Why Are Chinese EVs Such A Great Deal?

Why Are Chinese EVs Such A Great Deal?(Yicai) May 29 -- China dominates global electric vehicle (EV) production. Its factories accounted for 73 percent of the 22 million units manufactured in 2025.

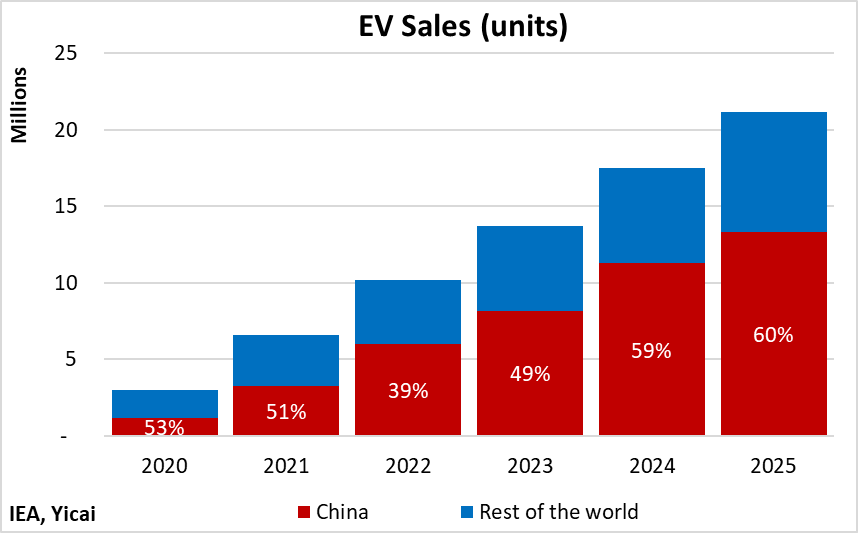

China is also, by far, the largest EV market. Last year, domestic sales rose by 18 percent to 13 million units, accounting for 60 percent of all EVs sold worldwide (Figure 1).

China’s exports doubled to 3 million units last year. These affordable offerings underpinned uptake in foreign markets, where they are winning praise: BYD surpassed Porsche and Mini to be voted the UK’s “most loved brand” in a 2025 online survey of 200,000 participants.

Figure 1

China’s EV success story is one of government foresight channeling market dynamism.

Government officials first targeted the production of EVs during the 10th Five-Year Plan (2001-2005). While the technology was not yet commercialized, the planners saw potential for electric vehicles to reduce China’s oil dependency, improve its air quality and provide a niche for domestic auto producers. The Three Verticals and Three Horizontals framework called for the development of three vehicle types (pure electric, hybrid, and fuel cell) and three core components (batteries, electric motors, and power electronics/control systems) over a 15-year horizon.

The advent of the Tesla Roadster in 2008 accelerated the timeline for mass market EVs. China initiated the Ten Cities, One Thousand vehicle program in 2009, under which grants were provided for the purchase of demonstration fleets. In 2010, the program expanded to include consumer subsidies, tax breaks and investment in charging stations. The “green plate” policy, which made it easier for purchasers of EVs to obtain licences, began in five cities in late 2016 and expanded nationwide by late 2018. The favourable treatment of EVs was key in inducing consumers to switch from the cheaper internal combustion engines (ICE) to battery-powered cars. The subsidies can also be seen as a way of offsetting the negative externalities – pollution and carbon emissions – caused by ICE vehicles.

As the EV market matured and the price of battery-powered cars dropped – 30 percent of China’s models were priced below USD20,000 last year – the government phased out its support to consumers. The subsidies ended in 2022 and the purchase tax exemption has been reduced and will expire in 2027.

On the producer side, much of the government support came in the form of subsidies for charging infrastructure, R&D and government procurement mandates. To incentivize the production of EVs, the government implemented the Dual Credit framework in 2018. This program set both fuel efficiency standards for ICE vehicles and EV production minimums for manufacturers. These standards have been progressively tightened over time, incentivizing firms to produce low- or zero-emission vehicles.

Tesla has played an important role in China’s EV development. In 2013, it opened its first showroom in Beijing. Chinese consumers’ ability to purchase these imported cars helped to raise the standards for domestic production. Tesla broke ground on its Shanghai Gigafactory in 2019. Its first cars were delivered in 2020. The factory now sources 95 percent of its components from 400 local suppliers, more than 60 of which are integrated into Tesla’s global supply chain. This has been an important channel for knowledge transfer.

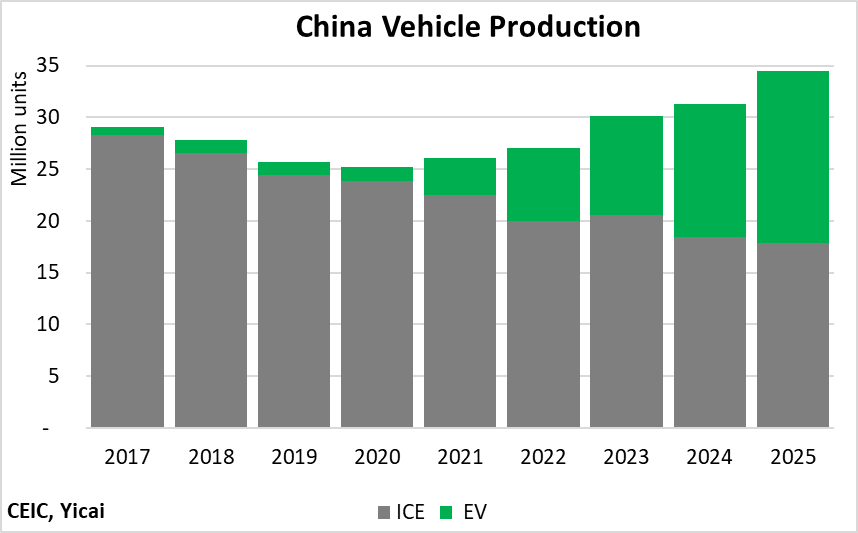

China’s embrace of EVs has transformed its auto industry. EV production increased close to fivefold from 2021 to 2025, representing nearly half of all vehicles manufactured. Total vehicle production reached a new high in 2025 despite a 10 million decline in ICE vehicle output from 2017 (Figure 2).

Figure 2

China’s ability to master the EV technology depended crucially on its established position as both a major producer and market for ICE vehicles. Indeed, by 2009, China was already the world’s largest vehicle producer. Experience in manufacturing ICE vehicles provided Chinese firms with considerable expertise in car and car part manufacture. A large, dynamic domestic market allowed firms to exploit economies of scale.

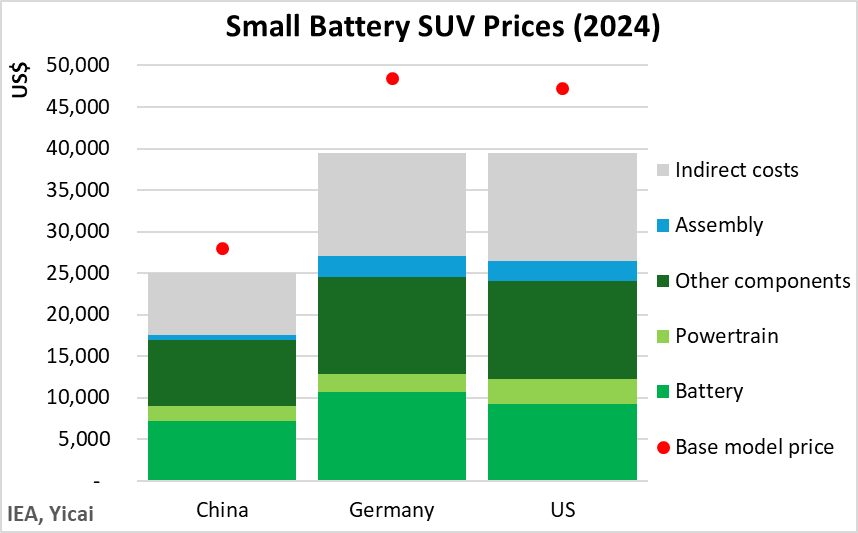

The International Energy Agency (IEA) provides a bottom-up analysis of battery-powered SUV prices in China, Germany and the US that illustrates the sources of Chinese EVs’ competitiveness. The bars in Figure 3 show the manufacturing cost. The red dot represents the price to the consumer in each of the three markets (Figure 3).

Figure 3

The cost of manufacturing a battery-powered SUV is about USD25,000 in China and just under USD40,000 in Germany and the US. This includes both direct and indirect costs. Direct costs comprise those of labour, energy, material and components. Indirect costs, essentially overhead, is made up of administration and marketing, R&D and capital expenditures.

The batteries and powertrains of the Chinese vehicles cost some 70-75 percent as much as the German and American ones. According to the IEA, “more advanced battery designs and faster innovation cycles are among the key advantages enhancing the competitiveness of Chinese companies in the electric car market.” Since China produces so many more batteries than the US and Europe (it accounted for 80 percent of global battery production in 2025), it has both lower unit costs and an edge in developing new technologies. The large scale of Chinese battery production means that firms can afford to invest in robotics and Chinese factories are much more automated than those elsewhere.

Chinese battery makers have made significant innovations in battery chemistry.

The traditional battery chemistry – nickel manganese cobalt (NMC) – offers the highest energy density, enabling longer driving ranges. In China, producers developed batteries with a lithium iron phosphate (LFP) chemistry. While not as energy-dense as NMC batteries, LFP batteries only depend on one critical mineral instead of four. Moreover, LFP batteries are cheaper to produce and last longer. While NMC batteries remain the most energy-dense, advances in recent years have increased the energy density of LFP batteries to 20 percent beyond what NMC batteries offered in 2020. In the face of growing demand, ongoing innovation in battery design has led to a 40 percent decline in LFP battery prices in the last five years.

The cost of components other than the powertrain is about one-third lower in China than in Germany and the US. These components include the interior sub-assemblies, the exterior, the body and the chassis. Some of Chinese firms’ advantage here comes from vertical integration – keeping the production of component parts in house rather than outsourcing them to other firms. Vertical integration requires greater investment up front but it eliminates supplier markups along the supply chain. A UBS study estimates that 75 percent of BYD’s Seal is produced in-house, compared with 46 percent for Tesla’s Model 3 and 35 percent for Volkswagen’s ID.3. Leapmotor reportedly produces 60–70 percent of its components in-house. Chinese labour costs, which are roughly three to five times lower than in most advanced economies, are also a key source of competitiveness.

The ability to produce at scale is an important factor driving down per unit indirect costs. The biggest EV factories in China can make over 1 million cars per year, compared with 0.1-0.6 million cars for typical plants outside China, most of which do not currently operate near full capacity. This allows Chinese firms to spread overhead costs across a greater number of vehicles.

As Figure 3 shows, not only is the cost of production lower in China than in Western countries, but the producers make smaller profits. The profits are the difference between the cost (height of the stacked bars) and the selling price (the red dot).

In China, the profit margin (profits divided by selling price) is 11 percent, while in Germany and the US they are 19 and 16 percent, respectively. The higher profit margins in Germany and the US could be a result of positioning EVs as premium vehicles – for consumers who are less price-sensitive. Lower margins in China could be the result of an extremely competitive market with over 50 active producers. Or the low Chinese margins could be the result of government subsidies.

The ability of Chinese firms to quickly gain market share in foreign countries raises the possibility that subsidies allow Chinese firms to undercut local manufacturers while maintaining their profitability.

In late 2024, the EU imposed countervailing duties on imports of battery electric vehicles from China, alleging that Chinese producers benefit from unfair government subsidies. They were imposed on top of the 10 percent import tariff that the EU levies on all car imports. The Chinese government has challenged the validity of the countervailing duties under the WTO and a panel has been established to adjudicate the case.

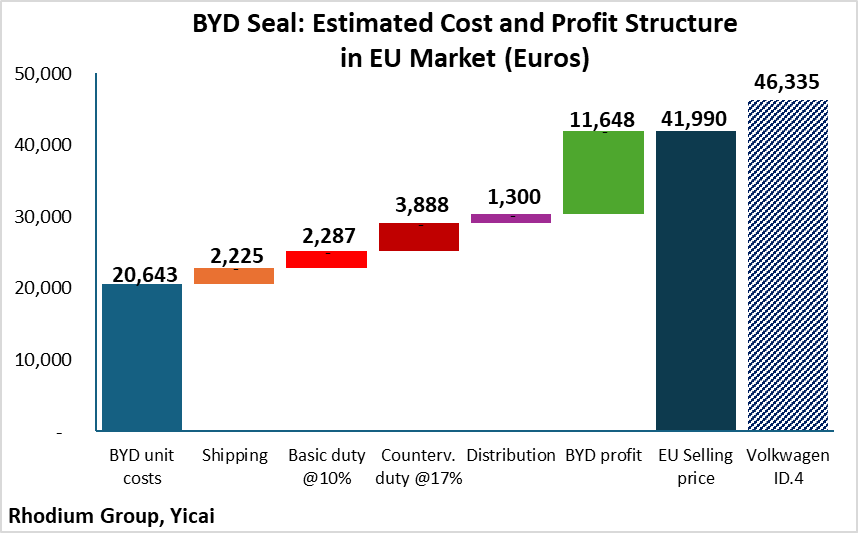

For the purposes of illustration, let us suppose that the 17 percent countervailing duty assessed against BYD accurately reflects the amount of the subsidy the company received. According to the Rhodium Group, BYD’s Seal U Comfort sold for just under EUR42,000 or 9 percent lower than Volkswagen’s comparable offering, the ID.4 (Figure 4).

At this price, BYD would be able to record a profit of EUR11,648 over its costs, shipping to Germany, distribution within Germany and payment of both of the import duties. The profit is three times as much as the subsidy calculated by the European Commission. This suggests that it is BYD’s lean cost structure, not the alleged subsidies, that make it super-competitive in foreign markets.

Figure 4

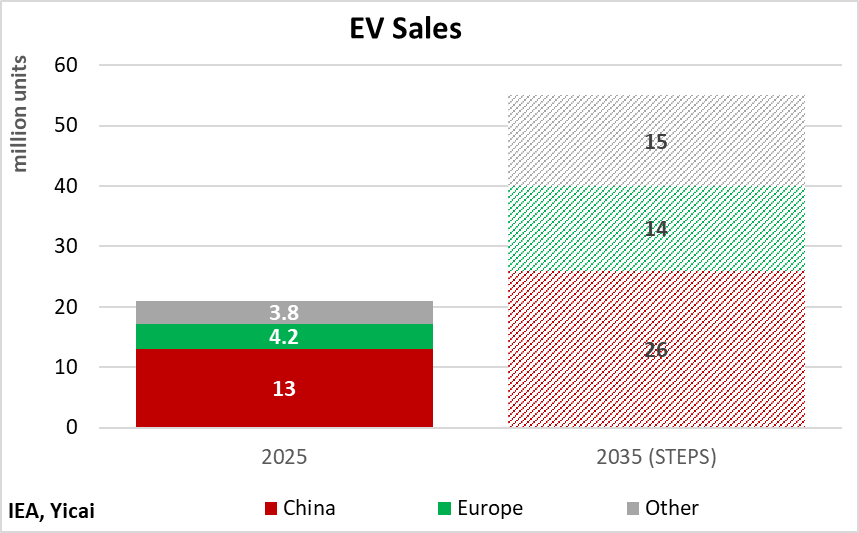

According to the IEA’s stated policies scenario (STEPS), which is designed to reflect country-specific energy, climate and related industrial policies, EV sales in 2035 will reach 55 million units, up from 21 million in 2025. Sales in China are expected to double from 2025 levels. European sales are seen as increasing by 233 percent, while those in “Other” countries are expected to rise fourfold (Figure 5).

Figure 5

The prospect of a rapidly growing global market has attracted the attention of numerous firms in China and abroad. They have invested in capacity that well exceeds current demand. According to the IEA, global EV manufacturing capacity was some 70 percent greater than production in 2024. Some of this capacity will be absorbed by the ongoing increase in demand. There will also be some consolidation as the more efficient producers thrive and the less efficient ones go out of business. But this process could take time.

From the producer perspective, overcapacity is an existential problem. However, for consumers, many firms competing on both price and quality is certainly preferable to production being dominated by a few oligopolistic firms. For society as a whole, cutthroat competition has led to a sharp decline in EV prices, supported early adoption and led to environmental benefits. The IEA estimates the stock of EVs was responsible for avoiding net emissions of 190 Mt CO2-equivalent last year. Increased EV adoption over the next ten years will save some 7 Gt CO2-equivalent or seven times the amount Japan produces annually.

There is nothing exceptional about the herding behaviour exhibited by EV producers. We are seeing the same phenomenon in the construction of data centers to support AI. We saw this in the rush to lay fibre optic cable during the dotcom bubble. Firms got ahead of demand during the electrification boom of the 1920s and the railway mania of the 1840s. While many companies ended up failing, useful technologies were put in place. Economist Joseph Schumpeter called this disorderly adoption of innovative processes “creative destruction” and it remains a key channel for our material progress.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.

Mark KrugerBased in Shanghai, Mark Kruger holds Senior Fellow appointments at the Yicai Research Institute, the Centre for International Governance Innovation and University of Alberta’s China Institute. Between 2020 and 2023, Mark was the Opinion Editor at Yicai Global. Previously, he had a 30-year career with the Bank of Canada in the course of which he served as a Senior Advisor to the Canadian Executive Director at the IMF and the head of the Economic and Financial Section of the Canadian Embassy in Beijing.