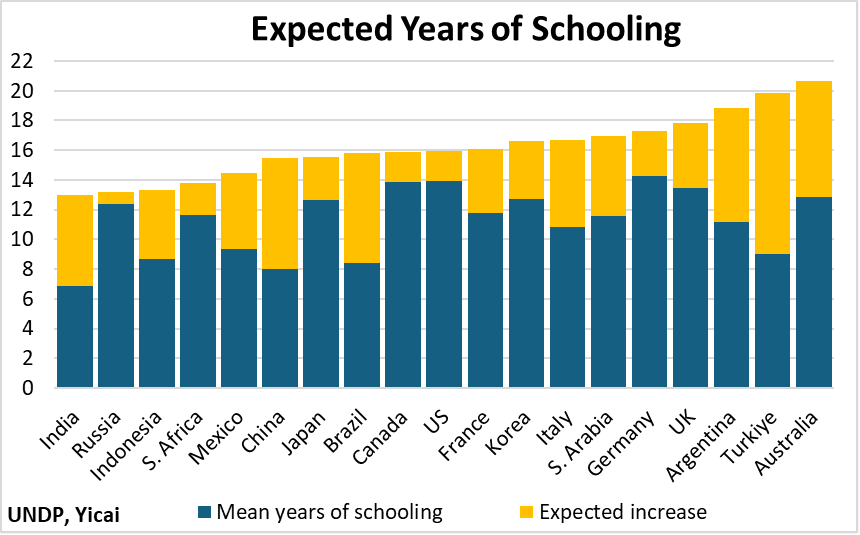

In China, those 25 years-old and older, on average, have only 8 years of schooling, well below the G20 mean of 11.6 years. However, due to years of ramping up educational opportunity, a Chinese youngster entering school this year can expect to receive 15.5 years of schooling. This is not far behind the G20 median of 15.9. Indeed, China’s increase in expected years of schooling is among the highest in the G20.

Figure 10

In a recent Working Paper, economists at the IMF have explored the extent to which increased social spending in China can support consumption. They find that additional government spending on education does not reduce household savings. More government spending on health and social security reduces savings for rural households only. However, the elasticity is low. They estimate that raising health and social security spending by a cumulative 15 percentage points of GDP over five years only leads consumption to increase by a cumulative 2.4 percentage points of GDP over the same period. It seems that these social interventions, which could be justified on their own merits, are less effective in stimulating consumption than a well-designed programme of coupons.

Chinese policymakers believe that, over the long run, household consumption depends on household income and the best way to raise incomes is by increasing productivity. New Quality Productive Forces means employing workers in those industries that create high value-added products.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.