China’s Economy Rebounds, But Caution Remains

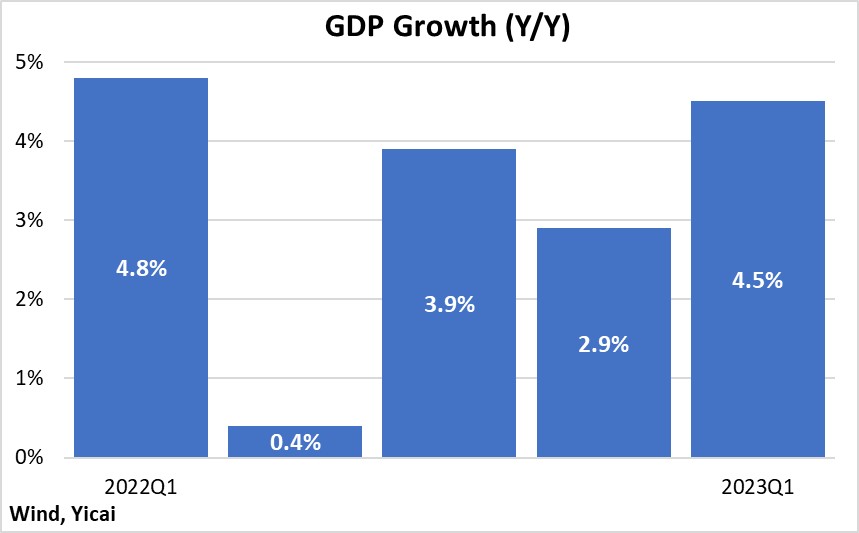

China’s Economy Rebounds, But Caution Remains (Yicai Global) April 21 -- On April 18, China’s National Bureau of Statistics (NBS) released the National Accounts for the first quarter of 2023. They showed that GDP grew by 4.5 percent year-over-year. The economy rebounded significantly from the 2.9 percent recorded in the final quarter of last year and exceeded the 4.0 percent forecast by the Chief Economists surveyed by the Yicai Research Institute.

While this better-than-expected outcome is certainly welcome, growth, at 4.5 percent, remains less than the 5 percent that the authorities are targeting for the year as a whole. Looking ahead, it is likely that measured economic activity will accelerate, in part, because growth in the second quarter of 2022 was depressed by the measures taken to limit the spread of Covid (Figure 1).

Figure 1

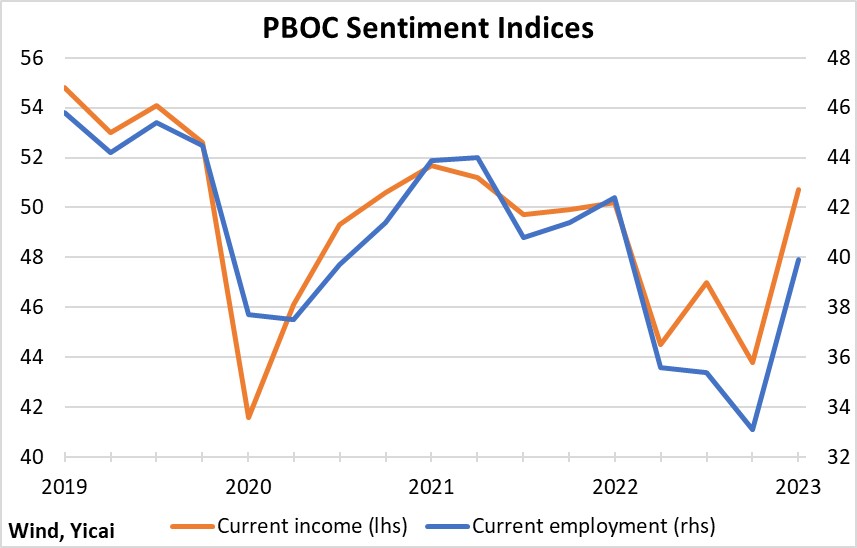

Consumption is being boosted by an improvement in consumer sentiment. However, consumers are not nearly as optimistic as they had been before the outbreak of the pandemic.

Surveys undertaken by the People’s Bank of China (PBOC) show that attitudes toward both current income and current employment recovered in the first quarter but they, nevertheless, remained well below those expressed during 2019 (Figure 2).

Figure 2

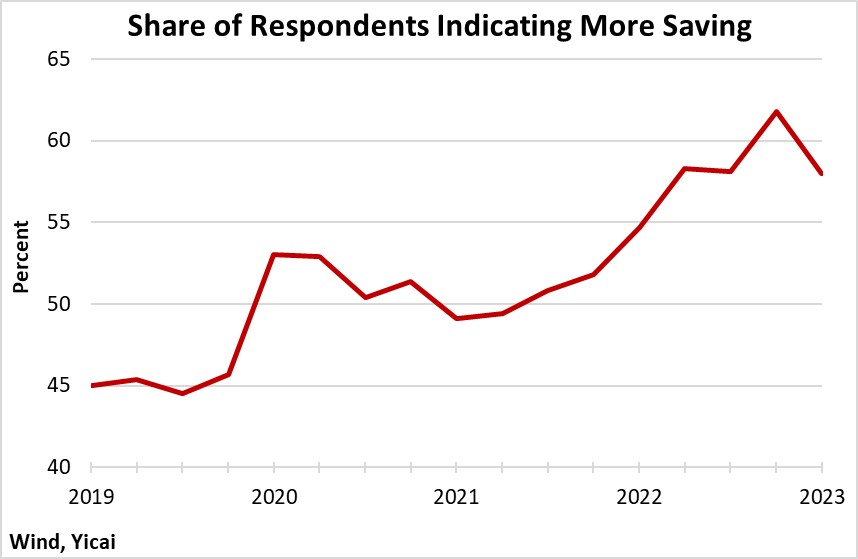

Moreover, while the PBOC’s survey results indicated a reduced willingness to save in the first quarter, the decline was small and consumers are likely to remain cautious (Figure 3).

Figure 3

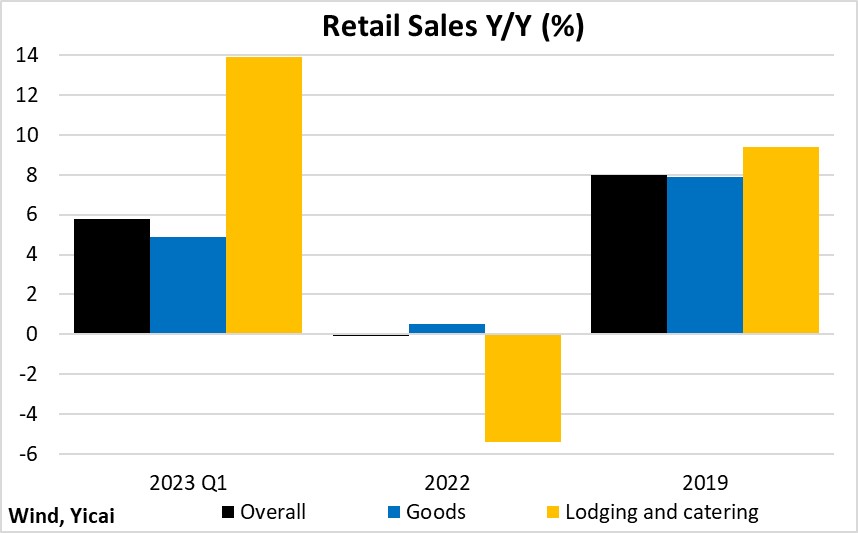

Ongoing consumer caution is born out by the retail sales data (Figure 4). Overall retail sales grew by close to 6 percent, year-over-year, in the first quarter. This represents a significant improvement from last year when sales were flat. But retail sales growth was still much slower than the 8 percent recorded before the pandemic hit in 2019.

According to NBS spokesman Fu Linghui, per capita spending on services exceeded that of overall consumption in the first quarter. This reflects the release of significant pent-up demand. Catering and lodging sales increased sharply in the quarter, jumping by close to 14 percent. With Covid under control, Chinese people have been much more willing to travel than in the recent past. Fu Linghui also noted passenger traffic was up 26 percent, year-over-year, in the first quarter.

It appears that the demand for travel remains strong in the second quarter as well. My wife and I were hoping to take our daughters somewhere interesting for the May 1st Labour Day holiday. Unfortunately, all of the train tickets to nearby attractions were already sold out last week. We are now looking at a staycation in Shanghai instead.

Goods consumption was lackluster, up 5 percent in the first quarter compared to 8 percent in 2019. This is consistent with lingering consumer uncertainty. We can often make do with the same car or television or vacuum cleaner just a little bit longer if we are concerned about the future.

Figure 4

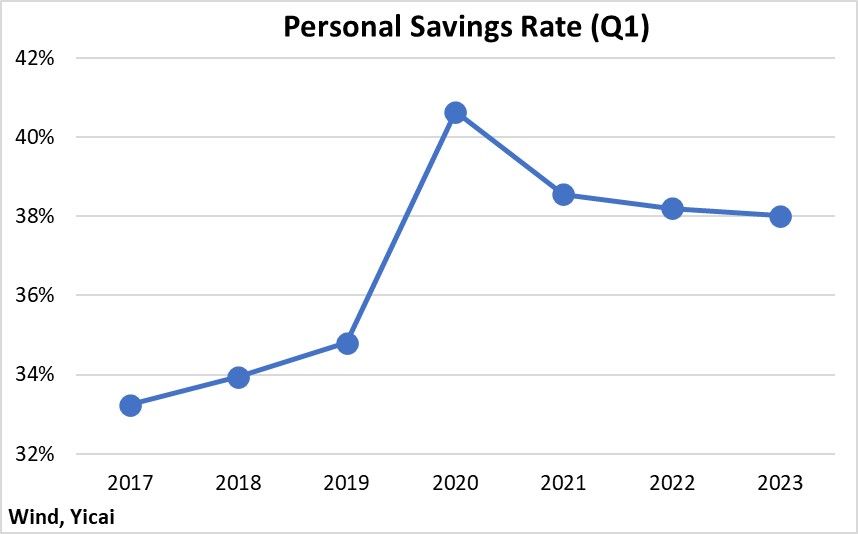

Figure 5 presents the personal savings rate for the first quarter of the last several years. It shows that, despite the reopening of the economy, the savings rate only edged down from last year and is still well above pre-pandemic levels.

While households’ caution continues to weigh on the economy, the spending of excess savings could fuel consumption in the second half of the year if the recovery proceeds smoothly and uncertainty continues to dissipate.

Figure 5

There are more signs that the property market is stabilizing.

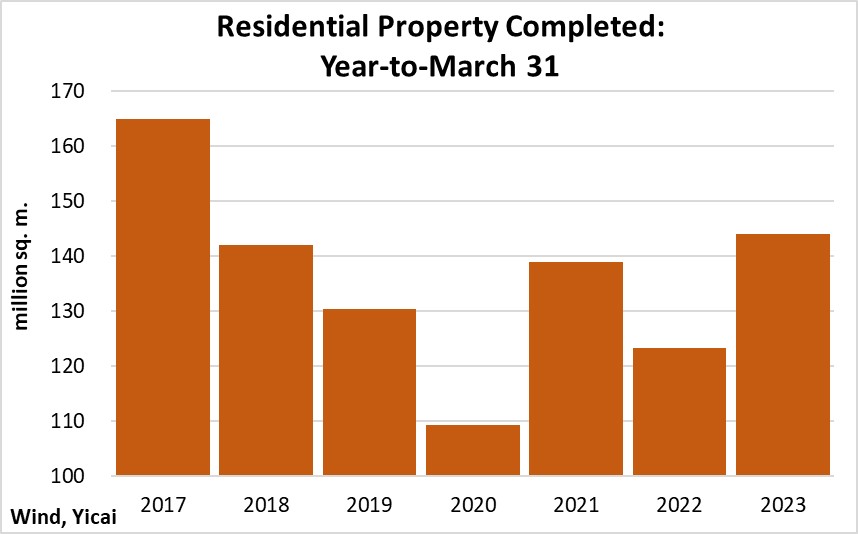

The volume of residential property completed in the first quarter, 144 million square meters, was up 17 percent from last year and was the largest amount since 2017 (Figure 6). This shows that measures undertaken to expedite the delivery of unfinished, presold projects – such as the CNY350 billion in special lending and the CNY200 billion in loan support –are beginning to pay off.

Figure 6

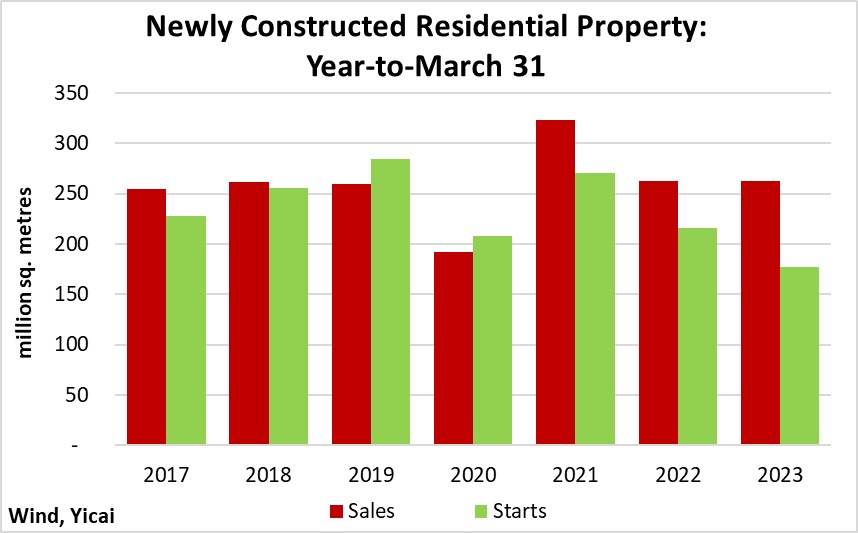

Following a decline of 27 percent last year, sales of residential real estate were essentially unchanged in the first quarter from year-ago levels (Figure 7). Sales are being supported by the many local governments that have eased restrictions on housing purchases. Nevertheless, housing starts, which fell by 40 percent last year, have continued to decline and were down 18 percent in the quarter.

Figure 7

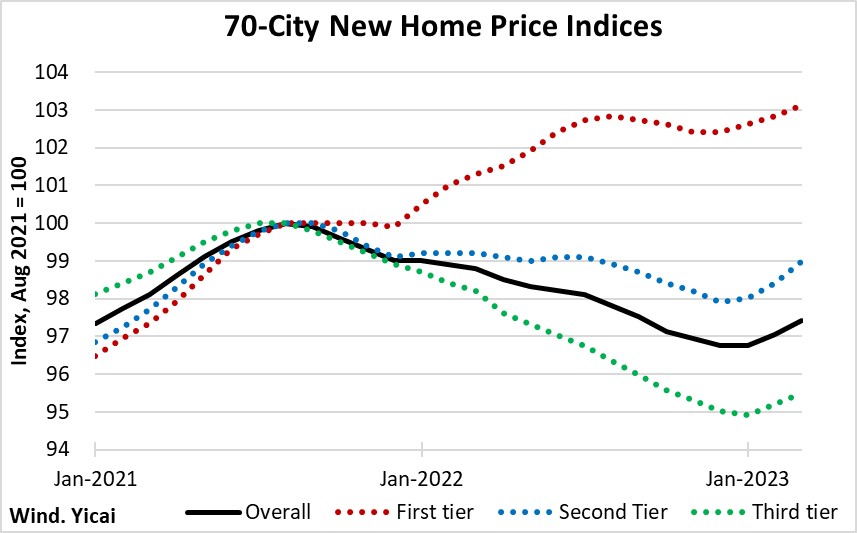

With housing demand holding up and new construction falling, we are starting to see a rebound in new home prices (Figure 8). On average, across the 70 cities surveyed by the NBS, prices have not fallen since December. In second-tier cities, prices are up 1.1 percent in the last three months, retracing half the decline from their August 2021 peak.

Figure 8

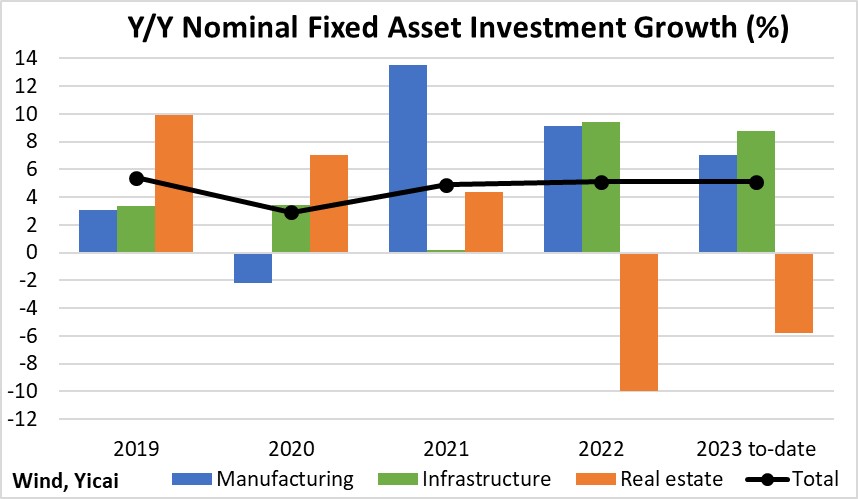

As was the case last year, the weakness in housing investment is being offset by more spending on infrastructure and manufacturing (Figure 9). Fu Linghui said that the rollout of key strategic projects under the 14th Five-Year Plan will continue to support future infrastructure spending.

Figure 9

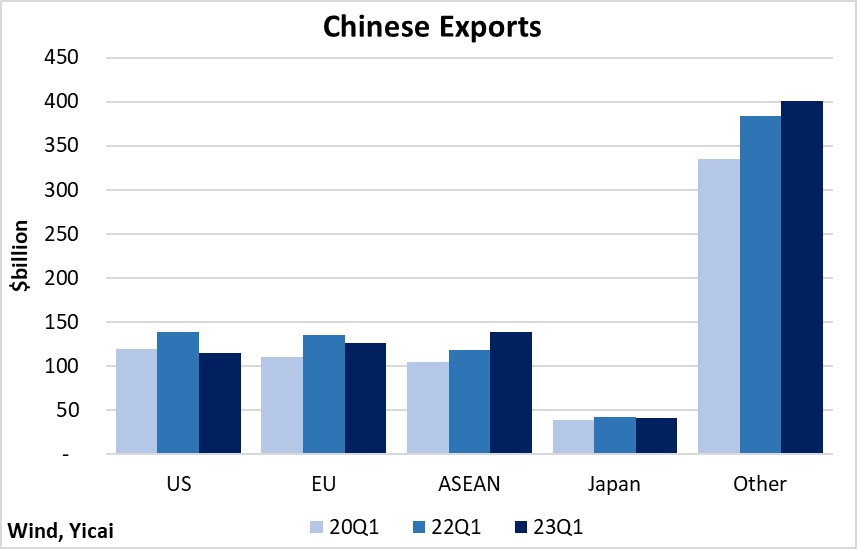

After falling for four consecutive months, China’s exports jumped by 15 percent, in dollar terms, in March. For the quarter, they were essentially unchanged from a year earlier. It was surprising that exports were able to match last year’s performance. Exports had grown rapidly over the three-year pandemic period, so the base was high. Moreover, the global economy is poised to slow this year as central banks keep interest rates high to rein in inflation. According to Fu Linghui, green exports – those of electric passenger vehicles, lithium batteries, and solar cells – were particularly strong in the first quarter.

Exports to key advanced-country markets, including the US, the EU and Japan, fell year-over-year in dollar terms (Figure 10). These declines were offset by stronger sales to the countries participating in the Regional Comprehensive Economic Partnership free trade zone and those involved in the Belt and Road initiative.

Figure 10

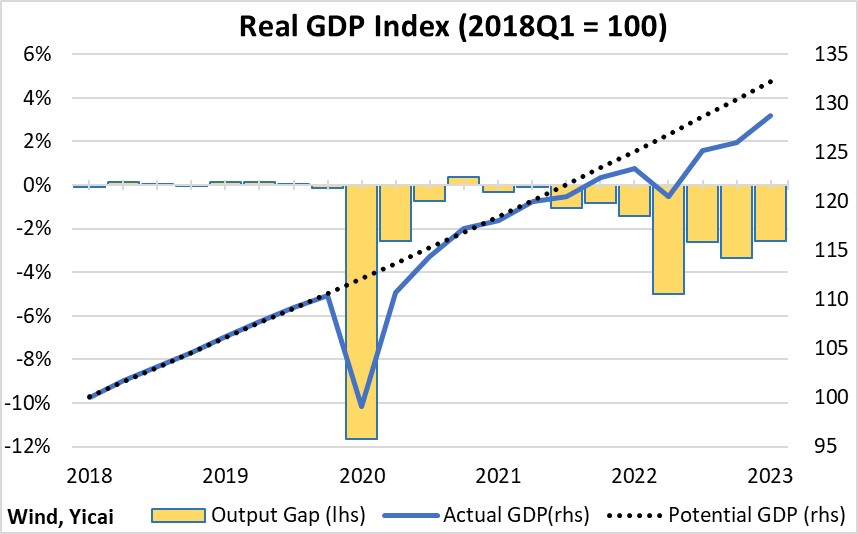

Despite the better-than-expected outturn in the first quarter, it appears that the Chinese economy is still operating well below capacity. I estimate the economy’s potential growth rate at between 5-6 percent. Average growth over 2020-22 was only 4.5 percent.

In the first quarter, GDP grew by 2.2 percent quarter-over-quarter – the equivalent of 9.1 percent at annual rates. This rapid growth closed the output gap, the difference between actual and potential GDP, by 1.2 percentage points. Still, I estimate that the level of GDP in Q1 was 2.4 percent below potential (Figure 11).

Figure 11

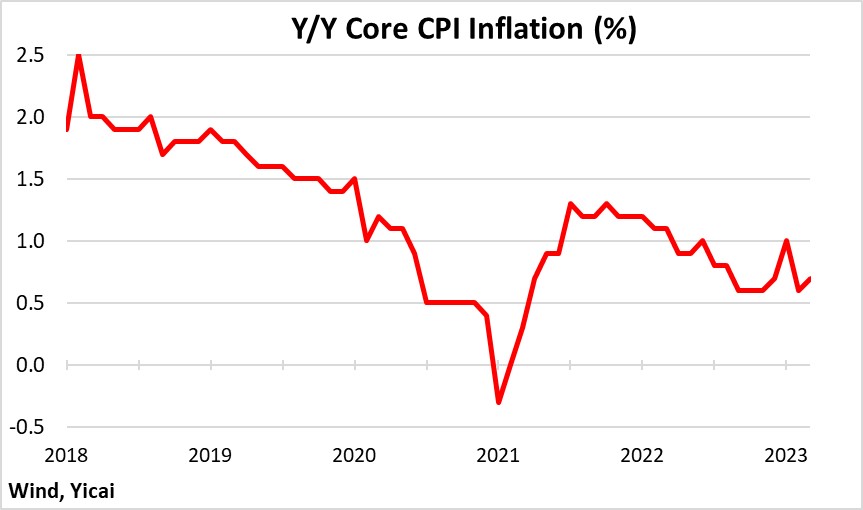

This persistent “excess supply gap” explains why core inflation has fallen from 1.8 percent over 2018-19 to only 0.7 percent in March this year (Figure 12).

Figure 12

In the US and the EU, the pandemic reduced labour supply along with aggregate demand. As a result, wages have been rising in both of these economies as output recovered. In China, labour supply seems to have been much more resilient, perhaps because Chinese public health policies were better able to keep Covid at bay.

In the US and the EU, the pandemic reduced labour supply along with aggregate demand. As a result, wages have been rising in both of these economies as output recovered. In China, labour supply seems to have been much more resilient, perhaps because Chinese public health policies were better able to keep Covid at bay.

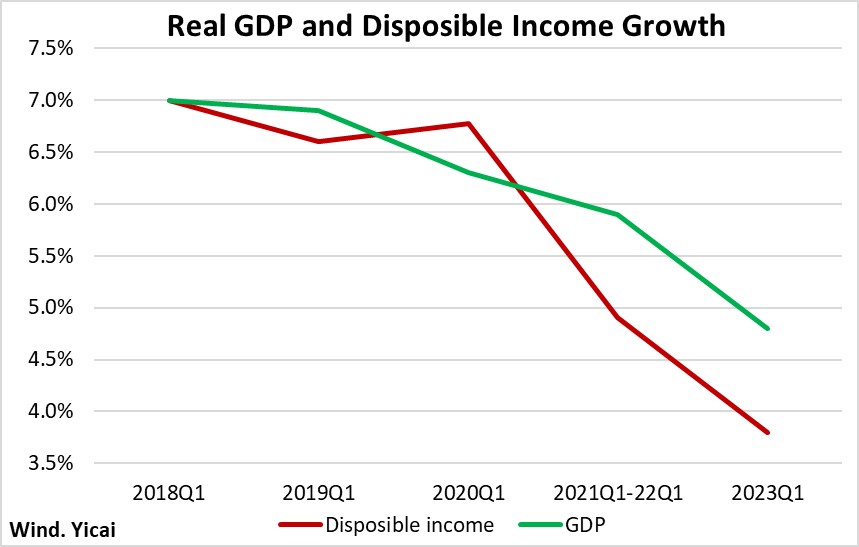

While the wage data in China is not nearly as rich as in many advanced economies, comparing the growth of real GDP and real disposable income is instructive. Figure 13 shows the year-over-year growth rates of these two variables for the first quarter over the last six years (I average 2021 and 2022 to look through their volatility). In 2018-20, the growth rates of real GDP and real disposable income were fairly similar. However, over the last three years, GDP has grown more rapidly than income.

Figure 13

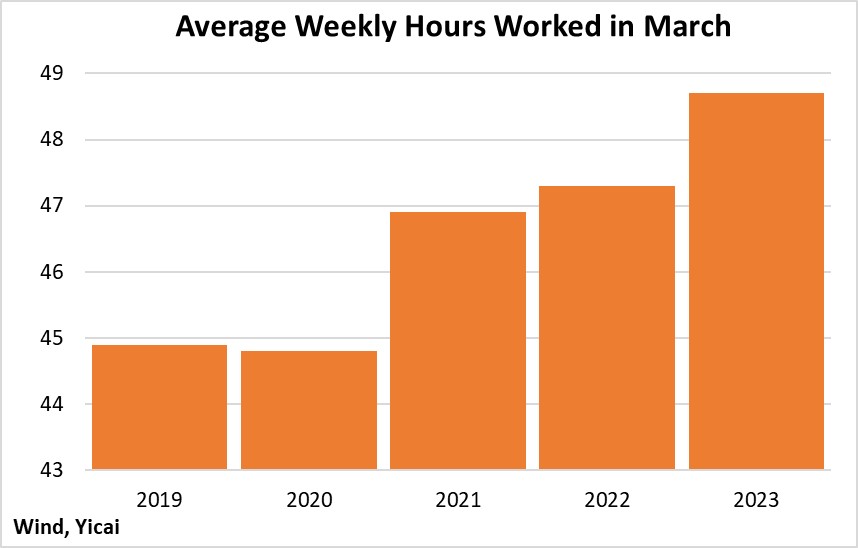

Rather than hire additional labour, risk-averse employers have been getting more out of their existing staff. In March, workers put in 3.8 more hours per week (+8 percent) than in 2019 (Figure 14).

The resilience of the labour market is good news. It means that, as its economy recovers, China will likely avoid the sort of wage pressures we have seen elsewhere. But it has a darker side too. It suggests that insipid wage growth will make raising consumption difficult.

Clearly, there are limits to how far employers can push their existing workforce. I expect that as the recovery becomes more entrenched, employers will become more confident and create new jobs.

Figure 14

There’s an old saying among economists: one data point does not make a trend. For the Chinese economy to fully recover, it will need to maintain a virtuous cycle of accelerating GDP and growing business and consumer confidence. Barring unforeseen events, this cycle should continue into the second quarter.

There’s an old saying among economists: one data point does not make a trend. For the Chinese economy to fully recover, it will need to maintain a virtuous cycle of accelerating GDP and growing business and consumer confidence. Barring unforeseen events, this cycle should continue into the second quarter.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.