What Explains the Turnaround in Chinese Industrial Profits?

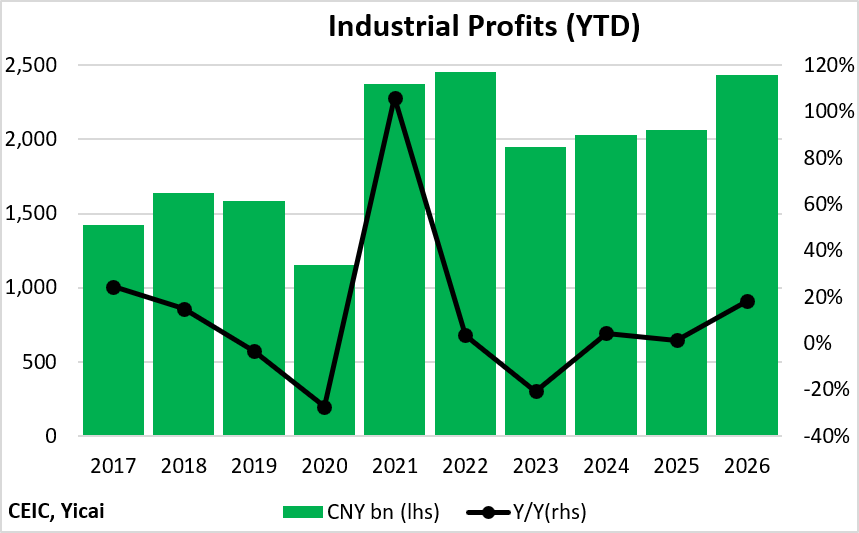

What Explains the Turnaround in Chinese Industrial Profits?(Yicai) June 22 -- In the first four months of the year, China’s industrial firms have recorded a striking turnaround in their profitability. In aggregate, industrial enterprises made CNY 2.4 trillion, up 18 percent from the January-to-April period in 2025 (Figure 1).

Industrial profits are highly cyclical. They surged in 2021–22, when exports expanded vigorously, as China’s economy proved more resilient to pandemic-related disruptions than those of other major countries. The fall in profits in 2023 was consistent with the drop in exports that year. Looking through the cyclicality, industrial profits have increased at about the same rate as GDP. Between 2017 and 2026, profits rose by an average annual rate of 6 percent.

Figure 1

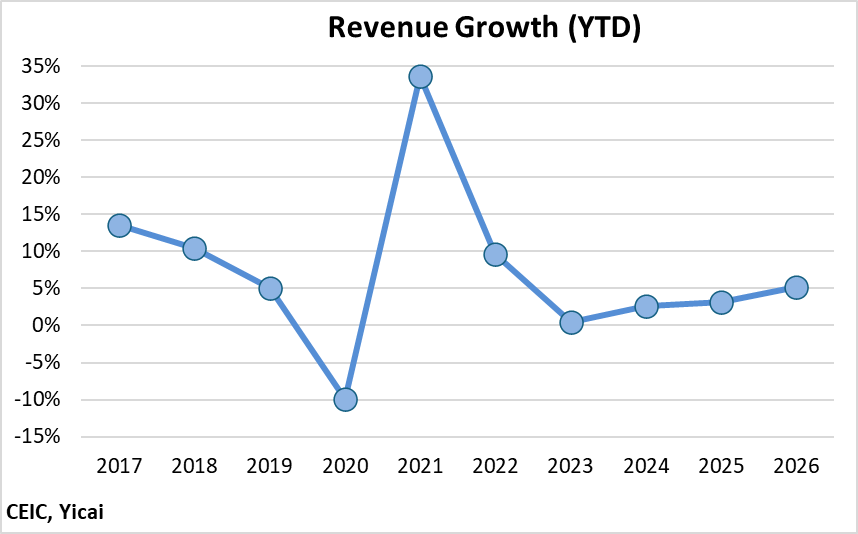

There are, essentially, two ways to grow profits. Revenue can increase or profit margins – the amount of profit per unit of revenue – can expand.

In the first four months of the year, industrial firms’ revenues rose by just over 5 percent. This was somewhat more rapid than the 3 percent increase recorded in the January-to-April period in both 2024 and 2025. However, revenue growth this year remains significantly slower than the 10 percent growth over 2017-19 (Figure 2).

Figure 2

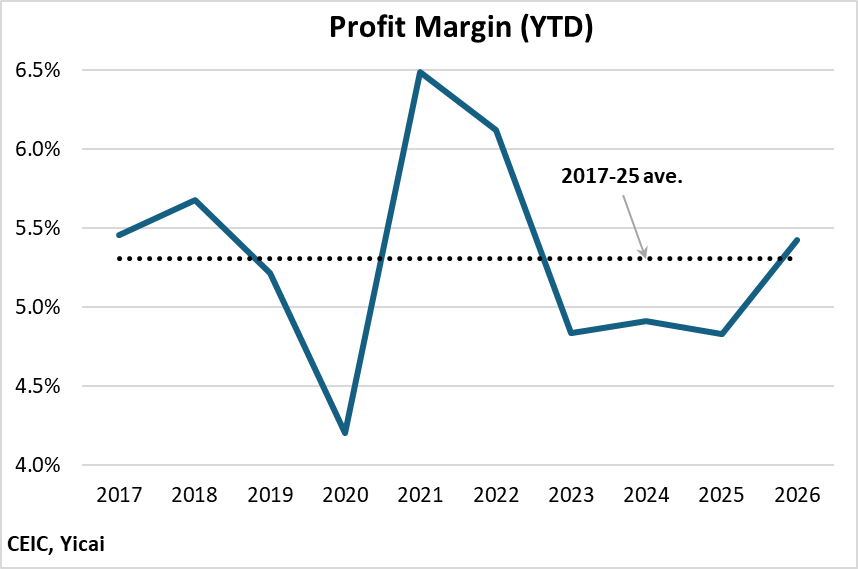

Profit margins, which have been depressed over the last three years, widened to 5.4 percent, or a touch higher than the 2017-25 average (Figure 3).

Figure 3

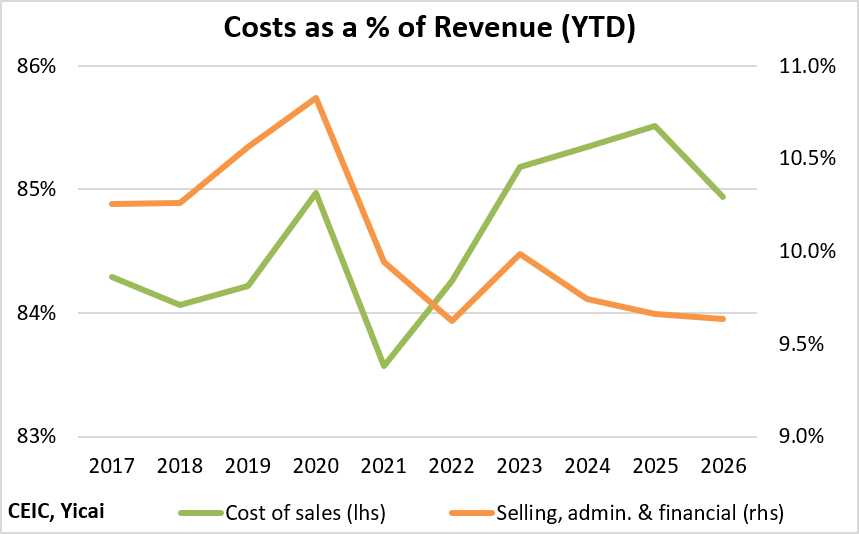

The improvement in profit margins arose from tighter cost control. Firms’ Cost of Sales (materials, labour, and manufacturing overhead) has been drifting upward as a share of revenue over time. However, it has dipped in early 2026, pointing to improved operational efficiency (Figure 4). Selling, administrative, and financial expenses, which are smaller as a share of revenue, have continued their long-term decline, ticking down this year.

Figure 4

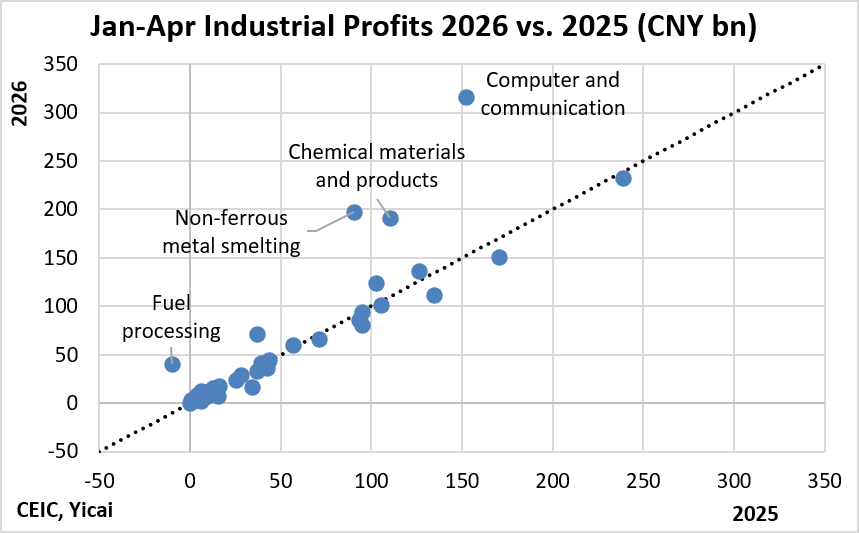

To see which industrial sectors have made the largest contribution to the turnaround in profitability, we plot the level of profits in the first four months of 2026 against those made in the first four months of 2025 (Figure 5).

Four industries stand out as being well above the 45-degree line that indicates equal profits in both periods: computers and communication equipment, chemical materials, non-ferrous metals smelting, and fuel processing.

Figure 5

The profits of the computer and communication equipment sector more than doubled, accounting for more than 40 percent of the improvement in industrial firms’ profitability so far this year. Revenue growth accelerated from 10 to close to 16 percent, while margins improved by 1½ percentage points to 5.4 percent.

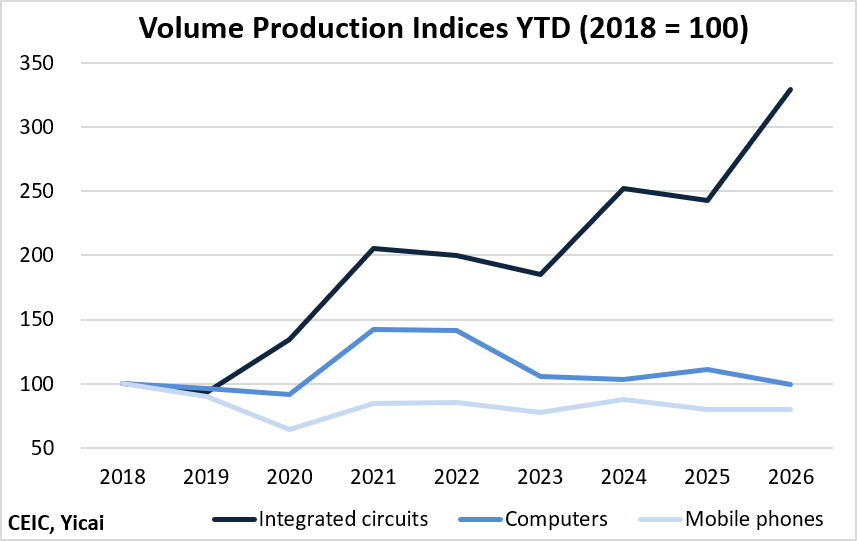

The sector is benefitting from the strong demand for integrated circuits. In volume terms, integrated circuit production jumped 36 percent from the same period in 2025 and stands more than three times as high as in 2018 (Figure 6). The prices of integrated circuits have also increased sharply. In contrast, the volume of computers produced, so far this year, is the same as eight years ago, while the volume of mobile phones is 20 percent lower.

Figure 6

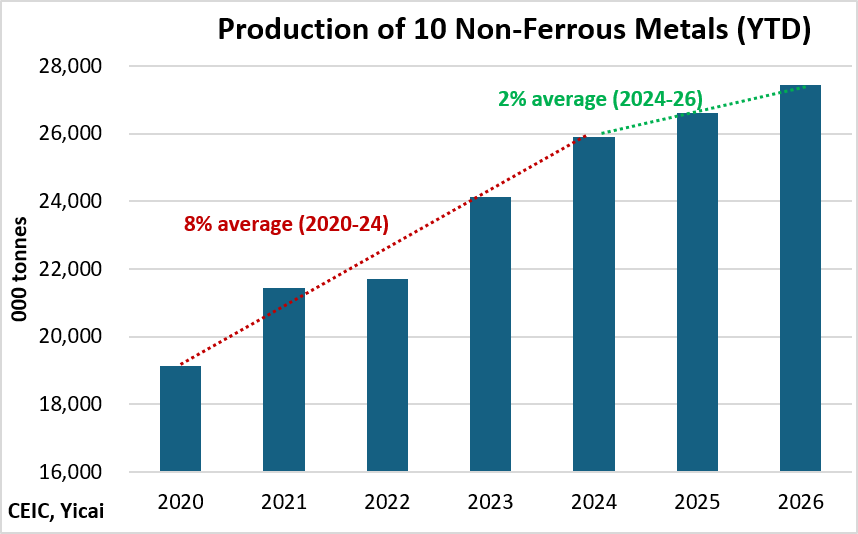

Profits in non-ferrous metal smelting have also more than doubled. In an effort to rein in oversupply and promote efficiency, the Ministry of Industry and Information Technology set a cap on non-ferrous metal output. As a result, production has only increased at an average annual rate of 2 percent since 2024, a significant slowdown compared to the 8 percent average posted over the previous four years (Figure 7).

Figure 7

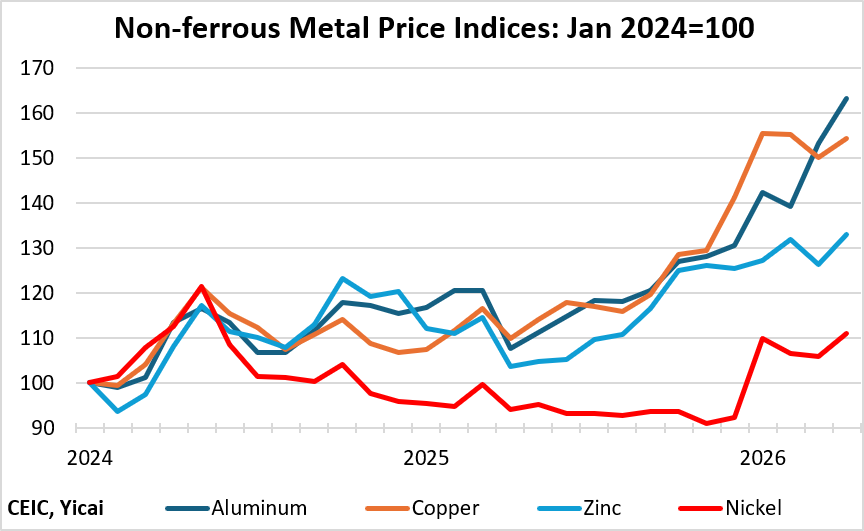

Demand for non-ferrous metals remains robust, including for inputs into EVs, power grids, green infrastructure, semiconductors and electronics. This led non-ferrous metal prices to rise rapidly in the second half of 2025 (Figure 8).

Figure 8

These high prices permitted firms to increase revenues by 6 percentage points to 24 percent even though production only increased modestly. A reduction in competitive pressure allowed margins to rise to 5.4 percent, so far this year, up from 3.1 percent in 2025.

Profits in the chemical materials sector were up 73 percent. Revenue growth increased by 6 percentage points to 9 percent and margins improved from 3.9 to 6.1 percent. Margins expanded on as a result of the much higher prices of ethylene and sulfuric acid, two of the sector’s major outputs. Supply disruptions in the Strait of Hormuz constrained the flow of sulphur, naphtha and liquid petroleum gas, which are key feedstocks for these chemicals. But, given the short supply globally, the increased cost of feedstock was more than offset by higher selling prices of finished chemicals.

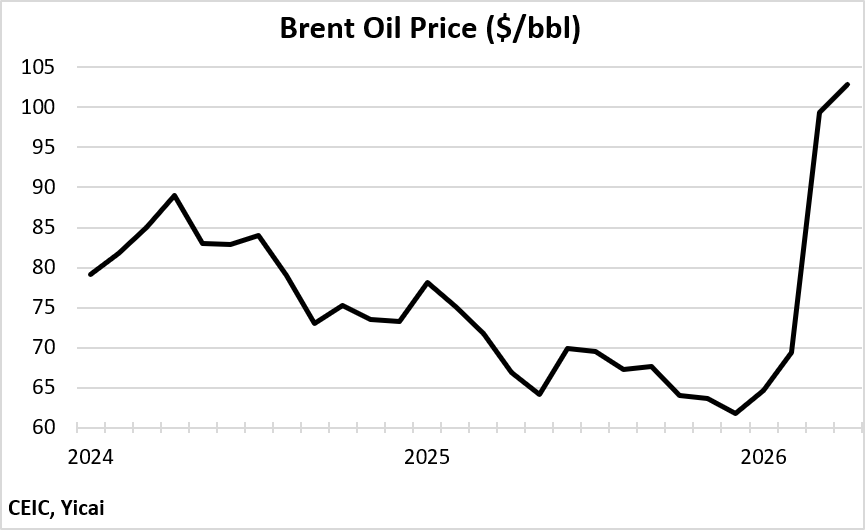

Even though margins were a thin 2.2 percent, the fuel processing industry has returned to profitability this year after posting losses in the January-April period in 2025 and 2024. Revenues did not grow, but that was an improvement on the 10 percent decline last year. Some of this newfound profitability could be temporary. The sharp rise in global crude oil prices (Figure 9), driven by Strait of Hormuz disruptions and Middle East tensions, increased the value of refiners’ existing crude inventories. This created a significant one-time inventory holding gain that boosted reported profits, even as new crude purchases became more expensive.

Figure 9

The turnaround in industrial profits may not prove sustainable.

The computer and communication equipment sector does appear well-positioned for continued strong profitability, underpinned by robust demand for integrated circuits and related components.

However, the gains in chemical materials, non-ferrous metals smelting, and fuel processing are more vulnerable. While supply disruptions in the Strait of Hormuz have, so far, allowed producers to pass on higher feedstock and input costs, any normalization of global supplies — or renewed weakness in domestic demand — could reverse these price gains and compress margins.

China’s unique position as the world’s dominant manufacturer provides some insulation to shocks like the closure of the Straight of Hormuz. The enormous scale of its production gives it significant bargaining power in sourcing inputs. Its oil companies are vertically integrated, which means that their upstream profits can cushion compression in refining margins. China has cultivated relationships with a wide spectrum of countries that allow it to diversify its sources of supply. It levers diplomacy and finance to secure long-term supply contracts. And its strategic reserves for oil and other commodities give it an important buffer against short-term supply disruptions.

Ultimately, a durable recovery in industrial profits will depend on continued strong demand and ongoing measures to improve efficiency rather than reliance on temporary price windfalls.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.