Breaking the Cage of the Mind: Beyond the Narrow Debt Sustainability Framework to Build and Revitalize Public Assets

Breaking the Cage of the Mind: Beyond the Narrow Debt Sustainability Framework to Build and Revitalize Public Assets(The author is Wang Yan, a senior academic researcher at Boston University Global Development Policy Center.)

(Yicai) April 20 -- On March 19, 2026, the U.S. Treasury released the Fiscal Year 2025 Financial Report of the United States Government. This report deserves serious attention not only because it once again acknowledges that the U.S. fiscal path is under mounting strain and is even approaching technical insolvency, but also because it inadvertently exposes a fundamental asymmetry in today’s system of international fiscal governance: when the United States evaluates itself, it uses the language of a more complete balance sheet; yet when the International Monetary Fund evaluates many developing countries, especially in Africa, it still largely remains trapped in a narrow, one-sided framework, the Debt Sustainability Framework, focused mainly on debt, deficits, and repayment capacity, while neglecting the role of public assets.

The Treasury report explicitly states that the current fiscal path is “unsustainable.” Yet the same report also emphasizes that cash-flow discussions centered on budget deficits and debt “tell only part of the story.” The key figures it presents are these: in FY2025, the U.S. government held approximately USD6.1 trillion in total assets and about USD47.8 trillion in total liabilities, leaving it with a negative net worth of USD41.7 trillion. Debt held by the public amounted to 99 percent of GDP, and under current policy assumptions, that ratio could rise to 576 percent by 2100. In other words, even the U.S. Treasury itself does not reduce America’s fiscal problem to a simple story of “too much debt.” Instead, it places the issue back within a more complete framework of assets, liabilities, and net worth.

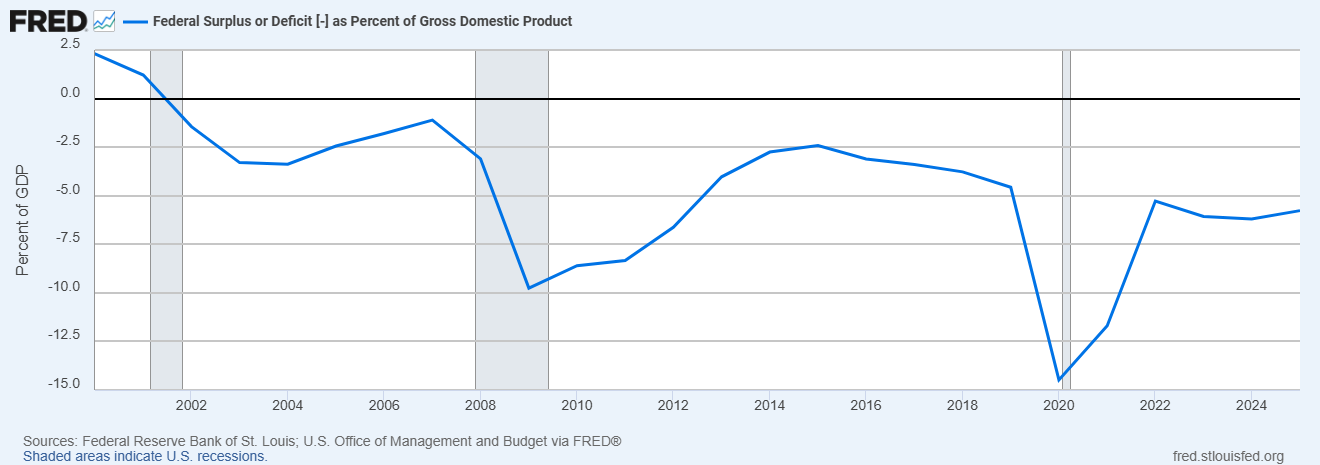

Figure 1. U.S. federal fiscal deficit as a share of GDP (with 0% as the baseline)

Source: FRED, Federal Surplus or Deficit [-] as Percent of Gross Domestic Product (FYFSGDA188S)

Figure 1 establishes the discussion on a very clear fact: the United States does face a real problem of fiscal unsustainability. This article is not denying the IMF’s concerns about U.S. deficits and debt. Rather, it seeks to point out that the problem is not that the IMF cares about debt, but that it has become far too accustomed to caring only about debt. If analysis stops at a single line, “the deficit as a share of GDP,” then public assets, future productive capacity, and the repayment base created by investment are systematically pushed aside. The Treasury’s own report does not stop there; it continues on to the level of the balance sheet.

The U.S. Treasury looks at the balance sheet, while the IMF still focuses mainly on the liability side when dealing with many developing countries

Readers are already well aware of the rapid rise in U.S. debt, so there is no need to repeat it here. The U.S. Treasury repeatedly emphasizes in its report that the current fiscal path is “unsustainable.” The key point, however, is that even in the face of such high deficits and debt, the Treasury’s own analysis does not stop at simply “looking at liabilities.” Instead, it places the fiscal problem back within a more complete framework of assets, liabilities, and net worth. By contrast, the IMF’s common approach toward many low-income countries and African countries still focuses mainly on debt-to-GDP, debt service, gross financing needs, and short-term fiscal adjustment. The asymmetry here is not about whether debt problems exist at all, but about the fact that the analytical method has not been applied evenhandedly.

This article does not treat the U.S. Treasury and the IMF as the same entity; they are obviously not the same institution. The real question worth asking is this: although the United States, as the IMF’s largest shareholder and most influential member, has already adopted a more complete balance-sheet language in assessing its own fiscal position, the IMF-led Debt Sustainability Framework has not more fully incorporated this approach. Economists from developing countries pointed this out repeatedly ten years ago (Lin Yifu and Yan Wang 2016), yet progress on reform has been extremely slow.

A plausible explanation for this is institutional inertia. Because the DSF is an analytical framework developed by IMF staff over many years and used continuously for a long time, its basic methodology has become deeply embedded in institutional practice and policy thinking. As a result, even though its limitations are becoming increasingly evident, any real revision may still be much slower and more difficult than outsiders expect. This also brings to mind the IMF’s belated correction around 2016 on the issue of capital account liberalization. That experience shows that once a policy framework has been institutionalized, adjustment is rarely linear and is often clearly constrained by path dependence. For this reason, judgments about sovereign fiscal sustainability should not rely solely on a few liability ratios. The problem is that this more complete balance-sheet language has not been applied equally within the IMF’s policy framework for countries in the Global South.

A more appropriate fiscal anchor should be public sector net worth. On this point, recent research has already pointed in a very clear direction: fiscal policy should not focus only on debt levels, but should instead turn toward public sector net worth, because net worth incorporates both the assets and the liabilities of the public sector and better captures the role of public investment in productive capacity and long-term growth. The advantage of the net-worth framework is that it encourages productive investment, helps prevent unsustainable debt dynamics, and more reasonably reflects the impact of interest-rate changes on fiscal constraints.

It is precisely for this reason that the shortcomings of the current DSF stand out so sharply. Its greatest problem is not that it cares about debt, but that it treats debt itself as the boundary of the problem. Nor is the problem that it calls for fiscal discipline, but rather that it narrows fiscal discipline into liability discipline. As a result, borrowing to pay wages and sustain current consumption, versus borrowing to build railways, power plants, and transport and energy networks, are often not fundamentally distinguished in IMF analysis. The outcome is that the long-term investment needs of developing countries are in turn constrained by a short-term debt-servicing framework. This methodological bias is itself clearly anti-investment in character.

Debt distress has never had only one answer, austerity; governments also have another lever: building and revitalizing public assets

When a country faces debt distress, it in fact has two policy levers. One is the one the IMF is most familiar with: fiscal adjustment, that is, reducing debt through spending cuts and revenue increases. The other has long been undervalued: building and revitalizing public assets, including human, natural, and productive assets, in order to expand future growth capacity, the tax base, employment, and repayment ability. The real question is not whether governments should control debt. It is whether an international institution has turned debt control into the only legitimate answer.

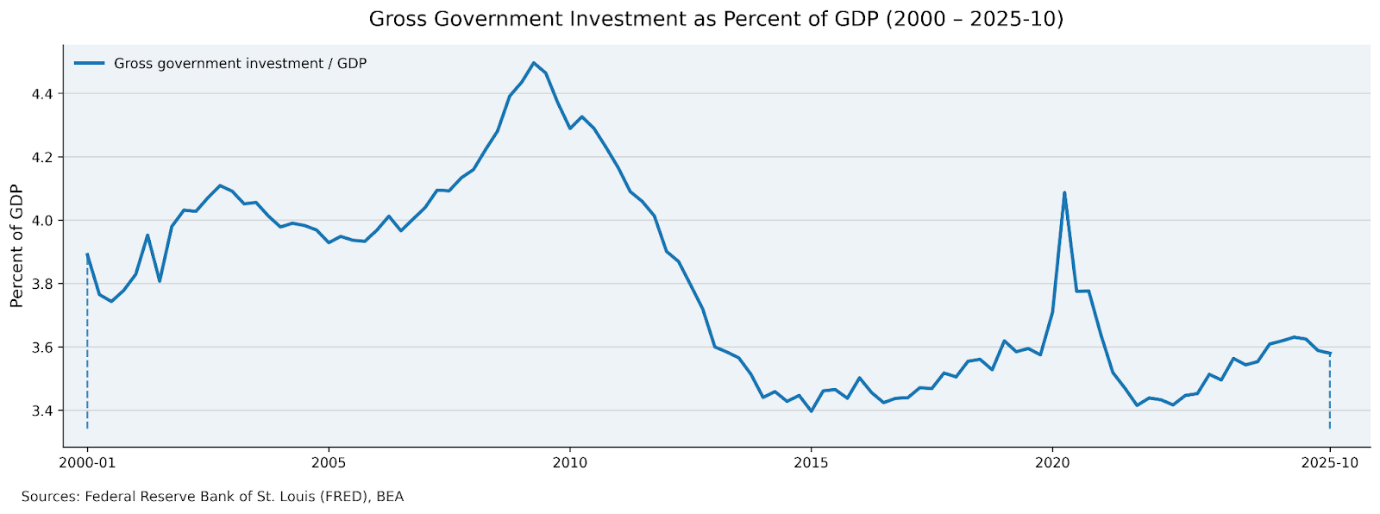

Figure 2: U.S. Public Investment Rate (Gross Government Investment / GDP)

Source: FRED, Gross Government Investment (A782RC1Q027SBEA); FRED, Gross Domestic Product (GDP)

The purpose of Figure 2 is to shift the discussion from the liability side back to the asset side. If Figure 1 shows that U.S. fiscal pressure is indeed real, then Figure 2 reminds us that fiscal discussion cannot stop at how to reduce deficits; it must also ask whether the country is continuing to build public assets. For the United States, this means that discussion of fiscal sustainability cannot revolve solely around “how much of the deficit should be cut.” It must also consider whether the country is addressing bottlenecks in its power system, transportation network, manufacturing infrastructure, and the foundational public assets and capabilities required in the age of AI. To speak only of austerity and not of asset building is to engage in an incomplete fiscal analysis.

This contrast becomes even more striking when set against the World Bank’s recent language. In 2026, the World Bank stated clearly that its advice on industrial policy from 30 years ago is “has not aged well,” and argued that industrial policy today “should be considered in the national policy toolkit of all countries.” At the same time, it emphasized that the problem is not that industrial policy itself is wrong, but that many governments have relied on crude tools while neglecting institutional capacity, transport and energy infrastructure, and macroeconomic fundamentals. The World Bank’s 2025 China Economic Update also made clear that China’s economy maintained growth momentum at the beginning of 2025, that policy support helped boost consumption, and that fiscal policy could partly offset downside pressure through higher infrastructure spending. In other words, compared with the IMF’s long-standing analytical habit of “look first at liabilities, speak first of austerity,” the World Bank now appears much more willing to openly acknowledge the role of industrial policy, policy support, and infrastructure building in growth and structural transformation. This does not mean that the World Bank has issued a final verdict endorsing Chinese industrial policy in a single sentence. But at the very least, its direction of discourse has already begun to diverge from the traditional IMF narrative.

What is truly concerning is not only theoretical bias, but the unequal standards the IMF itself applies across countries

The IMF’s problem is not only methodological narrowness. It is also inequality in political-economic standards. On this point, recent research has already provided strong evidence: since the 2008 global financial crisis, the intensity of fiscal consolidation demanded by the IMF has not changed significantly. The relaxations in 2009 and 2020 were both temporary, and statistically insignificant. More importantly, the countries that received relatively softer conditions were often those with closer ties to the IMF’s major shareholders, especially Western Europe and the United States. By contrast, countries with closer diplomatic relations with China often faced more severe IMF austerity requirements.

At the same time, Udaibir Das, in a 2026 article, points out that discussions of African debt have become increasingly sophisticated on the liability side, breaking debt down by size, maturity, currency denomination, spreads, creditors, restructuring mechanisms, and so on. Yet what gets treated as mere background is precisely the other side of the balance sheet: what the borrowed money actually built, and whether those investments strengthened a country’s future productive and repayment capacity. The current DSF mainly answers the creditor’s question: can this country repay? But it does not really answer the development question: has the borrowed financing been transformed into assets that can raise output, tax revenue, and resilience? Das even states bluntly that there is still no widely used “asset sustainability analysis” to match the existing tools for liability-side analysis.

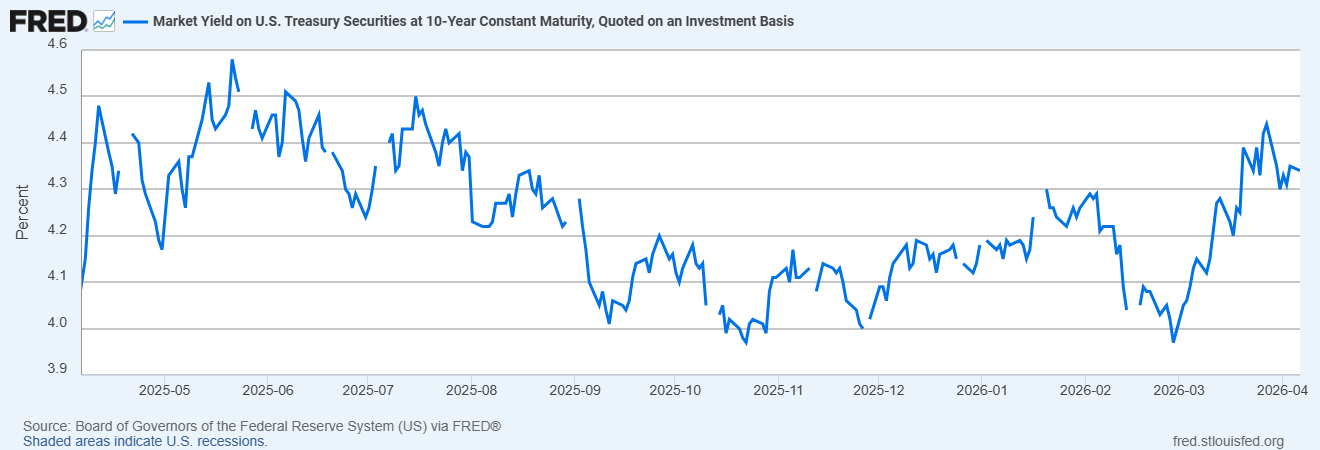

Figure 3. U.S. 10-year Treasury yield

Source: FRED, Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis (DGS10/GS10)

Figure 3 helps explain why the “debt narrative” has recently grown louder. As the 10-year Treasury yield rises, financing costs, interest payments, and market concerns about fiscal sustainability all increase, naturally reinforcing the policy impulse to “cut deficits first, control debt first.” But the real argument that Figure 3 supports is not that “therefore the IMF is right.” Rather, it is that rising yields do not mean we should retreat into the old framework of looking only at debt. On the contrary, changes in interest rates make it even more necessary to bring the asset side into the analysis as well, because interest rates affect not only the cost of debt but also the discounted present value of future returns on public assets. The reason the net-worth framework is superior is precisely that it reflects balance-sheet constraints on both sides more effectively than a simple debt ratio does.

There is also another direct point of comparison. In its April 2026 article on global imbalances, the IMF explicitly stated that global imbalances are ultimately driven mainly by domestic macroeconomic policy paths, rather than by tariffs or narrowly targeted industrial policies. It also identified the United States’ larger fiscal deficit and stronger domestic demand as major recent sources of widening global imbalances. The problem is not that the IMF is completely blind to U.S. problems. The problem is that when the IMF talks about the United States, its emphasis is more often on macroeconomic rebalancing, fiscal adjustment, and external imbalances; but when it talks about many African and other developing economies, the discussion is more easily compressed into debt burdens, financing gaps, and demands for austerity. On the question of how building public assets can improve future repayment capacity, it still has far too little to say.

If reform of the DSF continues to be delayed, the price will not be paid by African countries alone

What matters next is not simply to keep debating whether U.S. debt is too high, but to push for reform of the rules themselves. The more reasonable path is not to abandon fiscal discipline, but to transform fiscal discipline from a one-sided discipline focused on liabilities into a discipline accountable to both assets and liabilities. At a minimum, this means doing three things: distinguishing between investment debt and consumption debt; distinguishing between liquidity problems and solvency problems; and incorporating public assets, infrastructure, and long-term productive capacity into fiscal sustainability assessments. Only then can debt analysis avoid automatically sliding into anti-investment bias.

If such reform continues to be delayed, the most immediate consequence will be this: many developing countries will still be forced, under debt pressure, to cut public investment, infrastructure construction, and spending geared toward long-term growth, thereby further weakening their own future repayment capacity. At that point, what is treated today as “debt discipline” may tomorrow become a “penalty on growth.” By contrast, if the asset side is genuinely brought into the rules, the international community’s understanding of fiscal sustainability will shift from the one-sided logic of debt reduction to a more complete balance-sheet logic. This is important not only for African countries, but for the United States as well: the shortage of electricity has already become widely recognized as a bottleneck for AI development, urgently requiring investment from both the public and private sectors.

Conclusion: What truly needs to be broken is the mental cage of looking only at liabilities and not at assets

What makes this latest Treasury report an event worthy of serious attention is not only that it once again reminds the world that the pressure of U.S. fiscal unsustainability is intensifying. More importantly, it inadvertently reveals something even deeper: the United States understands itself through a balance sheet, while the IMF often understands others only through liability ratios.

This is one of the deepest blind spots in international debt governance today. Of course, a country’s fiscal sustainability must take debt and deficits into account. But it must never take debt and deficits alone into account. When governments face debt distress, they actually have two policy levers: one is fiscal adjustment, and the other is to build and revitalize public assets. The former is subtraction; the latter is addition. The former focuses on reducing the burden of the present; the latter focuses on expanding the repayment base of the future. The IMF’s biggest problem today is not that it cares about debt, but that it has become too accustomed to caring only about debt. Nor is the problem that it asks some countries to adjust their fiscal policies, but that it has not used the same full balance-sheet language to assess the United States, nor discussed the building of public assets with the same degree of seriousness. What truly needs to be broken is precisely this mental cage: the habit of looking at only one side of the balance sheet while ignoring the other.

Wang YanSenior academic researcher at Boston University Global Development Policy Center

Wang YanSenior academic researcher at Boston University Global Development Policy Center