Patient Capital, Long-Term Orientation, and Global Imbalances: a Rebuttal

Patient Capital, Long-Term Orientation, and Global Imbalances: a Rebuttal(The author is Yan Wang, a senior academic researcher at Boston University Global Development Policy Center.)

(Yicai) April 2 -- The global economy in early 2026 is confronted with an escalating war in the Middle East causing humanitarian disasters and energy crises. On the economic front, although there is a consensus that the 'global imbalance is widening,' solid evidence for the source of its sources is lacking.

In its ‘2025 Article IV consultation with China,' [1] completed in February 2026, the International Monetary Fund notes that the Chinese economy remains resilient overall, but its growth model is facing more pronounced internal and external imbalances. The IMF's core recommendation is to push China toward a more consumption-led growth model, reducing inefficient over-investment and precautionary savings through structural reforms.

Although the above assessment is not without merit, the narrative fails to address the other side of the global imbalances, namely the low savings rates and the extremely high fiscal deficits leading to rapid expansions of government debt in some of the G7 countries, especially the United States. Economists in China question the fairness of the IMF, blaming China for global imbalances.

For instance, 250 years of historical data provided by John Ross (2026) [2] validates that China's relatively high level of investment is not a sign of distortion or imbalance, but rather one of the main reasons the country has sustained rapid long-term growth.

In this short article, I provide a rebuttal to the IMF's critique of China's high savings rate by questioning whether it is desirable or realistic to reduce China's persistent high savings rate, rooted in the Chinese culture of long-term orientation (LTO), which constitutes part of China's soft power.

From the perspective of financing gaps for green development and building a resilient future, is it a good idea to lower China's savings rate? My friendly warning is: be careful what you wish for, and do not throw the baby out with the bathwater.

Patient Capital as a Comparative Advantage

Nine years ago, Justin Lin and I published a paper entitled 'New Structural Economics: Patient Capital as a Comparative Advantage' [3]. We pointed out that the IMF's promotion of capital account liberalization is misleading.

In fact, capital, just like labor, has never been homogeneous. Some capital is 'patient capital,' while other capital is highly mobile, or 'footloose,' that may leave a country at any time. Africa has been suffering from capital flight, about tens of billions of US dollars each year, according to Ndikumana and Boyce 2011.

We proposed a concept of 'patient capital that is dependent on the LTO of a country or region and the development of institutional investors in its banking and financial sector. We broadly defined 'patient capital' as the capital invested in a relationship in which the benevolent lender is willing to see the borrower growing up in the future to be able to provide decent returns, as in the cases of, for example, parents investing in children's education, state investment funds investing in innovative entities, and entrepreneurs investing in unlisted equity of infrastructure projects.

Those investors do not aim at the short-term returns but at the long-term future returns when the borrowers or invested projects scale up. Owners of patient capital are equity-like investors, and they are willing and better able to take risks.

Previous studies have attributed LTO to the pre-industrial agro-climatic characteristics that were conducive to higher returns in agricultural investment. It is a form of cultural endowment because it is rooted in the thousand-year history of agricultural development and Confucius' cultural background that values persistence, perseverance, thrift, and the ability to adapt and learn (Hofstede et al. 2010).

LTO has been widely considered as conducive to human and physical capital formation, technological advancement, and economic growth. For instance, the growth commission report found that "future orientation is related to high levels and effectiveness of savings and public and private investment" (Spence 2008, p.9).

However, LTO and savings are not the same as patient capital. Household savings for retirement, parents saving for their children's education, and residents building wealth for the future are all sources of long-term savings. But high saving rates alone are not enough. Institutions are crucial to activate the latent comparative advantage of high savings.

Only when a country develops financial institutions capable of transforming these savings into long-term capital can these savings truly become patient capital. In other words, a country may have an LTO and savings, which form a 'latent comparative advantage.' But only when banks, pension funds, sovereign wealth funds, and development finance institutions operate effectively does this latent advantage turn into a 'revealed' comparative advantage.

Nevertheless, the hard truth is that many developing countries often perform poorly when they adopt strategies that run counter to their comparative advantage. These strategies can lead to a nonviable business environment, fiscal burdens, inflation, financial repression, and external imbalances (Lin and Monga 2012) [5].

LTO and Net International Investment Positions

A key question, then, is which countries and regions have the LTO and can turn it into patient capital, and how to measure it?

Based on the work of Hofstede and his coauthors, we obtained the LTO index based on World Values Survey data collected by Misho Minkov (2007), Geert Hofstede, and his coauthors, and published in the book 'Cultures and Organizations: Software of the Mind,' pages 255-258 [4]. We also utilized another variable, the net international investment position (NIIP), as a proxy for a country's patient capital invested abroad, although it is not a comprehensive measure due to its focus on financial assets and liabilities.

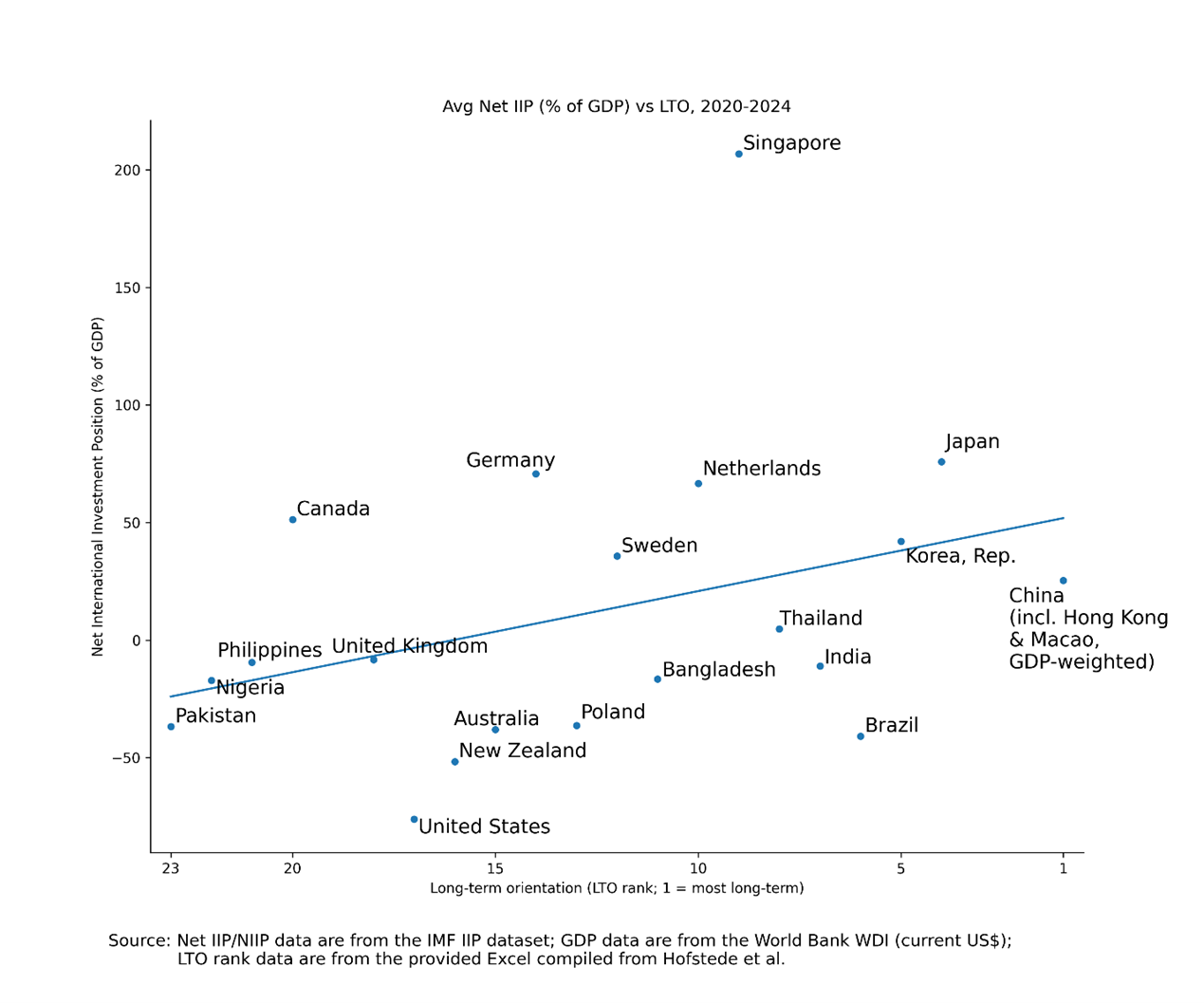

Figure 1: The relationship between NIIP as a percentage of the gross domestic product and LTO ranking, 2020-2024

A rough correlation analysis shows that the average NIIP in 2020-2024 is positively associated with the LTO index, as shown in Figure 1. That is, countries with stronger LTO, especially East Asian economies, are more likely to form a stronger net external creditor position. This is consistent with the Growth Commission work (Spence 2008); many of the East Asian economies, including Japan, South Korea, Taiwan, Hong Kong, China, and Singapore, possess similar characteristics of LTO.

Our hypothesis is that the NIIP of these economies may be higher than that of those without LTO. If this hypothesis can be further studied and corroborated by other evidence, such as Net foreign direct investment (outflows minus inflows) and cross-border mergers and acquisitions, we could consider that these economies have the revealed comparative advantage in patient capital as defined above.

On the other hand, countries with short-term orientation and low savings rates would see their NIIP, or net foreign assets positions, deteriorating and their foreign liabilities mounting, as shown by Mendoza et. al. (JPE, 2009) [5]. The US used to have a highly positive NIIP in the early 1980s, but by 1990, it became the world's largest debtor. By the end of the third quarter of 2025, the US net debtor position had deteriorated to about minus USD27 trillion, with USD41.27 trillion in assets and USD68.89 trillion in liabilities.

Mendoza and his coauthors argue that global financial imbalances (e.g., US current account deficits) result from integrating economies with differing financial development. Financially advanced nations run persistent deficits by importing capital, while less developed nations export it, yielding welfare gains for advanced nations.

China Is Utilizing Its Comparative Advantage in Patient Capital

The IMF mainly offers recommendations from the perspective of rebalancing and expanding consumption, but this line of thinking pays little attention to the deeper cultural and institutional foundations behind China's high savings rate.

China's high savings cannot be fully explained by the traditional determinants of precautionary saving and income factors, but they are deeply rooted in the cultural heritage of LTO, and institutional conditions for the creation of patient capital. The cultural explanation might seem slippery, but ultimately it is about how risk is perceived by individual households and by society as a whole.

In successive values surveys, China's LTO index has consistently ranked near the top (Hofstede, G. et al., 2010). It is precisely this LTO, together with institutional arrangements capable of transforming long-term savings into investment capacity, that has enabled China and some neighboring East Asian economies with a strong tradition of Confucianism to perform more strongly in infrastructure financing and long-term project investment than countries with weak long-term orientation.

We believe that the NIIP can serve as an important proxy for measuring a country's capacity to export capital. A positive NIIP shows that a country has obtained a relatively strong net external asset position. By contrast, countries with stronger short-term orientation and lower savings rates are more likely to face a deterioration in their external position and an accumulation of large amounts of external debt.

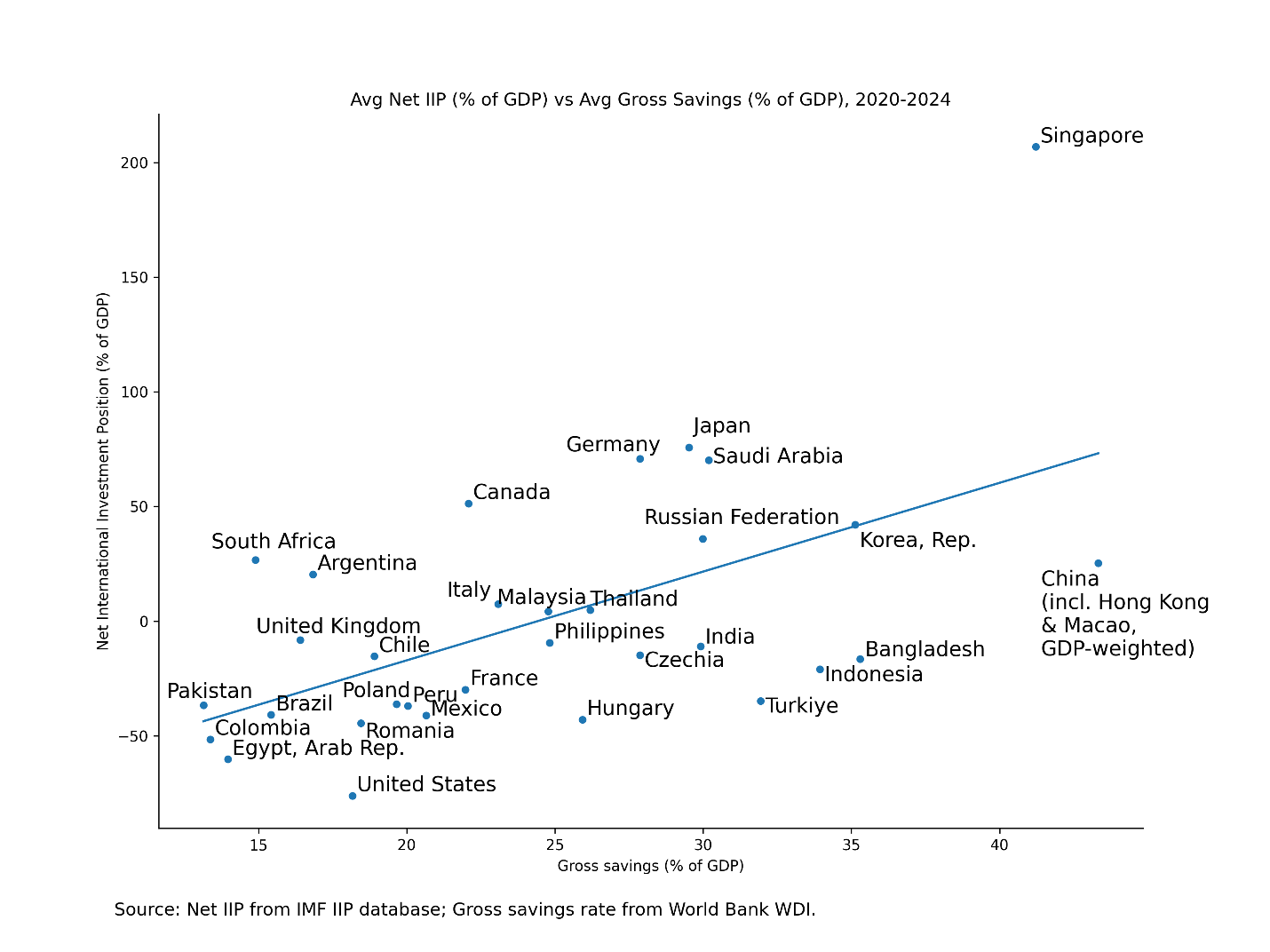

Figure 2: The relationship between NIIP as a percentage of the GDP and the average gross savings as a percentage of the GDP, 2020-2024 (Note: regression line: NIIP (% of GDP) = -94.539 + 3.871 Gross Saving (% of GDP) where p = 0.0007 < 0.05, therefore this linear relationship is statistically significant.)

As shown in Figure 2, the 2020-2024 data once again confirm that a high savings rate is highly correlated with a positive NIIP, and this relationship is positive and statistically significant. Although China is still a developing country, it has grown to be a major exporter of capital in recent years.

This phenomenon, called 'Lucas Paradox' (capital flowing from developing countries to developed countries), can be explained through long-term orientation: China possesses a kind of patience that the West often lacks -- that can be shown by the achievements under China's Five-Year Plans (the first one started in 1953 and the 15th in 2026). This patient capital can be utilized as a comparative advantage under certain institutional conditions, although further analysis is needed.

For China, rebalancing toward consumption may indeed be necessary, and establishing a more complete social security system may indeed help reduce excessive precautionary savings. In this process, however, the stronger capacity to patiently mobilize and invest long-term capital should be protected as a comparative advantage and a source of soft power that other Western countries lack. This capacity should not be weakened.

My warning is therefore a strategic one: policymakers should be cautious and avoid damaging the institutional conditions and cultural foundations that make patient capital possible.

Given the huge financing gaps to bridge the digital divide, advance green development, and combat climate change, more international long-term investment is needed. This is also the deeper meaning of my discussion on global imbalances: the international community, including the IMF, should hold major powers to higher standards to build bridges and global public assets, rather than destroying or discarding what is truly valuable in the course of rebalancing.

(The original version was published by the Boston University Global Development Policy Center. Please cite the original version dated 3/27/2026. Here https://www.bu.edu/gdp/2026/03/27/patient-capital-long-term-orientation-and-global-imbalances-a-rebuttal/ )

References

[1] IMF (2026). IMF Executive Board Concludes 2025 Article IV Consultation with China.

[2] Ross, John. 2026. 250年的历史数据说明:高水平投资才是中国经济的优势 ‘High level investment is the advantage of the Chinese economy based on 250 years of historic data (paper in Chinese).’

[3] Lin, J. Y., & Wang, Y. (2017), 'New Structural Economics: Patient Capital as a Comparative Advantage.' https://systems.enpress-publisher.com/index.php/jipd/article/view/28

[4] Hofstede, G., et al. (2010), 'Cultures and Organizations: Software of the Mind,' McGraw Hill, 2010, New York. https://www.google.com/books/edition/Cultures_and_Organizations_Software_of_t/o4OqTgV3V00C?hl=en

[5] Lin, Justin Yifu, Celestin Monga (2012) 'The Growth Report and New Structural Economics,' chapter II in Justin Yifu Lin, New Structural Economics: A Framework for Rethinking Development and Policy. The World Bank, Washington, D.C

[6] E. G. Mendoza, V. Quadrini, J. V. Ríos-Rull, 'Financial Integration, Financial Development and Global Imbalances,' Journal of Political Economy, volume 117, issue 3, p. 371 - 416, Posted: 2009.

Editor: Futura Costaglione

Wang YanSenior academic researcher at Boston University Global Development Policy Center

Wang YanSenior academic researcher at Boston University Global Development Policy Center