Will Wrangling Over the US Debt Limit Help Internationalize the Renminbi?

Will Wrangling Over the US Debt Limit Help Internationalize the Renminbi?(Yicai Global) May 15 -- More and more countries are looking to trade with China in yuan (CNY) instead of US dollars.

and have put the financial infrastructure in place to facilitate trade in CNY. is trading more extensively with China and settling these trades in CNY. China is in talks with to price crude oil sales in CNY. The move to accept CNY payments is not limited to emerging market countries. In March, France’s completed the first CNY-settled liquid natural gas trade through the Shanghai Petroleum and Natural Gas Exchange.

From China’s point of view, more widespread use of the CNY for international transactions offers clear benefits.

Foremost among these is the reduction of currency risk. Chinese exporters typically incur production costs in CNY but receive payments in US dollars. Similarly, its importers pay for their goods in US dollars yet sell them in the domestic market for CNY. Thus, both importers and exporters are exposed to currency fluctuations, which can be costly and difficult to hedge. Settling foreign trade in CNY helps Chinese companies by reducing exchange rate risk as well as eliminating the cost of purchasing foreign exchange.

Second, greater use of the CNY can help maintain trade finance during turbulent times. During crises, there is a flight to high-quality US dollar assets, typically government securities. As US-dollar liquidity tightens, trade finance can dry up. The shortage of trade finance was very evident in 2008-09 and it had a detrimental effect on China’s ability to export. Chinese financial institutions – whose funding base is in CNY – only have a limited ability to provide dollar-denominated trade finance before they incur sizable currency mismatches. To the extent that exports and imports can be settled in CNY, their ability to fund trade increases as does their role in stabilizing production and exchange.

Third, internationalizing the CNY will help further develop China’s financial sector. Internationalizing the CNY essentially means deepening the process of using Chinese financial markets as a platform for the rest of the world’s borrowing and lending. This requires providing sophisticated services and necessitates creating high-value-added financial sector jobs. The growth of the financial sector would raise the quality of Chinese services as well as transform Shanghai into a truly international financial center.

The CNY need not displace the dollar as the world’s reserve currency for China to reap these benefits. Foreigners simply need to be convinced that the CNY is a solid store of value, a dependable medium of exchange and the currency of choice when doing business with China.

Indeed, the CNY is increasingly being used for China’s cross-border payments.

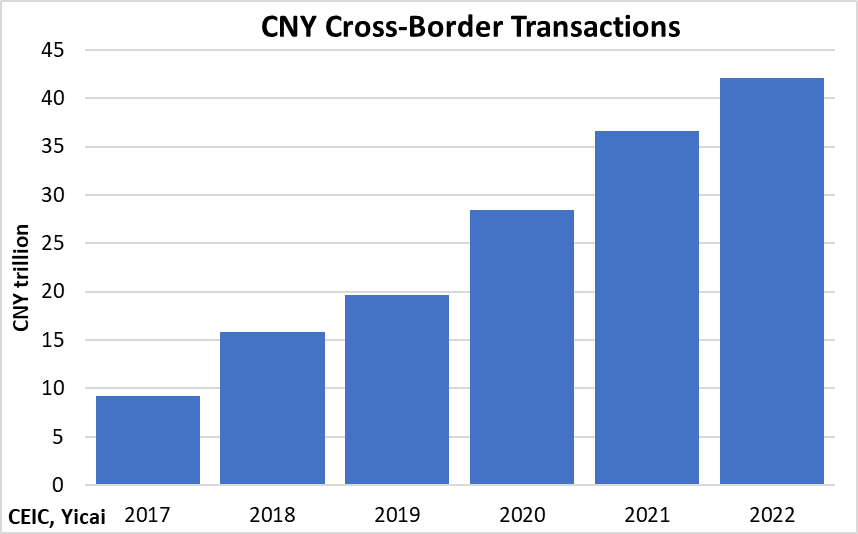

In 2022, CNY-denominated cross-border payments reached CNY42 trillion, up 15 percent from 2021. Since 2017, China’s CNY-denominated payments have grown more than fourfold (Figure 1). reported that 48 percent of China’s cross-border payments were made in CNY in March. For the first time, more of China’s cross-border payments were made in CNY than in US dollars. Bloomberg noted that in 2010, 83 percent of these payments were effected in US dollars and nearly none were made in CNY.

Figure 1

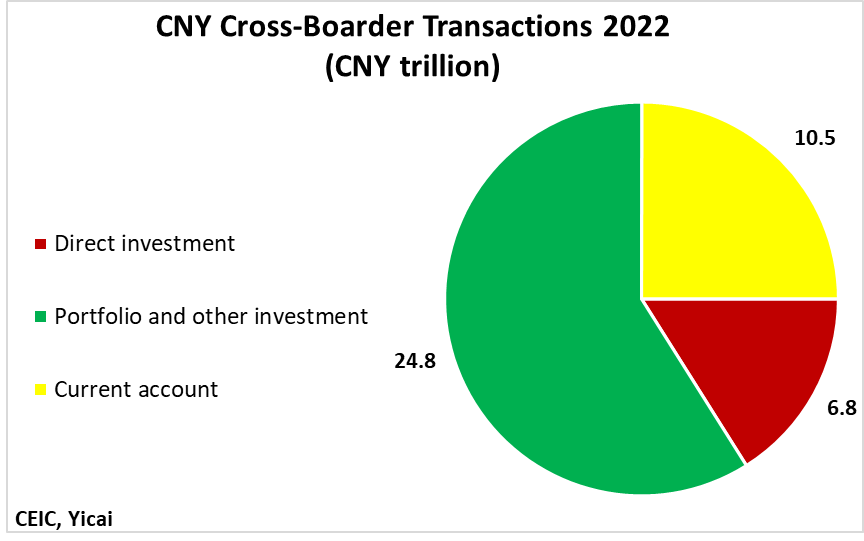

Three-quarters of the CNY-denominated cross-border payments made in 2022 were for investments, the majority of which were portfolio and other investments (Figure 2). Current account transactions, including payments for the export and import of goods and services, only represented a quarter of the total.

Figure 2

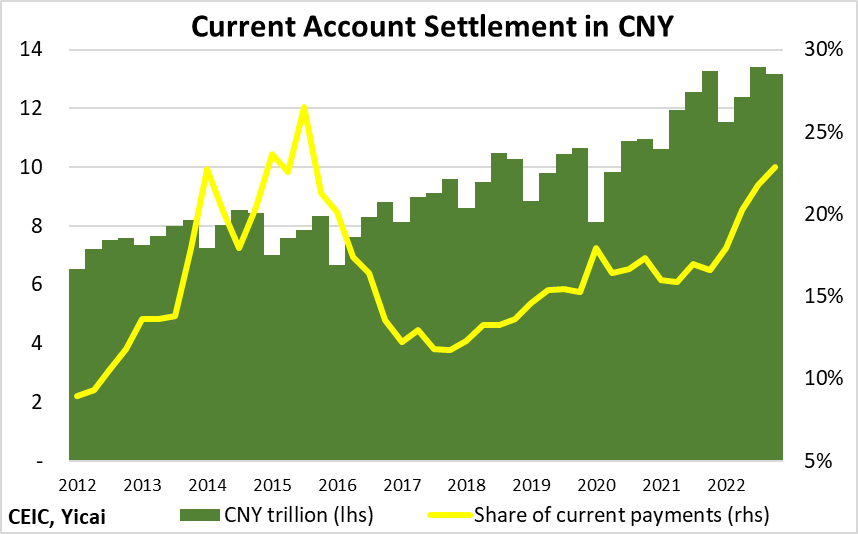

Last year’s CNY10.5 trillion in CNY-denominated payments for current account items was up 32 percent from 2021. The share of payments for current account items made in CNY rose throughout the year, reaching 23 percent in the fourth quarter (Figure 3).

Figure 3

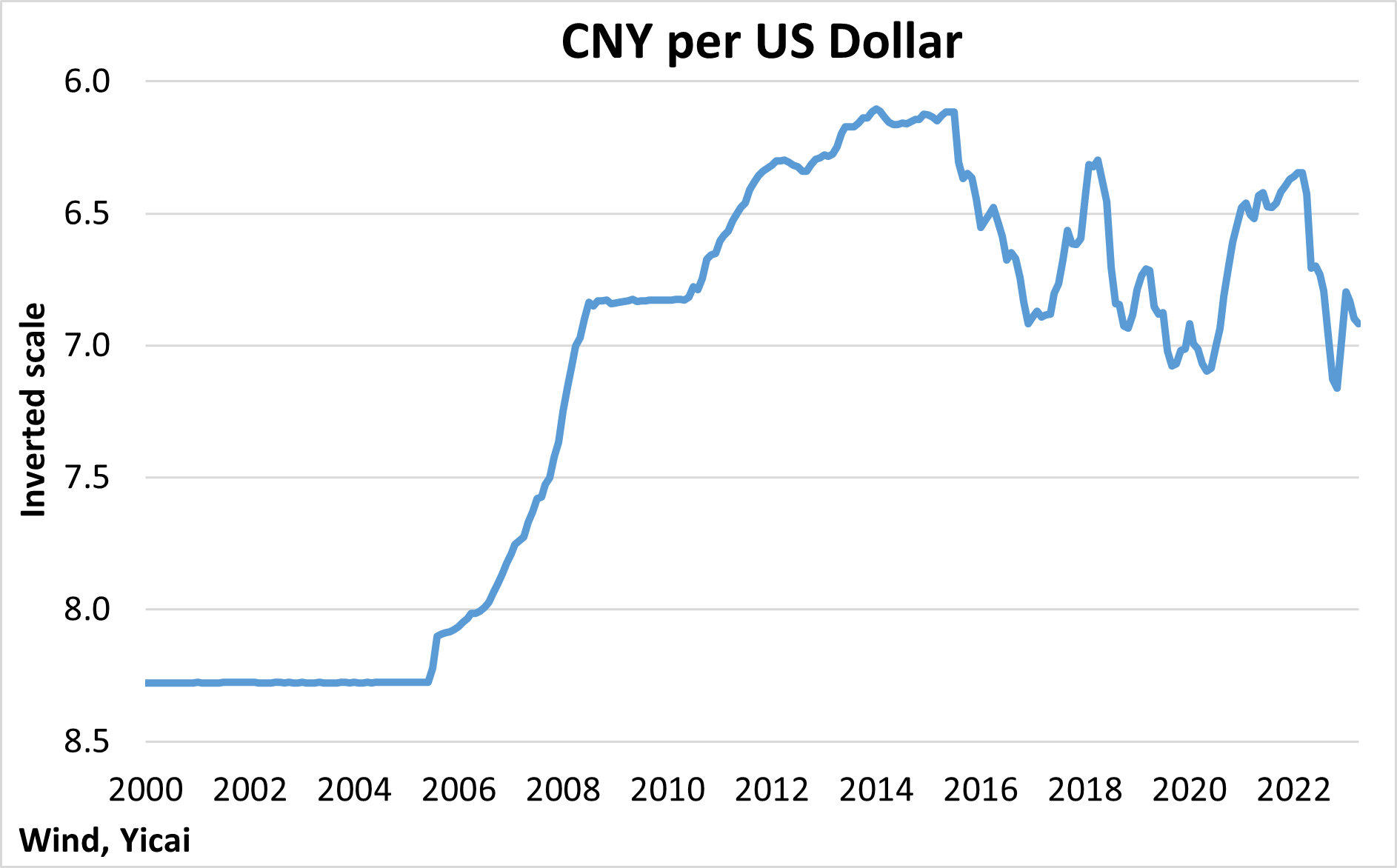

The CNY had been used for current account transactions even more extensively through mid-2015. However, interest dropped off after the Chinese currency depreciated by 3 percent against the US dollar that August and subsequently fell by an additional 9 percent to the end of 2016 (Figure 4).

The fall of the CNY followed an extended period during which its value had either increased or was stable in US-dollar terms. Its unexpected weakness likely unnerved China’s trading partners who became less willing to invest in CNY deposits. This episode appears to have retarded the adoption of the CNY as an international currency. Moreover, the very low US-dollar interest rates in recent years may have also dampened enthusiasm for the CNY as an international trading currency.

Figure 4

Despite these headwinds, the share of current transactions denominated in CNY has rebounded from its end-2017 low and is approaching its 2015 peak. Given the US’s relatively small share of China’s current account transactions and the recent rise in US interest rates, there appears to be significant opportunity to increase this ratio further.

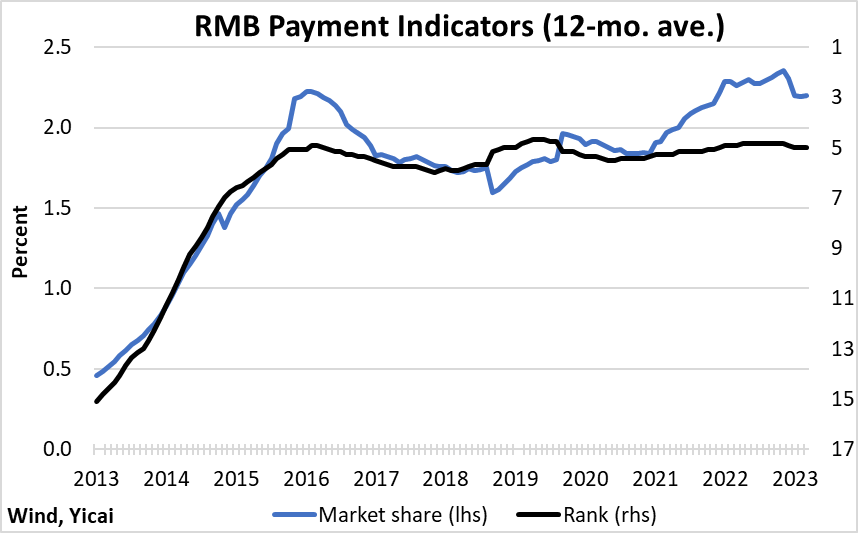

Looking across the globe, 2.2 percent of international payments were made using the CNY in the last 12 months, about the same as its previous peak in early 2016. In March, the currency was the fifth most used after the US dollar, the euro, the pound and the yen (Figure 5).

Figure 5

According to the Society for Worldwide Interbank Financial Telecommunication (SWIFT), 4.5 percent of global trade finance by value was conducted in CNY in March. With China accounting for some 15 percent of the global goods trade, there seems to be considerable scope to raise the CNY’s share of trade finance.

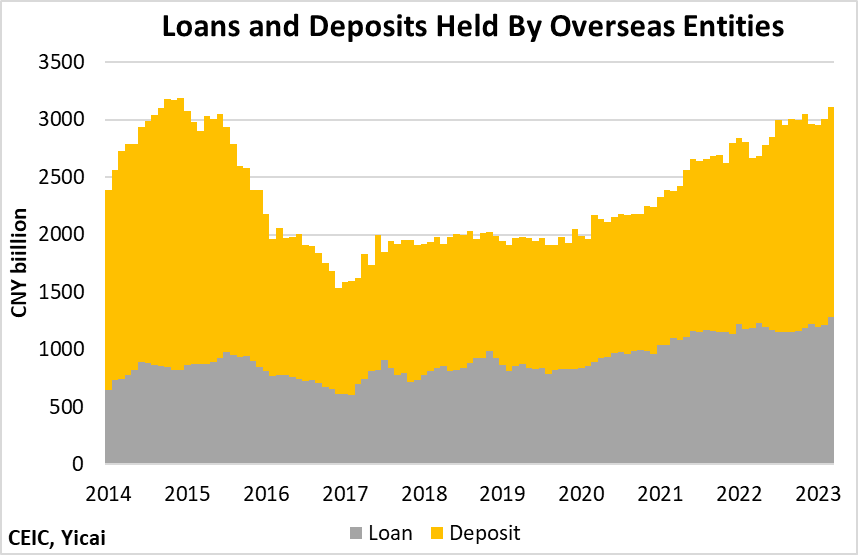

For the CNY to succeed as an international currency, China’s trading partners need to be comfortable holding CNY-denominated assets. It is, therefore, encouraging that foreigners’ holdings of CNY-denominated loans and deposits have essentially recovered their 2014 peak (Figure 6).

Figure 6

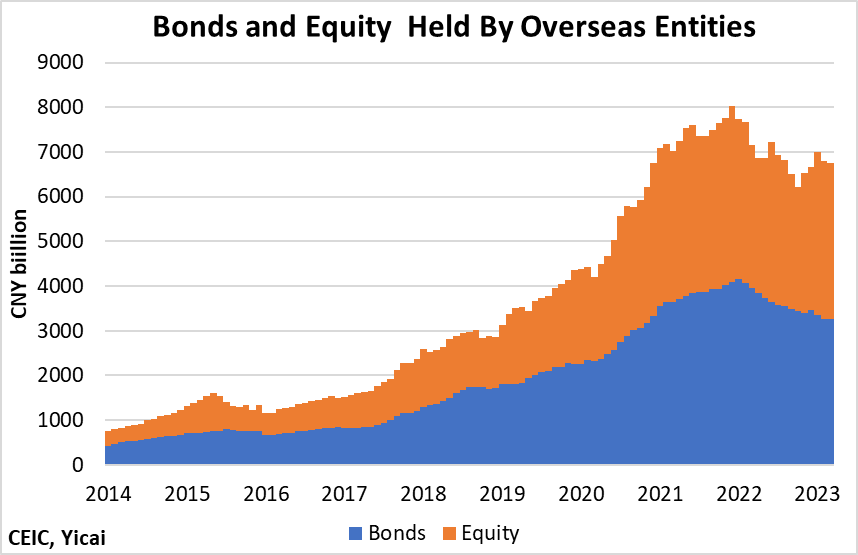

Moreover, foreigners hold much more in the way of CNY-denominated stocks and bonds than they did in 2015 (Figure 7).

Figure 7

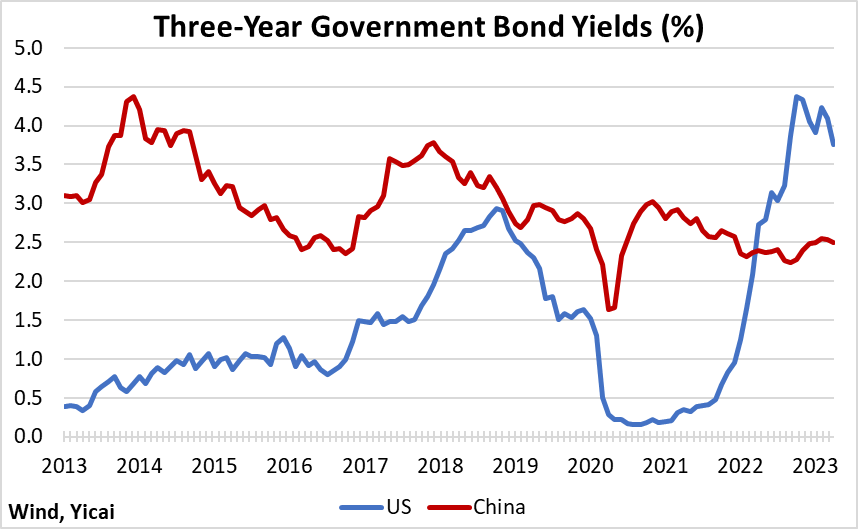

With US monetary policy squarely focused on bringing down inflation, interest rates in the US are uncharacteristically higher than those in China (Figure 8). Elevated US rates are leading firms to consider raising finance in CNY. In January, issued its inaugural Panda bond – the Panda market allows foreign entities to tap domestic CNY by issuing bonds. Deutsche raised CNY1 billion in 3-year senior preferred notes. , Deutsche’s Panda notes carried a 3.1 percent coupon, while yields on equivalent bonds in Frankfurt were more than 6 percent.

Figure 8

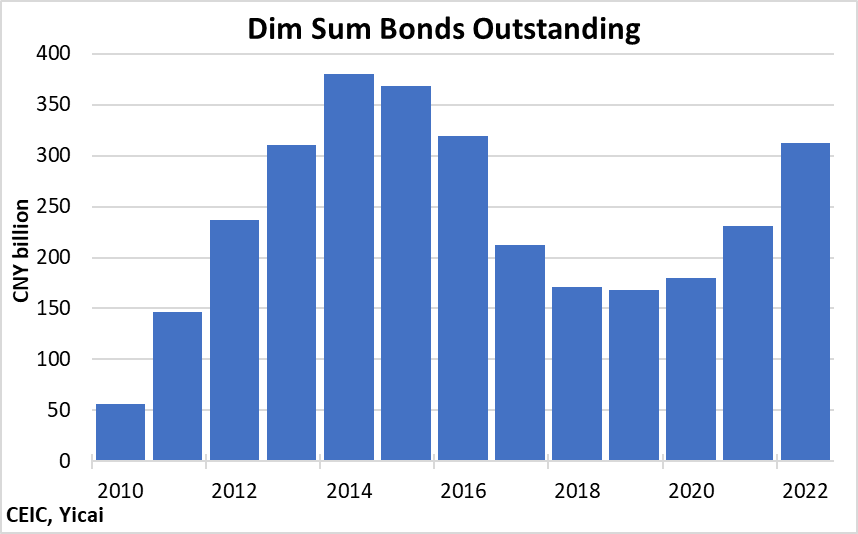

Low-interest rates are also likely to spur the continued rebound of Hong Kong’s dim sum bond market, in which foreign entities can raise funding in offshore yuan. The amount outstanding in the dim sum market last year rose 35 percent from 2021 and stood 83 percent above its 2018 trough (Figure 9). Here too funding rates remain attractive and issuance should increase this year.

Figure 9

While interest rates are an important factor in determining the pace of the CNY’s internationalization, a more crucial near-term issue is the perception of the US dollar as a store of value. The US is at risk of defaulting. The is the limit on the amount of debt the US government is permitted to incur. The current limit is USD31.5 trillion and Treasury Secretary Janet Yellen has Congress that the government will run out of cash in early June if the limit is not raised or suspended in time.

We may be simply witnessing an episode of political brinkmanship. Since 1960, under both Republican and Democratic presidents, the US Congress has raised the debt limit . However, the White House warns of should the US actually default, even for a short time.

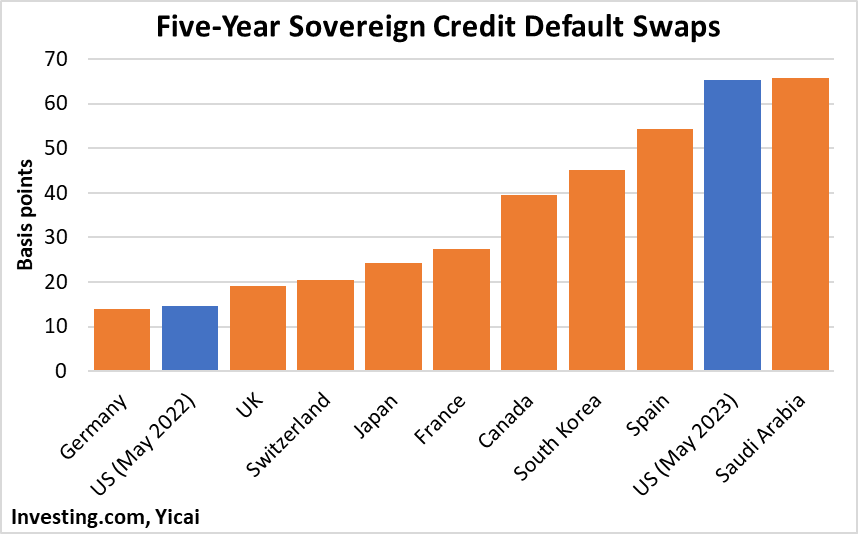

The cost of insuring US debt against default has risen sharply. The price of credit default swaps (CDS) in basis points reflects the cost of insuring USD10,000 of US bonds. The price of five-year US CDS rose from USD15 per USD10,000 last May to USD65 per USD10,000 this week. This implies that the US government’s creditworthiness deteriorated from Germany’s level to below that of Spain (Figure 10).

Figure 10

A sovereign default would be disastrous, not only for the US but also for its trading partners, including China. I believe that cooler heads will ultimately prevail. Nevertheless, using the US government’s creditworthiness as a political football may well encourage third countries to consider alternatives to the dollar.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.